|

시장보고서

상품코드

1846144

시트 성형 및 벌크 성형 컴파운드 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Sheet Molding And Bulk Molding Compounds - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

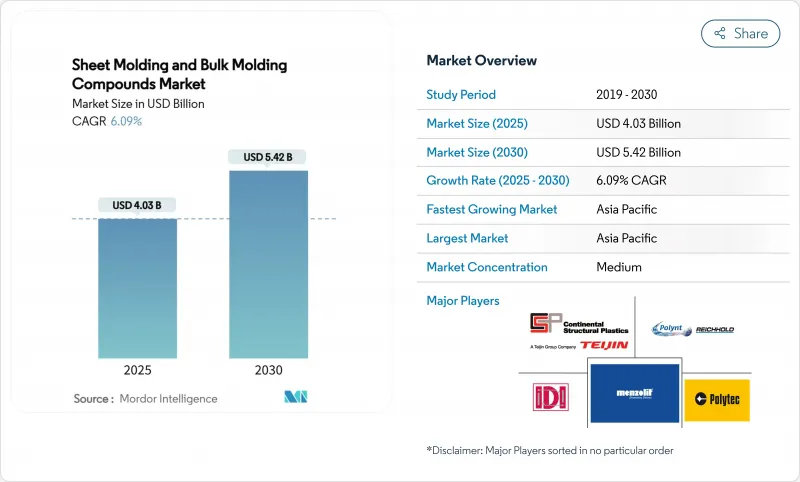

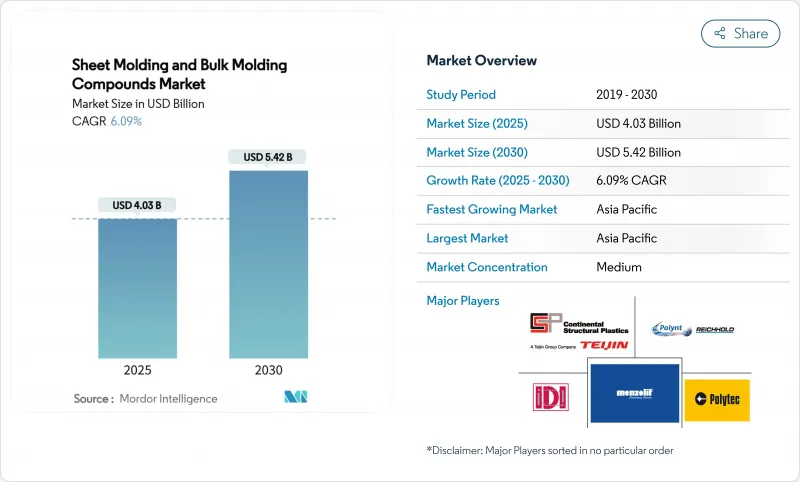

시트 성형 및 벌크 성형 컴파운드 시장 규모는 2025년에 40억 3,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.09%로 성장할 전망이며, 2030년에는 54억 2,000만 달러에 이를 것으로 예측됩니다.

전기자동차의 경량 구조 부품에 대한 수요의 지속, 압축 성형에 의한 스크랩율의 저하, 수지의 화학적 성질 개선에 의해 새로운 생산 능력에 대한 자본 유입이 계속되고 있습니다. 부품 당 비용 절감, 특히 이전에는 다단 프레스 성형에 의존했던 복잡한 형상의 비용 절감은 자동차 및 전기 장비 용도 분야 전체에서 금속 프레스 성형에의 압축 성형 컴파운드로의 교체를 가속화하고 있습니다. 주문자 상표 부착 제품 제조업체는 현재 클래스 A 마감재의 고급 시트 성형 재료를 지정하여 직접 외장에 사용할 수 있도록 하고, 일단 채용을 제한하고 있던 2차적인 도장 공정을 생략하고 있습니다. 아시아태평양은 높은 유동성, 저밀도 시트 성형 화합물의 비용 리더를 유지하고 있지만, 스티렌 배출에 관한 유럽 규정에 따라 에폭시 기반 대체품이 급격히 개발되고 있습니다.

세계의 시트 성형 및 벌크 성형 컴파운드 시장 동향 및 인사이트

전기자동차와 및하이브리드 자동차 OEM에 의한 경량화 추진

전기자동차는 큰 배터리 팩을 탑재하기 때문에 1킬로그램의 경량화로 항속 거리가 늘어납니다. 따라서 자동차 제조업체는 폐쇄, 바디 패널 및 배터리 하우징의 설계를 충돌 하중 경로 및 열 차폐 요구를 충족시키면서 동등한 알루미늄 설계에 비해 부품 중량을 최대 40% 줄이는 첨단 시트 성형 컴파운드를 사용하여 검토하고 있습니다. 테슬라, 제너럴 모터스, 중국의 주요 브랜드는 단발 압축 성형을 채택하고 용접 작업 및 라인의 택트 타임을 단축하는 다중 부품 통합 전략의 개요를 발표합니다. 시트 성형 및 벌크 성형 컴파운드 시장 진출 기업은 이러한 프로그램이 파일럿 생산에서 전체 생산으로 확장됨에 따라 이익을 얻고 있습니다.

전기 및 전자 부품 성형 허브의 급속한 생산 능력 향상

중국, 베트남, 말레이시아의 APAC 일렉트로닉스 클러스터는 자동 재료 공급과 적외선 경화 제어를 갖춘 고톤테이지 압축 프레스의 설치를 계속하고 있습니다. 컴파운더, 몰더 및 엔드 디바이스의 어셈블러가 공동으로 위치함으로써 공급망이 단축되고 제조업체는 커넥터 하우징 및 모터 절연 시스템에 필요한 엄격한 치수 공차를 충족할 수 있습니다. 고성능 폴리머의 자급을 목표로 하는 중국 정부 프로그램은 이러한 사업 확대를 강화하고 이 지역이 세계적인 수요 급증을 지원할 수 있도록 자리매김하고 있습니다.

스티렌 및 유리 섬유의 가격 변동

스티렌 단량체는 단단한 사이클로 거래되며 벤젠 원료의 변동과 출하 제약에 반응합니다. 스티렌의 톤당 100달러의 변동은 수지 가격에 연쇄되어 장기 공급 계약이 없는 소규모 시트 성형 컴파운드 업체의 마진을 압박합니다. 많은 구조용 등급에서 유리섬유 함량이 65wt%에 가까워지기 때문에 동시에 발생하는 유리섬유 서차지가 가격 안정을 더욱 방해하고 있습니다.

부문 분석

폴리에스테르 수지는 2024년 시트 성형 및 벌크 성형 컴파운드 시장 점유율의 55.19%를 차지했으며, 저비용, 광범위한 공급업체 기반 및 기존의 압축 라인에 맞는 경화 속도를 가졌습니다. 이 부문은 자동차의 언더푸드 커버 및 구조용 인테리어 브래킷과 같은 수요로부터 계속해서 이익을 얻고 있습니다. 동시에, 에폭시 등급은 2030년까지 CAGR 6.92%로 성장할 전망으로, 이는 휘발성 유기 화합물의 함량의 감소와 전기 드라이브 트레인 설계자에게 어필하는 내열성의 향상에 의한 것입니다. 에보닉이 주도한 유리 섬유 강화 에폭시 배터리 하우징의 프로그램은 차량 호모로게이션에 중요한 크래시포스 임계값을 유지하면서 10%에 육박하는 중량 삭감을 검증했습니다. 에폭시 시스템이 성숙함에 따라 경제성과 강도의 균형을 맞추기 위해 폴리 에스테르 스킨과 에폭시 코어를 혼합 한 하이브리드 레이업이 나타날 수 있습니다.

유리 섬유는 양호한 비용 성능과 전기 부품용의 우수한 절연 내력으로 2024년 매출의 80.22%를 유지했습니다. 주요 유리 섬유 제조업체의 지속적인 퍼니스 증설은 공급을 안정화시키고 아시아태평양과 북미의 대량 자동차 유리 섬유 출시를 지원합니다. 탄소섬유 시트 성형 컴파운드는 CAGR 7.06%를 기록해 항공우주 산업의 2차 구조물과 프리미엄 스포츠카로 기세를 늘리고 있습니다. 섬유 배향을 매핑하는 공정 시뮬레이션 툴은 개발 사이클을 단축하고 예측 가능한 기계적 성능을 제공하며 스크랩 속도를 줄입니다. 유리층과 탄소층을 번갈아 배치하는 하이브리드화 섬유 매트는 강성을 희생하지 않고 중급 수준의 비용 목표를 달성하는 데 도움이 됩니다.

시트 성형 및 벌크 성형 컴파운드 시장 보고서는 수지 유형별(에폭시, 폴리에스테르), 섬유 유형별(유리 섬유, 탄소섬유), 제조 공정별(압축 성형, 트랜스퍼 성형, 기타), 최종 사용자 산업별(자동차 및 운송, 전기 및 전자, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분되어 있습니다.

지역 분석

아시아태평양은 비용 우위를 유지하고 2024년 점유율 48.54%를 지원했습니다. 국내 EV 생산 활성화, 중간층 가전 소비 증가, 복합 부품 국산화에 대한 정부 우대 조치로 프레스기는 거의 생산 가능한 상태로 가동하고 있습니다. 추정 수요 성장률은 지역별 CAGR 6.45%로 성장이 전망되며, 시트 성형 및 벌크 성형 컴파운드 시장은 아시아의 밸류 체인으로 계속 옮겨가고 있습니다.

북미는 지역별 매출액으로 2위입니다. 초기 전동 픽업 출시에는 대형 구조 커버가 필요하며, 항공우주 프로그램에서는 2차 구조에 고탄성 탄소 시트 성형 컴파운드가 사용되고 있습니다. 육상 배터리 공장에 자금을 제공하는 연방 정책은 새로운 복합 배터리 박스 라인을 장려하고 현지의 복합 소비를 인상하고 있습니다.

유럽은 엄격한 환경 규제를 유지하고 낮은 스티렌 시트 성형 시스템과 에폭시 기술 혁신의 채택에 박차를 가하고 있습니다. 2030년부터 2035년까지 내연 기관을 폐지하는 자동차 제조업체의 로드맵은 경량 복합재료 수요를 확대할 전망입니다. 반면에 견고한 화학 산업의 인프라는 기계적 성능을 높이고 금형 수명을 연장하는 특수 수지 첨가제를 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전기자동차와 하이브리드 자동차 OEM에 의한 경량화 추진

- 전기 및 전자 부품 성형 허브에서 급속한 생산 능력 증강

- 비용 효율적인 대량 압축 성형 및 금속 프레스 성형의 비교

- 클래스 A 보디 패널을 가능하게 하는 고유동, 저밀도의 시트 성형 부품(SMC)

- 스마트 패널을 위한 인몰드 일렉트로닉스(IME)의 통합

- 시장 성장 억제요인

- 스티렌 및 유리 섬유의 가격 변동

- 배터리 박스의 시트 성형 부품(SMC)을 대체하는 엔지니어링 열가소성 플라스틱

- 열경화성 수지의 사용 후 재활용 장벽

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 수지 유형별

- 폴리에스테르

- 에폭시

- 섬유 유형별

- 유리 섬유

- 탄소 섬유

- 제조 공정별

- 압축 성형

- 사출 및 트랜스퍼 성형

- 수지 트랜스퍼 성형(RTM)

- 인발 성형

- 최종 사용자 산업별

- 자동차 및 운송

- 전기 및 전자

- 건축 및 건설

- 항공우주

- 가정용 가전제품

- 기타 최종 사용자 산업(에너지 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- AOC

- Ashland Container Corporation

- Astar SA

- Continental Structural Plastics(Teijin)

- Core Molding Technologies

- CSP

- DIC Corporation

- IDI Composites International

- Kingfa Sci.&Tech. Co.,Ltd.

- LyondellBasell Industries Holdings BV

- Menzolit

- National Manufacturing Group

- OPmobility SE

- POLYNT SPA

- Polynt-Reichhold

- Polytec Group

- Polytec Masterbatch LLC

- TORAY INDUSTRIES, INC.

제7장 시장 기회 및 전망

AJY 25.11.07The Sheet Molding & Bulk Molding Compounds Market size is estimated at USD 4.03 billion in 2025, and is expected to reach USD 5.42 billion by 2030, at a CAGR of 6.09% during the forecast period (2025-2030).

Sustained demand for lightweight structural parts in electric vehicles, low scrap rates from compression molding, and improved resin chemistries keep capital flowing into new capacity. Cost reductions per part, especially in complex geometries that previously relied on multi-stage stamping, accelerate the replacement of metal stampings with compression-molded composites across automotive and electrical applications. Original equipment manufacturers now specify advanced sheet molding materials with Class-A finishes, allowing direct exterior use and eliminating secondary paint steps that once limited adoption. Asia-Pacific retains cost-leadership in high-flow, low-density sheet molding compounds, while European regulations on styrene emissions fast-track epoxy-based alternatives.

Global Sheet Molding And Bulk Molding Compounds Market Trends and Insights

Light-weighting Push from Electric Vehicles and Hybrid Vehicle OEMs

Electric models move large battery packs, so every kilogram saved extends range. Automakers therefore redesign closures, body panels, and battery housings with advanced sheet molding compounds that cut part weight by up to 40% versus comparable aluminum designs while satisfying crash-load pathways and thermal shielding demands. Tesla, General Motors, and leading Chinese brands have publicly outlined multi-part consolidation strategies that favor single-shot compression molding, reducing weld operations and line takt time. Sheet molding and bulk molding compounds market participants benefit as these programs scale from pilot to full volume production.

Rapid Capacity Additions in Electrical and Electronics Components Molding Hubs

APAC electronics clusters in China, Vietnam, and Malaysia continue installing high-tonnage compression presses equipped with automated material dosing and infrared curing control. Co-location of compounders, molders, and end-device assemblers shortens supply chains and helps manufacturers meet stringent dimensional tolerances required for connector housings and motor insulation systems. Government programs in China that target self-sufficiency in high-performance polymers reinforce this build-out, positioning the region to support global demand spikes.

Styrene and Fiberglass Price Volatility

Styrene monomer trades in tight cycles, reacting to benzene feedstock swings and shipping constraints. Each USD 100 per ton change in styrene cascades into resin pricing, squeezing margins for small sheet molding compounders that lack long-term supply contracts. Simultaneous fiberglass surcharges further hinder price stability because glass fiber content approaches 65 wt % in many structural grades.

Other drivers and restraints analyzed in the detailed report include:

- Cost-effective High-volume Compression Molding versus Metal Stamping

- High-flow, Low-density Sheet Molding Components Enabling Class-A Body Panels

- Engineering Thermoplastics Replacing SMC in Battery Boxes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester resin accounted for 55.19% sheet molding and bulk molding compounds market share in 2024 thanks to low cost, broad supplier base, and cure kinetics tailored to legacy compression lines. The segment continues to profit from automotive demand for under-hood covers and structural interior brackets. At the same time epoxy grades post a 6.92% CAGR toward 2030, driven by reduced volatile organic compound content and elevated heat resistance that appeals to electric drivetrain designers. The Evonik-led program for glass-fiber-reinforced epoxy battery housings validated weight reductions approaching 10% while maintaining crush-force thresholds critical to vehicle homologation. As epoxy systems mature, hybrid lay-ups that blend polyester skins with epoxy cores may emerge to balance economics and strength.

Glass fiber kept 80.22% of 2024 revenue due to favorable cost-to-performance and excellent dielectric strength for electrical parts. Continuous furnace expansions at major glass fiber producers stabilize supply, supporting high-volume automotive launches in Asia-Pacific and North America. Carbon fiber sheet molding compounds, posting a 7.06% CAGR, gain momentum in aerospace secondary structures and premium sports cars where curb-weight targets override raw-material premiums. Process simulation tools mapping fiber orientation now shorten development cycles, delivering predictable mechanical performance and cutting scrap rates. Hybridized fiber mats that alternate glass and carbon layers help designers hit mid-tier cost targets without compromising stiffness.

The Sheet Molding & Bulk Molding Compounds Market Report is Segmented by Resin Type (Epoxy and Polyester), Fiber Type (Glass Fiber and Carbon Fiber), Manufacturing Process (Compression Molding, Transfer Molding, and More), End-User Industry (Automotive and Transportation, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific retains the cost advantage that underpins its 48.54% share in 2024. Intensifying domestic EV production, rising middle-class appliance consumption, and government incentives for composite part localization keep presses running near capacity. With estimated demand growth translating to a 6.45% regional CAGR, the sheet molding and bulk molding compounds market continues to shift toward Asian value chains.

North America sits second in regional revenue. Early electric-pickup launches require large structural covers, and aerospace programs consume high-modulus carbon sheet molding compounds for secondary structures. Federal policy that funds onshore battery factories encourages new composite battery-box lines, lifting local compound consumption.

Europe upholds strict environmental rules that spur adoption of low-styrene sheet molding systems and epoxy innovations. Automaker roadmaps that phase out internal combustion between 2030 and 2035 expand demand for lightweight composites. Meanwhile, robust chemical-industry infrastructure supports specialized resin additives that raise mechanical performance and prolong mold life.

- AOC

- Ashland Container Corporation

- Astar S.A.

- Continental Structural Plastics (Teijin)

- Core Molding Technologies

- CSP

- DIC Corporation

- IDI Composites International

- Kingfa Sci.&Tech. Co.,Ltd.

- LyondellBasell Industries Holdings B.V.

- Menzolit

- National Manufacturing Group

- OPmobility SE

- POLYNT SPA

- Polynt-Reichhold

- Polytec Group

- Polytec Masterbatch LLC

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Light-weighting Push from Electric Vehicles and Hybrid Vehicle OEMs

- 4.2.2 Rapid Capacity Additions in Electrical and Electronics Components Molding Hubs

- 4.2.3 Cost-effective High-volume Compression Molding versus Metal Stamping

- 4.2.4 High-flow, Low-density Sheet Molding Components (SMC) enabling Class-A body Panels

- 4.2.5 Integration of In-mold Electronics (IME) for Smart Panels

- 4.3 Market Restraints

- 4.3.1 Styrene and Fiberglass Price Volatility

- 4.3.2 Engineering Thermoplastics Replacing Sheet Molding Components (SMC) in Battery Boxes

- 4.3.3 End-of-life Recycling Hurdles for Thermosets

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyester

- 5.1.2 Epoxy

- 5.2 By Fiber Type

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.3 By Manufacturing Process

- 5.3.1 Compression Molding

- 5.3.2 Injection / Transfer Molding

- 5.3.3 Resin Transfer Molding (RTM)

- 5.3.4 Pultrusion

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Electrical and Electronics

- 5.4.3 Building and Construction

- 5.4.4 Aerospace

- 5.4.5 Domestic Appliances

- 5.4.6 Other End-user Industries (Energy, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AOC

- 6.4.2 Ashland Container Corporation

- 6.4.3 Astar S.A.

- 6.4.4 Continental Structural Plastics (Teijin)

- 6.4.5 Core Molding Technologies

- 6.4.6 CSP

- 6.4.7 DIC Corporation

- 6.4.8 IDI Composites International

- 6.4.9 Kingfa Sci.&Tech. Co.,Ltd.

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Menzolit

- 6.4.12 National Manufacturing Group

- 6.4.13 OPmobility SE

- 6.4.14 POLYNT SPA

- 6.4.15 Polynt-Reichhold

- 6.4.16 Polytec Group

- 6.4.17 Polytec Masterbatch LLC

- 6.4.18 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment