|

시장보고서

상품코드

1844722

서모크로믹 안료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Thermochromic Pigments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

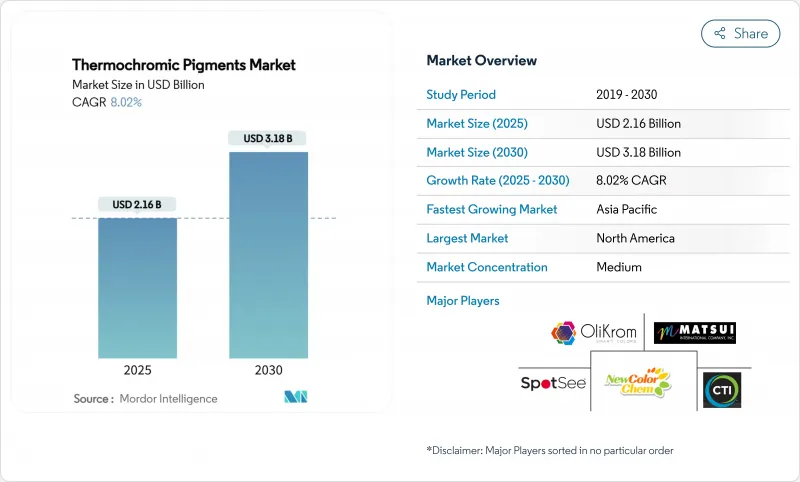

서모크로믹 안료 시장 규모는 2025년에 21억 6,000만 달러로 추정되며, 예측기간(2025-2030년)의 CAGR은 8.02%로, 2030년에는 31억 8,000만 달러에 달할 것으로 예상됩니다.

이 확장은 스마트 패키징, 섬유, 보안 인쇄에서 온도 응답성 재료의 사용 확대에 의해 추진되는 반면, 마이크로 캡슐화의 진보는 어려운 환경에서도 안료가 안정된 상태를 유지할 수 있습니다. 콜드체인·인디케이터에 대한 의약품 수요 증가, 에너지 효율이 높은 건축용 도료에의 축족, 미관과 열 관리를 융합시킨 자동차 용도가 더욱 기세를 늘리고 있습니다. 대규모 지역의 최종 사용자는 컴플라이언스 씰과 식품 포장에 스마트 안료를 지속적으로 통합하여 부패를 줄이고 소비자의 안전을 강화하고 있습니다. 합성에 있어서의 코스트 다운의 노력과, 눈에 보이는 온도 인디케이터를 지지하는 규제의 움직임이 함께, 시장의 성장 전망을 선명하게 하고 있습니다.

세계의 서모크로믹 안료 시장 동향과 인사이트

스마트 패키징 수요 증가

식품 및 의약품 공급업체가 물류 네트워크 전반에 걸쳐 제품의 무결성을 확인할 수 있는 눈에 보이는 온도 감응 표시기를 채택함에 따라 스마트 포장은 수요를 계속 확대하고 있습니다. 백신, 생물학적 제제 및 조리된 식품의 콜드체인 브레이크는 돌이킬 수 없는 색상 변화를 일으키며, 취급자와 최종 사용자에게 신속한 현장 확인을 제공합니다. 연구 결과, 보호되지 않은 열변색성 고분자 블렌드는 산성 조건 하에서 분해되는 것으로 밝혀졌으며, 용출하기 어려운 다층 장벽과 내구성 있는 마이크로캡슐의 개발이 요구되고 있습니다. 규제 당국은 현재 중요한 의약품에 준거한 씰을 요구하고 있으며, 성숙 시장에서도 신흥국 시장에서도 돌이킬 수 없는 안료 라벨의 기준선량을 인상하고 있습니다. 다국적 제약 회사는 북미에서 생산을 조달하고 조기 채용에 박차를 가하고 있습니다. 한편, 아시아와 아프리카의 소규모 지역 생산자들은 일관성 없는 냉장 인프라를 상쇄하기 위해 시각적 지표에 의존하고 있습니다. 마이크로캡슐화의 스케일 메리트가 개선됨에 따라 비용 프리미엄은 축소되고, 서모크로믹 안료 시장의 궤도가 강화됩니다.

스마트 섬유 산업에서 수요 증가

스마트 텍스타일은 체온, 주위 온도 또는 전기 입력에 반응하여 색조를 변화시키는 열 변색 캡슐을 실에 묻은 고성장 프론티어입니다. 습식 방사 라인은 캡슐을 균일하게 증착하여 피로하지 않고 수천 번의 색조를 변화시키는 섬유를 생산합니다. 태양 응답 섬유는 직사 광선 하에서 52.6℃에 도달하고 자외선의 강도를 나타내기 위해 주황색에서 녹색으로 변합니다. 전도성 실과의 통합은 저전압 회로를 통한 온디맨드 컬러 제어를 가능하게 하며, 스포츠웨어, 의료 모니터링, 적응형 위장으로의 길을 열 수 있습니다. 중국과 한국에서는 조종사 규모의 지속적인 생산으로 단가가 낮아지고 유럽 패션 하우스에서는 미적 새로움과 기능적 피드백을 융합시킨 한정 생산 의복이 시도되고 있습니다. 이러한 개발은 서모크로믹 안료 시장의 장기적인 상승을 지원합니다.

기존 안료에 대한 높은 비용

서모크로믹 안료는 표준 안료의 3배에서 5배의 비용이 드는 경우가 많아, 건축용 도료나 범용 텍스타일과 같은 양 주도의 분야에서는 이폭을 압박합니다. 마이크로캡슐화는 엄격한 공정 관리와 특수한 반응기를 필요로 하며 생산자의 CAPEX를 상승시킵니다. 채용 여부를 좌우하는 것은 포장업자나 인쇄업자가 제한된 예산 속에서 부패 감소와 법규제 준수를 통해 투자 대 효과를 실증할 수 있는지 여부입니다. 생산자는 생산 규모를 확대하고 공급망을 현지화하며 마이크로캡슐 벽재로 보다 저렴한 것을 채용함으로써 이 제약에 대항하고 있습니다. 특히 서모크로믹 안료 시장의 세계 수량이 증가함에 따라 이러한 조치는 점차 가격 차이를 줄이고 있습니다.

부문 분석

2024년 서모크로믹 안료 시장 점유율의 59.81%는 비가역형 변종이 차지했으며, 이는 단일 사용 의약품 및 식품 표시기에서 중요한 역할을 반영합니다. 이러한 제품은 특정 임계값을 초과하면 영구적으로 색상이 변하고 온도 남용의 증거로 법정에서도 인정됩니다. 백신 바이알이나 혈액백 등 이 분야의 설치 베이스가 크기 때문에 정기적인 수요가 확보되어 이 카테고리 전체의 서모크로믹 안료 시장 규모를 유지하고 있습니다.

그럼에도 불구하고 가장 높은 8.91%의 연평균 복합 성장률(CAGR) 전망에서 뒤집을 수 있는 제형이 주목을 받고 있습니다. 연속 컬러 사이클은 스마트 섬유, 재사용 가능한 데이터 로거, 산업용 공정 모니터에 적합합니다. 에폭시-실리카 하이브리드 캡슐에 의한 내구성의 향상은 퇴색하지 않고 10,000회 이상의 스위치 사이클을 가능하게 했습니다.

서모크로믹 안료 보고서는 유형별(가역성, 비가역성), 용도별(플라스틱, 폴리머, 페인트, 코팅, 패브릭, 잉크 및 기타 용도), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 서모크로믹 안료 시장에서 29.81%의 점유율을 차지하고 있으며, 생물제제, 인슐린, 특수식품에 가시온도 인디케이터를 요구하는 엄격한 FDA 지령이 그 요인이 되고 있습니다. 제약 대기업은 연구 개발, 제조, 유통을 미국 전역에 집적하고 있으며 조기 채용과 안정적인 판매량을 견인하고 있습니다. 캐나다 섬유 연구소는 노인 간호를 위한 웨어러블 센서를 개발하고 멕시코 자동차 공장은 열 축적을 완화하는 열 변색 바디 패널을 시도하고 있습니다.

아시아태평양의 2025-2030년 CAGR은 8.76%로 세계 최고에 달할 것으로 예상됩니다. 중국 섬유 제조 업체는 열 변색 캡슐을 폴리 에스테르에 직접 통합하는 습식 방사 라인을 확장하여 킬로그램 당 비용을 낮추고 대량 시장용 의류에 대한 액세스를 확대합니다. 일본의 소재연구소는 자율형 일렉트로닉스의 열관리에 적합한 근적외선 응답성 안료를 완성시키고, 한국의 가전기기 대기업은 스마트 컬러 필름을 접이식 디바이스에 통합하려고 하고 있습니다.

유럽은 여전히 매우 중요한 시장이며 엄격한 건축 에너지 규제와 자동차 안전 규제를 활용하고 있습니다. 독일의 화학 기업은 무촉매 합성 경로를 고안하여 용매 사용량을 줄이고 환경 컴플라이언스에 기여합니다. 프랑스와 이탈리아의 패션 하우스는 런웨이에서 열 램프 아래 색상을 변경하는 컬러 모핑 꾸뛰르를 시도하고 있습니다. 아시아태평양에 비하면 유럽의 성장은 완만하지만, 규제의 확실성과 그린 기술에 대한 자금 지원 제도가 서모크로믹 안료 시장의 침투를 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트 포장 수요 증가

- 스마트 텍스타일 산업에서의 수요 증가

- 위조 방지 인쇄용 보안 잉크의 성장

- 장식용 페인트 및 코팅의 확대

- 넷·제로·스마트 창유리의 채용 증가

- 시장 성장 억제요인

- 기존 안료에 비해 고비용

- 좁은 사용 온도 범위

- 내구성과 내광성의 문제

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모·성장 예측(금액 기준)

- 유형별

- 가역적

- 비가역적

- 용도별

- 플라스틱 및 폴리머

- 페인트 및 코팅

- 직물

- 잉크

- 기타 용도(스마트 윈도우, 건축자재 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Chromatic Technologies Inc.

- Global New Material International

- Hali Pigment Co. Ltd

- iSuoChem

- KingChroma Technology

- L'Arca SRL

- Matsui International Company Inc.

- Merck KGA

- NEW PRISMATIC ENTERPRISE CO., LTD.

- NewColorChem

- OliKrom SA

- QCR Solutions Corp.

- SFXC

- SMAROL Industrial Co. Ltd

- SpotSee

제7장 시장 기회와 전망

KTH 25.10.31The Thermochromic Pigments Market size is estimated at USD 2.16 billion in 2025, and is expected to reach USD 3.18 billion by 2030, at a CAGR of 8.02% during the forecast period (2025-2030).

This expansion is propelled by the widening use of temperature-responsive materials in smart packaging, textiles, and security printing, while progress in microencapsulation keeps pigments stable in demanding environments. Increasing pharmaceutical demand for cold-chain indicators, the pivot toward energy-efficient building coatings, and automotive applications that blend aesthetics with thermal management add further momentum. Large regional end-users continue to integrate smart pigments into compliance seals and food packaging, reducing spoilage and enhancing consumer safety. Cost-down efforts in synthesis, combined with regulatory moves favoring visible temperature indicators, sharpen the market's growth outlook.

Global Thermochromic Pigments Market Trends and Insights

Growing Demand for Smart Packaging

Smart packaging continues to amplify demand as food and pharmaceutical suppliers adopt visible, temperature-sensitive indicators that confirm product integrity across logistics networks. Cold-chain breaks for vaccines, biologics, and ready-to-eat meals trigger irreversible color changes, offering quick, on-site verification for handlers and end users. Studies highlight that unprotected thermochromic polymer blends degrade in acidic conditions, prompting multilayer barriers and durable microcapsules that resist leaching. Regulatory agencies now insist on compliant seals for critical medications, raising baseline volumes of irreversible pigment labels in both mature and developing markets. Multinational pharma firms sourcing North American production spur early adoption, while smaller regional producers in Asia and Africa rely on visual indicators to offset inconsistent refrigeration infrastructure. The cost premium narrows as scale economies in microencapsulation improve, reinforcing the thermochromic pigments market trajectory.

Rising Demand from Smart Textile Industry

Smart textiles represent a high-growth frontier, with yarns embedding thermochromic capsules that shift hue in response to body heat, ambient temperature, or electrical input. Wet-spinning lines deposit capsules uniformly, producing fibers that cycle between colors thousands of times without fatigue. Solar-responsive fabrics reach 52.6 °C in direct sun, changing from orange to green to signal ultraviolet intensity. Integration with conductive threads enables on-demand color control via low-voltage circuits, opening avenues in sportswear, medical monitoring, and adaptive camouflage. Continuous pilot-scale production in China and South Korea lowers unit cost, while fashion houses in Europe trial limited-edition garments that merge aesthetic novelty with functional feedback. These developments underpin the long-term uplift embedded in the thermochromic pigments market.

High Cost with Respect to Conventional Pigments

Thermochromic grades often cost three to five times more than standard pigments, pressuring margins in volume-driven segments such as architectural coatings and commodity textiles. Microencapsulation demands tight process control and specialized reactors, elevating CAPEX for producers. Adoption hinges on proven return-on-investment through spoilage reduction or regulatory compliance for packagers and printers working on razor-thin budgets. Producers counter this restraint by scaling production, localizing supply chains, and adopting less expensive wall materials for microcapsules. These steps gradually close the price gap, especially as global volumes rise inside the thermochromic pigments market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Security Inks for Anti-Counterfeit Printing

- Expansion of Decorative Paints and Coatings

- Narrow Operational Temperature Range

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Irreversible variants dominate with 59.81% of the thermochromic pigments market share in 2024, reflecting their critical role in single-use pharmaceutical and food indicators. These products deliver permanent color shifts once specific thresholds are crossed, providing court-admissible evidence of temperature abuse. The segment's large installed base across vaccine vials and blood bags ensures recurring demand, sustaining the overall thermochromic pigments market size for this category.

Reversible formulations nonetheless command attention with the highest 8.91% CAGR outlook. Continuous color cycling suits smart textiles, reusable data-loggers, and industrial process monitors. Durability gains from epoxy-silica hybrid capsules now permit more than 10,000 switch cycles without fading.

The Thermochromic Pigments Report is Segmented by Type (Reversible and Irreversible), Application (Plastics and Polymers, Paints and Coatings, Fabrics, Inks, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds a 29.81% share of the thermochromic pigments market, anchored by stringent FDA mandates that demand visible temperature indicators for biologics, insulin, and specialty foods. Pharmaceutical majors cluster research and development, manufacturing, and distribution across the United States, driving early adoption and stable volumes. Canadian textile labs develop wearable sensors for elder care, and Mexican automotive plants trial thermochromic body panels to mitigate heat buildup.

Asia-Pacific posts an 8.76% CAGR from 2025-2030, the highest worldwide. Chinese fiber producers scale wet-spinning lines that integrate thermochromic capsules directly into polyester, lowering the cost per kilogram and widening access for mass-market apparel. Japan's materials institutes are perfecting near-infrared responsive pigments suited to autonomous-electronics thermal management, and South Korea's consumer-electronic giants are incorporating smart color films into foldable devices.

Europe remains a pivotal market, leveraging stringent building-energy codes and automotive safety regulations. German chemical firms devise catalyst-free synthesis routes that reduce solvent use, aiding environmental compliance. Fashion houses in France and Italy experiment with color-morphing couture that changes on runways under heat lamps. Though European growth is moderate compared with Asia-Pacific, regulatory certainty and green-technology funding schemes keep thermochromic pigments market penetration elevated.

- Chromatic Technologies Inc.

- Global New Material International

- Hali Pigment Co. Ltd

- iSuoChem

- KingChroma Technology

- L'Arca SRL

- Matsui International Company Inc.

- Merck KGA

- NEW PRISMATIC ENTERPRISE CO., LTD.

- NewColorChem

- OliKrom SA

- QCR Solutions Corp.

- SFXC

- SMAROL Industrial Co. Ltd

- SpotSee

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Smart Packaging

- 4.2.2 Rising Demand from Smart Textile Industry

- 4.2.3 Growth of Security Inks for Anti-Counterfeit Printing

- 4.2.4 Expansion of Decorative Paints and Coatings

- 4.2.5 Increasing Adoption in Net-Zero Smart-Window Glazing

- 4.3 Market Restraints

- 4.3.1 High Cost with Respect to Conventional Pigments

- 4.3.2 Narrow Operational Temperature Range

- 4.3.3 Durability and Light?Fastness Issues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts )Value)

- 5.1 By Type

- 5.1.1 Reversible

- 5.1.2 Irreversible

- 5.2 By Application

- 5.2.1 Plastics and Polymers

- 5.2.2 Paints and Coatings

- 5.2.3 Fabrics

- 5.2.4 Inks

- 5.2.5 Other Applications (Smart Windows and Building Materials, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Chromatic Technologies Inc.

- 6.4.2 Global New Material International

- 6.4.3 Hali Pigment Co. Ltd

- 6.4.4 iSuoChem

- 6.4.5 KingChroma Technology

- 6.4.6 L'Arca SRL

- 6.4.7 Matsui International Company Inc.

- 6.4.8 Merck KGA

- 6.4.9 NEW PRISMATIC ENTERPRISE CO., LTD.

- 6.4.10 NewColorChem

- 6.4.11 OliKrom SA

- 6.4.12 QCR Solutions Corp.

- 6.4.13 SFXC

- 6.4.14 SMAROL Industrial Co. Ltd

- 6.4.15 SpotSee

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment