|

시장보고서

상품코드

1844712

실리콘 오일 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Silicone Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

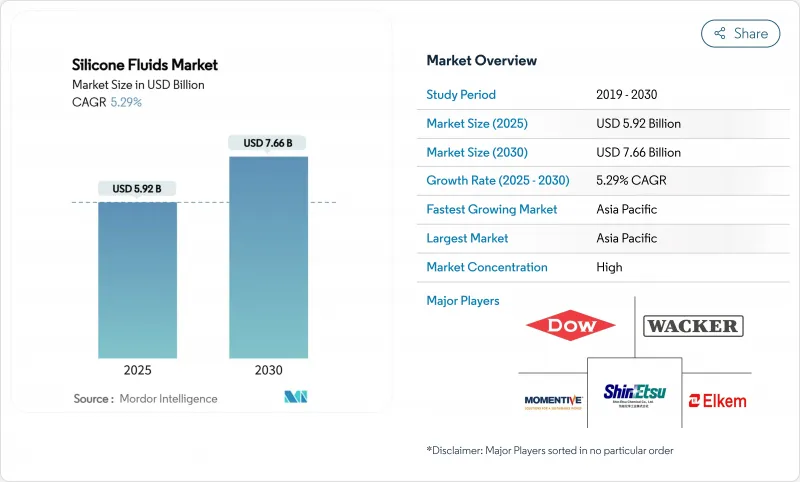

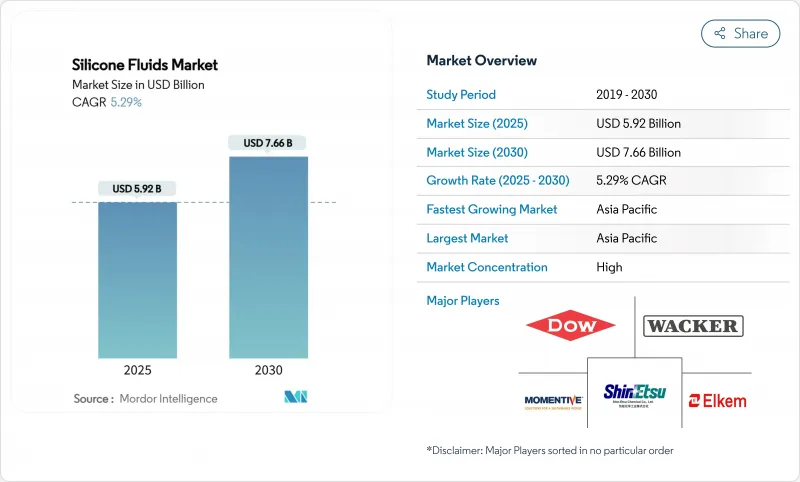

실리콘 오일 시장 규모는 2025년에 59억 2,000만 달러로 평가되었고, 2030년에 76억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 5.29%를 나타낼 전망입니다.

이러한 고성능 폴리머에 대한 수요는 OEM 및 제형 개발업체들이 극한 온도에서도 안정성을 유지하고 산화에 저항하며 전자기기를 절연하는 유체를 찾는 가운데 증가하고 있습니다. 이는 기존 광물성 또는 합성 탄화수소계 유체로는 따라잡을 수 없는 성능입니다. 전기 모빌리티로의 가속화된 전환, 하이퍼스케일 데이터 센터의 부상, 그리고 제조업체들이 더 안전하고 지속 가능한 화학 물질로 전환하도록 유도하는 규제 움직임이 성장을 더욱 강화하고 있습니다. 원자재 가격 변동성과 강화되는 환경 기준이 성장세를 다소 누그러뜨리지만, 실리콘 오일 시장은 수직 통합 추진, 재활용 투자, 틈새 응용 분야 혁신의 혜택을 지속적으로 누리고 있습니다. 이러한 요소들이 종합적으로 작용하여 향후 5년간 실리콘 오일 시장은 중간 단일 자릿수 성장률을 유지할 것으로 전망됩니다.

