|

시장보고서

상품코드

1844640

전자 접착제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electronics Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

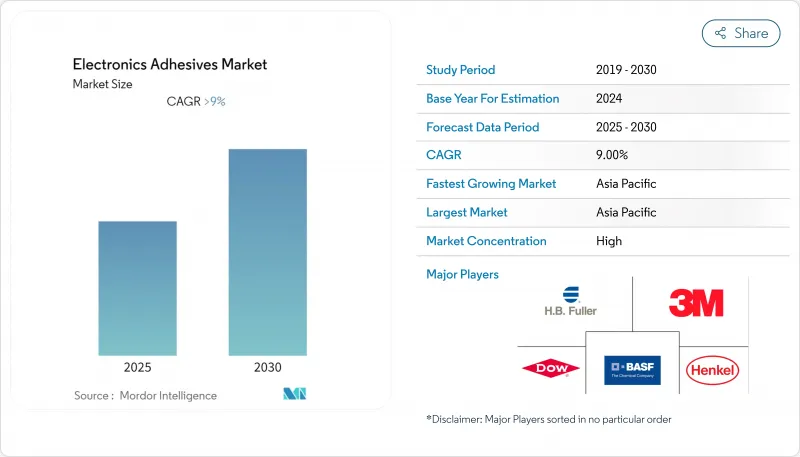

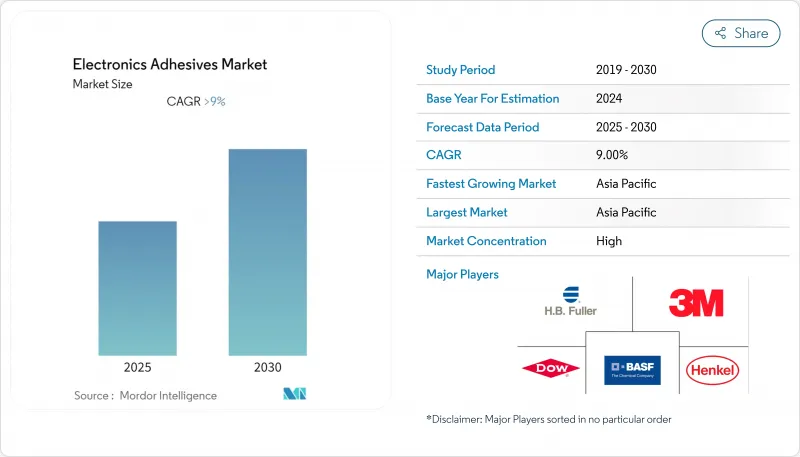

전자 접착제 시장 규모는 2025년에 65억 1,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 9.04%를 나타낼 것으로 예측되며, 2030년에는 100억 3,000만 달러에 이를 전망입니다.

부품 소형화의 가속화, 표면 실장 기술(SMT)의 광범위한 보급, 그리고 첨단 디스플레이의 급속한 채택이 이러한 진전을 이끄는 주요 동력입니다. 연결 부위 수를 늘리면서 열 부하를 증폭시키는 고밀도 패키징은 수요 모멘텀을 강화하며, 점차 소형화되는 장치 구조 사이에서 접착제가 필수적인 열적·기계적 완충재 역할을 하도록 합니다. 제조업체들은 또한 특히 아시아 계약 제조 허브를 중심으로 대량 생산 라인에서 사이클 시간을 단축하는 신속 경화 화학 물질을 우선시하고 있습니다. 동시에 지속가능성 규제로 인해 장기적 신뢰성을 저해하지 않는 PFAS 무첨가, 바이오 기반, 저휘발성 유기화합물(VOC) 제형으로의 전환이 촉진되고 있습니다. 종합하면, 이러한 주제들은 전자 접착제 시장이 양적 성장과 가치 중심 성장을 동시에 이루고 있으며, 높은 내열성과 광학적 순도가 요구되는 응용 분야에서 혁신적인 제품들이 시장 점유율 프리미엄을 확보하고 있음을 보여줍니다.

세계의 전자 접착제 시장 동향 및 인사이트

고밀도 패키징 급증

고밀도 패키징은 본드 라인을 마이크론 수준의 공차로 밀어붙여, 좁은 점도 범위, 제어된 가스 방출, 적층된 다이 간의 차동 팽창을 흡수하는 탄성 계수를 가진 접착제를 요구합니다. 웨이퍼 레벨 패키징(WLP)과 3D 통합은 접합부를 약 260°C 근처에서 정점에 달하는 리플로우 변동에 노출시키며, 이는 새로 개발된 에폭시-실록산 하이브리드 접착제가 충족하는 한계점입니다. DELO의 최신 웨이퍼 레벨 제품군은 정밀 제트 헤드에 적합한 유동성을 유지하면서 해당 온도를 견딥니다. 견고한 소재는 스마트폰을 넘어 첨단 운전자 보조 시스템(ADAS) 제어 장치와 소형 산업용 센서로 확대되었으며, 두 분야 모두 소비자 기기의 공간 제약을 반영합니다.

표면 실장 기술(SMT)용 접착제 수요 증가

SMT는 과거 비용 절감 역할을 수행했으나, 현재는 부품 간 간격이 솔더 페이스트 허용 오차를 하회하는 초미세 피치 조립을 가능케 합니다. 언더필 접착제는 플립칩 패키지의 열-기계적 응력을 재분배하고 주석 수염 전파를 차단하여 웨어러블 전자기기의 현장 고장률을 낮춥니다. 자동차 인포테인먼트 보드는 진동 감쇠 및 1,000시간 열순환 내구성에 대한 추가 요구사항을 더해 특수 에폭시-폴리이미드 블렌드 수요를 높입니다. 장비 제조사들은 고처리량 제트 디스펜서와 이중 단계 열/UV 경화 스테이션으로 대응하여 인라인 택트 타임을 최대 40% 단축함으로써 전자 접착제 시장 전반에 걸쳐 접착제 채택을 강화하고 있습니다.

에폭시 및 아크릴레이트 원료 가격 변동성

에피클로로히드린 공급 차질과 운임 할증료로 현물 에폭시 가격이 다년간 최고치를 기록하며 소규모 제형사의 총마진을 압박했습니다. 미국 국제무역위원회(ITC)의 특정 아시아산 에폭시 수입품에 대한 불허 결정으로 추가 관세가 부과되었고, 이는 몇 주 만에 계약 재협상으로 이어졌습니다. 복합재 등급 수지 생산업체들은 톤당 150-200유로의 가격 인상으로 대응하며 접착제 원가 기반을 직접적으로 상승시켰습니다. 최상위 공급업체들은 다년간 공급 계약을 통해 헤지하는 반면, 지역 전문업체들은 운영 자금 압박에 직면하여 혁신 속도가 둔화될 수 있습니다.

부문 분석

에폭시 수지는 전자 접착제 시장에서 2024년 매출의 30.19%를 차지하며 여전히 가장 중요한 위치를 유지했습니다. 높은 응집력, 절연 안정성, 가혹한 유체에 대한 내성 덕분에 자동차 엔진룸 내 모듈 및 산업용 드라이브에 깊숙이 자리 잡고 있습니다. 한편, 연평균 11.19% 성장률을 보이는 아크릴 화학 물질은 빛과 열을 이용한 빠른 경화 속도와 기판 유연성 향상이라는 특징을 제공하며, 이는 스마트폰 렌즈 스택 접합에 특히 유용합니다. 리그닌 및 식물성 오일 유도체를 활용한 바이오 기반 에폭시 개발은 260°C의 최고 온도 성능을 유지하면서 탄소 발자국을 줄이는 것을 목표로 합니다. 특수 조립 업체들 사이에서는 단일 제형으로 신속 경화 특성이 필요한 분야에서 하이브리드 에폭시-아크릴레이트 혼합물이 주목받고 있습니다. 기존 견고성과 신흥 유연성의 상호작용은 전자 접착제 시장을 주도하는 다양한 제형 로드맵을 강조합니다.

2차 폴리우레탄 시스템은 노면 충격에 노출되는 배터리 모듈과 같은 진동이 심한 환경을 해결하는 반면, 실리콘 및 시아노아크릴레이트 틈새 시장은 고온 전력 장치 및 신속한 고정 분야에서 지속되고 있습니다. 비스페놀-A 디글리시딜 에테르에 대한 규제적 관심이 에폭시 공급업체들을 대체 단량체로 유도하고 있으나, 장기적 수요 기반은 여전히 견고합니다. 제조사들은 -55°C에서 175°C까지 작동 범위를 확장하는 독자적 강화제를 통해 차별화를 지속하며, 아크릴계 제품의 판매량이 증가하는 상황에서도 에폭시의 주도적 위치를 공고히 하고 있습니다.

전기 전도성 등급은 2024년 매출의 43.90%를 차지하며, 솔더 공극이 회로 연속성을 위협하는 모든 곳에서 필수적임을 입증했습니다. 은박 에폭시는 플립칩 다이 부착 분야에서 우위를 점하고 있으며, 니켈 함유 제품은 5G 안테나용 비용 효율적인 전자기 간섭(EMI) 차폐 기능을 제공합니다. 연평균 복합 성장률(CAGR) 12.04%로 성장 중인 UV 경화 접착제는 라인 택트 타임을 초 단위로 단축하고 현장 광학 검사를 가능케 하여 카메라 모듈 공장의 1차 통과 수율을 높인다. 질화 알루미늄 또는 질화 붕소 충전재가 함유된 열전도성 변형 제품은 최대 5W/mK의 열을 방출하여 LED 루멘 유지율과 인버터 가동 시간을 연장합니다.

비전도성 구조용 에폭시는 고전압 트레이스와의 절연이 필수적인 분야, 특히 견인 인버터 및 데이터센터 전원 공급 장치에서 수요를 유지하고 있습니다. UV 사전 겔링과 열 후경화를 결합한 하이브리드 이중 경화 제품은 복잡한 3차원 조립체에 대한 최적의 선택지로 부상하고 있습니다. 현재 이용 가능한 다양한 성능 프로파일은 전자 접착제 시장을 강화하여 설계자가 전기적, 열적, 광학적 매개변수를 동시에 최적화할 수 있는 유연성을 제공합니다.

지역 분석

아시아태평양 지역은 2024년 매출의 58.69%를 차지하며 전자 접착제 시장의 단일 최대 지역 기둥으로 자리매김했습니다. 중국 본토는 첨단 패키징 라인에 대한 국가 보조금과 현지 웨이퍼 레벨 언더필 생산 능력 확장을 통해 2024년 전자 제품 생산량을 11.3% 증가시켰습니다. 태국과 베트남은 2025년 4월부터 미국이 전자제품 수입에 대해 선별적 관세 면제를 시행함에 따라 새로운 외국인 직접 투자를 유치하며 조립 프로그램을 아세안(ASEAN) 클러스터로 전환시켰습니다. 수지 반응기부터 완전 자동화 SMT 라인에 이르는 이 지역의 통합 공급망은 리드 타임을 단축하고 비용 경쟁력을 강화합니다.

북미의 리쇼어링(reshoring) 움직임은 국내 웨이퍼 제조에 520억 달러를 배정하는 'CHIPS and Science Act'를 통해 가속화되고 있습니다. 이러한 상류 부문 자본 투자는 클린룸 등급 언더필 및 액체 열전도성 재료에 대한 하류 접착제 수요를 자극하고 있습니다. 캐나다 퀘벡 회랑 역시 바이오 기반 화학 물질을 우선시하는 신규 인쇄전자 파일럿 플랜트를 유치하며 유럽에서 관찰되는 지속가능성 추진을 반영하고 있습니다.

유럽은 자체 EU 칩스 법안이 지역 마이크로전자 가치 사슬을 강화함에 따라 전자 접착제 시장 규모 회복을 도모 중입니다. 진보적인 PFAS 제한을 포함한 환경 규제는 불소 무함유 윤활성 충전재에 대한 연구개발을 촉진하고 있습니다. 독일의 자동차 1차 공급업체들은 대시보드 디스플레이용 분리 가능 등급을 인증 중이며, 스칸디나비아 EMS 공급업체들은 에너지 발자국 축소를 위해 저온 경화 기술을 강조하고 있습니다.

남미와 중동 및 아프리카는 신흥 시장으로 부상하고 있습니다. 브라질 마나우스 자유무역지대는 소비자 전자제품 조립을 확대하며 열대 습도에 맞춤화된 중간 점도 아크릴 접착제의 기회를 열고 있습니다. 아랍에미리트(UAE)는 자유무역지대 인센티브와 AI 중심 R&D 단지를 결합해 지역 물류 허브로 자리매김하며 현지 접착제 혼합 공장 설립의 발판을 마련 중입니다. 현재 규모는 작지만, 이러한 지역들은 기존 생산 중심지 내 집중 위험을 분산하려는 기업들에게 다각화 가능성을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고밀도 패키징 수요 급증

- 접착제가 필요한 표면 실장 기술(SMT) 수요 증가

- 미니 LED 및 마이크로 LED 백라이트 채택 확대

- 전자 접착제 기술 발전 가속화

- 가전 생산 확대

- 시장 성장 억제요인

- 에폭시 및 아크릴레이트 원료 가격 변동성

- 엄격한 VOC 및 RoHS/REACH 규정 준수 비용

- 초박형 유연 기판의 열적 불일치 결함

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 수지 유형별

- 에폭시

- 아크릴

- 폴리우레탄

- 기타 수지 유형(실리콘, 시아노아크릴레이트 등)

- 제품 유형별

- 전도성

- 열 전도성

- UV 경화

- 기타 제품 유형(비전도성 등)

- 용도별

- 컨포멀 코팅

- 표면 실장

- 캡슐화

- 와이어 태킹

- 기타 용도(언더필, 다이 부착)

- 최종 사용자 산업별

- 소비자용 하드웨어

- IT 하드웨어

- 자동차

- 기타 최종 사용자 산업(산업, 파워 전자 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Arkema

- Avery Dennison

- BASF

- DELO

- Dow

- Dymax Corporation

- HB Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC.

- ITW Engineered Polymers

- Master Bond Inc.

- NAMICS CORPORATION

- Panacol-Elosol GmbH

- Parker Hannifin Corp

- Permabond LLC

- Pidilite Industries Ltd.

- Shin-Etsu Chemical Co., Ltd.

제7장 시장 기회와 전망

HBR 25.11.07The Electronics Adhesives Market size is estimated at USD 6.51 billion in 2025, and is expected to reach USD 10.03 billion by 2030, at a CAGR of 9.04% during the forecast period (2025-2030).

Rising component miniaturization, wider surface-mount technology (SMT) penetration, and rapid adoption of advanced displays are the primary forces guiding this progress. Demand momentum is reinforced by high-density packaging that increases interconnect counts while amplifying thermal loads, positioning adhesives as indispensable thermal and mechanical buffers between ever-smaller device features. Manufacturers are also prioritizing fast-curing chemistries that cut cycle times in high-volume lines, especially across Asian contract manufacturing hubs. At the same time, sustainability regulations are prompting shifts toward PFAS-free, bio-based, and low-VOC formulations that do not compromise long-term reliability. Taken together, these themes illustrate an electronics adhesives market whose growth is both volume-driven and value-driven, with innovative products commanding share premiums in applications requiring elevated heat resistance and optical purity.

Global Electronics Adhesives Market Trends and Insights

Surge in High-Density Packaging

High-density packaging pushes bond lines toward micron-level tolerances, demanding adhesives with tight-viscosity windows, controlled outgassing, and elastic moduli that absorb differential expansion among stacked die. Wafer-level packaging (WLP) and 3D integration expose joints to reflow excursions that peak near 260 °C, a threshold met by newly formulated epoxy-siloxane hybrids. DELO's latest wafer-level range sustains that temperature while maintaining flow behavior suitable for precision jetting heads. Robust materials have broadened beyond smartphones into advanced driver-assistance systems (ADAS) control units and compact industrial sensors, both of which mirror consumer device space constraints.

Increase in Demand for Surface-Mount Technology Requiring Adhesives

SMT once filled cost-reduction roles but now enables ultra-fine-pitch assembly where component clearances fall below solder paste tolerances. Underfill adhesives redistribute thermo-mechanical stress in flip-chip packages and arrest tin-whisker propagation, cutting field-failure rates in wearable electronics. Automotive infotainment boards add further requirements for vibration damping and 1,000-hour thermal-cycling durability, elevating demand for specialty epoxy-polyimide blends. Equipment makers respond with high-throughput jet dispensers and dual-stage thermal/UV curing stations that shrink in-line takt times by up to 40%, reinforcing adhesive uptake throughout the electronics adhesives market.

Volatility in Epoxy and Acrylate Feedstock Prices

Epichlorohydrin supply disruptions and freight surcharges pushed spot epoxy prices to multi-year highs, crimping gross margins for small formulators. The U.S. International Trade Commission's ruling against certain Asian epoxy imports introduced additional tariffs that filtered into contract renegotiations within weeks. Composite-grade resin producers responded with EUR 150-200 per-ton price hikes, directly raising adhesive cost bases. While top-tier vendors hedge via multi-year supply deals, regional specialists face working-capital strain that may curb innovation pace.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Mini-LED and Micro-LED Backlighting Adoption

- Growing Technological Advancements in Electronic Adhesives

- Stringent VOC and RoHS/REACH Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy resins remained paramount, accounting for 30.19% of 2024 revenue within the electronics adhesives market. Their high cohesive strength, dielectric stability, and resistance to harsh fluids keep them entrenched in under-the-hood automotive modules and industrial drives. Meanwhile, acrylic chemistries, expanding at an 11.19% CAGR, offer faster light-plus-heat curing and greater substrate flexibility, features prized by smartphone lens-stack bonding. Bio-based epoxy initiatives, leveraging lignin and vegetable-oil derivatives, aim to cut carbon footprints without sacrificing 260 °C peak-temperature capability. Across specialty assembly houses, hybrid epoxy-acrylate blends are gaining traction where manufacturers need snap-cure attributes in a single formulation. This interplay of legacy robustness and emerging agility underscores the diverse formulation roadmap powering the electronics adhesives market.

Second-tier polyurethane systems address vibration-rich settings such as battery modules that face road-surface shocks, whereas silicone and cyanoacrylate niches persist for high-temperature power devices and rapid fixturing. Regulatory attention on bisphenol-A diglycidyl ether is nudging epoxy suppliers toward alternative monomers, yet long-term demand fundamentals remain intact. Manufacturers continue to differentiate through proprietary toughening agents that widen operating windows from -55 °C to 175 °C, thereby cementing epoxy's leadership even as acrylic volumes accelerate.

Electrically conductive grades delivered 43.90% of 2024 sales, proving indispensable wherever solder voids threaten circuit continuity. Silver-flake epoxies dominate flip-chip die-attach, while nickel-loaded versions offer cost-effective EMI shielding for 5G antennas. UV-curing adhesives, scaling at a 12.04% CAGR, compress line tact times to seconds and enable in-situ optical inspection, elevating first-pass yields in camera module factories. Thermally conductive variants, infused with aluminum nitride or boron nitride fillers, dissipate up to 5 W/mK, extending LED lumen maintenance and inverter uptime.

Non-conductive structural epoxies sustain demand where isolation from high-voltage traces is non-negotiable, notably in traction inverters and data-center power supplies. Hybrid dual-cure products that combine UV pre-gelling with thermal post-cure are emerging as the go-to option for complex three-dimensional assemblies. The breadth of performance profiles available today strengthens the electronics adhesives market, giving designers latitude to optimize electrical, thermal, and optical parameters simultaneously.

The Electronics Adhesives Market Report is Segmented by Resin Type (Epoxy, Acrylic, and More), Product Type (Electrically Conductive, Thermally Conductive, and More), Application (Conformal Coating, Surface Mounting, and More), End-User Industry (Consumer Hardware, IT Hardware, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 58.69% of 2024 revenue, making it the single largest regional pillar of the electronics adhesives market. Mainland China raised electronics output by 11.3% in 2024 through state grants for advanced packaging lines and local wafer-level underfill capacity expansions. Thailand and Vietnam absorbed fresh foreign direct investment after the United States granted selected tariff exemptions on electronics imports from April 2025, redirecting assembly programs into ASEAN clusters. The region's integrated supply base-from resin reactors to fully automated SMT lines-compresses lead times and reinforces its cost leadership.

North America's reshoring narrative gained momentum via the CHIPS and Science Act, which allocates USD 52 billion toward domestic wafer fabrication. This upstream capital outlay is stimulating downstream adhesive demand for clean-room-grade underfills and liquid thermal interface materials. Canada's Quebec corridor likewise hosts new printed-electronics pilot plants that prioritize bio-based chemistries, mirroring sustainability pushes seen in Europe.

Europe is charting an electronics adhesives market size rebound as its own EU Chips Act strengthens local microelectronic value chains. Environmental regulations, including progressive PFAS limitations, are galvanizing R&D into fluorine-free lubricious fillers. Germany's automotive Tier 1s are qualifying debondable grades for dashboard displays, while Scandinavian EMS providers emphasize low-temperature curing to shrink energy footprints.

South America and the Middle East and Africa represent emerging frontiers. Brazil's Manaus free-trade zone is broadening consumer-electronic assembly, opening opportunities for mid-viscosity acrylics tailored to tropical humidity. The United Arab Emirates is positioning itself as a regional logistics hub, pairing free-zone incentives with AI-centered R&D parks that could seed localized adhesive blending plants. Though smaller today, these geographies add diversification prospects for firms eager to de-risk concentration within traditional production centers.

- 3M

- Arkema

- Avery Dennison

- BASF

- DELO

- Dow

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC.

- ITW Engineered Polymers

- Master Bond Inc.

- NAMICS CORPORATION

- Panacol-Elosol GmbH

- Parker Hannifin Corp

- Permabond LLC

- Pidilite Industries Ltd.

- Shin-Etsu Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in High-Density Packaging Demand

- 4.2.2 Increase in Demand for Surface Mount Technology requiring Adhesives

- 4.2.3 Increasing Mini-LED and Micro-LED Backlighting Adoption

- 4.2.4 Growing Technological Advancements in Electronic Adhesives

- 4.2.5 Expansion of Consumer Electronics Production

- 4.3 Market Restraints

- 4.3.1 Volatility in Epoxy and Acrylate Feedstock Prices

- 4.3.2 Stringent VOC and RoHS/REACH Compliance Costs

- 4.3.3 Thermal-Mismatch Failures in Ultra-Thin Flexible Substrates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Polyurethane

- 5.1.4 Other Resin Types (Silicone, Cyanoacrylate, etc.)

- 5.2 By Product Type

- 5.2.1 Electrically Conductive

- 5.2.2 Thermally Conductive

- 5.2.3 UV Curing

- 5.2.4 Other Product Types (Non-conductive, etc.)

- 5.3 By Application

- 5.3.1 Conformal Coating

- 5.3.2 Surface Mounting

- 5.3.3 Encapsulation

- 5.3.4 Wire Tacking

- 5.3.5 Other Applications (Underfill, Die-Attach)

- 5.4 By End-user Industry

- 5.4.1 Consumer Hardware

- 5.4.2 IT Hardware

- 5.4.3 Automotive

- 5.4.4 Other End-user Industries (Industrial and Power Electronics, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison

- 6.4.4 BASF

- 6.4.5 DELO

- 6.4.6 Dow

- 6.4.7 Dymax Corporation

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG and Co. KGaA

- 6.4.10 Huntsman International LLC.

- 6.4.11 ITW Engineered Polymers

- 6.4.12 Master Bond Inc.

- 6.4.13 NAMICS CORPORATION

- 6.4.14 Panacol-Elosol GmbH

- 6.4.15 Parker Hannifin Corp

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Shin-Etsu Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment