|

시장보고서

상품코드

1844723

고온 단열재 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)High-temperature Insulation Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

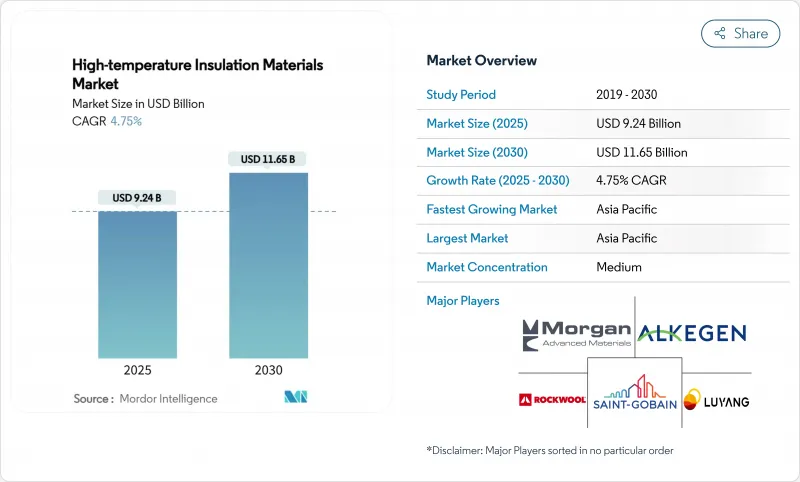

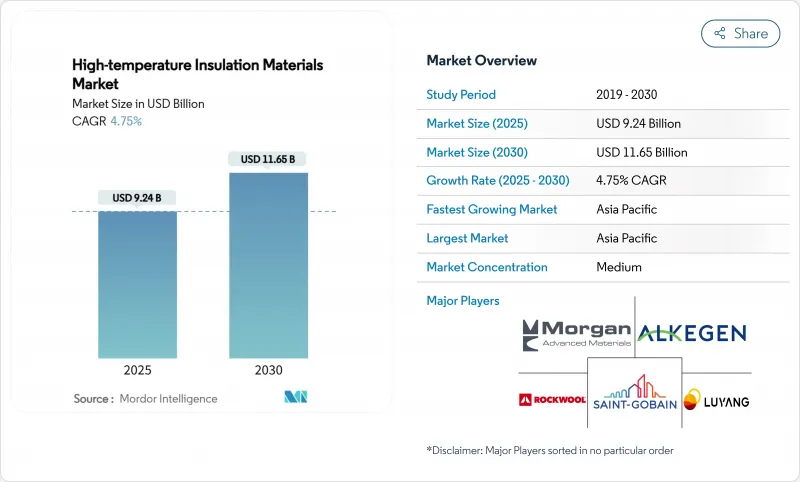

고온 단열재 시장 규모는 2025년에 92억 4,000만 달러로 추정되고 예측기간(2025-2030년)의 CAGR은 4.75%를 나타낼 전망이며, 2030년에는 116억 5,000만 달러에 달할 것으로 예상됩니다.

현재 시장 규모는 에너지 집약 산업이 운영 효율성과 배출량 감소를 추구함에 따라 수요가 꾸준히 성장하고 있음을 반영합니다. 엄격한 건축 에너지 규제, 아시아태평양의 석유화학과 금속의 급속한 능력 증대, 그린 수소 전기분해기의 설치 확대가 수요의 기간을 형성하고 있습니다. 제조업체 각사는 계속해서, 보다 엄격한 직업 노출 제한을 충족시키는 불연성 및 저생물 난분해성의 대체품을 우선하고 있습니다. 동시에 수직 통합 전략과 지역 생산 능력 확장은 주요 공급업체가 원료 가격 변동과 물류 병목 현상으로부터 보호할 수 있도록 도와줍니다. 알루미나, 실리카, 지르코니아의 가격 변동은 여전히 치열하지만, 연료 사용량과 유지 보수 비용 절감으로 인한 경제적 보상으로 채택이 증가하는 경향이 있습니다.

세계의 고온 단열재 시장 동향과 인사이트

에너지 효율이 높은 산업로에 대한 수요 급증

산업용 노 제조업체는 2024년 국제 에너지 보존 규정 하에서 허용 열 손실을 낮추고 공기 누출률을 엄격하게 하는 보다 엄격한 에너지 성능 규칙에 직면했습니다. 운영자는 연비를 손상시키지 않으면 서 1,000°C의 사용을 견디는 세라믹 섬유 담요와 미세 다공성 패널을 지정합니다. 전형적인 에너지 절약은 기존의 라이닝에 비해 30%에 가까워져 자본 비용이 높고 투자 회수율이 향상되고 있습니다. 똑똑한 열 관리 시스템을 첨단 단열재와 통합함으로써 예지 보전과 에너지 소비 최적화가 가능하며, 고온 단열재는 Industry 4.0 변혁 전략의 핵심 구성 요소로 자리매김합니다.

고온 단열재를 요구하는 건축 에너지 기준 강화

같은 2024년 국제 에너지 절약 기준(IECC) 개정은 상업용 건물의 쉘 요구사항도 첨예화되어 연속 단열과 열 브리지 완화에 대한 관심이 높아졌습니다. 유럽연합(EU)의 Fit-for-55 지침은 산업시설에서 보완적인 내열·내화 솔루션을 요구하고 있으며, 열성능과 화재안전성을 겸비한 재료가 점점 선호되고 미네랄 울이나 세라믹 파이버 시스템과 같은 불연성 옵션 수요를 견인하고 있습니다. 건물 소유자는 건물의 수명주기에 걸쳐 고성능 단열재를 경제적으로 매력적으로 만드는 에너지 비용 상승과 탄소 가격 메커니즘에 직면하고 있습니다. 에너지 효율의 의무화와 화재 안전성의 요구가 융합함으로써, 양쪽의 규제 요건에 동시에 대응할 수 있는 고온 단열재의 스위트 스폿이 탄생합니다.

합성 유리 섬유의 직업 노출 규제

OSHA는 내화성 세라믹 섬유의 허용 노출 한계를 입방 센티미터당 0.2개로 정하고 있습니다. 영국의 안전보건청은 내화성 세라믹 섬유를 발암성 물질 카테고리 2로 분류하고 있으며, COSHH규제에 의한 엄격한 관리조치가 필요합니다. 유럽 법률에서는 저생물 난분해성 대체품이 점점 더 선호되고 있으며, 알칼리 토류 실리케이트 섬유 시장 점유율은 비용이 많이 들고 온도 내성이 약간 낮아짐에도 불구하고 확대되고 있습니다. 생물용해성 섬유에 대한 규제 동향은 기존의 세라믹 섬유의 적용을 제한하는 반면 혁신적인 제조업체에게 기회를 제공합니다. 컴플라이언스 비용과 법적 책임에 대한 우려는 성능 트레이드 오프가 존재하더라도 산업 사용자를 대체 재료로 향하게합니다. 장기적인 궤도는 경쟁 구도를 재구성하고 강력한 저생물 난용성 섬유 포트폴리오를 가진 기업에 유리하게 작동하는 규제 압력이 계속 될 것임을 시사합니다.

부문 분석

세라믹 섬유는 1,260℃의 사용 한계, 저밀도, 담요, 모듈, 보드에 대한 적응성으로 2024년 매출의 56.19%를 차지했습니다. 이 리더십은 철강, 비철금속, 석유화학 등 가동 중단 비용이 재료 가격을 능가하는 자산이 많은 산업에서 정착하고 있습니다. 세라믹 섬유의 고온 단열재 시장 규모는 아시아태평양의 신규 설비가 가동됨에 따라 1자리대의 꾸준한 성장이 예상됩니다.

에어로겔 복합재료 및 미세다공성 패널과 같은 다른 재료 유형은 CAGR 6.18%로 가장 빠르게 성장하는 그룹입니다. 중량을 중시하는 최종 용도는 에어로겔의 0.020W/m*K(와트 매미터·켈빈) 이하의 전도성과 핸들링 강도를 높이는 섬유 보강을 조합하여 평가했습니다. 규제 주도의 저생물 난분해성 화학물질로의 전환은 특히 유럽에서 알칼리 토류 규산염 울의 흡수를 가속화하고 있습니다. 다결정 울은 1,500℃ 이상의 특수 용도에 대응하고, 진공 성형은 현장에서의 건닝이나 래밍에 비용이 많이 드는 복잡한 형상에 대응합니다. 고온 단열재 업계는 샷 함량, 강도, 내열 충격성의 균형을 맞추기 위해 소결 첨가제와 섬유 직경의 개선을 계속하고 있습니다.

지역 분석

아시아태평양의 2024년 시장 점유율은 47.51%로 평가되었고, CAGR은 5.66%를 나타낼 전망입니다. 중국에서는 철강, 알루미늄, 화학의 생산 능력 증진이 진행 중이며 벌크 수요가 유지되는 한편 인도의 국가 인프라 파이프라인과 수소 계획의 확대가 장기적인 성장을 강화하고 있습니다. 동남아시아 국가들은 역시 내화물 라이닝을 필요로 하는 석유화학 및 재생가능 에너지 자산을 늘리고 있습니다. 정책 입안자는 에너지 효율 기준을 점점 강화하고 있으며, 저도전 파이버 모듈과 에어로겔로 구매를 변화시키고 있습니다.

북미는 금액 기준으로 2위입니다. 연방 정부의 청정 에너지 공제와 주 수준의 탄소 상한은 정유소, 액화 천연 가스(LNG) 터미널, 펄프 공장에서의 단열 개수를 경제적으로 매력적으로 하고 있습니다. 이 지역에서는 반도체와 전지 제조의 리쇼어링이 진행되고 있어 초클린 절연 보드와 섬유 강화 에어로겔의 소비가 증가하고 있습니다. 산업 안전 강화도 알칼리 토류 규산염 울의 채용을 가속하고 있습니다.

유럽은 계속 기술 중심의 자세를 무너뜨리지 않고 엄격한 환경규칙과 카본보더 조정을 활용하여 저생물난분해성 재료를 지지하고 있습니다. 유럽연합(EU)의 그린딜 투자는 단열과 방화를 양립시키는 다층 라이닝을 사용한 기존 산업자산의 개수에 박차를 가합니다. 집광형 태양광 발전과 열에너지 저장의 혁신적인 파일럿 프로젝트는 첨단 세라믹을 채택하여 응용 분야를 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 에너지 효율이 높은 공업로 수요 급증

- 고온 단열을 요구하는 건축 에너지 규제의 강화

- 아시아의 석유화학 및 금속 섹터에서의 급속한 생산 능력 증강

- 그린 수소 전해조의 채용에는 고온 라이닝이 필요

- 경량으로 내구성이 있는 단열재 수요의 확대

- 시장 성장 억제요인

- 합성 유리 섬유의 직업 노출 규제

- 알루미나와 실리카의 가격 변동이 컨버터의 마진을 압박

- 고순도 지르코니아 전구체공급 체인·리스크

- 밸류체인 분석

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 업계의 라이벌 관계

제5장 시장 규모와 성장 예측

- 소재 유형별

- 유리 섬유

- 세라믹 섬유

- 광물솜

- 알칼리토금속 규산염(AES)

- 알루미늄 규산염 솜(ASW) 또는 내화 세라믹 섬유(RCF)

- 다결정 솜 또는 섬유(PCW)

- 장섬유

- 진공 성형 단열 제품

- 폴리우레탄 폼

- 폴리스티렌

- 단열 내화 벽돌(IFB)

- 기타 소재 유형(에어로겔 담요, 미세다공성 패널 등)

- 용도별

- 단열

- 산업기기

- 기타 용도(건축 및 방화 등)

- 최종 이용 산업별

- 석유화학

- 산업용

- 발전

- 운송

- 전기 및 전자

- 건설

- 기타 최종 이용 산업(금속 가공 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Alkegen

- Almatis

- Aspen Aerogels, Inc.

- BNZ Materials,Inc.

- Cabot Corporation

- Carlisle Companies Inc.

- Dyson Technical Ceramics

- Etex Group

- ISOLITE

- Knauf Insulation

- Luyang Energy-saving Materials Co., Ltd.

- ME Schupp Industriekeramik Gmbh

- Morgan Advanced Materials

- NUTEC Incorporated

- Pacor Inc.

- Pyrotek

- Rath-Group

- ROCKWOOL A/S

- Saint-Gobain

제7장 시장 기회와 전망

KTH 25.10.31The High-temperature Insulation Materials Market size is estimated at USD 9.24 Billion in 2025, and is expected to reach USD 11.65 Billion by 2030, at a CAGR of 4.75% during the forecast period (2025-2030).

The current market size reflects steady demand growth as energy-intensive industries pursue operational efficiency and lower emissions. Tight building-energy codes, rapid petrochemical and metals capacity additions in Asia-Pacific, and expanding green hydrogen electrolyser installations form the backbone of demand. Manufacturers continue to prioritize non-combustible and low-biopersistent alternatives that satisfy stricter occupational exposure limits. At the same time, vertical integration strategies and regional capacity expansions are helping large suppliers shield themselves from raw-material price swings and logistics bottlenecks. While alumina, silica, and zirconia pricing remains volatile, the economic payback from lower fuel use and maintenance costs keeps adoption on an upward trajectory.

Global High-temperature Insulation Materials Market Trends and Insights

Surging Demand for Energy-Efficient Industrial Furnaces

Industrial furnace builders face stricter energy-performance rules under the 2024 International Energy Conservation Code, which lowered allowable heat loss and tightened air-leakage rates. Operators specify ceramic fibre blankets and microporous panels that endure 1,000°C service without compromising fuel economy. Typical energy savings approach 30% over legacy linings, improving payback despite higher capital cost. Integrating smart thermal management systems with advanced insulation materials enables predictive maintenance and optimized energy consumption, positioning high-temperature insulation as a critical component in Industry 4.0 transformation strategies. .

Tightening Building-Energy Codes Requiring High-Temperature Insulation

The same 2024 International Energy Conservation Code (IECC) revision also sharpened commercial building shell requirements, magnifying interest in continuous insulation and thermal-bridge mitigation. European Union Fit-for-55 directives demand complementary heat- and fire-resistant solutions in industrial facilities, increasingly favoring materials that combine thermal performance with fire safety, driving demand for non-combustible options like mineral wool and ceramic fiber systems. Building owners face escalating energy costs and carbon pricing mechanisms that make high-performance insulation economically attractive over building lifecycles. The convergence of energy efficiency mandates and fire safety requirements creates a sweet spot for high-temperature insulation materials that can address both regulatory imperatives simultaneously.

Occupational Exposure Limits on Synthetic Vitreous Fibres

Regulatory authorities worldwide are tightening occupational exposure limits for synthetic vitreous fibers, with OSHA maintaining permissible exposure limits of 0.2 fibers per cubic centimeter for refractory ceramic fibers . The Health and Safety Executive in the UK has classified refractory ceramic fiber as a category 2 carcinogen, necessitating stringent control measures under COSHH regulations that increase handling costs and limit application flexibility. European legislation increasingly favors low-biopersistent alternatives, driving market share gains for alkaline earth silicate fibers despite their higher costs and slightly reduced temperature capabilities. The regulatory trend toward biosoluble fibers creates opportunities for innovative manufacturers while constraining traditional ceramic fiber applications. Compliance costs and liability concerns are pushing industrial users toward alternative materials, even when performance trade-offs exist. The long-term trajectory suggests continued regulatory pressure that will reshape the competitive landscape in favor of companies with strong low-biopersistent fiber portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Capacity Build-Out in Asian Petro-Chem and Metal Sectors

- Green-Hydrogen Electrolyser Adoption Needs High-Temperature Lining

- Volatile Alumina and Silica Prices Squeeze Converter Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceramic fibre held 56.19% of 2024 revenue owing to its 1,260°C service limit, low density, and adaptability into blankets, modules, and boards. This leadership is anchored in asset-heavy industries, such as steel, non-ferrous metals, and petrochemicals, where downtime costs dwarf material prices. The high-temperature insulation materials market size for ceramic fibre is expected to post steady single-digit growth as new capacities in Asia-Pacific come on stream.

Other material types, such as aerogel composites and microporous panels, are the fastest-growing group at 6.18% CAGR. Weight-sensitive end uses value aerogels' sub-0.020 W/m*K (Watt per metre Kelvin) conductivity combined with fiber reinforcement that boosts handling strength. Regulatory-driven migration to low-biopersistent chemistries accelerates alkaline earth silicate wool uptake, especially in Europe. Polycrystalline wool supports specialized duties above 1,500°C, while vacuum-formed shapes address complex geometries that would require costly on-site gunning or ramming. The high-temperature insulation materials industry continues to refine sintering additives and fiber diameters to balance shot content, strength, and thermal shock resistance.

The High-Temperature Insulation Materials Market Report Segments the Industry Into Material Type (Fiberglass, Ceramic Fibre, Mineral Wool, Polyurethane Foam, and More), Application (Insulation, Industrial Eqipment, and Other Applications), End-User Industry (Petrochemicals, Construction, Transportation, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific had a 47.51% market share in 2024 and is projected to advance at a 5.66% CAGR. China's ongoing capacity additions in steel, aluminum, and chemicals sustain bulk demand, while India's National Infrastructure Pipeline and expanding hydrogen plans reinforce long-term growth. Southeast Asian nations add petrochemical and renewables assets that likewise require refractory linings. Policymakers increasingly enforce energy-efficiency norms, shifting purchasing toward low-conductivity fibre modules and aerogels.

North America ranks second by value. Federal clean energy credits and state-level carbon caps make retrofit insulation economically attractive in refineries, liquidated natural gas (LNG) terminals, and pulp mills. The region's reshoring of semiconductor and battery manufacturing raises consumption of ultra-clean insulation boards and fiber-reinforced aerogels. Robust industrial safety enforcement also accelerates adoption of alkaline earth silicate wool.

Europe remains technology-focused, leveraging its stringent environmental rules and carbon-border adjustments to champion low-biopersistent materials. European Union (EU) Green Deal investments spur renovation of existing industrial assets with multilayer linings that marry insulation and fire-containment. Innovative pilot projects in concentrated solar power and thermal energy storage adopt advanced ceramics, broadening application footprints.

- 3M

- Alkegen

- Almatis

- Aspen Aerogels, Inc.

- BNZ Materials,Inc.

- Cabot Corporation

- Carlisle Companies Inc.

- Dyson Technical Ceramics

- Etex Group

- ISOLITE

- Knauf Insulation

- Luyang Energy-saving Materials Co., Ltd.

- M.E. Schupp Industriekeramik Gmbh

- Morgan Advanced Materials

- NUTEC Incorporated

- Pacor Inc.

- Pyrotek

- Rath-Group

- ROCKWOOL A/S

- Saint-Gobain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Energy-Efficient Industrial Furnaces

- 4.2.2 Tightening Building-Energy Codes Requiring High-Temperature Insulation

- 4.2.3 Rapid Capacity Build-Out in Asian Petro-Chem and Metal Sectors

- 4.2.4 Green-Hydrogen Electrolyser Adoption needs High Temperature Lining

- 4.2.5 Growing Lightweight, Durable Insulation Material Demand

- 4.3 Market Restraints

- 4.3.1 Occupational Exposure Limits on Synthetic Vitreous Fibres

- 4.3.2 Volatile Alumina and Silica Prices Squeeze Converter Margins

- 4.3.3 Supply-Chain Risk for High-Purity Zirconia Precursors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Fiberglass

- 5.1.2 Ceramic Fibre

- 5.1.3 Mineral Wool

- 5.1.3.1 Alkaline Earth Silicate (AES)

- 5.1.3.2 Aluminum Silicate Wool (ASW) or Refractory Ceramic Fibre (RCF)

- 5.1.3.3 Polycrystalline Wool or Fibre (PCW)

- 5.1.3.4 Long Fibre

- 5.1.4 Vacuum-Formed Insulating Products

- 5.1.5 Polyurethane Foam

- 5.1.6 Polystyrene

- 5.1.7 Insulating Fire-Bricks (IFB)

- 5.1.8 Other Material Types (Aerogel Blankets, Microporous Panels, etc.)

- 5.2 By Application

- 5.2.1 Insulation

- 5.2.2 Industrial Eqipment

- 5.2.3 Other Applications (Building and Fire-Protection, etc.)

- 5.3 By End-use Industry

- 5.3.1 Petrochemicals

- 5.3.2 Industrial

- 5.3.3 Power Generation

- 5.3.4 Transportation

- 5.3.5 Electrical and Electronics

- 5.3.6 Construction

- 5.3.7 Other End-use Industries (Metal Processing, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alkegen

- 6.4.3 Almatis

- 6.4.4 Aspen Aerogels, Inc.

- 6.4.5 BNZ Materials,Inc.

- 6.4.6 Cabot Corporation

- 6.4.7 Carlisle Companies Inc.

- 6.4.8 Dyson Technical Ceramics

- 6.4.9 Etex Group

- 6.4.10 ISOLITE

- 6.4.11 Knauf Insulation

- 6.4.12 Luyang Energy-saving Materials Co., Ltd.

- 6.4.13 M.E. Schupp Industriekeramik Gmbh

- 6.4.14 Morgan Advanced Materials

- 6.4.15 NUTEC Incorporated

- 6.4.16 Pacor Inc.

- 6.4.17 Pyrotek

- 6.4.18 Rath-Group

- 6.4.19 ROCKWOOL A/S

- 6.4.20 Saint-Gobain

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Lightweight Refractory Cements for Concentrated-Solar Receivers