세계의 실리콘 오일 시장 동향 및 인사이트

퍼스널케어 및 화장품에서의 수요 증가

제형 개발자들은 감각적 매력과 지속가능성을 결합한 차세대 소재로 규제 대상인 고리형 실리콘을 신속히 대체하고 있습니다. 실테크(Siltech)의 바이오 기반 알킬 디메티콘은 퍼짐성을 개선하면서 신규 화석 원료 의존도를 낮춥니다. CHT 그룹의 보실 RE-AMO 919 EM은 94% 이상의 재활용 단량체를 함유하여 유연성을 저하시키지 않으면서 순환 경제 목표를 충족합니다. 아시아태평양 지역의 중산층 인구 확대는 프리미엄 다기능 피부 및 헤어 케어 제품에 대한 수요를 촉진하며, 단일 혼합으로 컨디셔닝, 장벽 기능, 광택 효과를 제공하는 실리콘 오일 수요를 부추기고 있습니다. 브랜드가 제품 포트폴리오를 축소함에 따라 다기능성은 핵심 차별화 요소가 되며, 탄소 발자국 감소를 입증할 수 있는 공급업체가 선호 공급업체 지위를 획득합니다.

전기자동차용 열관리액 채택 증가

액체 냉각 배터리 팩에는 열폭주를 억제하면서도 열을 효율적으로 전달하는 절연 유체가 필요합니다. 루브리졸의 평생 충전형 실리콘 냉각제는 전기차 배터리 팩의 전체 수명 동안 안정성을 유지함으로써 이러한 변화를 대표합니다. 중국에서 곧 시행될 GB 29743.2 전도도 기준은 기존 글리콜-물 혼합물이 충족할 수 없는 높은 기준을 설정하여 자동차 제조업체들이 실리콘 기반 제형으로 전환하도록 유도하고 있습니다. 배터리 외에도 와이드 밴드갭 인버터, 전기 모터, 충전 시스템 역시 실리콘 오일의 넓은 작동 온도 범위의 혜택을 받습니다. 상류 부문에서는 전기차 성장과 연계된 실리콘 금속 수요가 2030년까지 연간 4.56% 증가할 전망으로, 원료 공급을 확보할 수 있는 수직 통합 생산업체에 유리합니다.

불안정한 금속 규소와 단량체 가격

중국은 전 세계 실리콘 금속 생산량의 약 4분의 3을 장악하고 있어 실리콘 오일 시장에 단일 국가 리스크가 파급됩니다. 에너지 가격 급등, 생산 제한, 지정학적 마찰은 현물 가격을 요동치게 하여 다운스트림 제형사의 예산 편성을 방해합니다. 미국은 인플레이션 감축법(IRA)에 따라 국내 제련소 프로젝트를 장려하고 있으나, 신규 생산 능력은 2030년 이전에 실질적으로 가동되기 어려울 전망입니다. 이에 생산사들은 장기 공급 계약으로 헤지하고 역방향 통합을 검토 중인데, 이는 중견 기업들이 감당하기 어려운 자본 투자를 요구합니다.

부문 분석

개질 등급은 비개질 등급보다 빠르게 성장하며, 제형사가 맞춤형 측쇄, 반응성 부위 또는 가교 가능 그룹을 가진 실록산을 지정함에 따라 연평균 복합 성장률(CAGR) 6.84%를 기록하고 있습니다. 이러한 맞춤형 분자는 기판에 선택적으로 결합하거나 접착력을 강화하거나 소수성 표면을 생성하여 최종 사용자가 과도한 설계 없이 성능 목표를 달성할 수 있게 합니다. 전기차(EV) 포팅, 컨포멀 코팅, 고신축성 텍스타일 잉크 분야에서 수요가 두드러집니다. 그럼에도 불구하고 일반 폴리디메틸실리콘(PDMS) 등급은 비용 효율성과 광범위한 사양 적용으로 여전히 물량 주도권을 유지하고 있습니다. 해당 공급망은 성숙했으며, 연속 공정 병목 현상 해소로 단위 비용이 추가로 감소하고 있습니다.

지속 가능한 생산을 둘러싼 경쟁이 격화되고 있습니다. 다우(Dow)와 서커실(Circusil)의 합작사는 PDMS 탄소 발자국을 50% 이상 절감할 수 있는 재활용 루프를 도입했습니다. 바커(Wacker)는 2025년 5월 중국에 신규 유체 및 에멀젼 생산라인을 가동하며 차세대 전자제품을 겨냥한 고순도 생산 능력을 추가했습니다. KCC의 2024년 모멘티브 인수는 상류 실록산 단량체부터 하류 특수 유체까지 수직적 사업 영역을 확장합니다. 순환 경제 목표가 강화됨에 따라 폐쇄형 순환 체계 역량을 보유한 생산업체들은 범주 3 배출량 감축 인증을 원하는 글로벌 OEM사들로부터 공급 계약 우선권을 얻고 있습니다.

실리콘 오일 시장 보고서는 제품 유형(일반 실리콘 오일 및 개질 실리콘 오일), 응용 분야(윤활유 및 그리스, 감쇠 매체, 액체 유전체, 유압유, 소포제, 퍼스널케어, 도료 및 코팅 첨가제, 섬유, 제약, 기타 응용 분야), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

지역 분석

아시아태평양 지역은 실리콘 금속 제련부터 완제품 제형에 이르는 통합 공급망을 활용하여 실리콘 오일 시장을 주도하고 있습니다. 중국의 비용 우위와 75%에 달하는 원자재 통제력이 이 지역의 리더십을 공고히 하는 한편, 일본과 한국은 초순도 유전체 유체가 필요한 소형 전자제품 및 메모리 반도체 분야에서 우위를 점하고 있습니다. 동남아시아는 제조업의 대안 지역으로 부상 중이며, 베트남과 태국은 특수화학 복합단지를 위한 외국인 직접 투자를 유치하고 있습니다. 인도는 국내 자동차 산업 확장과 퍼스널케어 시장 확대에 힘입어 현지 판매가 두 자릿수 증가를 기록하고 있습니다.

북미는 다른 역학 관계를 보여줍니다. 미국은 핵심 광물에 대한 공급망 국내 복귀를 주도하는 한편, 데이터센터 및 전기차(EV) 확장이 특수 유체 수요를 촉진하고 있습니다. 미시간주에서 실리콘 엘라스토머 생산 능력을 확대한 다우는 짧은 리드 타임을 원하는 지역 고객을 지원합니다. 엑슨모빌은 텍사스에 고점도 합성 기유 생산 능력을 추가하며 프리미엄 기능성 유체의 산업적 수용 확대를 시사했습니다. 캐나다는 수소 기반 금속용 실리콘을 공급하며, 멕시코의 마킬라도라 회랑은 전자제품 조립 및 자동차 배선 하네스 생산용 유체를 유치합니다.

유럽은 가장 엄격한 규제 장벽에 직면하면서도 여전히 혁신의 중심지 역할을 합니다. 바커는 2025년 실리콘 사업부 매출이 10% 성장할 것으로 전망합니다. 특수 등급 제품이 일반 제품 판매량 감소를 상쇄할 전망입니다. 독일 엔지니어링 기업들은 공작기계용 실리콘 감쇠 매체를 지정하고 있으며, 프랑스 화장품 기업들은 임박한 포장 및 탄소 발자국 규제를 충족하기 위해 업사이클링 실리콘 원료를 선도적으로 도입하고 있습니다. 북유럽 유틸리티 기업의 친환경 전력 매트릭스는 순환형 제조 주장의 신뢰성을 높여, 실리콘 오일 제조사들이 기술적 성능과 함께 환경적 가치를 판매하는 데 기여하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 퍼스널케어 및 화장품에서의 수요 증가

- 전기자동차의 열 관리용 유체에 있어서의 채택 증가

- 산업 자동화를 위한 고성능 윤활유 시장 성장

- 하이퍼스케일 데이터 센터의 액체 침지 냉각

- 생장촉진제 혼합물을 위한 정밀 농업용 소포제

- 시장 성장 억제요인

- 금속 규소와 단량체 가격의 변동

- 엄격한 VOC 및 REACH 규정 준수 비용

- 원료 실록산 분야의 높은 공급업체 집중도

- 밸류체인 분석

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 일반 실리콘 오일

- 폴리디메틸실리콘 오일

- 메틸페닐실리콘 오일

- 메틸하이드로젠 실리콘

- 기타 일반 실리콘

- 개질 실리콘 오일

- 반응성 실리콘 오일

- 비반응성 실리콘 오일

- 일반 실리콘 오일

- 용도별

- 윤활유 및 그리스

- 감쇠 매체

- 액체 유전체

- 유압작동유

- 소포제

- 퍼스널케어

- 도료 및 코팅 첨가제

- 섬유 마무리

- 의약품

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BRB International BV

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- GELEST Inc.

- Innospec Inc.

- IOTA silicone

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- Wacker Chemie AG

- Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

제7장 시장 기회와 전망

HBR 25.11.07The Silicone Fluids Market size is estimated at USD 5.92 billion in 2025, and is expected to reach USD 7.66 billion by 2030, at a CAGR of 5.29% during the forecast period (2025-2030).

Demand for these high-performance polymers is climbing as OEMs and formulators look for fluids that stay stable under extreme temperatures, resist oxidation, and insulate electronics-capabilities that conventional mineral or synthetic hydrocarbons cannot match. Growth is further reinforced by the accelerating shift to electric mobility, the rise of hyperscale data centers, and regulatory moves that push manufacturers toward safer, more sustainable chemistries. Although raw-material volatility and tightening environmental standards temper momentum, the silicone fluids market continues to benefit from vertical integration initiatives, recycling investments, and niche-application innovation. Collectively, these forces position the silicone fluids market for steady mid-single-digit expansion over the next five years.

Global Silicone Fluids Market Trends and Insights

Rising Demand from Personal Care and Cosmetics

Formulators are moving quickly to replace restricted cyclic silicones with next-generation materials that marry sensory appeal and sustainability. Bio-based alkyl dimethicones from Siltech improve spreadability while cutting reliance on virgin fossil feedstocks. CHT Group's BeauSil RE-AMO 919 EM incorporates over 94% recycled monomers to meet circular-economy targets without sacrificing emolliency. Expanding middle-class populations in Asia-Pacific are embracing premium multifunctional skin- and hair-care products, spurring demand for silicone fluids that deliver conditioning, barrier, and gloss benefits in a single blend. As brands tighten product portfolios, multifunctionality becomes a critical differentiator, and suppliers able to document lower carbon footprints gain preferred-supplier status.

Increasing Adoption in Electric Vehicle Thermal-Management Fluids

Liquid-cooled battery packs need dielectric fluids that suppress thermal runaway yet transfer heat efficiently. Lubrizol's lifetime-fill silicone coolant exemplifies this shift by remaining stable for the full service life of an EV battery pack. China's forthcoming GB 29743.2 conductivity threshold sets a high bar that conventional glycol-water blends cannot meet, steering automakers toward silicone-based formulations. Beyond batteries, wide-bandgap inverters, e-motors, and charging systems also benefit from the broad operating-temperature band of silicone fluids. Upstream, silicon metal demand tied to EV growth is rising 4.56% annually through 2030, rewarding vertically integrated producers that can secure raw supply.

Volatile Silicon Metal and Monomer Prices

China controls roughly three-quarters of the world's silicon metal output, creating a single-country risk that cascades through the silicone fluids market. Energy-price spikes, production curbs, and geopolitical frictions swing spot quotes, disrupting budgeting for downstream formulators. The United States is incentivizing domestic smelter projects under the Inflation Reduction Act, yet new capacity will not meaningfully come onstream before 2030. In the meantime, producers hedge with long-term supply contracts and evaluate backward integration, actions that demand capital many mid-sized players cannot muster.

Other drivers and restraints analyzed in the detailed report include:

- Growth in High-Performance Lubricants for Industrial Automation

- Liquid-Immersion Cooling of Hyperscale Data Centres

- Stringent VOC and REACH Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modified grades are expanding faster than unmodified counterparts, charting a 6.84% CAGR as formulators specify siloxanes with tailored side-chains, reactive sites, or crosslinkable groups. These custom molecules bond selectively to substrates, boost adhesion, or create hydrophobic surfaces, letting end-users hit performance targets without over-engineering. Demand is prominent in EV potting, conformal coatings, and high-flex textile inks. Straight polydimethyl-silicone grades nevertheless maintain volume leadership due to cost efficiency and broad spec inclusion. Their supply chains are mature, and continuous-process debottlenecking further reduces unit cost.

Competition is intensifying around sustainable production. Dow's joint venture with Circusil brings a recycling loop able to cut PDMS carbon footprint by more than 50%. Wacker commissioned new Chinese fluid and emulsion lines in May 2025, adding high-purity capacity aimed at next-gen electronics. KCC's 2024 purchase of Momentive broadens vertical reach from upstream siloxane monomers to downstream specialty fluids. As circular-economy targets harden, producers with closed-loop capabilities gain supply-award preference from global OEMs keen to certify Scope 3 reductions.

The Silicone Fluids Market Report is Segmented by Product Type (Straight Silicone Fluid and Modified Silicone Fluid), Application (Lubricants and Greases, Damping Media, Liquid Dielectrics, Hydraulic Fluids, Defoamers, Personal Care, Paints and Coating Additives, Textile, Pharmaceuticals, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific dominates the silicone fluids market, leveraging integrated supply chains that begin with silicon metal smelting and culminate in finished formulations. China's cost advantage and 75% raw-material control anchor the region's leadership, while Japan and South Korea champion miniaturized electronics and memory semiconductors that require ultra-pure dielectric fluids. Southeast Asia is emerging as a manufacturing hedge, with Vietnam and Thailand courting foreign direct investment for specialty-chemical complexes. India, supported by domestic automotive build-out and an expanding personal-care sector, records double-digit local sales increases.

North America presents a different dynamic. The United States orchestrates supply-chain onshoring for critical minerals, while datacenter and EV build-outs propel specialty-fluid demand. Dow's capacity expansion for silicone elastomers in Michigan supports regional customers seeking short lead times. ExxonMobil added high-viscosity synthetic base-stock capacity in Texas, signaling wider industrial acceptance of premium functional fluids. Canada supplies hydro-based metallurgical-grade silicon, and Mexico's maquiladora corridor pulls in fluids for electronics assembly and automotive wiring harness production.

Europe contends with the strictest regulatory hurdles yet remains an innovation epicenter. Wacker forecasts 10% revenue growth in its Silicones division for 2025 as specialty grades offset lower commodity volumes. Germany's engineering companies specify silicone damping media for machine tools, while France's cosmetic houses pioneer upcycled silicone ingredients to meet imminent packaging and carbon-footprint rules. Nordic utilities' green-power matrices lend credibility to circular-manufacturing claims, helping silicone fluid makers sell environmental value alongside technical performance.

- BRB International B.V.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- GELEST Inc.

- Innospec Inc.

- IOTA silicone

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- Wacker Chemie AG

- Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from personal care and cosmetics

- 4.2.2 Increasing adoption in electric vehicle thermal-management fluids

- 4.2.3 Growth in high-performance lubricants for industrial automation

- 4.2.4 Liquid-immersion cooling of hyperscale data centres

- 4.2.5 Precision agriculture anti-foam agents for biostimulant mixtures

- 4.3 Market Restraints

- 4.3.1 Volatile silicon metal and monomer prices

- 4.3.2 Stringent VOC and REACH compliance costs

- 4.3.3 High supplier concentration in raw siloxanes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Straight Silicone Fluids

- 5.1.1.1 Poly-dimethyl Silicone Fluid

- 5.1.1.2 Methylphenyl Silicone Fluid

- 5.1.1.3 Methylhydrogen Silicone Fluid

- 5.1.1.4 Other Straight Silicone Fluids

- 5.1.2 Modified Silicone Fluids

- 5.1.2.1 Reactive Silicone Fluid

- 5.1.2.2 Non-reactive Silicone Fluid

- 5.1.1 Straight Silicone Fluids

- 5.2 By Application

- 5.2.1 Lubricants and Greases

- 5.2.2 Damping Media

- 5.2.3 Liquid Dielectrics

- 5.2.4 Hydraulic Fluids

- 5.2.5 Defoamers

- 5.2.6 Personal Care

- 5.2.7 Paints and Coating Additives

- 5.2.8 Textile Finishes

- 5.2.9 Pharmaceuticals

- 5.2.10 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BRB International B.V.

- 6.4.2 CHT Germany GmbH

- 6.4.3 Dow

- 6.4.4 DuPont

- 6.4.5 Elkem ASA

- 6.4.6 GELEST Inc.

- 6.4.7 Innospec Inc.

- 6.4.8 IOTA silicone

- 6.4.9 KCC SILICONE CORPORATION

- 6.4.10 Momentive

- 6.4.11 Shin-Etsu Chemical Co., Ltd.

- 6.4.12 Siltech Corporation

- 6.4.13 Supreme Silicones India Pvt. Ltd.

- 6.4.14 Wacker Chemie AG

- 6.4.15 Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment