|

시장보고서

상품코드

1844719

풍력 터빈 복합재료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wind Turbine Composite Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

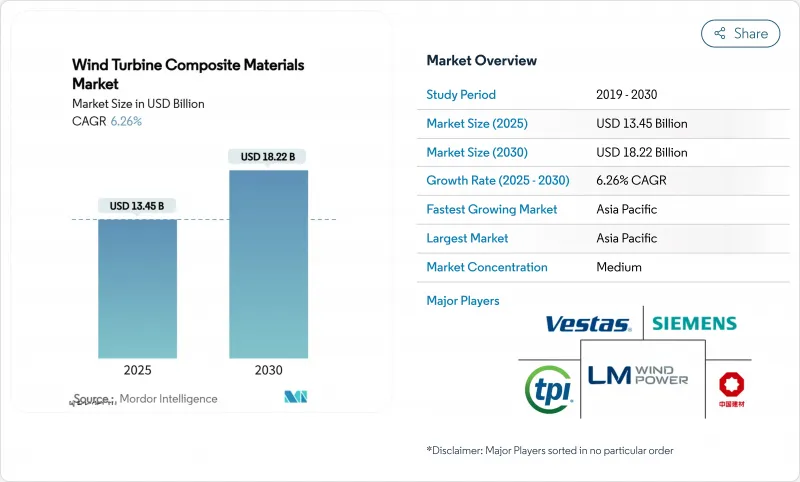

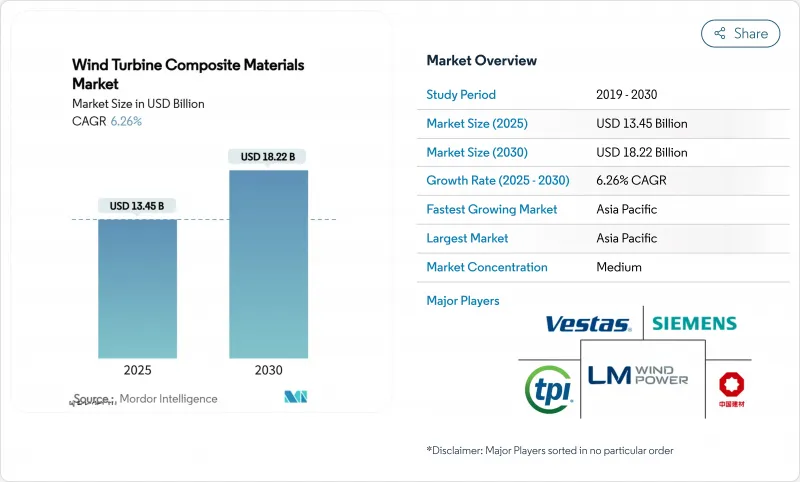

풍력터빈 복합재료 시장 규모는 2025년 134억 5,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 6.26%를 나타낼 것으로 예측되며 2030년에 182억 2,000만 달러에 이를 전망입니다.

100m 이상의 블레이드 보급이 확대되면서 경량 유리섬유, 탄소섬유 및 하이브리드 섬유 구조의 지원으로 터빈당 소재 사용량이 증가하고 있으며, 이는 공급업체들이 아시아태평양 및 유럽 지역에서 생산 능력을 확대하도록 촉진하고 있습니다. 영국의 차액 계약(CfD) 예산 및 중국의 2024년 신규 설치 117GW와 같은 정책 인센티브는 다년간의 주문 가시성을 보장하고 풍력 터빈 복합재료 시장 전반에 걸쳐 자동화 및 수직 통합 전략을 가속화하고 있습니다.

세계의 풍력 터빈 복합재료 시장 동향 및 인사이트

증가하는 육상 및 해상 터빈 용량이 첨단 복합재료 수요를 주도

세계의 풍력 터빈 등급은 해상에서 15MW를 일상적으로 초과하여 블레이드 길이를 115m 이상으로 늘리고, 첨단 복합재료만이 견딜 수 있는 구조적 하중을 배가시키고 있습니다. 베스타스의 V236-15MW 플랫폼에 장착된 115.5m 길이의 블레이드와 지멘스 가메사의 기밀 21.5MW 프로토타입은 로터당 복합재료 사용량을 확대하는 동시에 강성과 피로 저항성을 위해 더 가벼운 탄소 강화 스파 캡을 요구하는 규모 확대를 보여주는 대표적인 사례입니다. 영국만 해도 2030년까지 해상 풍력 설비 용량을 최대 50GW까지 확대할 계획이며, 이는 부식성 해양 환경에서 25년 설계 수명을 보장할 수 있는 고성능 적층 시스템에 대한 장기적 수요를 확고히 하는 목표입니다.

정부의 탈탄소화 정책이 복합재료 채택을 가속

영국의 12억 달러 규모 해상풍력 전용 CfD(차액결제계약) 라운드와 중국의 2024년 풍력설비 설치량 117GW라는 기록적 수치는 다중 기가와트 규모의 입찰 파이프라인을 확보하고 신규 복합재료 공장 투자 위험을 완화합니다. 저탄소 공급망에 보상을 제공하는 청정산업 보너스 제도는 현지 블레이드 생산과 친환경 수지 화학 기술 개발을 촉진하고 있습니다. 유럽 그린딜의 구속력 있는 2030년 재생에너지 목표와 독일의 80% 청정전력 목표는 풍력 터빈 복합재료 시장 전반에 걸쳐 수요 가시성을 공고히 하고 베스타스, LM 풍력 파워, 중국 유리섬유 대기업들의 생산 능력 확장을 촉진합니다. 탄소 가격 책정 및 재생에너지 인증서는 프로젝트 경제성을 더욱 향상시켜 경량, 내구성, 재활용성이 뛰어난 복합재료에 대한 지속적인 수요를 보장합니다.

탄소섬유의 가격 변동이 프리미엄 용도를 억제

100m 이상 블레이드 수요 급증으로 2027년까지 탄소섬유 소비량이 3배 증가할 전망이지만, 생산 능력 확장이 뒤처져 가격 급등이 발생하며 비용 민감형 터빈의 광범위한 도입을 저해하고 있습니다. 2023년 6만 9,000톤의 탄소섬유를 흡수한 중국 시장은 수출 제한과 지정학적 마찰로 공급망이 차질을 빚으며 가격 급등락을 경험했습니다. 이에 OEM 업체들은 변동성 헤지를 위해 하이브리드 유리섬유-탄소섬유 구조와 현지 조달을 추진 중입니다. 2030년 예상 생산량 45만 톤 달성을 위한 추가 생산라인 가동 전까지 풍력 터빈 복합재료 시장은 불규칙한 원자재 비용을 극복해야 합니다.

부문 분석

유리 섬유는 유리한 비용과 견고한 공급망에 힘입어 2024년 풍력 터빈 복합재료 시장에서 71.66%의 압도적 점유율을 유지했습니다. 그러나 탄소섬유는 OEM 업체들이 과도한 하중 없이 더 긴 로터가 높은 팁 속도를 견딜 수 있도록 무게 감소를 추구함에 따라 7.11%의 연평균 성장률(CAGR)로 성장하고 있습니다. LM Wind Power의 88.4m 블레이드에 적용된 하이브리드 탄소/유리 스파 캡은 비용 폭증 없이도 무게 절감이 가능함을 입증했습니다.

항공우주 등급보다 40% 저렴한 텍스타일 기반 탄소섬유의 점진적 채택도 중급 터빈 시장을 개척하며 성장세를 이끌고 있습니다. 야자나무나 아마 혼합 섬유는 핵심 기계적 성능을 유지하면서 내재 에너지를 낮춰 지속가능한 틈새 시장을 제공합니다. 예측 기간 동안 풍력 터빈 복합재료 시장은 강성, 피로 수명, 경제성 사이의 균형을 맞추기 위해 하이브리드화 전략이 핵심적 역할을 지속할 전망입니다.

에폭시 시스템은 성능 특성이 잘 규명되어 2024년 매출 점유율 34.88%를 차지했으나, 폴리에스터/비닐에스터 및 폴리우레탄 혼합물이 7.45%의 가장 빠른 연평균 성장률(CAGR)을 기록 중입니다. 입증된 10-25%의 공정 시간 단축과 향상된 습윤성으로 폴리우레탄 주입 공법은 대규모 자본 투자 없이 연간 생산량 확대를 위한 최적의 후보로 부상하고 있습니다.

라이프사이클 배출량을 30-40% 저감하는 바이오 기반 화학물질 수요는 제형 연구개발을 주도하며, 특히 탄소 발자국 공개가 이미 입찰에 반영된 유럽에서 친환경 수지 시장 규모를 확대할 것입니다. 발열 피크를 줄이는 Baxxodur 경화제 및 첨가제 패키지는 에폭시의 경쟁력을 한층 강화하여 2030년까지 다양한 수지 등급의 공존을 보장합니다.

풍력 터빈 복합재료 보고서는 섬유 유형(유리 섬유, 탄소 섬유, 천연/하이브리드 섬유), 수지 유형(에폭시, 폴리에스터/비닐 에스터, 폴리우레탄, 열가소성 수지), 기술(진공 주입, 프리프레그 등), 응용 분야(풍력 블레이드, 나셀 및 노즈 콘 등), 지역(아시아태평양, 북미, 유럽 등)별로 분류됩니다. 시장 전망은 가치(USD) 기준으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2024년 매출의 46.44%를 차지하며 풍력 터빈 복합재료 시장의 핵심 지역으로 자리매김하고 있으며, 6.99%의 선도적인 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 중국은 중국 주시(Jushi)와 CPIC를 우대하는 현지 조달 규정 덕분에 2024년 역대 최대 규모인 117GW의 신규 설비를 추가했으며, 이는 전 세계적으로 원단과 완제품 블레이드를 모두 수출하는 독보적인 공급망 기반을 뒷받침합니다.

유럽은 성숙한 기술 도입과 엄격한 지속가능성 규제로 뒤를 잇는다. 영국의 2030년까지 최대 50GW 해상풍력 목표, 독일의 80% 청정전력 목표, 프랑스의 순환경제 의무화는 유럽 제조사들을 재활용 가능 열가소성 플라스틱과 폐쇄성형 방식으로 이끌고 있습니다.

북미는 연방 세액 공제와 주 정부 조달을 결합해 대평원 지역의 육상 풍력 단지를 확장하고 연안 풍력 지대의 설비를 현대화하고 있습니다. 미국 에너지부는 2027년까지 복합재료 수요가 3배 증가할 것으로 전망하며, TPI 컴포지츠와 GE 버노바의 투자를 촉진해 스파 캡 및 루트 인서트 생산을 현지화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 성장 촉진요인

- 육상 및 해상 터빈 용량 증가는 더 가볍고 긴 블레이드 수요를 촉진

- 정부의 탈탄소화 목표와 CFD 경매는 풍력 에너지 개발을 가속화

- 비용 절감형 폴리우레탄 주입 수지는 사이클 시간을 단축

- 바이오 기반/재활용 가능 열가소성 시스템이 ESG 금융가능성을 개척

- 스마트 패브릭과 호환되는 복합재료가 블레이드의 디지털 트윈 촉진

- 시장 성장 억제요인

- 탄소섬유의 가격과 공급의 불안정성

- 복합재료에 대한 다가오는 BPA 및 스티렌 배출 제한

- 신흥 허브의 고급 주입 공정 숙련 노동력 부족

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 섬유 유형별

- 유리 섬유

- 탄소 섬유

- 천연 섬유 및 하이브리드 섬유

- 수지 유형별

- 에폭시

- 폴리에스터 및 비닐에스터

- 폴리우레탄

- 열가소성 수지

- 기술별

- 진공 주입

- 프리프레그

- 핸드 레이 업

- 필라멘트 와인딩

- 용도별

- 풍력 블레이드

- 나셀과 노즈콘

- 허브, 커버, 보조 부품

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- AVIC Huiteng Windpower

- BASF

- China Jushi Co., Ltd.

- Covestro AG

- Exel Composites

- Gurit Holding AG

- Hexcel Corporation

- INCA Renewtech

- Lianyungang Zhongfu Lianzhong Composite Material Group Co., Ltd

- LM WIND POWER

- Molded Fiber Glass Companies

- Owens Corning

- Reliance Industries Limited

- SGL Carbon

- Siemens AG

- Sinoma Science & Technology Co.,Ltd.

- Teijin Limited

- TORAY INDUSTRIES, INC.

- TPI Composites

- Vestas

- Zhongfu Lianzhong Group

제7장 시장 기회와 전망

HBR 25.11.07The Wind Turbine Composite Materials Market size is estimated at USD 13.45 billion in 2025, and is expected to reach USD 18.22 billion by 2030, at a CAGR of 6.26% during the forecast period (2025-2030).

Widespread adoption of blades longer than 100 m, supported by lighter glass-, carbon- and hybrid-fiber architectures, is raising material content per turbine and pushing suppliers to expand capacity in Asia Pacific and Europe. Policy incentives such as the United Kingdom's Contracts for Difference (CfD) budget and China's 117 GW of new 2024 installations assure multi-year order visibility and accelerate automation and vertical integration strategies across the wind turbine composites market.

Global Wind Turbine Composite Materials Market Trends and Insights

Increasing Onshore and Offshore Turbine Capacities Drive Demand for Advanced Composites

Global turbine ratings now routinely exceed 15 MW offshore, pushing blade lengths past 115 m and multiplying structural loads that only advanced composites can withstand. Vestas' 115.5 m-long blades on the V236-15 MW platform and Siemens Gamesa's confidential 21.5 MW prototype exemplify the scale-up that magnifies composite volume per rotor while simultaneously mandating lighter carbon-reinforced spar caps for stiffness and fatigue resistance. The United Kingdom alone aims to raise offshore capacity to as much as 50 GW by 2030, a target that cements long-term pull for high-performance laminate systems able to deliver a 25-year design life in corrosive marine environments.

Government Decarbonization Policies Accelerate Composite Material Adoption

Supportive frameworks, such as the United Kingdom's USD 1.2 billion CfD round dedicated to offshore wind and China's record 117 GW of 2024 wind installations, lock in multi-gigawatt auction pipelines and de-risk investments in new composite plants. Clean-industry bonus mechanisms that reward low-carbon supply chains are encouraging local blade production and greener resin chemistries. The European Green Deal's binding 2030 renewables targets, along with Germany's 80% clean-power ambition, consolidate demand visibility across the wind turbine composites market and motivate capacity expansions from Vestas, LM Wind Power, and Chinese glass-fiber majors. Carbon pricing and renewable energy certificates further boost project economics, ensuring sustained pull for lightweight, durable, and recyclable composites.

Carbon Fiber Price Volatility Constrains Premium Applications

Surging demand for 100 m-plus blades is expected to triple carbon consumption by 2027, yet capacity expansions lag, creating price spikes that discourage wider uptake in cost-sensitive turbines. China's market, which absorbed 69,000 t of carbon fiber in 2023, saw sharp swings as export restrictions and geopolitical frictions disrupted supply chains. OEMs, therefore, pursue hybrid glass-carbon architectures and localized sourcing to hedge volatility. Until additional lines lift global output toward the 450,000 tons predicted for 2030, the wind turbine composites market must navigate erratic input costs.

Other drivers and restraints analyzed in the detailed report include:

- Polyurethane Infusion Resins Transform Manufacturing Economics

- Bio-based Thermoplastic Systems Enable Circular-Economy Transition

- Regulatory Emission Limits Drive Manufacturing-Process Transformation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glass fiber retained a dominant 71.66% share of the wind turbine composites market in 2024, underpinned by favorable cost and robust supply chains. Carbon, however, is growing at 7.11% CAGR as OEMs chase mass reductions that let longer rotors survive higher tip speeds without excess loads. LM Wind Power's hybrid carbon/glass spar caps on its 88.4 m blade validated weight cuts without cost blowouts.

Incremental uptake also stems from textile-based carbon fibers that are 40% cheaper than aerospace grades, unlocking mid-tier turbine segments. Natural-fiber blends offer sustainable niches, with palm or flax hybrids matching key mechanical metrics while lowering embodied energy. Over the forecast horizon, hybridization strategies will remain pivotal as the wind turbine composites market balances stiffness, fatigue life and affordability.

Epoxy systems held 34.88% revenue share in 2024, thanks to well-characterized performance, yet polyester/vinyl-ester and polyurethane blends are tracking the fastest 7.45% CAGR. Proven 10-25% cycle-time savings and improved wet-out make polyurethane infusion the prime candidate for stretching annual output without large capex.

Demand for bio-based chemistries that curb life-cycle emissions by 30-40% will steer formulation research and development, broadening the wind turbine composites market size for greener resins, particularly in Europe, where carbon-footprint disclosures already feature in tenders. Baxxodur curing agents and additive packages that cut exotherm peaks further enhance epoxy competitiveness, ensuring multiple resin classes co-exist through 2030.

The Wind Turbine Composite Materials Report is Segmented by Fiber Type (Glass Fiber, Carbon Fiber, Natural/Hybrid Fibers), Resin Type (Epoxy, Polyester/Vinyl-Ester, Polyurethane, Thermoplastic Resins), Technology (Vacuum Infusion, Prepreg, and More), Application (Wind Blades, Nacelles and Nose Cones, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific, at 46.44% of 2024 revenue, remains the anchor region for the wind turbine composites market and posts a leading 6.99% CAGR. China's record 117 GW of 2024 additions, supported by local-content rules favoring China Jushi and CPIC, underpin an unrivaled supply-chain footprint that exports both raw fabrics and finished blades worldwide.

Europe follows with mature technology adoption and rigorous sustainability regulations. The United Kingdom's ambition to reach up to 50 GW of offshore wind by 2030, Germany's 80% clean-power target, and France's circular-economy mandates push European makers toward recyclable thermoplastics and closed molding.

North America couples federal tax credits with state procurement to expand onshore fleets in the Great Plains and repower coastal wind zones. The U.S. Department of Energy forecasts composite demand tripling by 2027, propelling investments from TPI Composites and GE Vernova that localize spar-cap and root-insert production.

- AVIC Huiteng Windpower

- BASF

- China Jushi Co., Ltd.

- Covestro AG

- Exel Composites

- Gurit Holding AG

- Hexcel Corporation

- INCA Renewtech

- Lianyungang Zhongfu Lianzhong Composite Material Group Co., Ltd

- LM WIND POWER

- Molded Fiber Glass Companies

- Owens Corning

- Reliance Industries Limited

- SGL Carbon

- Siemens AG

- Sinoma Science & Technology Co.,Ltd.

- Teijin Limited

- TORAY INDUSTRIES, INC.

- TPI Composites

- Vestas

- Zhongfu Lianzhong Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Increasing Onshore and Offshore Turbine Capacities Drive the Need for Lighter, Longer Blades.

- 4.1.2 Government Decarbonization Goals and CFD Auctions are Speeding Up Wind Energy Development.

- 4.1.3 Cost-Saving Polyurethane Infusion Resins Shorten Cycle Time

- 4.1.4 Bio-Based/Recyclable Thermoplastic Systems Unlock ESG Finance

- 4.1.5 Composites Compatible with Smart Fabrics Facilitate Digital Twinning of Blades.

- 4.2 Market Restraints

- 4.2.1 Carbon-Fiber Price and Supply Volatility

- 4.2.2 Upcoming BPA and Styrene Emission Limits for Composites

- 4.2.3 Skilled-Labour Deficit in Advanced Infusion for Emerging Hubs

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fiber Type

- 5.1.1 Glass Fiber

- 5.1.2 Carbon Fiber

- 5.1.3 Natural/Hybrid Fibers

- 5.2 By Resin Type

- 5.2.1 Epoxy

- 5.2.2 Polyester/Vinyl-Ester

- 5.2.3 Polyurethane

- 5.2.4 Thermoplastic Resins

- 5.3 By Technology

- 5.3.1 Vacuum Infusion

- 5.3.2 Prepreg

- 5.3.3 Hand Lay-up

- 5.3.4 Filament Winding / Pultrusion

- 5.4 By Application

- 5.4.1 Wind Blades

- 5.4.2 Nacelles and Nose Cones

- 5.4.3 Hubs, Covers and Ancillary Parts

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 AVIC Huiteng Windpower

- 6.3.2 BASF

- 6.3.3 China Jushi Co., Ltd.

- 6.3.4 Covestro AG

- 6.3.5 Exel Composites

- 6.3.6 Gurit Holding AG

- 6.3.7 Hexcel Corporation

- 6.3.8 INCA Renewtech

- 6.3.9 Lianyungang Zhongfu Lianzhong Composite Material Group Co., Ltd

- 6.3.10 LM WIND POWER

- 6.3.11 Molded Fiber Glass Companies

- 6.3.12 Owens Corning

- 6.3.13 Reliance Industries Limited

- 6.3.14 SGL Carbon

- 6.3.15 Siemens AG

- 6.3.16 Sinoma Science & Technology Co.,Ltd.

- 6.3.17 Teijin Limited

- 6.3.18 TORAY INDUSTRIES, INC.

- 6.3.19 TPI Composites

- 6.3.20 Vestas

- 6.3.21 Zhongfu Lianzhong Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Government net-zero targets are accelerating global wind power installations.