|

시장보고서

상품코드

1844738

실리콘 첨가제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Silicone Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

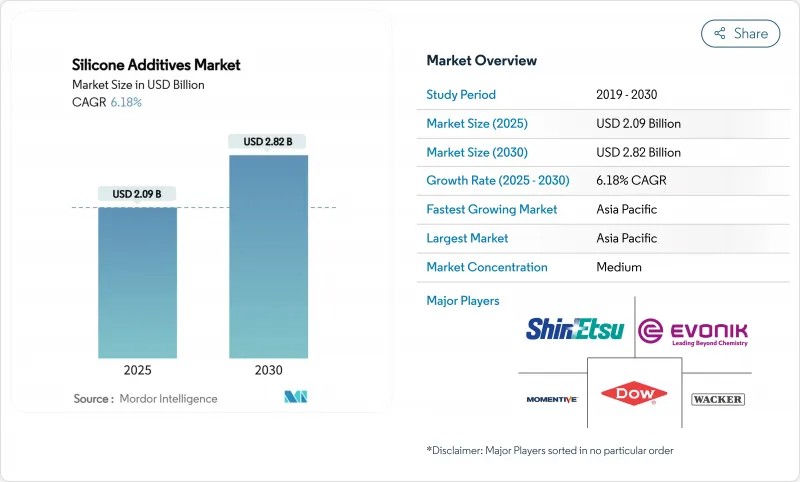

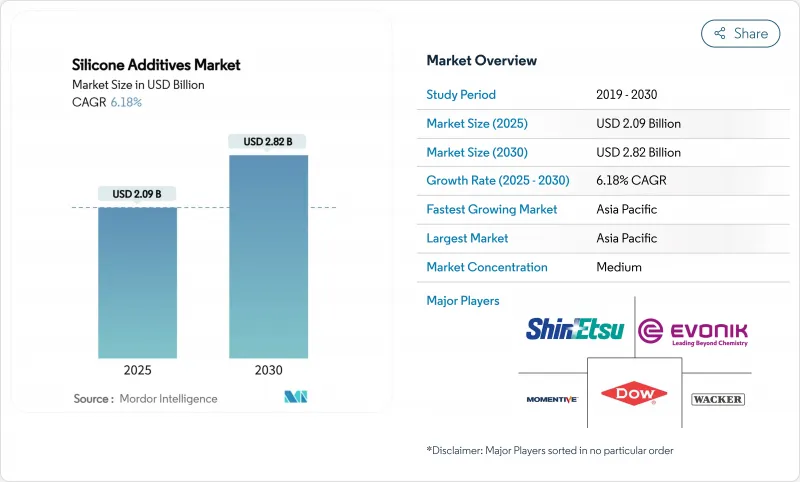

실리콘 첨가제 시장 규모는 2025년에 20억 9,000만 달러로 추정되며 예측 기간 중(2025-2030년) CAGR은 6.18%로, 2030년에는 28억 2,000만 달러에 달할 것으로 예상됩니다.

왕성한 수요는 열, 화학제품, 혹독한 날씨에 따라 코팅제, 중합체 및 유체를 안정적으로 유지하는 첨가제를 찾는 제조업체에 기인합니다. 휘발성 유기화합물(VOC) 배출량 저감의 규제 압력은 성능과 컴플라이언스를 양립시키는 실리콘 풍부한 시스템으로 배합자를 유도하고 있습니다. 성장세는 전기자동차용 열관리, 바이오의 퍼스널케어 제품 출시, 신흥 경제권의 식품 가공 자동화 증가를 반영하고 있습니다. 업계 재편(특히 2024년 KCC에 의한 Momentive 인수)은 규모 우위, 수직 통합, 혁신 파이프라인의 신속화로의 변화를 시사합니다.

세계의 실리콘 첨가제 시장 동향과 인사이트

퍼스널케어 업계에서의 수요 증가

소비자는 유분을 포함하지 않는 은은한 텍스처를 선호하기 때문에 배합자는 실크와 같은 느슨한 퍼짐과 지속적인 수분을 실현하는 실리콘 오일을 선호하게 되었습니다. 예를 들어, Shin-Etsu Chemical의 엘라스토머 인 오일 제품 라인은 원형 실록산의 지역 사용 금지를 충족하면서 원하는 피부 감촉을 유지하는 안정적인 수중 오일 에멀젼을 생산합니다. 공급업체는 Elkem의 PURESIL ORG 젤과 같은 식물 유래의 C13-15 알칸 캐리어를 전개하여 감각적 성능과 자연적인 위치 지정이 공존할 수 있음을 증명합니다. 아시아태평양의 화장품 제조업체는 이러한 특성을 활용하여 세계 프리미엄 브랜드와의 격차를 메우고 컬러 화장품 및 선케어에서 실리콘 첨가제 시장을 확대하고 있습니다.

페인트 및 코팅에서 낮은 VOC 제품에 대한 관심 증가

유럽과 북미의 법규제에 의해 용제의 허용함량에 상한이 설치되어 낮은 VOC에의 적합이 특징이라기보다는 오히려 전제조건이 되고 있습니다. 에보닉 TEGO Guard 9000은 에코 라벨의 임계값을 저촉하지 않고 외장 페인트에 조기 내우성을 제공합니다. 실텍은 장쇄 알킬 실리콘이 고형분을 증가시키면서 VOC를 줄이고, 배합자가 내구성을 유지하면서 그린 씰과 LEED의 목표를 달성할 수 있음을 보여줍니다. 이 파급효과는 신흥 시장에도 미치고 있으며, 건축업자는 방오성과 장기적인 색채를 위해 실리콘 표면 첨가제를 강화한 수성 도료를 지정하게 되었습니다.

고온에서 첨가제 마이그레이션

200 °C를 초과하면, 저분자 실록산은 표면에 블리딩되어 광학 투명성이 떨어지거나 접착성이 약해질 수 있습니다. 높은 페닐 실리콘 고무의 연구는 478° EV용 트랙션 모터나 항공우주용 덕트에는 휘발을 억제하는 배합이 필요하며 연구개발예산을 압박하고 있습니다.

부문별 분석

실리콘 오일은 2024년 실리콘 첨가제 시장 매출의 39.44%를 차지했으며 코팅, 퍼스널케어, 윤활제의 슬립제, 레벨링제, 열전달제로서 폭넓은 용도에 지지되었습니다. 낮은 표면 장력과 폭넓은 온도 안정성이 바닥 견고한 수요를 지원합니다. 에멀젼과 수지는 특히 건축용 실란트에서 수성 시스템과 구조 마감을 가능하게 하여 유체를 보완합니다. 대조적으로, 엘라스토머는 개스킷, 씰, 의료용 튜브와 같은 영구적인 탄성이 필요한 틈새 분야에 대응합니다.

분말과 과립은 매출의 1/4에 미치지 못하지만 2030년까지 연평균 복합 성장률(CAGR)은 7.65%로 가장 빠릅니다. 건조한 모양은 3D 프린팅 원료와 마스터 배치를 배합하는 데 도움이되며, 배합자에게 미세한 유변학 제어와 먼지없는 투여를 가능하게합니다. 새로운 UV 경화형 폴리실록산 파우더는 신속한 프로토타입을 위한 온디맨드 가교를 간소화하고, 설계에서 부품화까지의 사이클을 단축하고, 적층 성형을 위한 실리콘 첨가제 시장 규모를 확대합니다. 프린터가 항공우주뿐만 아니라 치과 및 소비재에까지 확산됨에 따라 분말 실리콘은 새로운 성장의 길을 열고 있습니다.

지역 분석

아시아태평양은 2024년 매출 점유율 47.34%로 실리콘 첨가제 시장의 선두를 차지했고 2030년을 향해 CAGR 7.10%를 나타낼 전망입니다. 중국의 장가항과 난징의 클러스터는 워커와 엘켐의 실록산 업스트림 생산 능력을 지원하고, 전자 및 EV 배터리의 대기업에 공급의 근접성을 확보하고 있습니다. 인도의 'Make in India' 정책은 품질 중심의 코팅제 및 접착제에 대한 국내 수요를 환기하고 고급 마무리와 내구성을 위해 실리콘 첨가제를 배합하도록 국내 배합업체에게 촉구하고 있습니다. 일본과 한국은 각각 선진적인 연구개발을 추진하고, 실리콘 첨가제를 고주파 일렉트로닉스, 포토닉스, 특수 필름에 응용하고 있습니다.

북미는 성숙하지만 기술 혁신이 활발한 지역입니다. 미국은 FDA/USP에 준거한 실리콘 시스템에 의해 의료기기나 항공우주용 복합재료에의 채용을 리드하고 있습니다. 미시간 주에 있는 다우의 실리콘 재활용 파일럿은 폴리디메틸실록산(PDMS)의 이산화탄소 배출량을 50% 줄이는 것을 목표로 하며 ESG 지침에 따라 구매자와 공명하고 있습니다. 캐나다의 EV 배터리 투자와 멕시코 자동차 산업 클러스터는 열 관리 첨가제에 더 많은 보급을 기대하고 있습니다.

유럽은 규모에서는 3위이지만, 지속가능성의 엄격함에서는 1위입니다. REACH와 임박한 PFAS 금지는 환상 화합물을 포함하지 않는 바이오 실리콘 대체물의 연구 개발을 강화합니다. 에보닉의 스마트 이펙트 사업 라인은 실록산과 유기적 스페셜티를 결합, 경량화, e-모빌리티, 디지털 헬스 시장에 임합니다. 독일과 프랑스는 자동차의 전기화 보조금에 주력하고 영국은 생명 과학 분야의 코팅에 중점을 둡니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 퍼스널케어 업계에서의 수요 증가

- 페인트 및 코팅에 있어서의 저VOC 제품에 대한 주목의 고조

- 식품 가공 산업에서의 수요 증가

- 의료 및 헬스케어 분야에서의 용도 확대

- 자동차 산업으로부터의 높은 이용

- 시장 성장 억제요인

- 고온에서의 첨가제의 이행

- 불안정한 원료 비용

- 마이그레이션이나 접착 문제 등의 기술적 과제

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 형태별

- 유체 및 오일

- 엘라스토머 및 검

- 수지

- 분말 및 과립

- 유화액

- 용도별

- 소포제

- 유변학 조절제

- 계면활성제

- 습윤 및 분산제

- 윤활제

- 접착 촉진제

- 기타 용도(이형제 등)

- 최종 사용자 산업별

- 식음료

- 플라스틱 및 복합재료

- 페인트 및 코팅

- 퍼스널케어

- 접착제 및 실란트

- 제지 및 펄프

- 석유 및 가스

- 기타 최종 사용자 산업(전자, 반도체 등)

- 지역

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- AB Specialty Silicones

- Altana AG

- Bluestar Silicones

- BRB International

- Clariant AG

- Dow

- Elkem ASA

- Evonik Industries AG

- Jiangsu Maysta Chemical

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Silibase Silicone

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- The Lubrizol Corporation

- Wacker Chemie AG

제7장 시장 기회와 전망

KTH 25.10.31The Silicone Additives Market size is estimated at USD 2.09 billion in 2025, and is expected to reach USD 2.82 billion by 2030, at a CAGR of 6.18% during the forecast period (2025-2030).

Robust demand stems from manufacturers seeking additives that keep coatings, polymers, and fluids stable under heat, chemicals, and harsh weather. Regulatory pressure to cut volatile-organic-compound (VOC) emissions is steering formulators toward silicone-rich systems that match performance with compliance . Growth momentum also reflects deeper penetration in thermal management for electric vehicles, bio-based personal-care launches, and rising food-processing automation across emerging economies. Industry consolidation-most notably KCC's take-over of Momentive in 2024-signals a shift toward scale advantages, vertical integration, and faster innovation pipelines.

Global Silicone Additives Market Trends and Insights

Increase in Demand from Personal Care Industry

Consumers gravitate toward light, non-oily textures, prompting formulators to favor silicone fluids for silky spread and lasting moisture. Shin-Etsu's elastomer-in-oil line, for example, builds stable oil-in-water emulsions that meet regional bans on cyclic siloxanes while sustaining the desired skin-feel. Suppliers are rolling out plant-origin C13-15 alkane carriers such as Elkem's PURESIL ORG gels, proving that sensory performance and natural positioning can coexist. Asia-Pacific labels are leveraging these attributes to bridge gaps with global premium brands, widening the silicone additives market in color cosmetics and sun care.

Growing Focus on Low-VOC Products in Paints and Coatings

Legislators in Europe and North America cap allowable solvent content, making low-VOC compliance a prerequisite rather than a feature. Evonik's TEGO Guard 9000 delivers early-rain resistance in exterior coatings without breaching eco-label thresholds. Siltech has shown that long-chain alkyl silicones lift solids content yet cut VOC totals, letting formulators maintain durability while meeting Green Seal or LEED targets. The ripple effect extends to emerging markets, where builders increasingly specify water-based paints fortified with silicone surface additives for stain repellence and long-term color retention.

Additive Migration at High Temperatures

Above 200 °C, low-molecular-weight siloxanes can bleed to surfaces, dulling optical clarity or weakening adhesion. Studies on high-phenyl silicone rubbers reveal improved thermal stability, with only 5% weight loss at 478 °C, yet premium grades raise costs. EV traction motors and aerospace ducting need formulations that curb volatilization, pressuring R&D budgets.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from Food-Processing Industry

- Increasing Usage in Medical and Healthcare Applications

- Volatile Raw-Material Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone fluids accounted for 39.44% of the silicone additives market in 2024 by revenue, riding on wide use as slip, leveling, and heat-transfer agents in coatings, personal care, and lubricants. Their low surface tension and broad temperature stability underpin a resilient demand base. Emulsions and resins complement fluids by enabling water-borne systems and structural finishes, particularly in construction sealants. In contrast, elastomers address gasket, seal, and medical-tube niches needing lasting elasticity.

Powders and granules, although less than one-quarter of sales, post the fastest 7.65% CAGR through 2030. Their dry format aids 3D printing feedstocks and masterbatch compounding, granting formulators fine rheology control and dust-free dosing. Emerging UV-curable polysiloxane powders simplify on-demand cross-linking for rapid prototypes, shrinking design-to-part cycles and enlarging the silicone additives market size for additive manufacturing. As printer fleets spread beyond aerospace into dental and consumer goods, powdered silicones capture fresh avenues for growth.

The Silicone Additives Market Report is Segmented by Product Form (Fluids and Oils, Elastomers and Gums, and More), Application (Defoamers, Rheology Modifiers, and More), End-User Industry (Food and Beverage, Plastics and Composites, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific sat atop the silicone additives market with 47.34% revenue share in 2024 and is marching at a 7.10% CAGR toward 2030. China's Zhangjiagang and Nanjing clusters anchor upstream siloxane capacity for Wacker and Elkem, ensuring supply proximity to electronics and EV battery giants. India's "Make in India" policy stokes domestic demand for quality-driven coatings and adhesives, compelling local formulators to incorporate silicone additives for premium finish and durability. Japan and South Korea each foster advanced R&D, channeling silicone additives into high-frequency electronics, photonics, and specialty films.

North America follows as a mature but innovation-rich arena. The United States leads adoption in medical devices and aerospace composites, relying on FDA/USP compliant silicone systems. Dow's silicone recycling pilot in Michigan aims to trim polydimethylsiloxane (PDMS) carbon footprints by 50% and resonates with buyers under ESG mandates. Canada's EV-battery investments and Mexico's automotive clusters promise incremental pull-through for thermal-management additives.

Europe ranks third in size yet first in sustainability stringency. REACH and impending PFAS bans intensify R&D for cyclic-free and bio-based silicone alternatives. Evonik's Smart Effects business line combines siloxane and organic specialties to tackle lightweighting, e-mobility, and digital health markets. Germany and France concentrate vehicle electrification grants, while the United Kingdom emphasizes life-science coatings, collectively protecting a steady flow of high-margin orders.

- AB Specialty Silicones

- Altana AG

- Bluestar Silicones

- BRB International

- Clariant AG

- Dow

- Elkem ASA

- Evonik Industries AG

- Jiangsu Maysta Chemical

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Silibase Silicone

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- The Lubrizol Corporation

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand from Personal Care Industry

- 4.2.2 Growing Focus on Low-VOC Products in Paints and Coatings

- 4.2.3 Growing Demand from Food-Processing Industry

- 4.2.4 Increasing Usage in Medical and Healthcare Applications

- 4.2.5 High Utilization from the Automotive Industry

- 4.3 Market Restraints

- 4.3.1 Additive Migration at High Temperatures

- 4.3.2 Volatile Raw-material Costs

- 4.3.3 Technical Challenges such as Migration and Adhesion Issues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Product Form

- 5.1.1 Fluids and Oils

- 5.1.2 Elastomers and Gums

- 5.1.3 Resins

- 5.1.4 Powders and Granules

- 5.1.5 Emulsions

- 5.2 By Application

- 5.2.1 Defoamers

- 5.2.2 Rheology Modifiers

- 5.2.3 Surfactants

- 5.2.4 Wetting and Dispersing Agents

- 5.2.5 Lubricating Agents

- 5.2.6 Adhesion Promoters

- 5.2.7 Other Applications (Release Agents, etc.)

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Plastics and Composites

- 5.3.3 Paints and Coatings

- 5.3.4 Personal Care

- 5.3.5 Adhesives and Sealants

- 5.3.6 Paper and Pulp

- 5.3.7 Oil and Gas

- 5.3.8 Other End-User Industries (Electronics and Semiconductor, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AB Specialty Silicones

- 6.4.2 Altana AG

- 6.4.3 Bluestar Silicones

- 6.4.4 BRB International

- 6.4.5 Clariant AG

- 6.4.6 Dow

- 6.4.7 Elkem ASA

- 6.4.8 Evonik Industries AG

- 6.4.9 Jiangsu Maysta Chemical

- 6.4.10 KCC SILICONE CORPORATION

- 6.4.11 Momentive

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Silibase Silicone

- 6.4.14 Siltech Corporation

- 6.4.15 Supreme Silicones India Pvt. Ltd.

- 6.4.16 The Lubrizol Corporation

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Analysis

- 7.2 Growing Research and Development to Improve the Sustainability of Silicones