|

시장보고서

상품코드

1844701

소수성 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hydrophobic Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

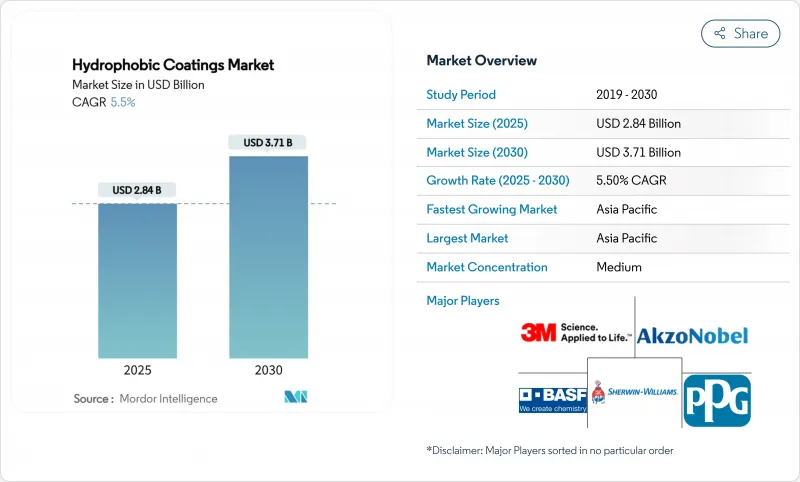

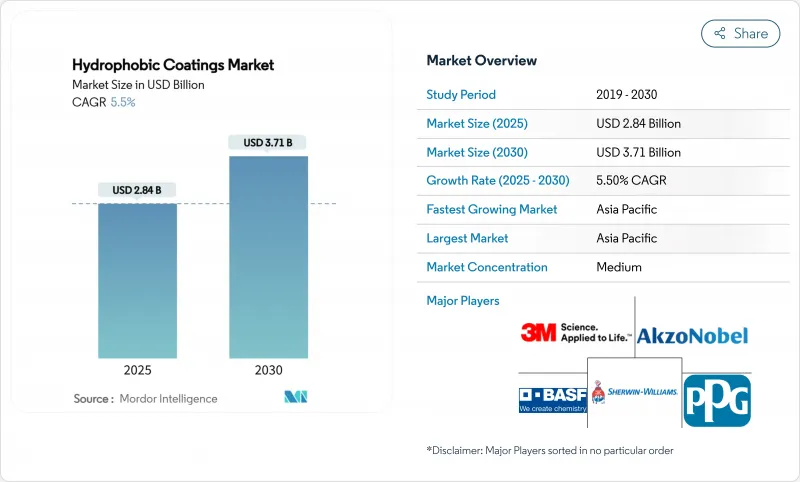

소수성 코팅 시장 규모는 2025년에 28억 4,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.5%를 나타낼 것으로 예측되며 2030년에 37억 1,000만 달러에 이를 전망입니다.

규제 압박으로 불소계 화학물질에서 무불소 화학물질로의 전환이 가속화되고 있으며, 지속적인 인프라 투자, 전자제품 소형화, 의료 수요 증가가 종합적으로 물량 성장을 견인하고 있습니다. 기술 차별화는 이제 기존 불소수지 성능을 따라잡거나 능가하는 실리콘계, 바이오 기반, 나노구조 솔루션에 집중되고 있습니다. 대형 구매사들은 발수성과 함께 부식 방지, 항균, 결빙 방지 특성을 결합한 다기능 제품을 우선시하고 있으며, 이는 광범위한 제형 전문성을 보유한 공급업체에 유리한 추세입니다. 글로벌 화학 대기업들이 사업 매각, 전략적 제휴, 신속한 특허 출원을 통해 민첩한 나노코팅 전문업체들과의 경쟁에서 점유율을 방위함에 따라 경쟁 강도는 중간 수준입니다.

세계의 소수성 코팅 시장 동향 및 인사이트

건설 부문의 강력한 성장

지속적인 도시화와 인프라 재건은 소수성 코팅 시장의 수요를 견인하고 있습니다. 실란 및 실록산 기반 콘크리트 함침은 교량, 터널, 해안 구조물의 염화이온 방지를 위한 표준 기술로 자리잡아 수명을 연장하고 유지보수 비용을 절감합니다. 친환경 건축 인증과의 연계로 지속가능성을 중시하는 공공 프로젝트에서 바이오 기반 발수성 처리가 선호 솔루션으로 자리매김하고 있습니다. 아시아태평양 지역의 스마트시티 프로그램은 기후 변화로 인한 열화를 방지하기 위한 발수성 장벽을 의무화하며 시장 규모를 확대 중입니다. 건설 부문이 2024년 매출에서 차지하는 29.64%의 비중은 자산 수명이 국가 인프라 예산에 직접적인 영향을 미치는 대규모 토목 공사에서 보호 코팅의 필수성을 반영합니다.

자동차산업 수요 증가

자동차 제조업체들은 도장 보호, 자가 세정, 부식 방지 효과를 제공하는 소수성 다기능 코팅으로 전환하고 있습니다. 자가 치유 나노 복합체는 마감 내구성을 향상시키며, 이는 잔존 가치 보존에 관심이 많은 고급 자동차 브랜드가 중시하는 특성입니다. 전동화는 배터리 케이스와 전력 전자 하우징이 습기 침투와 열 사이클링을 견뎌야 하므로 새로운 보호 요소를 추가합니다. VOC 배출 규제 상한선은 수성 발수성 화학물질의 채택을 가속화하여, 공급업체들이 처리량을 희생하지 않으면서도 용매 기반 성능을 재현하도록 압박합니다. 첨단 운전자 보조 센서와 인포테인먼트 디스플레이의 통합은 차량 내부에 초박형, 광학적으로 투명한 방수층을 적용할 기회를 더욱 확대합니다.

복잡한 공정와 높은 초기 투자 비용

초소수성 층 생산은 표면 거칠기와 화학 성분을 정밀하게 제어해야 하며, 종종 불활성 분위기에서 다단계 텍스처링, 기능화 및 경화 공정을 수반합니다. 플라즈마 반응기, 레이저 패터닝 장치 및 정교한 품질 관리 계측 장비에 대한 자본 지출은 중소기업의 재정 부담을 가중시킵니다. 다운스트림 사용자들도 학습 곡선에 직면합니다. 기판 세정, 주변 습도 및 경화 프로파일을 모두 최적화해야 발표된 접촉각 사양을 달성할 수 있습니다. 이러한 복잡성은 신규 진입자의 확장 속도를 제한하여 시장 경쟁을 억제하고, 비용에 민감한 최종 사용 부문에서의 혁신 확산을 잠재적으로 지연시킵니다.

부문 분석

2024년 부식 방지제 제형은 39.18%의 소수성 코팅 시장 점유율을 유지했으며, 이는 해양, 석유 및 가스, 운송 부문에서 철강 및 알루미늄 자산을 보호해야 하는 지속적인 필요성을 반영합니다. 교량 보수 및 해상 풍력 발전 설비 설치 프로젝트의 견고한 수요가 해당 부문 매출을 더욱 공고히 했습니다. 반면, “기타 제품 유형” 군에 속하는 자가 세정 및 방빙 제품은 태양광 O&M 기업들이 PV 모듈에 나노코팅을 적용한 후 최대 15%의 에너지 생산량 증가를 검증함에 따라 6.92%의 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 항공우주 OEM 업체들 역시 방빙액 사용량을 줄여주는 저빙착 표면을 중요하게 여깁니다.

부식 방지 부문은 가격 경쟁력을 유지하고 있으나, 아연 함유 프라이머와 용매형 탑코트에 대한 규제 압박으로 인해 그래핀 또는 세라믹 플레이크가 내장된 수성 하이브리드 제품으로 조달이 전환되고 있습니다. 특수 자가 세정 제품은 건조 지역에 위치한 태양광 발전소의 수동 세정 노동력을 줄일 수 있는 능력 덕분에 더 높은 마진을 확보하고 있습니다. 한편, 소수성 코팅 산업에서는 수동적 발수성과 능동적 태양열 가열을 결합한 광열적 방빙층이 등장하고 있으며, 이는 연료 절감형 제빙 전략을 추구하는 항공사들의 공감을 얻는 하이브리드 접근법입니다.

지역 분석

아시아태평양 지역은 2024년 매출 점유율 48.15%를 유지했으며, 이는 중국의 제조 규모, 인도의 인프라 건설 계획, 일본의 재료 과학 역량에 힘입은 결과입니다. 공공 건물이 친환경 건설 기준을 충족하도록 하는 정부 규제로 인해 저휘발성 유기화합물(VOC) 발수성 제품의 채택이 증가했습니다. 해당 지역의 전자제품 위탁 제조업체들은 글로벌 스마트폰 브랜드로부터 수출 계약을 확보하기 위해 서브마이크론 방수층을 요구하고 있습니다. 동남아시아 태양광 모듈 공장의 지속적인 생산 능력 증설은 공장 가동 시간을 늘리는 자가 세척형 PV 코팅에 대한 수요를 유지하고 있습니다.

북미는 기술적 선도 역할을 수행 중입니다. 미국은 항공우주 및 방위 산업용 고성능 응용 분야를 육성하며, 초소수성 결빙 방지 코팅이 항공사와 군 함대의 운영 비용을 절감합니다. 캐나다의 단계적 PFAS 금지 정책은 불소 무함유 화학 제품에 대한 국내 수요를 증가시켜, 지역 공급업체들이 실리콘 및 폴리우레탄 대체재의 인증 절차를 가속화하도록 촉진하고 있습니다. 멕시코의 자동차 수출 허브는 전기차 배터리 케이스에 소수성 처리를 통합하여 원자재 및 적용 장비의 국경 간 공급망을 강화하고 있습니다.

유럽은 엄격한 환경 정책과 산업 경쟁력을 균형 있게 조율하고 있습니다. 유럽화학물질청(ECHA)이 10,000종 이상의 PFAS 물질 제한을 제안함에 따라 제형 개발사들은 생물 기반 대체재 검증에 박차를 가하고 있습니다. 독일 자동차 1차 공급업체들은 부식 방지성과 도장 공정 배출 목표를 동시에 충족하는 그래핀 강화 수성 탑코트를 공동 개발 중입니다. 북유럽 국가들의 순환경제 모델 선호는 포장용 생분해성 소수성 차단재 수요를 촉진하며, 셀룰로오스 기반 솔루션으로의 혁신을 가속화하고 있습니다. 이처럼 소수성 코팅 시장은 지리적으로 다양한 수요 요인에 힘입어 글로벌 성장 모멘텀을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건설 부문의 견조한 성장

- 자동차 산업에서의 수요 증가

- 가전 분야에서의 채택 증가

- 3D 프린팅을 통한 개조형 초소수성 표면

- 항바이러스성의 공공 인프라용 코팅 수요 증가

- 시장 성장 억제요인

- 복잡한 공정와 높은 초기 투자 비용

- 마모성 환경에서의 내구성 문제

- 장쇄 불소중합체에 대한 금지 조치 임박

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 특허 분석

- 가격 분석

제5장 시장 규모와 성장 예측

- 제품 유형별

- 부식방지

- 항균

- 방오

- 방습

- 기타 제품 유형(자가 세척, 결빙 방지 등)

- 기질별

- 금속

- 세라믹

- 유리

- 콘크리트

- 플라스틱 및 폴리머

- 기타 기질(섬유, 종이, 골판지 등)

- 최종 사용자 산업별

- 건설

- 자동차

- 항공우주

- 전자

- 헬스케어

- 해양

- 기타 최종 사용자 산업(석유 및 가스, 재생에너지 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- AccuCoat Inc.

- Aculon Inc.

- Advanced Nanotech Lab

- AkzoNobel NV

- Arkema

- Artekya Teknoloji

- BASF SE

- COTEC GmbH

- Cytonix, LLC

- Nanofilm

- NeverWet, LLC.

- Nukote Coating Systems International

- P2i Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- UltraTech International, Inc.

제7장 시장 기회와 전망

HBR 25.11.07The Hydrophobic Coatings Market size is estimated at USD 2.84 billion in 2025, and is expected to reach USD 3.71 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

Regulatory pressure has accelerated the transition toward fluorine-free chemistries, while sustained infrastructure investment, electronics miniaturization, and growing healthcare demand collectively reinforce volume growth. Technology differentiation now centers on silicone-, bio-based, and nanostructured solutions that match or exceed legacy fluoropolymer performance. Large buyers are prioritizing multifunctional products that combine water-repellency with anti-corrosion, antimicrobial, and anti-icing attributes, a trend that favors suppliers with broad formulation expertise. Competitive intensity is moderate as global chemical majors defend share against agile nanocoating specialists through divestment, strategic partnerships, and rapid patent filings.

Global Hydrophobic Coatings Market Trends and Insights

Robust Growth of Construction Sector

Sustained urbanization and infrastructure renewal continue to anchor demand in the hydrophobic coatings market. Silane- and siloxane-based concrete impregnation has become standard for chloride-ion protection of bridges, tunnels, and coastal structures, extending service life and lowering maintenance costs. Alignment with green-building certifications positions bio-based hydrophobic treatments as preferred solutions for public projects that emphasize sustainability. Asia-Pacific smart-city programs are amplifying volumes by specifying water-repellent barriers against climate-induced deterioration. The construction segment's 29.64% 2024 revenue share reflects the indispensability of protective coatings in large civil works, where asset longevity directly influences national infrastructure budgets.

Rising Demand from Automotive Industry

Automotive manufacturers have shifted toward hydrophobic multifunctional coatings that deliver paint protection, self-cleaning, and anti-corrosion benefits. Self-healing nanocomposites improve finish durability, an attribute valued by luxury car brands keen on residual-value preservation. Electrification adds new protection points as battery enclosures and power-electronics housings must resist moisture ingress and thermal cycling. Regulatory caps on VOC emissions accelerate water-borne hydrophobic chemistries, pressing suppliers to replicate solvent-based performance without sacrificing throughput. Integration of advanced driver-assistance sensors and infotainment displays further widens opportunities for ultra-thin, optically clear waterproof layers inside vehicles.

Complex Process and High Initial Investment Cost

Producing superhydrophobic layers demands precise control of surface roughness and chemistry, often involving multi-step texturing, functionalization, and curing in inert atmospheres. Capital expenditure on plasma reactors, laser patterning units, and sophisticated QC instrumentation strains the finances of small and mid-size enterprises. Down-line users also face learning curves: substrate cleaning, ambient humidity, and cure profiles must all be optimized to achieve published contact-angle specifications. These complexities restrict the pace at which new entrants can scale, limiting market competition and potentially slowing innovation diffusion in cost-sensitive end-use sectors.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption in Consumer Electronics

- 3-D Printed Retro-fit Superhydrophobic Surfaces

- Durability Challenges Under Abrasive Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anti-corrosion formulations maintained a 39.18% hydrophobic coatings market share in 2024, reflecting the perennial need to safeguard steel and aluminum assets in marine, oil-and-gas, and transport sectors. Robust demand from bridge refurbishment and offshore wind installation projects further anchored segment revenues. In contrast, self-cleaning and ice-phobic products within the "Other Product Types" cluster are forecast to post a 6.92% CAGR, buoyed by solar O&M firms that have validated up to 15% energy-yield gains after applying nanocoatings to PV modules. Aerospace OEMs likewise value low-ice-adhesion surfaces that cut anti-icing fluid usage.

The anti-corrosion sub-sector remains price competitive, yet regulatory pressure on zinc-rich primers and solvent-borne top-coats is shifting procurement toward water-borne hybrids with embedded graphene or ceramic flakes. Specialty self-cleaning products command higher margins due to their ability to reduce manual cleaning labor for solar farms located in arid regions. Meanwhile, the hydrophobic coatings industry is witnessing the emergence of photothermal ice-phobic layers that combine passive water repellence with active sunlight-driven heating, a hybrid approach that resonates with airlines pursuing fuel-saving de-icing strategies.

The Hydrophobic Coatings Market Report is Segmented by Product Type (Anti-Corrosion, Anti-Microbial, Anti-Fouling, Anti-Wetting, and More), Substrate (Metals, Ceramics, Glass, Concrete, and More), End-User Industry (Construction, Automotive, Aerospace, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 48.15% revenue share in 2024, driven by China's manufacturing scale, India's infrastructure pipeline, and Japan's material-science prowess. Government mandates that public buildings meet green-construction benchmarks have boosted uptake of low-VOC hydrophobic products. Electronics contract manufacturers across the region specify sub-micron waterproof layers to secure export contracts from global smartphone brands. Continued capacity additions in Southeast Asian solar module plants sustain demand for self-cleaning PV coatings that increase plant uptime.

North America stands as a technological bellwether. The United States cultivates high-performance aerospace and defense applications, where superhydrophobic anti-icing layers reduce operational costs for airlines and military fleets. Canada's phased PFAS prohibition elevates domestic demand for fluorine-free chemistries, compelling regional suppliers to accelerate the qualification of silicone and polyurethane alternatives. Mexico's automotive export hubs integrate hydrophobic treatments in electric-vehicle battery enclosures, reinforcing cross-border supply chains for raw materials and application equipment.

Europe balances strict environmental policy with industrial competitiveness. The European Chemicals Agency proposal to restrict over 10,000 PFAS substances has triggered a rush among formulators to validate bio-based replacements. Germany's automotive Tier-1 suppliers co-develop graphene-reinforced water-borne top-coats that satisfy both corrosion-resistance and paint-shop emission targets. Nordic nations' preference for circular-economy models stimulates demand for biodegradable hydrophobic barriers in packaging, pushing innovation toward cellulose-based solutions. The hydrophobic coatings market is thus experiencing geographically diverse pull factors that collectively sustain global growth momentum.

- 3M

- AccuCoat Inc.

- Aculon Inc.

- Advanced Nanotech Lab

- AkzoNobel N.V.

- Arkema

- Artekya Teknoloji

- BASF SE

- COTEC GmbH

- Cytonix, LLC

- Nanofilm

- NeverWet, LLC.

- Nukote Coating Systems International

- P2i Ltd.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- UltraTech International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth of construction sector

- 4.2.2 Rising demand from automotive industry

- 4.2.3 Increasing adoption in consumer electronics

- 4.2.4 3-D printed retro-fit superhydrophobic surfaces

- 4.2.5 Increasing demand for anti-viral public-infrastructure coatings

- 4.3 Market Restraints

- 4.3.1 Complex process and high intial investment cost

- 4.3.2 Durability challenges under abrasive environments

- 4.3.3 Impending bans on long-chain fluoropolymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Patent Analysis

- 4.7 Pricing Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Anti-corrosion

- 5.1.2 Anti-microbial

- 5.1.3 Anti-fouling

- 5.1.4 Anti-wetting

- 5.1.5 Other Product Types (Self-cleaning, Ice-phobic, etc.)

- 5.2 By Substrate

- 5.2.1 Metals

- 5.2.2 Ceramics

- 5.2.3 Glass

- 5.2.4 Concrete

- 5.2.5 Plastics and Polymers

- 5.2.6 Other Substrates (Textiles, Paper and Cardboard, etc.)

- 5.3 By End-user Industry

- 5.3.1 Construction

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Electronics

- 5.3.5 Healthcare

- 5.3.6 Marine

- 5.3.7 Other End-user Industries (Oil and Gas, Renewable Energy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AccuCoat Inc.

- 6.4.3 Aculon Inc.

- 6.4.4 Advanced Nanotech Lab

- 6.4.5 AkzoNobel N.V.

- 6.4.6 Arkema

- 6.4.7 Artekya Teknoloji

- 6.4.8 BASF SE

- 6.4.9 COTEC GmbH

- 6.4.10 Cytonix, LLC

- 6.4.11 Nanofilm

- 6.4.12 NeverWet, LLC.

- 6.4.13 Nukote Coating Systems International

- 6.4.14 P2i Ltd.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 UltraTech International, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment