|

시장보고서

상품코드

1844645

북미의 시아노아크릴레이트 접착제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)North America Cyanoacrylate Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

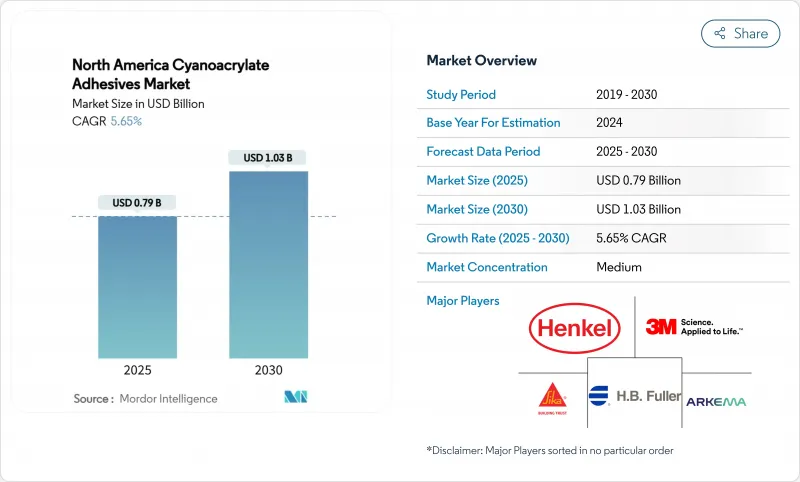

북미의 시아노아크릴레이트 접착제 시장 규모는 2025년에 7억 9,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 5.65%를 나타낼 것으로 예측되며, 2030년에는 10억 3,000만 달러에 달할 전망입니다.

이러한 전망은 많은 특수 화학 제품들이 가격 압박과 강화된 환경 규제로 어려움을 겪는 가운데 접착제 부문이 성장할 수 있는 역량을 부각시킵니다. 전자제품의 지속적인 소형화, 의료 기기 혁신, 운송 분야의 경량화 프로그램이 수요를 뒷받침하고 있습니다. 용매 기반 화학물질을 제한하는 규제 움직임은 구매자들을 즉시 경화형 대체재로 유도하고 있으며, 공급망이 최종 시장 가까이로 이동함에 따라 북미와 멕시코의 생산 거점이 유리해지고 있습니다. 경쟁은 제형 속도, 생체 적합성 및 지속 가능성에 집중되며, 글로벌 규모와 응용 분야별 노하우를 결합한 기업들이 계속해서 시장 점유율을 확보하고 있습니다.

북미의 시아노아크릴레이트 접착제 시장 동향 및 인사이트

소형화된 소비자 전자제품 조립 수요 급증

기기의 급속한 소형화로 제조업체들은 나사와 클립을 포기하고 저점도 시아노아크릴레이트를 채택하고 있습니다. 이 접착제는 마이크론 단위의 틈새로 흘러 들어가 몇 초 내에 경화되어 섬세한 기판을 변형시킬 수 있는 추가 열 사이클을 제거합니다. 첨단 칩 패키징에서의 이종 통합은 접착제가 다중 재료 스택을 고정하면서 전도 경로를 차단해야 하므로 성장을 가속화합니다. 웨어러블 기기, IoT 센서, 자동차 인포테인먼트 모듈도 동일한 제약 조건을 적용하며 글로벌 수요를 확대하고 있습니다. OEM 업체들은 최소한의 표면 처리만으로 플라스틱, 금속, 복합재를 접합할 수 있는 이 접착제의 화학적 특성을 높이 평가하며, 아시아 지역의 대량 생산 공장에서 생산 효율을 극대화하고 있습니다. 그 결과 프리미엄급 시아노아크릴레이트 접착제가 모든 신세대 스마트 기기에 지속적으로 적용되고 있습니다.

의료기기 접착제 및 상처 봉합 분야의 급속한 채택

의료용 시아노아크릴레이트는 더 빠른 시술 시간, 작은 흉터, 감염률 감소 덕분에 봉합사를 대체하고 있습니다. Dermabond Prineo 메쉬 시스템은 다기관 임상시험에서 수술 후 합병증을 두 자릿수 비율로 감소시켰습니다. 장쇄 부틸 및 옥틸 변형체는 조직 독성이 낮고 체액 하에서도 인장 강도를 유지하여 내부 및 외부 적용에 대한 승인을 촉진하고 있습니다. H.B. 풀러의 메디필 인수 및 진행 중인 GEM 거래는 유럽 공급망을 확장하며, 공급업체들이 엄격한 ISO 10993 및 FDA 기준을 충족하기 위해 경쟁하는 모습을 보여줍니다. 고령화 인구 증가와 함께 전 세계 수술 건수가 증가함에 따라, 병원들은 교육 간소화와 회복 기간 단축을 위해 일회용 조직 접착제로 계속 전환하고 있어 의료 수요가 다른 모든 분야를 앞지르고 있습니다.

엄격한 VOC 규제 및 노동 위생 규제

EPA 에어로졸 코팅 제한, 캐나다의 130개 제품군 VOC 상한선, 호주의 독성학 연구 초안 결과로 인해 제형 개발사들은 용매를 제거하고 경고 라벨을 추가해야 하며, 이로 인해 소규모 생산자의 경우 매출의 최대 12%에 달하는 규정 준수 비용이 증가합니다. 개선된 환기 시스템, 개인 보호 장비, 의무적인 작업장 모니터링은 선진 지역의 운영 비용을 더욱 부풀립니다. 저취 제품 라인이 주목받지만, 종종 마진을 압박하는 고가의 안정제가 필요합니다. 전담 규제 팀을 보유한 다국적 기업들은 이러한 부담을 흡수하지만, 소규모 지역 브랜드들은 퇴출 또는 인수 위험에 직면하여 업계 통합을 촉진하고 있습니다.

부문 분석

에틸 에스터 기반 제형은 수십 년에 걸친 공정 최적화를 통해 저비용과 광범위한 기질 호환성을 제공함으로써 2024년 시아노아크릴레이트 접착제 시장 규모에서 47.18%라는 압도적인 점유율을 유지했습니다. 전자 부품 하위 어셈블리 및 자동차 하네스 시장으로의 판매가 높은 생산량을 유지하고 있으며, 안티블룸 첨가제와 같은 점진적 개선을 통해 경쟁력을 유지하고 있습니다. 동시에 바이오 기반 또는 특수 등급을 묶은 “기타 제품 유형”은 기업의 기후 약속과 차별화된 성능을 추구하는 최종 사용자의 요구를 반영하여 2030년까지 연평균 6.69%의 성장률을 보일 것으로 예상됩니다.

마이크로 본딩 속도가 최종 강도를 앞서는 분야에서는 메틸 에스터 등급에 대한 관심이 지속되나, 충격이 많은 플라스틱용 더 강력한 본딩을 추구하는 엔지니어들로 인해 물량은 감소합니다. 알콕시 에틸 변형체는 틈새 시장이지만 120°C 이상의 주기적 열안정성을 요구하는 프로젝트에서 우위를 점합니다. 대학 연구실에서는 박리 강도가 24% 향상된 에톡시에틸 알파-시아노아크릴레이트 제조 경로를 발표 중이며, 이는 경제성 확보 시 잠재적 파괴적 진입자가 등장할 수 있음을 시사합니다. 예측 기간 동안 공급업체들은 조달 평가 기준에 대응하여 기존 에틸 에스터 생산량과 고마진 친환경 또는 고온 제품군을 균형 있게 조합해 포트폴리오를 다각화할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소형화된 소비자 가전 제품 조립 수요 급증

- 의료 기기 접착제 및 상처 봉합 분야에서의 신속한 채택

- 자동차 및 전기 이동 수단의 경량화 추진

- DIY 및 소비자의 수리문화 확대

- 가구 산업에서의 수요 증가

- 시장 성장 억제요인

- 휘발성 유기 화합물(VOC) 및 직업 건강 관련 엄격한 규제

- 대체재 대비 제한된 전단 저항성 또는 내열성

- 원유 가격 변동성

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 알콕시 에틸계

- 에틸에스테르계

- 메틸 에스테르계

- 기타 제품 유형(바이오 기반 등)

- 최종 사용자 산업별

- 운송

- 신발 및 가죽

- 가구

- 소비재

- 헬스케어

- 전자

- 기타 최종 사용자 산업(섬유, 해양 등)

- 지역별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%) 랭킹 분석

- 기업 프로파일

- 3M

- Arkema

- Aron Alpha

- Chemence

- DELO

- Dymax

- HB Fuller Company

- Henkel AG and Co. KGaA

- Hernon Manufacturing

- ITW Performance Polymers

- Master Bond Inc.

- Permabond LLC

- Sika AG

제7장 시장 기회와 전망

HBR 25.11.07The North America Cyanoacrylate Adhesives Market size is estimated at USD 0.79 billion in 2025, and is expected to reach USD 1.03 billion by 2030, at a CAGR of 5.65% during the forecast period (2025-2030).

This outlook underscores the adhesive sector's ability to grow even as many specialty chemicals struggle with price pressures and stricter environmental rules. Robust electronics miniaturization, medical device innovation and lightweighting programs in transportation underpin demand. Regulatory moves that restrict solvent-based chemistries are steering buyers toward instant-curing alternatives, while supply-chain shifts closer to end-markets favour production hubs in North America and Mexico. Competition centres on formulation speed, biocompatibility and sustainability, and firms that combine global scale with application-specific know-how continue to capture share.

North America Cyanoacrylate Adhesives Market Trends and Insights

Surging Demand from Miniaturised Consumer-Electronics Assembly

Rapid device shrinkage forces manufacturers to abandon screws and clips in favour of low-viscosity cyanoacrylates that flow into micron-scale gaps and cure within seconds, eliminating added heat cycles that can warp delicate substrates. Growth is amplified by heterogeneous integration in advanced chip packaging, where adhesives must secure multi-material stacks while preventing conductive pathways. Wearables, IoT sensors and automotive infotainment modules replicate these constraints, extending the driver's global reach. OEMs value the chemistry's ability to bond plastics, metals and composites with minimal surface preparation, streamlining throughput in high-volume Asian plants. The result is consistent pull-through of premium-grade cyanoacrylates into every new generation of smart devices.

Rapid Adoption in Medical Device Adhesives and Wound Closure

Medical-grade cyanoacrylates are gaining on sutures thanks to faster procedure times, smaller scars and reduced infection rates; the Dermabond Prineo mesh system cut post-operative complications by double-digit margins in multi-centre trials. Long-chain butyl and octyl variants show lower tissue toxicity and maintain tensile strength under bodily fluids, fostering approvals for internal and external applications. H.B. Fuller's acquisition of Medifill and pending GEM deal expands European supply, illustrating how suppliers race to clear strict ISO 10993 and FDA hurdles. As global surgical volumes rise alongside ageing populations, hospitals continue switching to single-use tissue adhesives that simplify training and shorten recovery, pushing healthcare demand above all other sectors.

Strict VOC and Occupational-Health Regulations

EPA aerosol-coating limits, Canada's VOC caps on 130 product categories and Australia's draft toxicology findings compel formulators to strip out solvents and add warning labels, raising compliance costs by up to 12% of sales for small producers . Upgraded ventilation, personal protective equipment and mandatory workplace monitoring further inflate operating expenses in developed regions. While low-odour lines gain traction, they often require costly stabilizers that squeeze margins. Multinationals with dedicated regulatory teams absorb these burdens, but smaller regional brands risk exit or acquisition, nudging sector consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Initiatives in Automotive and E-Mobility

- Expanding DIY and Consumer Repair Culture

- Limited Shear or Thermal Resistance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethyl Ester-based formulations retained a commanding 47.18% share of the cyanoacrylate adhesives market size in 2024, buoyed by decades of process optimization that deliver low cost and broad substrate compatibility. Sales into electronics sub-assemblies and automotive harnesses keep throughput high, and incremental tweaks-such as anti-bloom additives-preserve competitiveness. In parallel, "Other Product Types" that bundle bio-based or specialty grades are set to climb at a 6.69% CAGR through 2030, reflecting corporate climate pledges and end-user quests for differentiated performance.

Renewed interest in Methyl Ester grades persists where micro-bonding speed outranks final strength, yet volume dips as engineers chase tougher bonds for impact-laden plastics. Alkoxy Ethyl variants, while niche, win projects demanding cyclic thermal stability beyond 120 °C. University labs are publishing routes to ethoxyethyl a-cyanoacrylate with 24% higher peel strength, signalling potential disruptive entrants should scale economics line up. Over the forecast horizon, suppliers will likely hedge portfolios by balancing legacy Ethyl Ester tonnage with high-margin green or high-temperature offerings in response to procurement scorecards.

The North America Cyanoacrylate Adhesive Market Report Segments the Industry by Product Type (Alkoxy Ethyl-Based, Ethyl Ester-Based, Methyl Ester-Based, and Other Product Types), End-User Industry (Transportation, Footwear and Leather, Furniture, Consumer Goods, Healthcare, Electronics, and Other End-User Industries), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Aron Alpha

- Chemence

- DELO

- Dymax

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Hernon Manufacturing

- ITW Performance Polymers

- Master Bond Inc.

- Permabond LLC

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from miniaturised consumer-electronics assembly

- 4.2.2 Rapid adoption in medical device adhesives and wound closure

- 4.2.3 Lightweighting initiatives in automotive and e-mobility

- 4.2.4 Expanding Do-It-Yourself (DIY) and consumer repair culture

- 4.2.5 Growing demand from furniture industry

- 4.3 Market Restraints

- 4.3.1 Strict Volatile Organic Compound (VOC) and occupational-health regulations

- 4.3.2 Limited shear or thermal resistance in comparison to alternatives

- 4.3.3 Peedstock price-volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Alkoxy Ethyl-based

- 5.1.2 Ethyl Ester-based

- 5.1.3 Methyl Ester-based

- 5.1.4 Other Product Types (Bio-based, etc.)

- 5.2 By End-user Industry

- 5.2.1 Transportation

- 5.2.2 Footwear and Leather

- 5.2.3 Furniture

- 5.2.4 Consumer Goods

- 5.2.5 Healthcare

- 5.2.6 Electronics

- 5.2.7 Other End-user Industries (Textile, Marine, etc.)

- 5.3 By Geography

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Aron Alpha

- 6.4.4 Chemence

- 6.4.5 DELO

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG and Co. KGaA

- 6.4.9 Hernon Manufacturing

- 6.4.10 ITW Performance Polymers

- 6.4.11 Master Bond Inc.

- 6.4.12 Permabond LLC

- 6.4.13 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 The Development of Bio-based Adhesives