|

시장보고서

상품코드

1844709

자동차 안전 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Safety Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

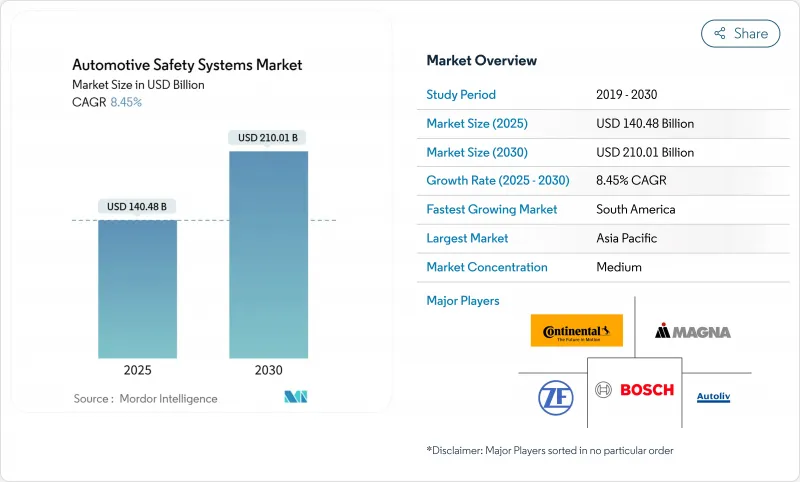

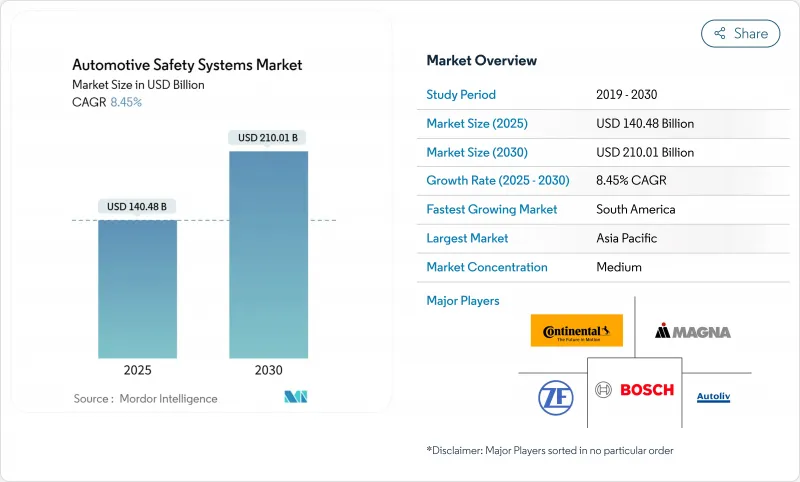

자동차 안전 시스템 시장 규모는 2025년에 1,404억 8,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 8.45%를 나타낼 것으로 예측되며 2030년에 2,100억 1,000만 달러에 이를 전망입니다.

수요는 글로벌 안전 규제의 동시적 진전, 센서 가격의 급격한 하락, 무선 업데이트가 가능한 소프트웨어 정의 차량의 부상을 반영합니다. 하드웨어 기반 제동 장치에서 센서와 소프트웨어가 통합된 플랫폼으로의 전환은 차량이 실시간으로 충돌을 예측, 회피 및 완화할 수 있게 합니다. 자동차 제조사들은 특히 별점 평가 프로그램이 구매 행동에 영향을 미치는 시장에서 능동 제동, 차선 유지, 운전자 모니터링 및 사이버 보안 업데이트 경로를 표준 사양으로 패키징하고 있습니다.

세계의 자동차 안전 시스템 시장 동향 및 인사이트

세계의 NCAP 및 UNECE 안전 규정

2026년 유로 NCAP 프로토콜은 모든 차종에 보행자 자동 긴급 제동 및 운전자 모니터링을 의무화하여 공통 준수 기준을 마련합니다. 중국 산업정보화부는 2025년 안전 기능에 영향을 미치는 모든 소프트웨어 업데이트에 대한 형식 승인을 의무화하는 규정을 도입했습니다. 2024년 7월부터 시행 중인 EU 일반 안전 규정 II(GSE II)는 모든 신차에 지능형 속도 보조 및 긴급 차선 유지 기능을 의무화합니다. 미국 NHTSA는 2026년형 모델을 대상으로 신차 평가 프로그램(NCAP)을 업데이트하여 사각지대 경고, 차선 유지 보조, 보행자 AEB를 추가하며 10년에 걸친 능동 안전 기술 추진을 시사합니다. 글로벌 규격 통합은 제조사들이 개발 비용을 더 큰 판매량에 분산시키고 첨단 기능의 확산을 가속화하는 촉매 역할을 합니다.

ADAS 표준화를 가능케 하는 센서 가격의 급속한 하락

자동차용 레이더 가격은 현재 매년 약 18% 하락하는 반면, 프로세서 성능은 18개월마다 두 배로 증가하여 보급형 가격대에서도 고성능 인식이 가능해졌다. 4차원 이미징 레이더는 기존 3D 장치와 유사한 비용 수준으로 센티미터 단위 감지 정확도를 제공하여 적응형 크루즈 컨트롤을 넘어선 활용 영역을 확장하고 있습니다. 이미지 센서는 스마트폰 공급망의 혜택을 받습니다. HDR 기능이 탑재된 800만 화소 자동차용 칩이 10달러 미만으로 공급됩니다. NITI Aayog는 ADAS 콘텐츠를 중심으로 차량당 반도체 가치가 2030년까지 1,200달러로 두 배 증가할 것으로 전망합니다. 비용 감소 추세로 인해 자동차 안전 시스템 시장은 레벨 1 및 레벨 2 기능을 아시아와 라틴 아메리카에서 판매되는 소형차까지 확대할 수 있습니다.

다국적 규정 준수를 위한 높은 검증 및 인증 비용

제조사들은 중국의 C-NCAP 2024 테스트 매트릭스와 Euro NCAP 2026 요구사항을 조화시켜야 하며, 유사한 시나리오에 대해 충돌 및 소프트웨어 검증을 반복하는 경우가 많다. TUV SUD는 이제 EU 규정에 따라 의무적인 침투 테스트를 수행하여 시장 출시 전 수개월의 사이버 보안 검토를 추가합니다. ISO/SAE 21434는 차량 전체 라이프 사이클에 걸친 위협 분석을 요구하여 개발 일정을 연장시키고 중소 자동차 제조사의 비용을 증가시킵니다. 이러한 요인들은 비용에 민감한 시장에서 첨단 기능의 확산을 늦추며, 규격 조화가 개선될 때까지 자동차 안전 시스템 시장의 일부 성장을 제약합니다.

부문 분석

2024년 기준 능동형 안전 시스템이 자동차 안전 시스템 시장 규모에서 67.13%로 가장 큰 비중을 차지했습니다. 유로 NCAP 및 NHTSA 규정이 강화됨에 따라 자동 긴급 제동, 적응형 크루즈 컨트롤, 차선 유지 보조, 운전자 모니터링 기능이 중급 트림에도 적용되고 있습니다. 공급업체들이 실시간 머신러닝 모델을 실행하는 도메인 컨트롤러를 통해 레이더, 카메라, 라이다 데이터를 통합함에 따라 경쟁 강도가 높아지고 있습니다. 이 부문은 또한 보험사가 충돌 방지 기술을 탑재한 트럭에 대해 보험료 할인을 제공함에 따라 차량 수요의 혜택을 받고 있습니다.

실내 생체 인식 플랫폼은 2030년까지 연평균 8.11%의 성장률로 가장 빠르게 성장하는 하위 부문으로 부상하고 있습니다. 이러한 솔루션은 운전자의 주의력, 심박수, 심지어 산소 포화도까지 추적하여 위험한 상황이 발생하기 전에 사전 경고를 발령합니다. 실내 센서가 능동 제동 제어기와 연동되면 탑승자는 외부 및 내부 위협을 모두 예측하는 폐쇄 루프 안전 보호막을 받게 됩니다. 자율주행차의 새로운 좌석 배열에 맞춰진 스마트 에어백과 적응형 안전벨트를 통해 수동 안전 기술은 여전히 중요하지만 성장세는 완만합니다.

레이더 모듈은 2024년 자동차 안전 시스템 시장의 34.36%를 차지했으며, 비, 눈, 안개 속에서도 안정적으로 작동하는 비용 효율적인 77GHz 칩셋이 이를 뒷받침했습니다. 4D 이미징 레이더로의 전환은 각도 분해능을 높이고 물체 분류를 가능하게 하여, 더 낮은 BOM(Bill of Materials)으로 LiDAR와의 성능 격차를 좁히고 있습니다. 카메라 시스템은 스마트폰 경제성을 지속적으로 활용하여 OEM이 주차 및 저속 주행 시 360도 시야를 추가할 수 있게 합니다.

LiDAR은 고체 상태 아키텍처가 움직이는 부품을 줄이고 센서당 가격을 낮추는 데 힘입어 8.75%의 연평균 성장률(CAGR)로 가장 빠른 확장을 기록합니다. 프리미엄 세단에 도입된 레벨 3 고속도로 자율 주행 시스템은 중복 깊이 인식 및 도로 잔해 감지를 위해 전방 장착형 라이더에 의존하며, 이는 채택을 가속화합니다. 제어 장치는 제동, 조향, 인식 데이터를 단일 칩으로 통합하여 배선과 무게를 줄입니다. 자동차 안전 시스템 시장이 예측 안전으로 전환됨에 따라, 에지 프로세서에 자체 학습 알고리즘을 적용하는 소프트웨어 혁신이 공급업체 간 차별화 요소로 부상하고 있습니다.

지역 분석

아시아태평양 지역은 2024년 자동차 안전 시스템 시장에서 39.84%의 점유율로 최대 지역 위치를 유지했습니다. 중국의 MIIT(산업정보기술부) 규정은 모든 ADAS 소프트웨어 업데이트에 대한 강제 승인을 요구하여 기능 출시를 가속화하는 강력한 규정 준수 생태계를 조성합니다. 기술 - 자동차 융합은 화웨이와 엑스펑(Xpeng)의 협력 사례처럼 공통 소프트웨어 스택에 레이더, 카메라, 라이다를 통합하는 도메인 컨트롤러를 공동 개발하는 형태로 나타납니다. 일본은 도시 중심부를 위한 자율주행 셔틀을 시범 운영하는 AI 기반 스타트업을 육성하는 반면, 인도의 강화된 충돌 규정은 소형차용 비용 최적화 에어백 및 AEB 수요를 촉진합니다.

남미는 2030년까지 연평균 8.77% 성장률로 가장 높은 성장세를 기록할 전망입니다. 스텔란티스는 2025년부터 2030년까지 56억 유로를 투자해 현지 공장에서 유로 NCAP 테스트 프로토콜을 준수하는 40여 개 모델을 출시할 계획입니다. 브라질, 아르헨티나 및 인접 시장들은 안전 규정을 조화시켜 글로벌 공급업체들이 맞춤형 튜닝 없이 검증된 센서 패키지를 복제할 수 있도록 합니다. 에탄올 엔진과 배터리 팩을 결합한 바이오 하이브리드 파워트레인은 열 및 전기 안전 시스템에 새로운 통합 과제를 제시합니다.

북미와 유럽은 높은 차량당 적용률과 소프트웨어 정의 차량 규제로 성숙한 위치를 유지합니다. 해당 지역의 자동차 안전 시스템 시장 점유율은 안정적이지만, UNECE 규정 155호가 완전한 사이버보안을 의무화하며 모든 안전 ECU가 해킹 방지 기준을 충족하도록 함에 따라 단위당 가치는 상승합니다. 중동 및 아프리카 지역은 인프라 확장에 힘입어 낮은 기준선에서 발전하고 있으나, 극한의 지역 기후로 인해 견고한 센서 하우징과 방진 레이더 인클로저에 대한 수요가 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 강화되는 세계의 NCAP 및 UNECE 안전 규정

- ADAS 표준화를 가능케 하는 센서 비용의 급속한 하락

- 소프트웨어 정의 차량의 급증(OTA 안전 기능 업그레이드)

- 상용차의 레벨 2 자율성으로의 시프트(플릿 TCO 플레이)

- AI 기반 실내 생체 인식 안전 분석 기술의 부상(피로도, 생체 신호)

- 차량 안전 데이터의 사용량 기반 통합

- 시장 성장 억제요인

- 다국적 규정 준수를 위한 높은 검증 및 인증 비용

- 칩셋 공급 불안정으로 인한 OEM 안전 기능 출시 지연

- 안전 ECU와 센서 버스에 대한 사이버 물리 공격 위험

- 800V 배터리 전기차의 고전압 전자기 간섭(EMI) 및 열 부하

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 시스템 유형별

- 능동형 안전 시스템

- 충돌 방지(AEB, FCW)

- 운전자 모니터링 및 HMI 경고

- 차체 제어 (ESC, ABS)

- 수동형 안전 시스템

- 에어백(프런트, 사이드, 커튼, 퍼 사이드)

- 안전벨트&프리텐셔너

- 능동형 안전 시스템

- 기술 컴포넌트별

- 센서

- 레이더

- 카메라

- LiDAR/초음파

- 컨트롤 유닛과 도메인 컨트롤러

- 소프트웨어 및 알고리즘

- 최종 사용자별

- OEM

- 애프터마켓/개조

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차 및 버스

- 추진력별

- 내연기관(ICE)

- 배터리 전기자동차(BEV)

- 하이브리드 전기자동차(HEV)

- 연료전지 전기자동차(FCEV)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Joyson Safety Systems

- Mobileye NV

- Valeo SA

- Hitachi Astemo

- Hyundai Mobis

- NXP Semiconductors

- Infineon Technologies AG

- Texas Instruments Inc.

- Renesas Electronics Corp.

- Veoneer AB

- WABCO(ZF CV Systems)

- Bendix Commercial Vehicle Systems

- Lear Corporation(E-Systems)

제7장 시장 기회와 전망

HBR 25.11.07The Automotive Safety Systems Market size is estimated at USD 140.48 billion in 2025, and is expected to reach USD 210.01 billion by 2030, at a CAGR of 8.45% during the forecast period (2025-2030).

Demand reflects simultaneous progress in global safety regulation, rapid sensor price erosion, and the rise of software-defined vehicles that permit over-the-air upgrades. The shift from hardware-only restraint devices toward integrated sensor-plus-software platforms allows vehicles to predict, avoid, and mitigate collisions in real time. Automakers now package active braking, lane keeping, driver monitoring, and cyber-secure update pathways as standard content, especially in markets where star-rating programs influence buying behavior.

Global Automotive Safety Systems Market Trends and Insights

Tightening Global NCAP & UNECE Safety Mandates

Euro NCAP protocols for 2026 require pedestrian automatic emergency braking and driver monitoring across all model classes, creating a common compliance baseline. China's Ministry of Industry and Information Technology introduced rules in 2025 that obligate type approval for every software update touching safety functions. The EU General Safety Regulation II, in force since July 2024, obliges intelligent speed assistance and emergency lane keeping on every new vehicle. NHTSA updated its New Car Assessment Program to add blind-spot warning, lane keeping assistance, and pedestrian AEB for 2026 models, signaling a decade-long push for active safety. Global alignment lets manufacturers spread development cost across larger volumes and catalyzes faster diffusion of advanced functions.

Rapid Sensor-Cost Deflation Enabling ADAS Standardisation

Automotive radar prices now fall nearly 18% each year, while processor capability doubles every 18 months, permitting high-performance perception at entry-segment price points. Four-dimensional imaging radar brings centimeter-grade detection accuracy at cost levels close to legacy 3-D units, broadening use beyond adaptive cruise control. Image sensors benefit from smartphone supply chains: 8-megapixel automotive chips with HDR are available below USD 10. NITI Aayog projects semiconductor value per vehicle to double to USD 1,200 by 2030, led by ADAS content. The declining cost curve allows the automotive safety system market to extend Level-1 and Level-2 features to compact cars sold in Asia and Latin America.

High Validation & Homologation Cost for Multicountry Compliance

Manufacturers must reconcile China's C-NCAP 2024 test matrix with Euro NCAP 2026 requirements, often repeating crash and software validation for similar scenarios. TUV SUD now runs mandatory penetration testing under EU rules, adding months of cybersecurity reviews before market release. ISO/SAE 21434 demands threat analysis across the full vehicle lifecycle, lengthening development schedules and raising costs for small automakers. These factors slow the spread of cutting-edge features in cost-sensitive markets, restraining part of the automotive safety system market until harmonisation improves.

Other drivers and restraints analyzed in the detailed report include:

- Boom in Software-Defined Vehicles (OTA Safety Feature Upgrades)

- Shift Toward Level-2+ Autonomy in Commercial Vehicles (Fleet TCO Play)

- Chip-Set Supply Volatility Delaying OEM Safety Roll-Outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active Safety Systems generated the largest slice of the automotive safety system market size at 67.13% in 2024. Automated emergency braking, adaptive cruise, lane keeping, and driver monitoring now appear in mid-range trims as Euro NCAP and NHTSA protocols grow stricter. Competitive intensity rises as suppliers integrate radar, camera, and LiDAR data through domain controllers that run machine-learning models in real time. The segment also benefits from fleet demand, with insurers offering premium discounts for trucks equipped with crash-avoidance technology.

In-cabin biometric platforms stand out as the fastest subsegment, advancing at an 8.11% CAGR to 2030. These solutions track driver alertness, heart rate, and even oxygen saturation, issuing proactive warnings before dangerous conditions emerge. As cabin sensors link with active braking controllers, occupants receive a closed-loop safety envelope that anticipates both external and internal threats. Passive safety remains relevant through smart airbags and adaptive seat belts that fit new seat layouts in autonomous vehicles, yet growth stays moderate.

Radar modules accounted for 34.36% of the automotive safety system market in 2024, underpinned by cost-effective 77-GHz chipsets that function reliably in rain, snow, and fog. The move to 4-D imaging radar sharpens angle resolution and permits object classification, narrowing the performance gap with LiDAR at a lower bill of materials. Camera systems continue to leverage smartphone economics, letting OEMs add 360-degree vision for parking and low-speed manoeuvres.

LiDAR registers the quickest expansion at an 8.75% CAGR, supported by solid-state architectures that trim moving parts and cut price per sensor. Level-3 highway-pilot launches in premium sedans rely on forward-facing LiDAR for redundant depth perception and road debris detection, accelerating adoption. Control units merge braking, steering, and perception data into single chips, reducing wiring and weight. Software innovations that apply self-learning algorithms on edge processors differentiate suppliers as the automotive safety system market transitions toward predictive safety.

The Automotive Safety System Market Report is Segmented by System Type (Active Safety Systems and Passive Safety Systems), Technology Component (Sensors, Radar, Camera, and More), End User (OEM and Aftermarket), Vehicle Type (Passenger Car, Light Commercial Vehicle, and More), Propulsion (ICE, Battery-Electric Vehicles, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific retained the largest regional position with 39.84% share of the automotive safety system market in 2024. China's MIIT rules compelling approval for every ADAS software update foster a robust compliance ecosystem that speeds feature rollout. Technology - auto convergence appears in partnerships such as Huawei and Xpeng, which co-develop domain controllers integrating radar, camera, and LiDAR on a common software stack. Japan nurtures AI-driven start-ups that pilot autonomous shuttles for urban centres, while India's tighter crash regulations boost demand for cost-optimised airbags and AEB in compact cars.

South America posts the highest growth, advancing at an 8.77% CAGR through 2030. Stellantis committed EUR 5.6 billion between 2025 and 2030 to launch more than 40 models from local plants, each aligned with Euro NCAP test protocols. Brazil, Argentina, and neighbouring markets harmonise safety laws, letting global suppliers replicate validated sensor suites without custom tuning. Bio-hybrid powertrains that blend ethanol engines with battery packs open fresh integration tasks for thermal and electrical safety systems.

North America and Europe uphold mature positions with high per-vehicle content and software-defined vehicle regulations. The automotive safety system market share in these regions remains stable, yet value per unit rises as UNECE Regulation 155 enforces full cybersecurity, obliging every safety ECU to meet anti-hacking standards. The Middle East and Africa progress from low baselines, stimulated by infrastructure expansion, yet local climate extremes drive demand for robust sensor housings and dust-proof radar enclosures.

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Joyson Safety Systems

- Mobileye N.V.

- Valeo SA

- Hitachi Astemo

- Hyundai Mobis

- NXP Semiconductors

- Infineon Technologies AG

- Texas Instruments Inc.

- Renesas Electronics Corp.

- Veoneer AB

- WABCO (ZF CV Systems)

- Bendix Commercial Vehicle Systems

- Lear Corporation (E-Systems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening global NCAP & UNECE safety mandates

- 4.2.2 Rapid sensor-cost deflation enabling ADAS standardisation

- 4.2.3 Boom in software-defined vehicles (OTA safety feature upgrades)

- 4.2.4 Shift toward Level-2+ autonomy in commercial vehicles (fleet TCO play)

- 4.2.5 Rise of AI-based in-cabin biometric safety analytics (fatigue, vitals)

- 4.2.6 Bundling of vehicle-safety data into Usage

- 4.3 Market Restraints

- 4.3.1 High validation & homologation cost for multicountry compliance

- 4.3.2 Chip-set supply volatility delaying OEM safety roll-outs

- 4.3.3 Cyber-physical attack risk on safety ECUs & sensor buses

- 4.3.4 High-voltage electromagnetic interference (EMI) and thermal loads in 800-V battery-electric

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By System Type

- 5.1.1 Active Safety Systems

- 5.1.1.1 Collision-Avoidance (AEB, FCW)

- 5.1.1.2 Driver Monitoring & HMI Alerts

- 5.1.1.3 Chassis Control (ESC, ABS)

- 5.1.2 Passive Safety Systems

- 5.1.2.1 Airbags (Frontal, Side, Curtain, Far-side)

- 5.1.2.2 Seat-belt & Pretensioners

- 5.1.1 Active Safety Systems

- 5.2 By Technology Component

- 5.2.1 Sensors

- 5.2.2 Radar

- 5.2.3 Camera

- 5.2.4 LiDAR/Ultrasonic

- 5.2.5 Control Units and Domain Controllers

- 5.2.6 Software & Algorithms

- 5.3 By End-User

- 5.3.1 OEM Factory-Fit

- 5.3.2 Aftermarket / Retrofit

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles & Buses

- 5.5 By Propulsion

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Battery-Electric Vehicles (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Autoliv Inc.

- 6.4.5 Denso Corporation

- 6.4.6 Aptiv PLC

- 6.4.7 Magna International Inc.

- 6.4.8 Joyson Safety Systems

- 6.4.9 Mobileye N.V.

- 6.4.10 Valeo SA

- 6.4.11 Hitachi Astemo

- 6.4.12 Hyundai Mobis

- 6.4.13 NXP Semiconductors

- 6.4.14 Infineon Technologies AG

- 6.4.15 Texas Instruments Inc.

- 6.4.16 Renesas Electronics Corp.

- 6.4.17 Veoneer AB

- 6.4.18 WABCO (ZF CV Systems)

- 6.4.19 Bendix Commercial Vehicle Systems

- 6.4.20 Lear Corporation (E-Systems)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment