|

시장보고서

상품코드

1844652

자기 충전 콘크리트(SCC) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Self-Consolidating Concrete (SCC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

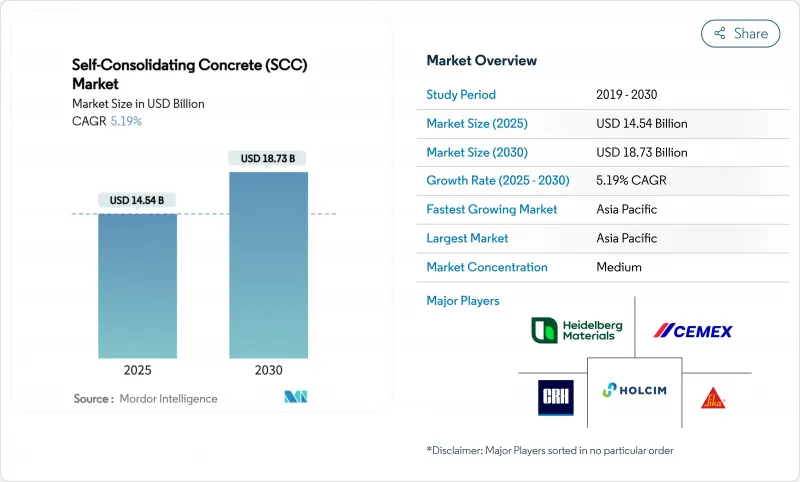

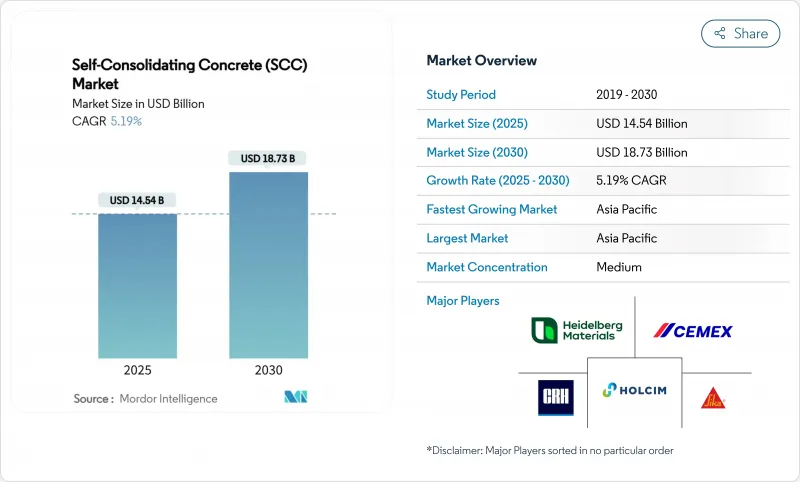

자기 충전 콘크리트(SCC) 시장 규모는 2025년에 145억 4,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 5.19%를 나타낼 것으로 예측되며, 2030년에는 187억 3,000만 달러에 달할 전망입니다.

시산업체들이 기계적 진동 없이 복잡한 철근 케이지를 캐스팅해야 하는 수요가 견고하게 발생하고 있으며, 이는 강화되는 노동 규정 및 자동화 목표와 부합합니다. 특히 북미와 유럽에서 내재 탄소 배출을 억제하라는 규제 압박은 보충성 시멘트질 재료가 풍부한 혼합물로의 전환을 가속화합니다. 기존 혼합제 제조사들은 폴리카르복실레이트 화학을 활용해 낮은 물-결합제 비율에서도 유동성을 향상시키고 있으며, 디지털 모니터링 플랫폼은 시멘트 함량을 줄이는 데 도움이 되는 실시간 강도 데이터를 제공합니다. 이러한 요소들은 종합적으로 성능 향상, 노동 강도 감소, 지속가능성 요구사항이 모두 자기 충전 콘크리트 시장에 유리하게 작용하는 선순환 구조를 강화합니다.

세계의 자기 충전 콘크리트(SCC) 시장 동향 및 인사이트

프리캐스트 및 현장 작업에서의 노동력 절감 배치

만성적인 숙련공 부족으로 건설사들은 진동 없이 시공하는 방식을 채택하게 되었으며, 이는 사이클 시간을 최대 73% 단축하고 더 적은 인원으로 작업할 수 있게 합니다. 프리캐스트 공장은 섬유보강 자가다짐 혼합물을 도입할 경우 28%의 생산성 향상을 기록하며, 이 수치는 현재 북미와 일본 전역에서 관찰되고 있습니다. 재료비가 15-25% 비싸더라도 빠른 작업 속도로 기존 콘크리트 대비 비용 경쟁력을 확보합니다. 특히 철근이 밀집된 구역에서 진동이 비실용적이거나 물리적으로 불가능할 때 이점은 배가되어, 자가밀결 콘크리트 시장은 고층 건물 및 교량 공사의 핵심으로 부상하고 있습니다.

저탄소 SCM(슬래그/비산회) 풍부 혼합물 수요

뉴욕주의 주 차원 “Buy Clean” 규정은 공공 프로젝트에 공급되는 콘크리트의 내재 탄소 상한선을 강제하여, 생산자들이 자연스럽게 유동성 혼합물과 결합되는 높은 슬래그 및 비산회 함량을 채택하도록 유도합니다. 캘리포니아 CALGreen 규정과 프랑스 RE2020 프레임워크의 유사한 기준은 제1종 혼합물 대비 30-50% CO2 감축을 달성하는 배합에 가격 프리미엄을 부여합니다. 현대적 폴리카르복실레이트 초고감수제는 클링커 비율 감소 시에도 요구되는 유동성을 유지하여, 자기 충전 콘크리트 시장을 단순 노동력 해결책이 아닌 지속가능성 도구로 공고히 합니다.

높은 혼합 설계 및 재료 비용 프리미엄

기존 콘크리트 대비 15-25%의 비용 차이는 임금이 낮고 프로젝트 소유주가 프리미엄 가격 책정을 거부하는 지역에서 여전히 장애물로 작용합니다. 적절히 등급이 분류된 골재와 수입 혼합제의 필요성은 동남아시아 및 라틴 아메리카 일부 지역에서 비용을 부풀려, 명백한 노동력 절감 효과에도 불구하고 자기 충전 콘크리트 시장 성장을 저해합니다. 시공사는 초기 비용과 후속 효율성 사이의 균형을 맞춰야 하므로 소규모 작업에서의 도입이 제한됩니다.

부문 분석

시멘트는 2024년 자기 충전 콘크리트(SCC) 시장의 37.18%를 차지했으며, 이는 성장 모멘텀보다는 구조적 규모에 기인한 선두 지위입니다. 혼합제는 현재 7.18%의 연평균 복합 성장률(CAGR)을 기록 중이며, 이는 유동성을 저하시키지 않으면서도 0.30에 가까운 물-결합제 비율을 가능케 하는 4세대 폴리카르복실레이트 에테르의 급속한 채택에 힘입은 것입니다. 점도 조절제와 결합된 이 화학 물질들은 더 높은 SCM 대체 수준을 가능케 하여 생산자들이 강화되는 CO2 배출 제한을 준수하는 데 도움을 줍니다. 골재는 가치 기준으로 2위를 차지하며, 최소 수두 압력 하에서 막힘 현상을 완화하기 위해 박리성이 낮은 간격 등급 석재에 대한 수요가 증가하고 있습니다. 생산자들이 시멘트 톤수보다 성능을 중시함에 따라 구성 요소 혼합은 화학적 최적화 쪽으로 기울어져 있으며, 이는 글로벌 주요 기업들이 혼합제 분야에서 R&D 제휴 및 인수를 우선시하는 이유를 강조합니다.

SCM 통합으로의 전환은 공급업체 계층 구조를 재편하고 있습니다. 석탄 발전 감소로 서구 시장에서 플라이애시 공급이 불안정해지면서 소성 점토와 분쇄 유리 포졸란에 대한 관심이 높아지고 있습니다. 프리캐스트 적용 분야에서는 섬유 첨가가 증가하며, 진동 없는 주조 공정에 보완되는 균열 제어 기능을 제공합니다. SikaGrind-400은 클링커 요인이 감소할 때 표적 연마제가 초기 강도를 어떻게 향상시켜 자기 충전 콘크리트 시장 접근성을 확대하는지 보여줍니다. 시멘트 생산자들은 시장 점유율 유지를 위해 저탄소 바인더를 자체 혼합제 라인과 묶어 판매하며 대응하고 있으며, 이는 향후 경쟁 우위가 원자재 톤수보다 통합 화학 솔루션에 더 크게 좌우될 것임을 시사합니다.

지역 분석

아시아태평양 지역은 2024년 글로벌 매출의 49.55%를 차지했으며, 막대한 인프라 투자와 심각한 노동력 부족을 반영하여 7.45%의 연평균 성장률(CAGR)로 확장될 것으로 예상됩니다. 중국의 고속철도 고가교와 인도의 스마트시티 프로그램은 고밀도 철근 케이지에 진동 없는 콘크리트를 정기적으로 지정합니다. 일본의 초과근무 법안은 현장 작업 시간을 제한하여 프리캐스트 야드와 현장 캐스팅 작업 모두에서 자동화 배합의 사업성을 강화합니다. 북미는 가치 기준으로 2위를 차지하며, 양당 합의 인프라 지출은 뉴욕의 내재 탄소 상한선과 부합하는 교량 데크 및 고속도로 재활 기회를 창출합니다.

유럽은 성숙하면서도 혁신적인 시장으로 남아 있습니다. 프랑스의 RE2020 탄소상승한계와 아일랜드의 클링커 감축 의무는 SCM(지속가능 콘크리트) 채택을 가속화하여 혼합제 수요를 촉진합니다. 중동·아프리카 및 남미는 기반이 작지만 기술 서비스 네트워크가 확장되고 초대형 프로젝트가 증가함에 따라 관심이 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 프리캐스트 및 현장 캐스팅 작업에서의 노동력 절감 배치

- 저탄소, SCM 풍부 혼합물에 대한 수요 가속화

- 자동/로봇 캐스팅 라인의 급증

- 복잡한 고층 및 초대형 인프라에서의 채택

- 정부의 친환경 건축 의무화

- 시장 성장 억제요인

- 높은 혼합 설계 및 재료 비용 프리미엄

- 신흥 지역의 한정된 현장 노하우

- 품질 변동성을 유발하는 혼합제 민감도

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 성분별

- 시멘트

- 골재

- 혼합제 및 첨가제

- 기타 성분

- 용도별

- 프리캐스트 콘크리트 제품

- 건축 요소

- 주택 구조물

- 인프라(다리, 터널 등)

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BASF

- Breedon Group plc

- Cemex SAB de CV

- CRH

- GCP Applied Technologies

- Heidelberg Materials

- Holcim

- Saint-Gobain

- Sika AG

- Tarmac Ltd.

- UltraTech Cement Ltd.

- Unibeton Ready Mix

- Vicat Group

제7장 시장 기회와 전망

HBR 25.11.07The Self-Consolidating Concrete Market size is estimated at USD 14.54 billion in 2025, and is expected to reach USD 18.73 billion by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

Robust demand arises from contractors' need to pour intricate reinforcement cages without mechanical vibration, a requirement that lines up with tightening labor regulations and automation goals. Regulatory pressure to curb embodied carbon, especially in North America and Europe, accelerates the shift toward supplementary-cementitious-material-rich mixes. Established admixture producers leverage polycarboxylate chemistry to enhance flow at lower water-binder ratios, while digital monitoring platforms provide real-time strength data that helps reduce cement content. Collectively, these factors reinforce a virtuous cycle in which better performance, lower labor intensity and sustainability mandates all favor the self-consolidating concrete market.

Global Self-Consolidating Concrete (SCC) Market Trends and Insights

Labor-saving placement in precast and in-situ works

Chronic craft-worker shortages prompt builders to adopt vibration-free placement methods that cut cycle times by up to 73% and permit leaner crew sizes. Precast plants record 28% productivity gains when integrating fiber-reinforced self-consolidating mixes, a figure now observable across North America and Japan. Faster turnarounds yield cost parity against conventional concrete despite a 15-25% materials premium. The benefit multiplies on congested rebars where vibration is either impractical or physically impossible, placing the self-consolidating concrete market at the center of high-rise and bridge work.

Demand for low-carbon SCM-rich mixes

State-level "Buy Clean" rules in New York enforce embodied-carbon ceilings for concrete supplied to public projects, pushing producers toward high slag and fly-ash dosages that pair naturally with flowable mixes. Similar thresholds under California's CALGreen code and France's RE2020 framework create a price premium for formulations that deliver 30-50% CO2 cuts relative to Type I blends. Modern polycarboxylate superplasticizers sustain required flow at reduced clinker factors, reinforcing the self-consolidating concrete market as a sustainability lever rather than just a labor solution.

High mix-design & material cost premium

A 15-25% cost delta over conventional concrete remains a headwind wherever wages are low and project owners resist premium pricing. The need for well-graded aggregates and imported admixtures can inflate costs in Southeast Asia and parts of Latin America, dampening self-consolidating concrete market growth despite clear labor savings. Contractors must balance up-front expense against downstream efficiencies, limiting uptake in small-scale jobs.

Other drivers and restraints analyzed in the detailed report include:

- Surge in automated robotic casting lines

- Adoption in complex high-rise and mega-infrastructure

- Limited field know-how in emerging regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cement accounted for 37.18% of the self-consolidating concrete market in 2024, a lead attributable to structural volume rather than growth momentum. Admixtures now post a 7.18% CAGR, underpinned by the rapid uptake of fourth-generation polycarboxylate ethers that enable water-binder ratios near 0.30 without sacrificing flow. Paired with viscosity modifiers, these chemistries unlock higher SCM replacement levels that help producers comply with tightening CO2 caps. Aggregates rank second by value; demand intensifies for gap-graded stone with low flakiness to mitigate blocking under minimal head pressure. The constituent mix tilts toward chemical optimization as producers emphasize performance over cement tonnage, underscoring why global majors prioritize R&D alliances and acquisitions in the admixture space.

The pivot toward SCM integration reshapes supplier hierarchies. Fly-ash availability remains volatile in Western markets due to declining coal power, spurring interest in calcined clay and ground-glass pozzolans. Fiber additions grow in precast applications, offering crack control that complements vibration-free casting. SikaGrind-400 illustrates how targeted grinding aids elevate early strength when clinker factors drop, widening the addressable self-consolidating concrete market. Cement producers counter by bundling low-carbon binders with in-house admixture lines to retain share, signaling that future competitive advantage depends less on raw tonnage and more on integrated chemical solutions.

The Self-Consolidating Concrete Market Report is Segmented by Constituent (Cement, Aggregates, Admixtures & Additives, Other Constituents), Application (Precast Concrete Products, Architectural Elements, Residential Structures, Infrastructure, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 49.55% of global revenue in 2024 and is projected to expand at a 7.45% CAGR, reflecting massive infrastructure outlays coupled with acute labor shortages. China's high-speed-rail viaducts and India's smart-cities program routinely specify vibration-free concrete for dense reinforcement cages. Japan's overtime legislation caps site hours, strengthening the business case for automated placement in both precast yards and cast-in-place work. North America ranks second by value; bipartisan infrastructure spending unlocks bridge-deck and highway rehabilitation opportunities that align with New York's embodied-carbon caps.

Europe remains a mature yet innovative arena. Embodied-carbon ceilings under RE2020 in France and Ireland's clinker-reduction mandate accelerate SCM adoption, thereby boosting admixture demand. Middle East & Africa and South America start from smaller bases but display rising interest as technical service networks expand and megaprojects proliferate.

- BASF

- Breedon Group plc

- Cemex SAB de CV

- CRH

- GCP Applied Technologies

- Heidelberg Materials

- Holcim

- Saint-Gobain

- Sika AG

- Tarmac Ltd.

- UltraTech Cement Ltd.

- Unibeton Ready Mix

- Vicat Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor-saving placement in precast and in-situ works

- 4.2.2 Accelerating demand for low-carbon, SCM-rich mixes

- 4.2.3 Surge in automated/robotic casting lines

- 4.2.4 Adoption in complex, high-rise & mega-infrastructure

- 4.2.5 Government green-building mandates

- 4.3 Market Restraints

- 4.3.1 High mix-design & material cost premium

- 4.3.2 Limited field know-how in emerging regions

- 4.3.3 Admixture-sensitivity causing quality variability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Constituent

- 5.1.1 Cement

- 5.1.2 Aggregates

- 5.1.3 Admixtures and Additives

- 5.1.4 Other Constituents

- 5.2 By Application

- 5.2.1 Precast Concrete Products

- 5.2.2 Architectural Elements

- 5.2.3 Residential Structures

- 5.2.4 Infrastructure (Bridges, Tunnels, etc.)

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Breedon Group plc

- 6.4.3 Cemex SAB de CV

- 6.4.4 CRH

- 6.4.5 GCP Applied Technologies

- 6.4.6 Heidelberg Materials

- 6.4.7 Holcim

- 6.4.8 Saint-Gobain

- 6.4.9 Sika AG

- 6.4.10 Tarmac Ltd.

- 6.4.11 UltraTech Cement Ltd.

- 6.4.12 Unibeton Ready Mix

- 6.4.13 Vicat Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment