|

시장보고서

상품코드

1844721

로우 프로파일 첨가제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Low Profile Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

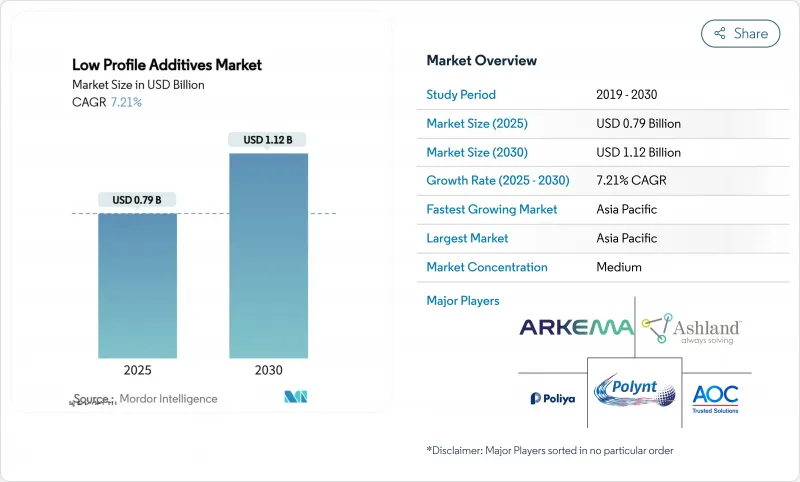

로우 프로파일 첨가제 시장 규모는 2025년에 7억 9,000만 달러로 추정되며 예측 기간(2025-2030년)의 CAGR은 7.21%로, 2030년에는 11억 2,000만 달러에 달할 것으로 예상됩니다.

전기자동차, 건축 보강재, 정밀 공업 부품의 고성능 복합재료 수요 증가가이 성장 궤도를 지원합니다. 자동차 제조업체는 시트 몰딩 컴파운드(SMC) 및 벌크 몰딩 컴파운드(BMC) 부품의 수축을 억제하고 클래스 A의 표면 품질을 보장하기 위해 낮은 프로파일 첨가제를 채택합니다. 병행하여 철근을 섬유 강화 플라스틱으로 대체하는 인프라 프로젝트에도 기세가 있어 바이오의 화학물질이 정책적인 지지를 얻고 있습니다. 공급업체는 재생가능한 원료의 통합을 겨루고, 컴파운드성과 표면 미관으로 차별화를 도모하고 있기 때문에 경쟁의 격렬함은 완만하면서 상승하고 있습니다.

세계의 로우 프로파일 첨가제 시장 동향과 인사이트

자동차 산업에서 고성능 SMC 제형 수요 증가

자동차 제조업체는 완벽한 클래스 A 마감이 필요한 배터리 인클로저, 바디 패널 및 구조 인서트 성형으로 SMC의 규모를 확대하고 있습니다. 낮은 프로파일 첨가제는 부피 수축을 제한하고 열 사이클 하에서 치수 안정성을 보장합니다. 다우의 폴리우레탄-탄소섬유 스파 캡은 90% 이상의 경화 효율을 나타내며 차세대 첨가제가 얼마나 빠른 프레스를 지원하는지 보여줍니다. 대형 차량 플랫폼과 두꺼운 단면 부품은 수축 억제 요구 사항을 더욱 높여 아시아태평양의 급성장하는 전기자동차 허브에서 고급 로우 프로파일 첨가제가 필수적입니다.

가속하는 EV 경량화 의무

유럽연합(EU)의 CO2 규정과 중국의 신에너지 자동차 할당은 섬유 강화 플라스틱의 급속한 채용에 박차를 가하고 있습니다. 낮은 프로파일 첨가제는 복합재료 어셈블리에서도 흠집이나 굴곡을 방지하고 이러한 복합재료를 지원합니다. 버지니아 대학의 조사에서는 그래핀으로 개질한 시멘트 복합재료로 31%의 경량화가 확인되었으며, 이는 자동차 구조에서도 유사한 질량 삭감을 기대할 수 있음을 보여주고 있습니다. 배터리의 항속거리에 대한 기대 증가는 계속해서 경량 복합재를 견인하여 첨가제 수요를 지속시킬 것으로 보입니다.

가교성 스티렌 단량체에 의한 불포화 폴리에스터 수지의 높은 중합 수축률

UPR-스티렌 시스템은 경화 중에 본질적으로 수축되어 보이드와 인쇄 스루를 생성하므로 얇은 첨가제는 이에 대항해야 합니다. 공급업체는 수축을 억제하기 위해 반응성 희석제 및 변성 가교제를 시도하고 있지만, 이러한 미세 조정은 비용과 사이클 시간의 복잡성을 증가시킵니다. 자동차 클래스 A 마무리는 높은 장애물을 설정하기 때문에 배합자는 빠른 움직임을 가진 대량 생산 라인에서도 혁신을 계속할 필요가 있습니다.

부문 분석

폴리스티렌 계급은 자동차용 SMC에서 입증된 비용 성능 밸런스에 의해 2024년 로우 프로파일 첨가제 시장 점유율의 39.08%를 유지했습니다. 기타 제품 유형(주로 바이오)의 로우 프로파일 첨가제 시장 규모는 급속히 확대되고 OEM이 탄소 삭감 크레딧을 추구하는 가운데 2030년까지의 CAGR은 9.20%를 나타낼 것으로 보입니다.

폴리 비닐 아세테이트와 PMMA는 충격 강도와 광학 투명성이 요구되는 틈새 시장을 차지하며 고밀도 폴리에틸렌 등급은 예산이 낮은 부품에 적합합니다. 폴리에스터를 주성분으로 하는 제품은 순수한 것과 PU 변성한 양쪽이 있어, 부식성이나 고온 환경에 대응하고 있습니다. BASF의 바이오물질 수지 EPS는 기존 공급업체가 지속가능성과 기존 프로세스를 융합시키는 방법을 명확하게 보여줍니다.

지역 분석

아시아태평양은 2024년에 44.81%의 점유율을 차지했고, 2030년까지의 CAGR 전망에서는 8.02%로 얇은 첨가제 시장을 독점할 전망입니다. 중국의 전기차 급증과 국가지원에 의한 인프라 정비가 컴포지트 채용을 뒷받침하는 한편, 현지 공급업체는 열경화성 수지의 생산 능력을 확대하고 있습니다. 인도의 자동차산업 확대와 한국의 전자수출이 쫓겨납니다. BASF의 난징 거점 확장은 지역 생산에 대한 전략적 주력을 강조합니다.

북미는 2위로 EV플랫폼 출시, 항공우주 재구축, 풍력발전 캠페인에 지지를 받고 있습니다. 미국에는 첨단 수지 실험실과 인발 라인이 있으며, 멕시코는 OEM 공장에 가깝기 때문에 부품의 현지화가 진행되고 있습니다. 다우의 윈드블레이드 수지 프로그램은 지역의 기술력을 두드러지게 하고 있습니다.

유럽은 엄격한 지속가능성 요구사항을 특징으로 하며, 바이오 저 프로파일 첨가제의 보급을 서두르고 있습니다. 독일의 고급 자동차 브랜드는 바디 인 화이트에 컴포지트를 채용하고, 북유럽 국가들은 재생에너지에 대한 투자를 대형 터빈 블레이드에 돌리고 있습니다. 에보닉 리그닌 프로그램과 BYK의 VOC 프리 계면활성제는 혁신의 추진력의 대표입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 업계로부터의 고성능 SMC(시트 몰딩 컴파운드) 배합물에 대한 수요 증가

- EV 경량화의 가속

- 철근(콘크리트 구조물을 강화하는데 사용되는 철근)의 대체

- 섬유 강화 플라스틱(FRP)의 새로운 용도

- 리그닌과 피마자유를 원료로 하는 바이오 베이스 LPA에 대한 주목의 고조

- 시장 성장 억제요인

- 가교성 스티렌 단량체에 의한 불포화 폴리에스터 수지의 높은 중합 수축률

- 열가소성 복합체와의 경쟁

- 열경화성 부품의 제한된 수리 가능성

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모·성장 예측

- 제품 유형별

- 폴리스티렌 베이스

- 폴리비닐 아세테이트 베이스

- PMMA 베이스

- 고밀도 폴리에틸렌(HDPE) 베이스

- 폴리에스터 베이스

- 순수 포화 폴리에스터

- PU 개질 포화 폴리에스터

- 기타 제품 유형(EVA, SAN, 바이오 베이스)

- 용도별

- 사출 및 압축 성형(SMC/BMC)

- 인발 성형

- 수지 전이 성형(RTM)

- 수동 적층 성형

- 스프레이 성형

- 최종 사용자 산업별

- 자동차 및 운송

- 건축 및 건설

- 전기 및 전자

- 산업 기계

- 기타(소비재, 해양)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- ALTANA AG

- AOC

- Arkema

- Ashland

- Clariant

- Composites One

- Evonik Industries AG

- INEOS

- Link Composites Pvt. Ltd.

- Mechemco

- Mitsubishi Chemical Group Corporation.

- Monachem

- Poliya

- Polynt SpA

- Scott Bader Company Ltd

- Swancor

- Synthomer Plc

- Wacker Chemie AG

제7장 시장 기회와 전망

KTH 25.10.31The Low Profile Additives Market size is estimated at USD 0.79 billion in 2025, and is expected to reach USD 1.12 billion by 2030, at a CAGR of 7.21% during the forecast period (2025-2030).

Rising demand for high-performance composites in electric vehicles, construction reinforcements, and precision industrial parts is sustaining this growth trajectory. Automakers are adopting low profile additives to control shrinkage in Sheet Molding Compound (SMC) and Bulk Molding Compound (BMC) components, ensuring Class A surface quality. Parallel momentum stems from infrastructure projects that replace steel rebar with fiber-reinforced plastics, while bio-based chemistries are gaining policy support. Competitive intensity is moderate yet rising as suppliers race to integrate renewable feedstocks and differentiate on compoundability and surface aesthetics.

Global Low Profile Additives Market Trends and Insights

Increase in Demand for High-performance SMC Formulations from Automotive Industry

Automakers are scaling SMC to mold battery enclosures, body panels, and structural inserts that need flawless Class A finishes. Low profile additives limit volumetric shrinkage, securing dimensional stability under thermal cycling. Dow's polyurethane-carbon fiber spar cap demonstrates cure efficiencies exceeding 90%, exemplifying how next-generation additives support high-speed presses. Larger vehicle platforms and thick-section parts further raise shrinkage control requirements, making advanced low profile additives indispensable across Asia-Pacific's fast-growing electric vehicle hubs.

Accelerated EV Lightweighting Mandates

The European Union's CO2 rules and China's New Energy Vehicle quotas spur rapid fiber-reinforced plastic adoption. Low profile additives underpin these composites by preventing sink marks and waviness even in multi-material assemblies. University of Virginia research shows weight savings of 31% in graphene-modified cement composites, a proxy for similar mass-reduction prospects in auto structures. Rising battery range expectations will continue to pull lightweight composites, sustaining additive demand.

High Polymerization Shrinkage of Unsaturated Polyester Resin with Crosslinking Styrene Monomer

UPR-styrene systems inherently contract during cure, generating voids and print-through that low profile additives must counteract. Suppliers experiment with reactive diluents and modified crosslinkers to curb shrinkage, but such tweaks add cost and cycle-time complexity. Automotive Class A finishes set a high bar, pressuring formulators to keep innovating even in fast-moving, high-volume lines.

Other drivers and restraints analyzed in the detailed report include:

- Replacement of Steel Rebar with Fiber-reinforced Plastics

- Growing Emphasis on Bio-based LPAs from Lignin & Castor Oil

- Competition from Thermoplastic Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polystyrene-based grades retained 39.08% low profile additives market share in 2024 through proven cost-performance balance in automotive SMC. The low profile additives market size for "Other" product types-largely bio-based-should rise swiftly, expanding at 9.20% CAGR to 2030 as OEMs chase carbon reduction credits.

Polyvinyl acetate and PMMA variants occupy niches that demand impact strength or optical clarity, while high-density polyethylene grades suit budget-sensitive parts. Polyester-based offerings, both pure and PU-modified, tackle corrosive or high-temperature environments. BASF's biomass-balance EPS underscores how incumbent suppliers blend sustainability with incumbent processes.

The Low Profile Additives Market Report is Segmented by Product Type (Polystyrene-Based, Polyvinyl Acetate-Based, and More), Application (Injection and Compression Molding, Pultrusion, and More), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the low profile additives market with 44.81% share in 2024 and an 8.02% CAGR outlook to 2030. China's electric vehicle surge and state-backed infrastructure rollouts underpin composite adoption, while local suppliers scale thermoset capacity. India's automotive expansion and South Korea's electronics exports add tailwinds. BASF's Nanjing site enlargement underscores strategic focus on regional production.

North America ranked second, buoyed by EV platform launches, aerospace rebuilds, and wind-repowering campaigns. The United States houses advanced resin labs and pultrusion lines, while Mexico's proximity to OEM plants fuels part localization. Dow's wind-blade resin programs highlight regional technical prowess.

Europe follows, characterized by strict sustainability requirements that hasten bio-based low profile additives uptake. Germany's premium auto brands adopt composites for body-in-white elements, and Nordic nations channel renewables investments into large turbine blades. Evonik's lignin programs and BYK's VOC-free surfactants typify the innovation thrust.

- ALTANA AG

- AOC

- Arkema

- Ashland

- Clariant

- Composites One

- Evonik Industries AG

- INEOS

- Link Composites Pvt. Ltd.

- Mechemco

- Mitsubishi Chemical Group Corporation.

- Monachem

- Poliya

- Polynt S.p.A

- Scott Bader Company Ltd

- Swancor

- Synthomer Plc

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for High-performance SMC (Sheet Molding Compound) Formulations from Automotive Industry.

- 4.2.2 Accelerated EV lightweighting mandates

- 4.2.3 Replacement of Steel Rebar (Reinforcing Bar Employed to Strengthen Concrete Structures)

- 4.2.4 Emerging Applications in Fiber-reinforced Plastics (FRP)

- 4.2.5 Growing emphasis on Bio-based LPAs from lignin & castor oil

- 4.3 Market Restraints

- 4.3.1 High Polymerization Shrinkage of Unsaturated Polyester Resin with the Crosslinking Styrene Monomer

- 4.3.2 Competition from thermoplastic composites

- 4.3.3 Limited repairability of thermoset parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polystyrene-based

- 5.1.2 Polyvinyl Acetate-based

- 5.1.3 PMMA-based

- 5.1.4 High Density Polyethylene (HDPE)

- 5.1.5 Polyester-based

- 5.1.5.1 Pure Saturated Polyester

- 5.1.5.2 PU-modified Saturated Polyester

- 5.1.6 Other Product Types (EVA, SAN, Bio-based)

- 5.2 By Application

- 5.2.1 Injection and Compression Molding (SMC/BMC)

- 5.2.2 Pultrusion

- 5.2.3 Resin Transfer Molding (RTM)

- 5.2.4 Hand Lay-Up

- 5.2.5 Spray-Up

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Industrial Machinery

- 5.3.5 Others (Consumer Goods, Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ALTANA AG

- 6.4.2 AOC

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 Clariant

- 6.4.6 Composites One

- 6.4.7 Evonik Industries AG

- 6.4.8 INEOS

- 6.4.9 Link Composites Pvt. Ltd.

- 6.4.10 Mechemco

- 6.4.11 Mitsubishi Chemical Group Corporation.

- 6.4.12 Monachem

- 6.4.13 Poliya

- 6.4.14 Polynt S.p.A

- 6.4.15 Scott Bader Company Ltd

- 6.4.16 Swancor

- 6.4.17 Synthomer Plc

- 6.4.18 Wacker Chemie AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment