|

시장보고서

상품코드

1844680

스마트 헬스케어 제품 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Healthcare Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

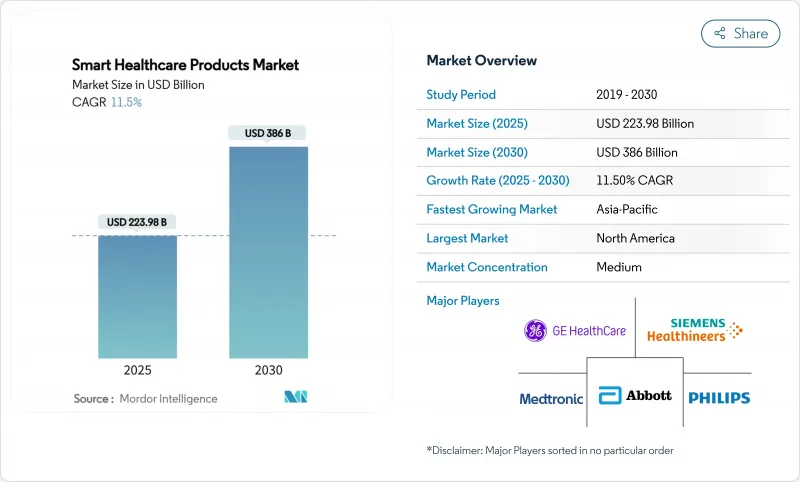

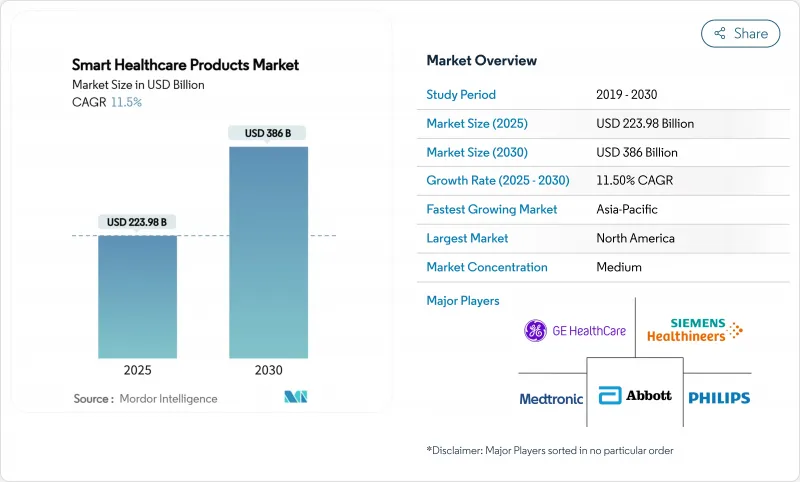

스마트 헬스케어 제품 시장 규모는 2025년 2,239억 8,000만 달러로 평가되었고, 2030년에 3,860억 달러에 이를 것으로 예측되며, 기간 동안 CAGR은 11.5%를 나타낼 전망입니다.

사물인터넷(IoT) 지원 기기의 확산, 인공지능과 임상 워크플로우의 융합, 원격 모니터링 솔루션을 포괄하는 보상 모델이 도입을 가속화하고 있습니다. 싱가포르의 1억 5천만 달러 규모 GenAI 프로그램과 유럽 건강 데이터 공간 규정(European Health Data Space Regulation) 같은 정부 인센티브는 데이터 교환을 표준화하고 통합 비용을 절감하며 공급업체 투자를 촉진하고 있습니다. 기기 제조사, 클라우드 제공업체, 병원 시스템 간의 전략적 파트너십은 경쟁 전략을 재편하는 한편, 사이버 보안 규제는 준수 요건을 강화하고 있습니다. 이러한 요소들이 종합적으로 작용하여 스마트 헬스케어 제품 시장을 견인하고 있으나, 자본 집약적 인프라와 데이터 프라이버시 우려가 성장 궤도를 다소 완화시키고 있습니다.

세계의 스마트 헬스케어 제품 시장 동향 및 인사이트

IoT 기반 의료 기기 채택 증가

커넥티드 기기의 확산은 환자 데이터를 실시간으로 수집하고 진료 현장에서 실행 가능한 인사이트를 제공함으로써 임상 관행을 재편하고 있습니다. 5G 네트워크가 전송 지연을 110밀리초로 낮추고 패킷 손실을 0.07%로 줄이면서, 2025년까지 미국의 원격 환자 모니터링 사용자는 7,100만 명을 넘어설 것으로 예상됩니다. 의료 서비스 제공자의 엣지 컴퓨팅 지출은 2025년 103억 달러에 달할 것으로 전망되며, 이는 초기 단계 개입을 위한 예측 분석을 지원합니다. 아시아태평양 지역 공급업체들은 부정맥 및 혈당 이상을 감지하는 AI 기반 웨어러블 기기를 출시하며 새로운 수익원을 창출하고 상호운용성 요구사항을 높이고 있습니다. 기기 제조사들은 전력 소모량을 30% 절감하는 보안 칩셋을 내장해 장기 모니터링을 위한 배터리 수명을 연장하고 있습니다. 이러한 요소들은 종합적으로 임상 결과를 개선하고 스마트 헬스케어 제품 시장 전반의 규모 성장을 주도합니다.

증가하는 만성질환 부담과 고령화 인구 구조

2024년 전 세계 사망 원인 중 만성 질환이 74%를 차지했으며, 아시아태평양 지역 경제권에서 부담이 가장 컸습니다. 지속적 모니터링 솔루션은 재입원률을 85% 감소시켜 지불자에게 실질적 비용 절감을 가져오며 환자 만족도 점수를 97%까지 향상시킵니다. 고령화 인구는 장기 요양을 필요로 하여 스마트 침대, 낙상 감지 센서, AI 기반 영상 장비 수요를 촉발합니다. 경제적 이점은 상당하며, AI는 진단 오류와 행정적 오버헤드를 줄여 연간 최대 3,600억 달러를 절감할 것으로 예상됩니다. 보편적 의료 시스템을 갖춘 국가들은 만성 질환 프로그램에 스마트 헬스케어 제품을 통합하여 대량 전개를 가속화하고 데이터 교환 프로토콜을 표준화하고 있습니다.

스마트 헬스케어 생태계의 높은 자본 비용

oT 플랫폼, 엣지 서버, 사이버 보안 계층을 구축하려면 상당한 초기 투자가 필요하며, 소규모 공급업체들은 자금 조달에 어려움을 겪습니다. 제안된 HIPAA 개정안은 암호화, 다중 인증, 교육 의무화 등을 포함해 규제 대상 기관에 첫해 93억 달러의 비용을 발생시킬 수 있습니다. 입법자들은 '건강 인프라 보안 및 책임법(Health Infrastructure Security and Accountability Act)'을 도입해 표준 준수를 위해 13억 달러를 배정했으나, 여전히 병원들이 업그레이드 비용 대부분을 부담해야 합니다. 자본 집약성은 서비스별 요금제(fee-for-service)가 유지되고 마진이 좁은 신흥 시장에서 도입 속도를 늦추고 있습니다. 공급업체들은 비용을 다년간에 걸쳐 분산하는 ‘서비스형 기기(Device-as-a-Service)’ 계약으로 대응하고 있습니다. 그러나 도입 일정은 자금 조달 가능성에 여전히 좌우되어, 스마트 헬스케어 제품 시장의 단기 출하량에 부담을 주고 있습니다.

부문 분석

전자건강기록(EHR)은 2024년 전체 매출의 28.51%를 차지하며 임상 워크플로우의 데이터 백본으로서의 위상을 입증했습니다. 베트남의 3,200만 건 환자 기록 병원 전체 디지털화 같은 국가 프로그램은 정부 지원을 재확인시켜 플랫폼 공급업체의 지속적인 라이선스 수익을 보장합니다. 오라클이 재향군인부(VA) 시스템 구축을 위해 신청한 35억 달러 예산은 기업 규모 구현에 대한 기관 차원의 의지를 보여줍니다. 지속적인 사용자 경험 개선과 HL7 FHIR 준수 강화는 전환 비용을 공고히 합니다. 선진국에서 일차 진료 환경의 보급률이 정체됨에 따라 EHR 스마트 헬스케어 제품 시장 규모는 한 자릿수 성장률로 꾸준히 확대될 전망입니다.

스마트 웨어러블 기기는 19.25%의 연평균 복합 성장률(CAGR은)을 기록할 것으로 전망되며, 외래 환자 모니터링 분야의 미충족 수요를 포착하고 있습니다. 커프 없는 혈압 모니터 및 손목 기반 맥박 감지 기술과 같은 FDA 승인 혁신 기술은 임상적 수용성을 확대합니다. 스타트업들은 클라우드 연결성과 AI 알고리즘을 활용해 구독 기반 분석 서비스를 제공함으로써 하드웨어 마진 의존도를 낮춥니다. 기기 제조사들은 소프트웨어를 최신 상태로 유지하는 무선 업데이트(OTA) 파이프라인을 내장해 제품 수명과 서비스 수익을 연장합니다. 따라서 웨어러블 스마트 헬스케어 제품 시장 규모는 다른 기기 분류 대비 비정상적인 성장을 보일 전망입니다.

병행 부문들은 보조 역할을 수행합니다. 원격의료 플랫폼은 웨어러블을 가상 진료에 통합하며, 스마트 알약은 혈액 검출에 대한 FDA De Novo 승인을 받은 후 위장관 진단 분야에서 주목받고 있습니다. 스마트 RFID 캐비닛은 고가 소모품을 보호하여 재고 손실을 최대 15%까지 줄이고 관리 책임 체인 규정 준수를 개선합니다. 지멘스가 칸톤스슈피탈 바덴에 7,000개의 IoT 센서를 배치한 것과 같은 스마트 병원 인프라 투자는 스마트 헬스케어 제품 시장 전반에 걸친 종단간 통합이 확대되고 있음을 보여줍니다.

지역 분석

북미는 정교한 지불자 시스템, 선진 인프라, 상당한 벤처 캐피털 유입에 힘입어 2024년 37.82%의 매출 점유율을 유지했습니다. 디지털 헬스 연구에 1억 달러 이상을 투입한 ARPA-H 여성 건강 스프린트(ARPA-H Women's Health Sprint)와 같은 연방 정부 이니셔티브는 혁신 파이프라인을 강화합니다. 메디케어의 원격의료 유연성 확대(2025년까지)는 원격 모니터링 활용을 더욱 공고히 하고 공급자 수요를 안정화합니다. 캐나다는 표준 기반 상호운용성 촉진을 위한 인포웨이 임상혁신센터(Infoway Centre for Clinical Innovation)를 출범시켜 지역 역동성을 보완합니다. 양국 모두 강력한 사이버보안 감독 체계를 갖추고 있어 보안 침해 사건 보도에도 불구하고 지속적인 투자가 보장됩니다.

아시아태평양 지역은 국가 차원의 전략적 협력, 중산층 인구 확대, 농촌 지역의 미충족 임상 수요 덕분에 17.31%라는 가장 빠른 연평균 복합 성장률(CAGR은)을 기록할 전망입니다. 싱가포르의 5년간 1억 5천만 달러 규모 'GenAI 계획'은 공공병원 전반에 걸쳐 영상 AI 및 자동화된 기록 전사 시스템을 신속히 도입합니다. 한국은 8억 3천만 달러를 AI 기반 응급 시스템에 배정해 실시간 환자 이송 관리의 기준을 제시합니다. 동남아시아 디지털 헬스 시장 규모는 2024년 61억 달러에 달할 전망이며, 높은 스마트폰 보급률과 수급 격차에 투자자들이 주목하고 있습니다. 호주의 헬스 커넥트 플랫폼은 원활한 데이터 공유를 촉진해 의료기관 참여를 가속화합니다.

유럽은 2025년 3월 발효 예정인 유럽 건강 데이터 공간 규정(European Health Data Space Regulation)으로 디지털 헬스 서비스 단일 시장이 구축되며 Xt-EHR, EUVAC 등 프로젝트가 지원됩니다. 통일된 규정은 공급업체 분열을 줄이고 국경 간 원격의료를 촉진합니다. 독일과 프랑스 국가 보건 시스템은 전자처방 의무화를 시행하며 디지털화에 대한 의지를 강조했습니다. 중동 및 아프리카에서는 남아프리카공화국이 국가 차원의 전자건강 전략을 시범 운영 중이며, 걸프협력회의(GCC) 회원국들은 스마트 병원 건설에 투자하고 있습니다. 남미는 특히 브라질에서 도시화와 민간 보험 가입 증가가 수요를 촉진하며 성장세를 보이고 있으나, 거시경제적 변동성이 성장을 다소 억제하고 있습니다. 전반적으로 지리적 다각화는 확장 위험을 상쇄하며 스마트 헬스케어 제품 시장의 지속적인 성장을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- IoT 기반 의료 기기의 확산

- 만성 질환 부담 증가 및 인구 고령화

- 디지털 헬스 인프라에 대한 정부의 인센티브

- 원격의료 서비스에 대한 확대된 보험 적용

- 지속적 관리를 위한 웨어러블 초음파 및 스마트 섬유

- 초저전력 센서 구현을 위한 에너지 효율적 경량 암호화 기술

- 시장 성장 억제요인

- 스마트 헬스케어 에코시스템의 높은 자본 비용

- 사이버 보안 및 데이터 프라이버시 우려

- 규정 준수 지연을 유발하는 BLE 프로토콜 취약점

- 첨단 미니 센서 공급망 취약성

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 원격 의료

- 전자건강기록(EHR)

- m건강 솔루션

- 스마트 알약

- 스마트 주사기

- 스마트 RFID 캐비닛

- 스마트 및 웨어러블 기기

- 스마트 병원 인프라

- 용도별

- 보관 및 재고 관리

- 원격 모니터링

- 진단

- 치료 및 약물전달

- 웰니스 및 예방의료

- 최종 사용자별

- 병원

- 재택치료

- 전문 클리닉

- 외래수술센터(ASC)

- 장기 간병 시설

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 사우디아라비아

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Medtronic plc

- GE Healthcare

- Siemens Healthineers AG

- Koninklijke Philips NV

- Samsung Medison Co. Ltd.

- McKesson Corporation

- Oracle Corporation(Cerner)

- NextGen Healthcare Inc.

- Olympus Corporation

- Capsule Technologies Inc.

- Omron Healthcare Co. Ltd.

- Teladoc Health Inc.

- DexCom Inc.

- Apple Inc.

- Allscripts Healthcare Solutions Inc.

- IBM Corporation(Watson Health)

- Cisco Systems Inc.

- Boston Scientific Corporation

- iRhythm Technologies Inc.

제7장 시장 기회와 전망

HBR 25.11.07The smart healthcare products market size is valued at USD 223.98 billion in 2025 and is forecast to reach USD 386.00 billion by 2030, expanding at an 11.5% CAGR through the period.

Rising deployment of IoT-enabled devices, the convergence of artificial intelligence with clinical workflows, and reimbursement models that now cover remote monitoring solutions are accelerating adoption. Government incentives such as Singapore's USD 150 million GenAI programme and the European Health Data Space Regulation are standardising data exchange, reducing integration costs, and stimulating supplier investment. Strategic partnerships among device makers, cloud providers, and hospital systems are reshaping competitive strategies, while cybersecurity regulations tighten compliance requirements. Taken together, these forces propel the smart healthcare products market, even as capital-intensive infrastructure and data-privacy concerns temper the growth trajectory.

Global Smart Healthcare Products Market Trends and Insights

Rising Adoption of IoT-Enabled Medical Devices

The proliferation of connected devices is reshaping clinical practice by capturing patient data in real time and delivering actionable insights at the point of care. Remote patient monitoring users in the United States are expected to surpass 71 million by 2025 as 5G networks lower transmission latency to 110 milliseconds, reducing packet loss to 0.07%. Healthcare provider spending on edge computing is forecast to reach USD 10.3 billion in 2025, supporting predictive analytics for early-stage intervention. Asia-Pacific suppliers are rolling out AI-driven wearables that detect arrhythmia and glucose anomalies, creating new revenue pools and raising interoperability requirements. Device makers are embedding secure chipsets that consume 30% less power, extending battery life for long-term monitoring. Collectively, these factors improve clinical outcomes and drive volume growth across the smart healthcare products market.

Escalating Chronic-Disease Burden & Ageing Demographics

Chronic diseases accounted for 74% of global deaths in 2024, with the highest burden in Asia-Pacific economies. Continuous monitoring solutions reduce hospital readmissions by 85%, generating tangible savings for payers while enhancing patient satisfaction scores to 97%. An ageing population requires long-term care, triggering demand for smart beds, fall-detection sensors, and AI-enabled imaging. The economic upside is considerable, with AI projected to save up to USD 360 billion annually by trimming diagnostic errors and administrative overhead. Countries with universal healthcare systems are integrating smart healthcare products into chronic-disease programmes, accelerating volume deployment and standardising data exchange protocols.

High Capital Cost of Smart Healthcare Ecosystems

Deploying IoT platforms, edge servers, and cybersecurity layers requires sizable upfront outlays that smaller providers struggle to finance. Proposed HIPAA revisions could cost regulated entities USD 9.3 billion in the first year, covering encryption, multifactor authentication, and training mandates. Legislators introduced the Health Infrastructure Security and Accountability Act, which budgets USD 1.3 billion for standards compliance but still leaves hospitals funding the bulk of upgrades. Capital intensity slows rollouts in emerging markets where reimbursement remains fee-for-service and margins are thinner. Vendors are responding with device-as-a-service contracts that spread costs over multi-year terms. Yet adoption timelines remain contingent on financing availability, weighing on near-term units shipped in the smart healthcare products market.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Digital-Health Infrastructure

- Broader Reimbursement for Telemedicine Services

- Cyber-Security & Data-Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronic Health Records contributed 28.51% to overall revenue in 2024, underlining their position as the data backbone of clinical workflows. National programmes such as Vietnam's hospital-wide digitisation of 32 million patient files reaffirm government support, ensuring sustained licensing income for platform vendors. Oracle's USD 3.5 billion budget application for the Veterans Affairs rollout further demonstrates institutional commitment to enterprise-scale implementations. Continuous user-experience upgrades and HL7 FHIR compliance solidify switching costs. The smart healthcare products market size for EHRs is projected to expand steadily, albeit at a single-digit rate, as penetration in primary care settings plateaus in developed economies.

Smart Wearable Devices, forecast to record a 19.25% CAGR, are capturing unmet needs in ambulatory monitoring. FDA-cleared innovations such as cuffless blood-pressure monitors and wrist-based pulse detection broaden clinical acceptability. Start-ups leverage cloud connectivity and AI algorithms to offer subscription-based analytics, reducing reliance on hardware margins. Device makers embed over-the-air update pipelines that keep software current, extending product life and service revenue. The smart healthcare products market size for wearables is therefore positioned for outsized expansion relative to other device classes.

Parallel segments play supporting roles. Telemedicine Platforms integrate wearables into virtual-care visits, while Smart Pills gain traction in gastrointestinal diagnostics following FDA De Novo clearance for blood detection. Smart RFID Cabinets protect high-value consumables, cutting inventory shrinkage by up to 15% and improving compliance with chain-of-custody mandates. Investments in smart hospital infrastructure, such as Siemens' deployment of 7,000 IoT sensors at Kantonsspital Baden, illustrate growing end-to-end integration across the smart healthcare products market.

The Smart Healthcare Products Market Report is Segmented by Product Type (Telemedicine, Electronic Health Records, Mhealth Solutions, Smart Pills, Smart Syringes, Smart RFID Cabinets, and More), Application (Storage and Inventory Management, Remote Monitoring, and More), End User (Hospitals, Home Care Settings, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.82% revenue share in 2024, buoyed by sophisticated payer systems, advanced infrastructure, and sizeable venture capital flows. Federal initiatives such as the ARPA-H Women's Health Sprint, which committed more than USD 100 million to digital health research, strengthen the innovation pipeline. Medicare's extension of telehealth flexibilities through 2025 further entrenches remote monitoring usage and stabilises supplier demand. Canada complements the region's dynamism by launching the Infoway Centre for Clinical Innovation to foster standards-based interoperability. Strong cybersecurity oversight in both countries ensures continued investment despite breach headlines.

Asia-Pacific delivers the fastest CAGR at 17.31% thanks to coordinated national strategies, expanding middle-class populations, and unmet clinical demand in rural areas. Singapore's five-year USD 150 million GenAI plan fast-tracks imaging AI and automated record transcription across public hospitals. South Korea allocates USD 830 million for AI-enabled emergency systems, setting benchmarks for real-time patient transfer management. Southeast Asia's digital health revenue is poised to reach USD 6.1 billion in 2024, with investors attracted to high smartphone penetration and supply-demand gaps. Australia's Health Connect platform promotes seamless data sharing, accelerating provider onboarding.

Europe benefits from the European Health Data Space Regulation, effective March 2025, setting a single market for digital health services and supporting projects such as Xt-EHR and EUVAC. Unified rules reduce vendor fragmentation and encourage cross-border telemedicine. National health systems in Germany and France have rolled out e-prescription mandates, underlining commitment to digitalisation. In the Middle East and Africa, South Africa pilots national e-health strategies, while Gulf Cooperation Council states invest in smart hospital builds. South America shows momentum, particularly in Brazil where urbanisation and private insurance uptake fuel demand, although macroeconomic volatility moderates growth. Overall, geographic diversification balances expansion risks and underpins sustained growth across the smart healthcare products market.

- Abbott Laboratories

- Medtronic

- GE Healthcare

- Siemens Healthineers

- Koninklijke Philips

- Samsung Medison Co. Ltd.

- Mckesson

- Oracle

- NextGen Healthcare

- Olympus

- Capsule Technologies

- Omron Healthcare Co. Ltd.

- Teladoc Health

- Dexcom

- Apple

- Allscripts

- IBM Corporation (Watson Health)

- Cisco Systems

- Boston Scientific

- iRhythm Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption Of Iot-Enabled Medical Devices

- 4.2.2 Escalating Chronic-Disease Burden & Ageing Demographics

- 4.2.3 Government Incentives For Digital-Health Infrastructure

- 4.2.4 Broader Reimbursement For Telemedicine Services

- 4.2.5 Wearable Ultrasound & Smart Textiles For Continuous Care

- 4.2.6 Energy-Efficient Lightweight Cryptography Unlocking Ultra-Low-Power Sensors

- 4.3 Market Restraints

- 4.3.1 High Capital Cost Of Smart Healthcare Ecosystems

- 4.3.2 Cyber-Security & Data-Privacy Concerns

- 4.3.3 BLE Protocol Vulnerabilities Triggering Compliance Delays

- 4.3.4 Supply-Chain Fragility For Advanced Mini-Sensors

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers / Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Telemedicine

- 5.1.2 Electronic Health Records

- 5.1.3 mHealth Solutions

- 5.1.4 Smart Pills

- 5.1.5 Smart Syringes

- 5.1.6 Smart RFID Cabinets

- 5.1.7 Smart Wearable Devices

- 5.1.8 Smart Hospital Infrastructure

- 5.2 By Application

- 5.2.1 Storage & Inventory Management

- 5.2.2 Remote Monitoring

- 5.2.3 Diagnostics

- 5.2.4 Treatment & Drug-Delivery

- 5.2.5 Wellness & Preventive Care

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Home-Care Settings

- 5.3.3 Specialty Clinics

- 5.3.4 Ambulatory Surgical Centers

- 5.3.5 Long-Term Care Facilities

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.4.3.1 Saudi Arabia

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Medtronic plc

- 6.3.3 GE Healthcare

- 6.3.4 Siemens Healthineers AG

- 6.3.5 Koninklijke Philips N.V.

- 6.3.6 Samsung Medison Co. Ltd.

- 6.3.7 McKesson Corporation

- 6.3.8 Oracle Corporation (Cerner)

- 6.3.9 NextGen Healthcare Inc.

- 6.3.10 Olympus Corporation

- 6.3.11 Capsule Technologies Inc.

- 6.3.12 Omron Healthcare Co. Ltd.

- 6.3.13 Teladoc Health Inc.

- 6.3.14 DexCom Inc.

- 6.3.15 Apple Inc.

- 6.3.16 Allscripts Healthcare Solutions Inc.

- 6.3.17 IBM Corporation (Watson Health)

- 6.3.18 Cisco Systems Inc.

- 6.3.19 Boston Scientific Corporation

- 6.3.20 iRhythm Technologies Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment