|

시장보고서

상품코드

1844661

바이오알코올 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bio-alcohols - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

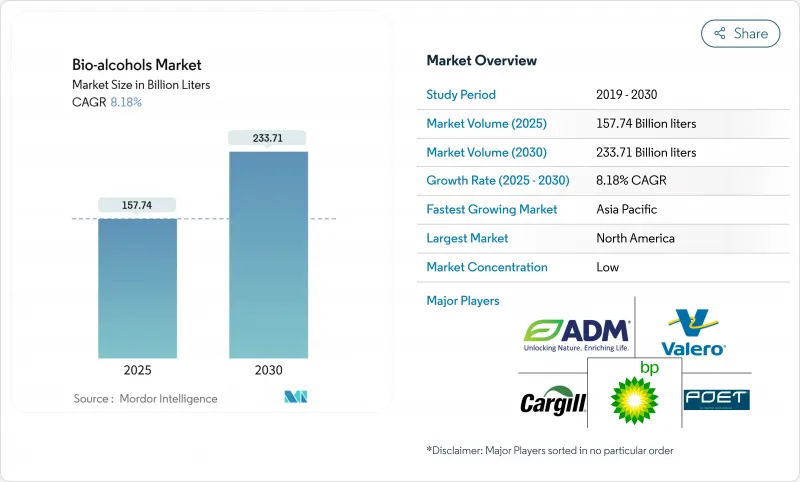

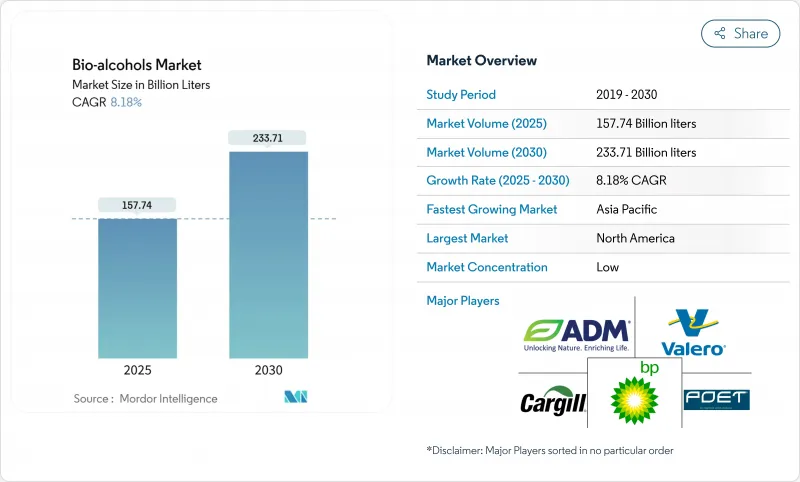

바이오알코올 시장 규모는 2025년에 1,577억 4,000만 리터로 평가되었고, 2030년에는 2,337억 1,000만 리터에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 8.18%를 나타낼 전망입니다.

이러한 성장은 재생 가능 연료 규제의 강화, 알코올-항공유 전환 인증의 신속한 진전, 정유사에 새로운 수익원을 제공하면서 배출량을 줄이는 상업용 탄소 포집-알코올 전환 시스템의 등장 등을 반영합니다. 지속 가능한 해상 연료 공급망, 소비재의 고급 화학 용도, 저탄소 공급망에 대한 투자자의 강한 관심 또한 수요 구조를 재편하고 있습니다. 기존 북미 생산업체들은 규모의 경제 우위를 유지하고 있으나, 아시아태평양 지역은 정책적 지원과 비용 최적화 기술 덕분에 생산 능력을 더 빠르게 확대하고 있습니다. 특히 조류 및 산업 부산 가스를 활용한 원료 혁신은 농산물 가격 변동과 연계된 마진 위험을 완화하는 데 기여하고 있으며, 항공사 및 해운사와의 전략적 공급 계약은 투자자들에게 현금 흐름의 명확성을 제공합니다.

세계의 바이오알코올 시장 동향 및 인사이트

의무적 에탄올 혼합 목표

혼합 의무화는 수요를 보장하고 투자자 위험을 줄이며 공장 확장을 가속화합니다. 이미 20%를 달성한 인도의 2030년까지 30% 혼합 목표는 야심찬 정책이 창출할 수 있는 상승 여력을 보여줍니다. EU의 ReFuelEU 항공 규정은 2025년 2% SAF(지속가능 항공 연료)로 시작해 2050년까지 70%로 증가하며, 알코올-제트 연료 프로젝트에 명확한 성장 경로를 제공합니다. 브라질의 E27 프로그램은 물류 장벽이 완화되면 높은 혼합 비율의 모델로 남을 전망입니다. 의무화 정책이 원자재 가격 변동으로부터 물량을 보호하므로 생산자는 장기 원료 공급 계약을 체결하고 자금 조달 비용을 낮출 수 있습니다.

알코올-제트 연료 경로의 신속한 항공 SAF 인증

항산업계의 탄소중립 추진으로 알코올-제트 연료 경로 시험이 급속히 가속화되고 있습니다. 조지아에 위치한 란자제트(LanzaJet)의 프리덤 파인스 퓨얼스(Freedom Pines Fuels) 공장은 이미 연간 900만 갤런을 생산하며 대규모 플랜트의 안정적 가동에 대한 금융계의 신뢰를 확보했습니다. 악센스(Axens)의 제타놀(Jetanol) 프로젝트는 현재 연간 10억 갤런 이상의 계획 생산 능력을 보유하며 해당 기술의 금융적 실행 가능성을 입증하고 있습니다. SAF는 기존 제트 연료보다 2-3배 비싼 가격에 판매되는 경우가 많아, 바이오에탄올 생산사들은 항공 고객으로 전환할 때 더 큰 마진을 누릴 수 있습니다. 사우스웨스트 항공과 USA 바이오에너지 간의 계약과 같은 장기 항공사 구매 계약은 프로젝트 현금 흐름의 위험을 더욱 낮춥니다.

고농도 알코올 혼합에 대한 파이프라인 호환성 부족

대부분의 석유 파이프라인은 부식 및 수분 흡수로 인해 고농도 알코올 혼합물을 처리할 수 없어 트럭이나 철도에 의존해야 합니다. 추가 물류 비용은 특히 혼합 터미널에서 멀리 떨어진 지역에서 납품 가격 경쟁력을 약화시킵니다. 파이프라인 업그레이드는 다수 소유주 간 협력이 필요하며, 일부 시장에서는 아직 정당화하기 어려운 높은 자본 투자가 필요합니다.

부문 분석

바이오에탄올은 성숙한 플랜트, 표준화된 사양, 지원 정책에 힘입어 2024년 바이오 알코올 시장 점유율 68.05%를 유지했습니다. 변환 비용 우위와 글로벌 공급망이 주도적 위치를 공고히 합니다. 바이오에탄올 시장 규모는 휘발유 소비량이 정점에 달하더라도 전국적 혼합 의무량 증가로 절대량이 확대됨에 따라 꾸준히 성장할 전망입니다. 반면 바이오부탄올은 우수한 에너지 밀도와 즉시 대체 가능성으로 9.40%의 연평균 복합 성장률(CAGR)과 프리미엄 화학 수요 점유율 상승을 이끌고 있습니다.

알코올-제트 연료 전환 기술의 돌파구는 에탄올에 고부가가치 출구를 제공합니다. 란자젯(LanzaJet)의 초기 운영 데이터는 저비용 농업용 에탄올을 2-3배 가격 배수로 판매되는 지속가능 항공연료(SAF)로 업그레이드 가능함을 입증했습니다. 한편 바이오 메탄올은 선박 연료 및 플라스틱 시장에서 입지를 다지고 있으며, 바이오 BDO는 제약 및 공학 소재 틈새 시장을 공략 중입니다. 종합적으로 특수 알코올은 바이오알코올 시장의 다각화를 이끌며 도로 연료 수요 변동에 대한 민감도를 완화합니다.

본 바이오알코올 시장 보고서는 제품 유형(바이오메탄올, 바이오에탄올, 바이오부탄올, 바이오BDO 등), 원료(전분 기반 작물, 당류 기반 작물, 리그노셀룰로오스 바이오매스 등), 응용 분야(운송, 건설, 전자 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 전망은 용량(리터) 기준으로 제공됩니다.

지역별 분석

북미의 2024년 점유율 39.44%는 밀집된 옥수수-에탄올 공급망, 풍부한 철도 물류, 그리고 기준 생산량을 유지하는 재생 가능 연료 기준(RFS)을 반영합니다. 캐나다의 2025년 청정 연료 규제는 미국을 넘어 저탄소 혼합 연료 수요를 확대합니다. 멕시코의 신규 밀 가공 공장 투자는 대륙을 상호 보완적 공급망으로 연결합니다. 서밋 넥스트 젠의 16억 달러 규모 텍사스 에탄올-SAF 복합 시설(JETI 보조금 대상)은 지역 보조금이 연방 세액 공제와 연계되어 초대형 프로젝트를 유치하는 방식을 보여줍니다.

아시아태평양 지역은 성장 엔진으로, 인도의 30% 혼합 가속화 정책과 사상 최대 쌀 원료 수요에 힘입어 연평균 9.55% 성장률을 기록 중입니다. 중국은 2060 탄소중립 계획과 연계된 CO2-to-알코올 시범사업 자금 지원을 통해 추진력을 더하고, 일본과 한국은 정유소 및 공항을 대상으로 녹색 연료 인센티브를 집중하고 있습니다. 필리핀을 포함한 아세안 시장도 혼합 규정을 강화하며 지역 수요를 광범위하게 유지하고 있습니다. 이러한 정책적 상승세는 현지 원료와 수입 기술을 결합하는 합작 투자를 유치해 생산 능력 확장을 가속화합니다.

유럽은 엄격한 탄소 가격 책정과 지속가능 항공연료 의무화 정책으로 프리미엄 틈새시장을 촉진합니다. ReFuelEU 규정집은 투자자들에게 향후 SAF 확대 계획에 대한 명확성을 제공하며, 독일과 영국은 국내 생산을 보장하기 위해 국가 보조금을 운영 중입니다. 사탕무와 폐기물 바이오매스를 포함한 원료 유연성은 공급 충격 완화에 기여합니다. 남미는 저렴한 사탕수수와 바가스를 처리하는 첨단 2세대 제분소를 지속적으로 활용해 적자 지역에 꾸준한 수출 흐름을 유지하고 있습니다. 중동과 아프리카는 규모는 작지만 다각화 전략의 일환으로 시범 프로젝트를 추진 중입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의무화된 에탄올 혼합 목표

- 알코올-제트 연료 전환 경로의 신속한 항공용 지속가능한 항공유(SAF) 인증

- 정유소 내 이산화탄소 포집·저장(CCU) 설비와 알코올 생산 시설의 통합

- 소비재(CPG) 산업에서 저탄소 화학 원료로서의 바이오알코올 활용

- 신흥 메탄올 추진 해상 운송 노선

- 시장 성장 억제요인

- 원료 가격 변동성

- 고농도 알코올 혼합에 대한 파이프라인 호환성 부족

- 2027년 이후 정체된 글로벌 경차량 생산

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측(수량)

- 제품 유형별

- 바이오메탄올

- 바이오에탄올

- 바이오부탄올

- 바이오BDO

- 기타 바이오알코올

- 원료별

- 전분 기반 작물

- 당류 기반 작물

- 리그노셀룰로오스 바이오매스

- 조류 바이오 매스

- 산업폐기물

- 용도별

- 운송

- 건설

- 전자

- 의약품

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Abengoa

- ADM

- BASF SE

- BP plc

- Cargill Incorporated

- CropEnergies AG

- Gevo

- Green Plains Inc.

- INEOS

- Mascoma LLC

- POET LLC

- Raizen

- SEKISUI CHEMICAL CO., LTD.

- Valero Energy Corporation

제7장 시장 기회와 전망

HBR 25.11.07The Bio-alcohols Market size is estimated at 157.74 billion liters in 2025, and is expected to reach 233.71 billion liters by 2030, at a CAGR of 8.18% during the forecast period (2025-2030).

This growth reflects tightening renewable-fuel rules, quick progress in alcohol-to-jet certification, and the arrival of commercial carbon-capture-to-alcohol systems that give refiners fresh revenue while cutting emissions. Demand is also being reshaped by sustainable marine-fuel corridors, premium chemical uses in consumer goods, and stronger investor appetite for low-carbon supply chains. Established North American producers keep scale advantages, yet Asia-Pacific is adding capacity faster thanks to policy tailwinds and cost-optimized technologies. Feedstock innovation, especially with algae and industrial off-gases, is helping moderate margin risks linked to crop price swings, while strategic offtake deals with airlines and shippers give investors cash-flow clarity.

Global Bio-alcohols Market Trends and Insights

Mandated Ethanol-Blend Targets

Blend mandates guarantee demand, reduce investor risk, and speed plant expansions. India's goal of 30% blending by 2030, having already reached 20%, shows the upside that ambitious policy can unlock. The EU's ReFuelEU Aviation rule starts with 2% SAF in 2025 and rises to 70% by 2050, offering a clear runway for alcohol-to-jet projects. Brazil's E27 program remains a template for high blend ratios once logistics barriers ease. Because mandates shield volumes from commodity swings, producers can line up long-term feedstock contracts and lower financing costs.

Rapid Airline SAF Certification of Alcohol-to-Jet Pathways

Aviation's net-zero push has sharply accelerated testing of alcohol-to-jet routes. LanzaJet's Freedom Pines Fuels site in Georgia already makes 9 million gallons a year and gives financiers confidence that large plants will run reliably. Axens' Jetanol projects now top 1 billion gallons per year of planned capacity, underlining the technology's bankability. SAF often sells at two to three times the price of conventional jet fuel, so bio-ethanol producers enjoy wider margins when they pivot toward aviation customers. Long-term airline offtake deals, such as Southwest's agreement with USA BioEnergy, further derisk project cash flows.

Insufficient Pipeline Compatibility for High-Blend Alcohols

Most petroleum pipelines cannot handle high alcohol blends due to corrosion and water uptake, forcing reliance on truck or rail. The extra logistics cost erodes delivered-price competitiveness, especially in regions far from blending terminals. Upgrading lines needs cooperation between many owners and warrants high capital that some markets cannot justify yet.

Other drivers and restraints analyzed in the detailed report include:

- Integration of CO2-to-Alcohol CCU Plants at Refineries

- Bio-Alcohol as Low-Carbon Chemical Feedstock in CPG

- Stagnant Global Light-Vehicle Production Post-2027

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bio-ethanol kept a 68.05% 2024 Bio-alcohol market share, underpinned by mature plants, standardized specs, and supportive mandates. Its conversion cost edge and global supply chain reinforce leadership. The Bio-alcohol market size for bio-ethanol is expected to expand steadily in line with nationwide blend limits that increase absolute volume even as gasoline peaks. Yet bio-butanol's superior energy density and drop-in compatibility are propelling its 9.40% CAGR and a rising slice of premium chemical demand.

Alcohol-to-jet breakthroughs provide a higher-value outlet for ethanol. LanzaJet's early operating data confirm that low-cost agricultural ethanol can be upgraded into SAF that sells at a 2-3X price multiple. Meanwhile, bio-methanol is carving room in marine fuels and plastics, and bio-BDO caters to pharmaceutical and engineered-material niches. Collectively, specialty alcohols diversify the Bio-alcohol market and lessen sensitivity to road-fuel swings.

The Bio-Alcohol Market Report is Segmented by Product Type (Bio-Methanol, Bio-Ethanol, Bio-Butanol, Bio-BDO, and More), Feedstock (Starch-Based Crops, Sugar-Based Crops, Lignocellulosic Biomass, and More), Application (Transportation, Construction, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

Geography Analysis

North America's 39.44% 2024 share mirrors its dense corn-to-ethanol corridor, ample rail logistics, and the Renewable Fuel Standard that keeps baseline volumes. Canada's 2025 Clean Fuel Regulation widens demand for low-carbon blends beyond the United States. Mexico's new mill investments knit the continent into a self-reinforcing supply chain. Summit Next Gen's USD 1.6 billion Texas ethanol-to-SAF complex, eligible for JETI subsidies, underlines how local grants align with federal tax credits to lure mega-projects.

Asia-Pacific is the growth engine, tracking a 9.55% CAGR on the back of India's fast-tracked 30% blend agenda and record rice-feedstock pull. China adds momentum by funding CO2-to-alcohol pilots that dovetail with its 2060 neutrality plan, while Japan and South Korea channel green-fuel incentives at refineries and airports. ASEAN markets, including the Philippines, are lifting blending rules too, keeping regional demand broad-based. This policy updraft attracts joint ventures that stitch together local feedstock with imported technology, accelerating capacity rollout.

Europe moves with stringent carbon-pricing and SAF mandates that jump-start premium niches. The ReFuelEU rulebook gives investors clarity on future SAF ramp-ups, while Germany and the UK run national subsidies to ensure domestic production. Feedstock flexibility, including sugar beet and waste biomass, helps buffer supply shocks. South America continues leveraging cheap sugarcane and advanced second-generation mills that process bagasse, supporting steady export flows to deficit regions. The Middle East and Africa, though smaller, are piloting projects as part of diversification strategies.

- Abengoa

- ADM

- BASF SE

- BP p.l.c.

- Cargill Incorporated

- CropEnergies AG

- Gevo

- Green Plains Inc.

- INEOS

- Mascoma LLC

- POET LLC

- Raizen

- SEKISUI CHEMICAL CO., LTD.

- Valero Energy Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated ethanol-blend targets

- 4.2.2 Rapid airline SAF certification of Alcohol-to-Jet pathways

- 4.2.3 Integration of CO2 to alcohol CCU plants at refineries

- 4.2.4 Bio-alcohol use as low-carbon chemical feedstock in CPG

- 4.2.5 Emerging methanol-powered shipping corridors

- 4.3 Market Restraints

- 4.3.1 Feedstock price volatility

- 4.3.2 Insufficient pipeline compatibility for high-blend alcohols

- 4.3.3 Stagnant global light-vehicle production post-2027

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Bio-Methanol

- 5.1.2 Bio-Ethanol

- 5.1.3 Bio-Butanol

- 5.1.4 Bio-BDO

- 5.1.5 Other Bio-Alcohols

- 5.2 By Feedstock

- 5.2.1 Starch-based Crops

- 5.2.2 Sugar-based Crops

- 5.2.3 Lignocellulosic Biomass

- 5.2.4 Algal Biomass

- 5.2.5 Industrial Off-gases and MSW

- 5.3 By Application

- 5.3.1 Transportation

- 5.3.2 Construction

- 5.3.3 Electronics

- 5.3.4 Pharmaceuticals

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abengoa

- 6.4.2 ADM

- 6.4.3 BASF SE

- 6.4.4 BP p.l.c.

- 6.4.5 Cargill Incorporated

- 6.4.6 CropEnergies AG

- 6.4.7 Gevo

- 6.4.8 Green Plains Inc.

- 6.4.9 INEOS

- 6.4.10 Mascoma LLC

- 6.4.11 POET LLC

- 6.4.12 Raizen

- 6.4.13 SEKISUI CHEMICAL CO., LTD.

- 6.4.14 Valero Energy Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment