|

시장보고서

상품코드

1844685

행동 및 정신건강 소프트웨어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Behavioral And Mental Health Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

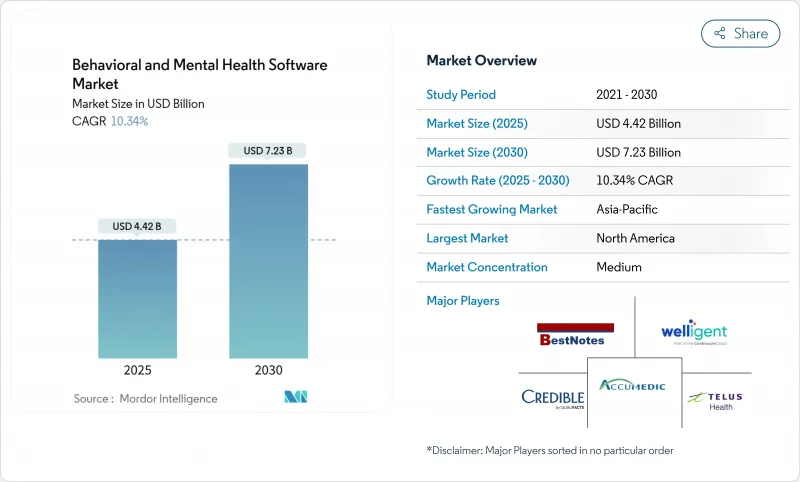

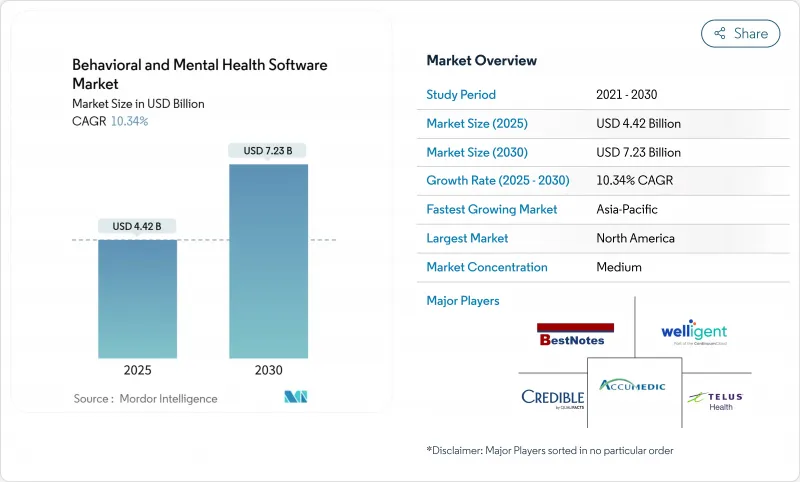

행동 및 정신건강 소프트웨어 시장 규모는 2025년에 44억 2,000만 달러로 평가되었고, 2030년에 72억 3,000만 달러에 이를 것으로 예측되며, CAGR은 10.34%를 나타낼 전망입니다.

모든 의료 서비스 환경에서 보험사, 의료 제공자, 고용주들은 기존 업무 프로세스를 맞춤형 행동 치료 도구로 전환하고 있습니다. AI 기반 분류, 측정 기반 치료, 자동화된 문서화가 의료진의 업무 부담을 줄이고 치료 성과를 높일 수 있음을 입증했기 때문입니다. 주요 성장 요인으로는 영구적인 원격 정신건강 진료비 청구 코드, 소규모 진료소의 자본 장벽을 제거하는 클라우드 비용 효율성, 그리고 행동 치료 제공자에게 급성 치료 동료들과 동등한 EHR 보조금을 제공하는 연방 인센티브가 포함됩니다. 동시에 기후 불안과 직장 번아웃에 대한 대중의 우려 증가로 자가 관리 수요가 근거 기반 앱으로 재편되면서, 검증된 평가 도구와 인지행동치료(CBT) 기반 미세 개입 기능을 탑재한 소프트웨어 공급업체의 총 잠재 수요가 확대되고 있습니다. 공급업체 간 통합 가속화와 사모펀드 및 전략적 투자자로부터의 지속적인 자금 유입은 행동 및 정신건강 소프트웨어 시장의 중기 성장 전망을 더욱 공고히 합니다.

세계의 행동 및 정신건강 소프트웨어 시장 동향 및 인사이트

증가하는 스트레스 관련 정신 건강 질환

매년 미국 성인의 26% 이상이 진단 가능한 정신 질환을 보고하며, 이러한 유병률은 현재 여러 유럽 국가에서도 유사하게 나타나고 있어, 서비스 제공자들이 확장 가능한 디지털 스크리닝 및 치료 안내 도구로 전환하도록 촉진하고 있습니다. 소프트웨어 벤더들은 기후 불안, 직장 번아웃, 소셜미디어 유발 스트레스 위험을 경고하는 400여 가지 표준화된 평가 도구와 실시간 분석 기능을 패키지화하고 있습니다. 아시아에서는 1990년부터 2019년 사이 정신 장애 관련 장애 조정 생명 연한(DALY)이 4,390만 년에서 6,900만 년으로 급증하며, 대규모 농촌 인구를 분류할 수 있는 다국어 모바일 앱 수요를 주도하고 있습니다. 인터마운틴 헬스의 뉴로플로우 AI 위험 모델 도입 사례는 일상적인 일차 진료 과정에서 자살 충동을 식별함으로써 개입까지의 시간을 단축하는 예측 점수의 효과를 보여줍니다. 이러한 모듈이 핵심 EHR 워크플로우와 원활하게 통합됨에 따라 기업형 의료 시스템과 개인 진료소 모두에서 도입이 가속화되고 있습니다. 이러한 역학적 및 기술적 추세는 행동 및 정신 건강 소프트웨어 시장의 규모를 확대하고 있습니다.

행동 건강을 위한 정부 자금 지원 및 EHR 인센티브

미국 '행동 건강 정보 기술 접근성 개선법(Improving Access to Behavioral Health Information Technology Act)'은 CMS가 인증된 EHR 도입에 대해 심리학자, 정신병원, 지역사회 정신건강 센터에 비용을 상환할 수 있는 길을 열었다. 별도의 ONC 프로그램은 행동 건강 워크플로우에 2,000만 달러를 배정했으며, SAMHSA 기금은 위기 대응 및 원격 행동 치료 기능을 지원하는 소프트웨어에 대한 주 메디케이드 매칭을 확대합니다. 이러한 조치들은 종합적으로 전문 행동 건강 시설의 EHR 사용률이 병원(97%) 대비 6%에 불과했던 역사적 디지털 격차를 좁히고 있습니다. 소규모 진료소는 이제 맞춤형 보조금과 공급업체 평가 및 변화 관리를 간소화하는 기술 지원 허브를 이용할 수 있습니다. 자금 유입이 증가함에 따라 공급업체들은 사상 최대의 제안 요청(RFP) 물량을 기록하며 행동 및 정신 건강 소프트웨어 시장의 성장을 촉진하고 있습니다.

데이터 프라이버시 및 사이버 보안 격차

행동 데이터는 낙인 위험이 높아 유출 시 과도한 규제 및 평판 손실을 초래합니다. FTC의 Cerebral 단속은 추적 픽셀 오용을 부각시켜 공급업체들이 기기 내 분석, 지오펜싱 동의, 제로 트러스트 아키텍처 채택을 촉진했습니다. EU GDPR 규정은 국경 간 전개를 더욱 복잡하게 만들어 세분화된 데이터 최소화 및 ‘잊혀질 권리’ 워크플로우를 강제합니다. 많은 소규모 진료소는 24시간 모니터링을 위한 사이버 보안 예산이 부족해 민감한 차트를 클라우드 스택으로 이전하는 것을 주저합니다. 결과적으로 개인정보 보호 의문이 해결되지 않은 지역에서는 단기 행동 및 정신 건강 소프트웨어 시장 확장이 둔화됩니다.

부문 분석

임상 모듈은 2024년 매출의 55.12%를 차지하며 모든 현대적 전개 결정의 기반이 됩니다. 이러한 우위는 의료진이 매일 의존하는 전자 차트 작성, 처방 세트, 통합 치료 계획에서 비롯됩니다. 오라클 헬스의 환경 기록 기능은 기록 시간을 40% 단축시켜, 의료기관이 플랫폼 선택을 임상적 깊이에 기반하는 이유를 보여줍니다. 자동화된 접수, 의뢰 경로 설정, 사전 승인 확인을 추구하는 의료기관으로 인해 행정용 부가 기능이 11.21%의 연평균 성장률(CAGR은)로 가장 빠르게 성장하고 있습니다. 청구 처리율 향상을 추구하는 구매자들을 유인하는 수익 주기 위젯도 주목받습니다. 포괄적 제품군이 진전 기록과 접수 설문지, 청구 편집 기능을 통합함에 따라 행동 및 정신 건강 소프트웨어 시장 전반에서 교차 판매 증대 효과가 지속되고 있습니다.

인라인 분석과 AI 분류 기능은 임상적 가치를 한층 높입니다. 뉴로플로우(NeuroFlow)의 위험 엔진은 PHQ-9(우울증 평가 척도), 생체 신호, 사회적 결정 요인을 종합해 자살 위험성을 경고함으로써 의료진이 조기에 개입할 수 있도록 합니다. 인구 건강 대시보드는 우편번호별 우울증 유병률을 시각화하여 보조금 신청을 지원합니다. 정밀 측정이 보상과 연계됨에 따라, 2030년까지 임상 기능의 시장 점유율은 행동 및 정신 건강 소프트웨어 시장 규모의 절반 이상을 유지할 것입니다. 한편 행정 자동화는 스프레드시트에서 벗어나려는 서비스 취약 지역 단독 진료소에서 신규 수익을 창출합니다.

의료 시스템이 통합 기술 스택을 표준화함에 따라 소프트웨어는 2024년 지출의 63.64%를 차지했습니다. 구매자들은 포인트 솔루션을 통합하고 API 유지보수를 제거하는 단일 벤더 제품군을 선호합니다. 그럼에도 워크플로 재설계 수요와 규제 보고 체계 구축으로 전문 서비스 매출은 연평균 11.09% 성장세를 보입니다. 벤더들은 DSM-5 템플릿을 FHIR 리소스에 매핑하고, 직원 교육을 실시하며, 클라우드 구성을 보안하는 자문 계약을 통해 수익을 창출합니다.

모바일 앱은 진료실 밖으로 치료를 확장해 고객 충성도를 높입니다. 질환별 도구는 매일 인지행동치료(CBT) 알림을 제공하며, 측정 일지는 임상가 대시보드에 직접 연동되어 시의적절한 개입을 가능하게 합니다. 고객 성공 팀이 참여도 측정 데이터를 최적화함에 따라 구독 갱신률이 상승하며 총계약가치(TCV)가 확대됩니다. 결과적으로 소프트웨어와 서비스를 결합한 번들 상품이 제안요청서(RFP) 평가에서 우위를 점하며, 행동 및 정신건강 소프트웨어 산업 전반에 걸쳐 지갑 점유율이 심화되고 있습니다.

지역 분석

북미는 연방 정부 환급 정책의 명확성과 지속적인 보조금 지원으로 2024년 매출의 42.21%를 차지했습니다. CMS의 2025년 의사 수수료 일정은 소프트웨어 플랫폼이 청구 규정 준수를 위해 자동화하는 새로운 진료 조정 수정자를 도입했습니다. 강화된 메디케이드 매칭 비율을 활용하는 주들은 위기 상담 전화 분류 도구와 실시간 병상 등록 시스템을 도입하며 공공 네트워크 전반에 소프트웨어를 통합하고 있습니다. 오라클의 120만 평방피트 규모 내슈빌 캠퍼스는 기술 대기업들이 지역 디지털 헬스 수요에 대한 장기적 투자를 시사합니다.

아시아태평양 지역은 2030년까지 연평균 11.42% 성장률로 가장 빠르게 확장되는 시장입니다. 정신질환 DALY(장애조정한생명연수)는 1990년 이후 57% 급증했으며, 미치료 질환으로 인한 GDP 손실은 2030년까지 인도와 중국에서 9조 달러를 넘어설 전망입니다. 정부들은 모바일 중심 프레임워크로 대응 중이며, APEC 디지털 허브는 FHIR 기반 일차의료 통합을 통해 검진 프로토콜 확산을 추진합니다. 지역별 다운로드 차트를 주도하는 8개 정신건강 모바일 앱 카테고리는 언어적 및 문화적 맞춤화 요구를 반영합니다. 코로나19로 원격의료가 보편화되었으나 접근성 격차는 지속되어, 저대역폭 지역을 위한 오프라인 지원 앱과 SMS 체크인 솔루션이 필요합니다. 행동 및 정신건강 소프트웨어 시장이 지역별로 심화되면서 사용자 경험(UX)을 현지화하고 통신사와 협력하는 업체들이 점유율을 확보하고 있습니다.

유럽은 꾸준하지만 완만한 도입세를 보입니다. GDPR은 설계 단계부터 개인정보 보호를 의무화하여 동의 관리 복잡성을 높이지만, 동시에 최종 사용자 신뢰를 구축합니다. 여러 국가 보건 서비스가 단계적 치료 디지털 치료제를 지원함에 따라 공급업체들은 동료 검토를 거친 증거를 발표하도록 촉진됩니다. 다국어 지원 구축과 엄격한 CE 인증 절차로 출시 일정이 지연되지만, 일단 승인되면 대량으로 보험 적용이 승인되어 지속적인 수익을 창출합니다. 중동 및 아프리카 지역에서는 걸프 국가들의 정신건강 예산이 증가하는 반면, 남미는 클라우드 플랫폼을 활용해 자본 인프라 격차를 뛰어넘고 있습니다. 종합적으로 지리적 다각화는 행동 및 정신건강 소프트웨어 시장 전반에 걸쳐 통화 및 정책 리스크를 완화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스트레스 관련 정신 건강 질환 증가

- 행동 건강을 위한 정부 자금 지원 및 EHR 인센티브

- 원격 정신 건강 서비스에 대한 보험사 수용 및 보상

- AI 기반 임상 의사 결정 지원으로 치료 결과 개선

- 기후 불안으로 인한 디지털 자가 치료 도구 수요 증가

- 고용주 부담의 정신 건강 플랫폼이 급증

- 시장 성장 억제요인

- 데이터 프라이버시 및 사이버 보안 취약점

- 소규모 제공업체의 종이 기반 워크플로 지속 사용

- 일반 EHR과 행동건강(BH) 전용 EHR 간 상호운용성 격차

- 디지털 치료제 환급을 위한 불확실한 동등성 법규

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 기능별

- 임상 기능

- 전자 건강 기록(EHR)

- 임상 의사 결정 지원

- 치료 계획/집단 건강 관리

- 기타 임상 기능

- 관리 기능

- 환자 예약

- 사례 관리

- 기타 관리 기능

- 재무 기능

- 수익주기 관리

- 매입채무 / 총계정원장

- 기타 재무 기능

- 임상 기능

- 솔루션별

- 소프트웨어

- 통합 스위트

- 독립형 모듈

- 모바일 앱

- 서비스별

- 소프트웨어

- 전개 모드별

- 클라우드 기반

- 온프레미스

- 최종 사용자별

- 지역 클리닉

- 병원

- 개인 개업의

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oracle(Cerner)

- Netsmart Technologies

- Epic Systems

- Qualifacts Systems

- AdvancedMD

- Valant Medical

- Welligent Inc.

- Accumedic Computer Systems

- BestNotes

- Planet DDS(NXGN)

- CloudMD Software

- TELUS Health

- Psyquel

- Behave Inc.

- Kareo Inc.

- TheraNest(Counsol.com)

- SimplePractice

- Streamline Healthcare Solutions

- MindLinc(Duke)

- Allscripts Healthcare Solutions

제7장 시장 기회와 전망

HBR 25.11.07The behavioral and mental health software market size stood at USD 4.42 billion in 2025 and is forecast to reach USD 7.23 billion by 2030, advancing at a 10.34% CAGR.

Across every delivery setting, payers, providers, and employers are re-platforming legacy workflows onto purpose-built behavioral tools as AI-driven triage, measurement-based care, and automated documentation prove they can compress clinician workload and lift outcomes. Key lift factors include permanent tele-mental-health reimbursement codes, cloud cost efficiencies that remove capital barriers for small practices, and federal incentives that finally put behavioral providers on parity with acute-care peers for EHR subsidies. In parallel, growing public concern over climate anxiety and workplace burnout is redirecting self-care traffic toward evidence-based apps, expanding total addressable demand for software vendors that embed validated assessments and CBT-based micro-interventions. Accelerating consolidation among vendors and sustained funding flows from private equity and strategics further reinforce the medium-term expansion thesis for the behavioral and mental health software market.

Global Behavioral And Mental Health Software Market Trends and Insights

Increasing Stress-Related Mental-Health Conditions

More than 26% of U.S. adults report a diagnosable mental condition each year, a prevalence now mirrored across several European countries, pushing providers toward scalable digital screening and care-navigation tools . Software vendors are packaging over 400 standardized assessments and real-time analytics that flag risk for climate anxiety, workplace burnout, and social-media-induced stress. In Asia, disability-adjusted life years tied to mental disorders jumped from 43.9 million to 69 million between 1990 and 2019, steering demand for multilingual mobile apps that can triage large rural populations. Intermountain Health's deployment of NeuroFlow's AI risk models illustrates how predictive scoring cuts time to intervention by identifying suicidal ideation within routine primary-care encounters. As these modules integrate seamlessly with core EHR workflows, adoption accelerates across both enterprise health systems and solo practices. Together, these epidemiologic and technology trends enlarge the addressable behavioral and mental health software market.

Government Funding & EHR Incentives for Behavioral Health

The U.S. Improving Access to Behavioral Health Information Technology Act cleared the path for CMS to reimburse psychologists, psychiatric hospitals, and community mental-health centers for certified EHR adoption. Separate ONC programs earmarked USD 20 million for behavioral workflows, while SAMHSA funds extend state Medicaid matches for software that supports crisis response and tele-behavioral capabilities. Collectively, these initiatives shrink the historic digital divide where only 6% of specialty behavioral facilities used EHRs versus 97% of hospitals. Smaller practices now access targeted grants plus technical-assistance hubs that streamline vendor evaluation and change management . As dollars flow, vendors see record inbound RFP volume, fueling growth in the behavioral and mental health software market.

Data-Privacy & Cybersecurity Gaps

Behavioral data carry heightened stigma risk, so breaches prompt outsized regulatory and reputational penalties. The FTC's enforcement against Cerebral spotlighted tracking-pixel misuse, pushing vendors to adopt on-device analytics, geofenced consent, and zero-trust architectures. EU GDPR rules further complicate cross-border deployments, forcing granular data-minimization and "right to be forgotten" workflows. Many small practices lack cyber budgets for 24/7 monitoring, making them hesitant to migrate sensitive charts to cloud stacks. As a result, near-term behavioral and mental health software market expansion slows where privacy doubts remain unresolved.

Other drivers and restraints analyzed in the detailed report include:

- Payer Acceptance & Reimbursement for Tele-Mental-Health

- AI-Powered Clinical Decision Support Improves Outcomes

- Continued Use of Paper Workflows Among Small Providers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical modules captured 55.12% of 2024 revenue, underpinning every modern deployment decision. This dominance stems from electronic charting, order sets, and integrated care plans that clinicians rely on daily. Oracle Health's ambient documentation reduces note time by 40%, illustrating why providers anchor platform selection on clinical depth. Administrative add-ons are heating fastest with an 11.21% CAGR as practices seek automated intake, referral routing, and prior-auth checks. Revenue-cycle widgets further entice buyers chasing clean-claim rates. Because comprehensive suites now marry progress notes with intake questionnaires and billing edits, cross-sell uplift remains strong across the behavioral and mental health software market.

Inline analytics and AI triage heighten clinical value further. NeuroFlow's risk engines synthesize PHQ-9, vital signs, and social determinants to flag suicidality, letting care teams intervene earlier. Population-health dashboards map depression prevalence by zip code, guiding grant applications. As precision measurement becomes reimbursement-linked, clinical functionality's share will hold above half of the behavioral and mental health software market size through 2030. Administrative automation meanwhile pulls new dollars from underserved solo practices transitioning away from spreadsheets.

Software sustained 63.64% of 2024 spend as health systems standardized on unified tech stacks. Buyers favor single-vendor suites that collapse point solutions and eliminate API maintenance. Still, professional services revenue is trending at an 11.09% CAGR, fueled by workflow redesign demands and regulatory reporting setup. Vendors monetize advisory engagements that map DSM-5 templates to FHIR resources, train staff, and secure cloud configurations.

Mobile apps add stickiness by extending care outside clinic walls. Condition-specific tools push daily CBT nudges, whereas measurement diaries feed directly into clinician dashboards for just-in-time interventions. As customer success teams optimize engagement telemetry, subscription renewals climb, enlarging total contract value. Consequently, blended software-plus-services bundles now dominate RFP scoring, deepening wallet share throughout the behavioral and mental health software industry.

The Behavioral and Mental Health Software Market is Segmented by Function (Clinical Functionality [Electronic Health Records, and More], Administrative Functionality, and More), Solution (Software and Services), Deployment Mode (Cloud-Based and On-Premise) End-User (Community Clinics, Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 42.21% of 2024 revenue, anchored by federal reimbursement clarity and sustained grant pipelines. CMS's 2025 Physician Fee Schedule unlocked new care-coordination modifiers that software platforms automate for billing compliance. States tapping enhanced Medicaid match rates deploy crisis-line triage tools and real-time bed registries, embedding software across public networks. Oracle's 1.2 million-sq-ft Nashville campus signals tech giants' long-term bet on regional digital-health demand.

Asia-Pacific is the fastest-expanding territory at 11.42% CAGR through 2030. Mental-disorder DALYs surged 57% since 1990, and GDP drag from untreated conditions could top USD 9 trillion in India and China by 2030. Governments respond with mobile-first frameworks; the APEC Digital Hub promotes FHIR-based primary-care integration to spread screening protocols. Eight categories of mental-health mobile apps dominate regional download charts, reflecting linguistic and cultural tailoring needs. COVID-19 accelerated tele-health normalization, yet access inequities persist, requiring offline-capable apps and SMS check-ins for low-bandwidth zones. Vendors that localize UX and partner with telecoms capture share as the behavioral and mental health software market deepens regionally.

Europe exhibits steady but moderate uptake. GDPR mandates privacy-by-design, elevating consent orchestration complexity but also establishing trust among end users. Several national health services fund stepped-care digital therapeutics, spurring vendors to publish peer-reviewed evidence. Multi-language build-outs and stringent CE-marking processes elongate launch timelines, yet once approved, reimbursement clears in bulk, yielding durable revenue. The Middle East and Africa see rising mental-health budgets in Gulf states, whereas South America leverages cloud platforms to leapfrog capital infrastructure gaps. Collectively, geographic diversification cushions currency and policy risk across the behavioral and mental health software market.

- Oracle

- Netsmart Technologies

- Epic Systems

- Qualifacts Systems

- AdvancedMD

- Valant Medical

- Welligent

- Accumedic Computer Systems

- BestNotes

- Planet DDS (NXGN)

- CloudMD Software

- TELUS Health

- Psyquel

- Behave

- Kareo Inc.

- TheraNest (Counsol.com)

- SimplePractice

- Streamline Healthcare Solutions

- MindLinc (Duke)

- Allscripts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Stress-Related Mental-Health Conditions

- 4.2.2 Government Funding & EHR Incentives for Behavioral Health

- 4.2.3 Payer Acceptance & Reimbursement for Tele-Mental-Health

- 4.2.4 AI-Powered Clinical Decision Support Improves Outcomes

- 4.2.5 Climate-Anxiety Boosts Demand for Digital Self-Help Tools

- 4.2.6 Employer-Sponsored Mental-Health Platforms Surge

- 4.3 Market Restraints

- 4.3.1 Data-Privacy & Cybersecurity Gaps

- 4.3.2 Continued Use of Paper Workflows Among Small Providers

- 4.3.3 Interoperability Gaps Between General & BH-Specific Ehrs

- 4.3.4 Uncertain Parity Laws for Digital Therapeutics Reimbursement

- 4.4 Technological Outlook

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Function

- 5.1.1 Clinical Functionality

- 5.1.1.1 Electronic Health Records

- 5.1.1.2 Clinical Decision Support

- 5.1.1.3 Care Plans / Population Health

- 5.1.1.4 Other Clinical Functions

- 5.1.2 Administrative Functionality

- 5.1.2.1 Patient Scheduling

- 5.1.2.2 Case Management

- 5.1.2.3 Other Administrative Functions

- 5.1.3 Financial Functionality

- 5.1.3.1 Revenue Cycle Management

- 5.1.3.2 Accounts Payable / General Ledger

- 5.1.3.3 Other Financial Functions

- 5.1.1 Clinical Functionality

- 5.2 By Solution

- 5.2.1 Software

- 5.2.1.1 Integrated Suites

- 5.2.1.2 Stand-alone Modules

- 5.2.1.3 Mobile Apps

- 5.2.2 Services

- 5.2.1 Software

- 5.3 By Deployment Mode

- 5.3.1 Cloud-based

- 5.3.2 On-premise

- 5.4 By End-user

- 5.4.1 Community Clinics

- 5.4.2 Hospitals

- 5.4.3 Private Practices

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Oracle (Cerner)

- 6.3.2 Netsmart Technologies

- 6.3.3 Epic Systems

- 6.3.4 Qualifacts Systems

- 6.3.5 AdvancedMD

- 6.3.6 Valant Medical

- 6.3.7 Welligent Inc.

- 6.3.8 Accumedic Computer Systems

- 6.3.9 BestNotes

- 6.3.10 Planet DDS (NXGN)

- 6.3.11 CloudMD Software

- 6.3.12 TELUS Health

- 6.3.13 Psyquel

- 6.3.14 Behave Inc.

- 6.3.15 Kareo Inc.

- 6.3.16 TheraNest (Counsol.com)

- 6.3.17 SimplePractice

- 6.3.18 Streamline Healthcare Solutions

- 6.3.19 MindLinc (Duke)

- 6.3.20 Allscripts Healthcare Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessmen