|

시장보고서

상품코드

1846146

스트리밍 분석 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Streaming Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

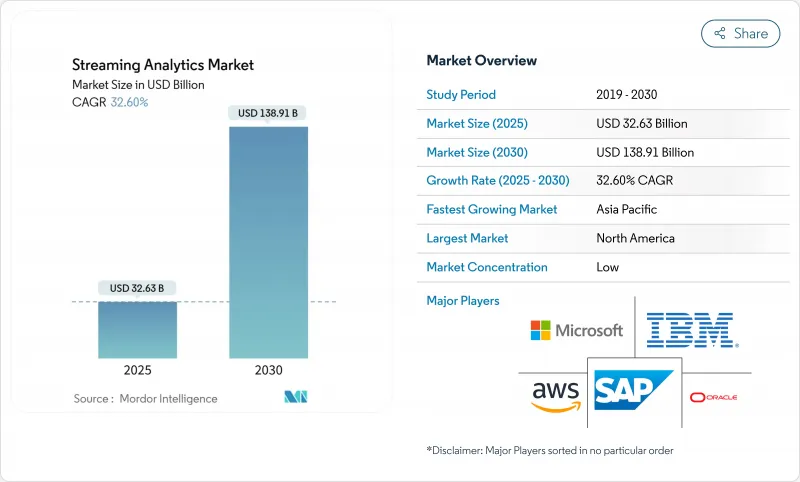

스트리밍 분석 시장의 2025년 시장 규모는 326억 3,000만 달러로 추정되고, 2030년에는 1,389억 1,000만 달러에 이를 전망이며, CAGR 33.6%로 성장할 것으로 예측됩니다.

지속적으로 흐르는 데이터로부터 생성되는 순간에 가까운 인사이트는 기업이 배치 처리에서 응답성이 높은 AI를 강화한 의사결정 루프로 축발을 옮기면서 이사회의 우선사항이 되고 있습니다. 데이터 파이프라인에 직접 통합된 생성 모델, 에지 추론 칩의 광범위한 가용성 및 관리형 클라우드 서비스 증가로 인해 데이터 검색부터 작업까지의 시간이 크게 단축됩니다. 공급업체는 프로비저닝 부담 없이 실시간 워크로드를 확장할 수 있도록 종량 과금 가격을 개선하고 오케스트레이션을 간소화합니다. 초기 채용 기업은 부정 검지나 추천 엔진에 주력하고 있었지만, 2025년에는 산업용 신뢰성 이용 사례, 원격 의료 모니터링, 5G 대응 네트워크 최적화 등이 증가하는 것으로 보여지고 있습니다. 데이터 전송 비용에 대한 민감도와 인력 부족이 기타 왕성한 수요를 억제하고 있지만, 이벤트 기반 아키텍처로의 기본적인 변화로 인해 스트리밍 분석 시장은 급성장 노선을 유지하고 있습니다.

세계의 스트리밍 분석 시장 동향 및 인사이트

생성형 AI를 통합한 데이터 파이프라인

높은 처리량 브로커와 통합된 컨텍스트 인식 모델은 원시 이벤트를 밀리초 단위로 처방적 조치로 변경됩니다. 언어 모델과 스트리밍 텔레메트리를 결합한 금융기관은 오감지를 줄이면서 부정 검사의 정확도를 40% 향상시켰다고 보고하고 있습니다. Confluent Tableflow와 Databricks Delta Lake 간의 양방향 커넥터는 모델에 항상 신선하고 풍부한 데이터를 제공하므로 수동 업데이트 사이클이 필요하지 않습니다. 소매업체는 프로모션 매개변수를 실시간으로 자동 조정하여 플래시 세일 시 전환율을 높일 수 있습니다. 벡터 검색 및 시맨틱 인리치먼트를 위한 라이브러리가 코어 스트림 엔진에 합류함에 따라 예측 유지보수 및 비정상적인 트리어지는 대시보드에서 폐쇄 루프 자율성으로 이동하고 있습니다. 그 결과, 기존의 ETL의 레이턴시 페널티에 시달리지 않고 AI를 운용하려는 기업의 의욕이 높아지고 있습니다.

온 디바이스 처리를 가능하게 하는 엣지 AI 칩

NVIDIA의 Jetson AGX Thor는 이전 세대의 최대 8배의 컴퓨팅과 128GB의 메모리를 제공하여 소스에서 엄청난 변환 추론을 지원합니다. 제조업체는 진동 센서 옆에 이 모듈을 배치하여 비용이 많이 드는 다운타임이 발생하기 전에 베어링의 마모를 감지할 수 있습니다. 병원은 엣지 추론을 활용하여 환자의 생명력이 벗어날 때 간호사에게 경고하고 지속적인 클라우드 업로드를 제한하는 개인 정보 보호 규칙을 준수합니다. Groq의 LPU와 같은 새로운 액셀러레이터는 토큰 생성을 초당 300개의 토큰으로 끌어올려 대화 어시스턴트를 키오스크 단말기 내에서 실행할 수 있게 합니다. 백홀 대기 시간과 대역폭 수수료를 피함으로써 기업은 안정적인 연결성이 없는 선박, 광산, 지역 셀 타워에서 실시간 이용 사례를 풀 수 있습니다. 이 기술은 스트리밍 분석 시장의 지리적 범위를 넓히는 동시에 데이터 주권 규정 준수를 강화합니다.

증가 Kafka 기술 세트의 부족과 임금 인플레이션

Fortune 100 기업의 80% 이상이 Kafka를 사용하고 있음에도 불구하고 채용 정보 사이트에는 자격을 갖춘 엔지니어보다 훨씬 더 많은 모집이 게재되어 있습니다. 미국 급여는 10만 달러를 넘어 중견기업 예산을 압박하고 있습니다. 브로커, 복제 요소, 의미론의 정확성 등에 대한 어려운 학습 곡선이 신인을 망설이는 반면, 클라우드 벤더가 고위 직원을 끌어내기 때문에 인재 확보는 어렵습니다. 관리 플랫폼은 도움이 되지만, 유연성과 교환하여 구독 비용이 부과됩니다. 컨설팅 파트너는 교육 부트 캠프를 확대하고 있지만 시작에 걸리는 시간은 여전히 프로젝트 기한보다 늦습니다. 교육 파이프라인이 따라잡을 때까지 인재 부족은 특히 아웃소싱이 제약되는 규제 분야에서의 전개를 억제하는 것으로 보입니다.

부문 분석

브로커, 프로세서, 대화형 쿼리 엔진의 폭넓은 채용을 반영해 솔루션이 2024년 스트리밍 분석 시장의 구조적 백본이 되어 매출은 65.4%를 차지했습니다. 하지만 기업이 설계도, 전환 지원, 24시간 365일 SRE 지원을 요구하고 있기 때문에 서비스는 2030년까지 연평균 복합 성장률(CAGR) 33.8%로 가속화되고 있습니다. 아키텍처 평가, 데이터 품질 개선, 스키마 거버넌스는 새로운 업무 명세서의 대부분을 차지합니다. Confluent와 EY는 2025년에 전략적 제휴를 맺고, 구현 가속기를 번들함으로써 외부 전문 지식에 대한 수요를 명확히 하고 있습니다. 관측 가능성과 비용 최적화에 대한 요구가 높아짐에 따라 관리형 서비스는 간단한 호스팅에서 이벤트 속도를 기반으로 용량의 자동 조정까지 확장됩니다.

기술 부족으로 인해 위험을 피하는 분야조차도 런타임 운영을 아웃소싱하게 되고 예산은 자본 지출에서 경상 서비스로 이동하고 있습니다. 공급업체의 로드맵에 따르면 PCI-DSS 및 HIPAA를 지원하는 컴플라이언스 모듈이 구독 계층에 사전 패키지되어 있어 규제 도입 장벽이 낮습니다. 그 결과 스트리밍 분석의 전문 서비스와 매니지드 서비스 시장 규모는 핵심 소프트웨어 수익을 초과할 것으로 예상되며, 도구 수가 아닌 노하우가 공급자를 차별화하는 선순환이 강화됩니다.

클라우드는 2024년 매출의 59.5%를 차지했으며, CAGR은 34.2%로 전망됩니다. 하이퍼스케일러는 자동 스케일링 스트림 엔진을 레이크하우스 및 벡터 데이터베이스와 결합하여 하드웨어를 조달하지 않고도 ML 기능을 인제스트, 강화 및 제공할 수 있습니다. Google Cloud는 Pub/Sub, Dataflow, BigQuery, Vertex AI를 관리되는 연속체에 연결하여 분산 시스템의 인력이 부족한 기업의 부담을 경감하고 있습니다. 온프레미스 워크로드를 대상으로 하는 스트리밍 분석 시장 규모는 방위, 핀테크, 공중보건에서 여전히 중요하지만, 업데이트 사이클과 자본 투자 장애물로 인해 클라우드 성장에 미치지 못합니다.

하이브리드 블루프린트는 클라우드의 ML 엔드포인트로 집계를 전송하기 전에 Azure SQL Edge를 사용하여 공장 내에서 민감한 원격 측정을 처리하여 igless 비용을 줄입니다. 공급자는 이제 정책 기반 주제 배치를 가능하게 하고 개별 파티션이 국경 내에 유지되도록 하여 새로운 주권 규칙을 충족합니다. 향후 IAM, 계보 및 거버넌스에 걸친 멀티클라우드 페더레이션 도구는 구매자가 출구 비용을 보호하기 위해 공급업체 선택에 영향을 미칠 것으로 보입니다.

지역 분석

북미는 조기 하이퍼스케일러 생태계와 성숙한 카프카 전문가 집단을 통해 2024년 29.7%의 매출을 획득했습니다. 금융 서비스, 라이드 헤일링, 소매 파이오니어가 ROI를 검증하고, 레퍼런스 디자인을 만들며, 분야를 넘어 보급했습니다. 그러나 포화 상태이기 때문에 점진적인 성장은 바람직하지 않으며, 숙련 노동자의 병목 현상은 도입 예산에 영향을 미치는 임금 프리미엄을 유발합니다. 기상, 산불, 이동 등을 커버하는 실시간 공공 부문 대시보드를 요구하는 정부의 움직임은 엄격한 컴플라이언스 수준인 반면, 안정된 수요를 추가하고 있습니다.

아시아태평양은 5G 전개, 스마트 팩토리 프로그램, 소블린 클라우드 이니셔티브가 융합하여 CAGR이 34.1%로 가장 빠릅니다. 중국의 AI 매출 예측은 2030년까지 3,000억 달러 가까이에 이를 전망이며, 엣지 스트리밍은 자율 생산 셀에 필수적이라고 여겨지고 있습니다. 인도의 공공 디지털 인프라는 이벤트 스트림을 세금, ID 및 결제 레일에 통합하고 동남아시아 전자상거래 플랫폼은 실시간 개인화에 따라 모바일 사용자를 획득했습니다. 또한 동남아시아의 전자상거래 플랫폼은 모바일 사용자와의 경쟁을 극복하기 위해 실시간 개인화를 위해 노력하고 있습니다. 현지 칩 제조업체와 통신 사업자는 공동 혁신을 통해 하드웨어 비용을 절감하고 지역 벤더 에코시스템을 강화함으로써 보급세를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 생성형 AI를 통합한 데이터 파이프라인

- 온 디바이스 스트림 처리를 가능하게 하는 엣지 AI칩

- 시민 개발자용의 로우 코드, 노코드 및 스트리밍, 워크 벤치

- 이벤트 구동형 마이크로서비스의 주류화

- 클라우드 스트림 애널리틱스에 대한 중소기업 수요 증가(컨센서스 드라이버)

- IoT 및 산업 자동화 확대(컨센서스 드라이버)

- 시장 성장 억제요인

- Kafka 스킬 세트 부족 및 임금 인플레이션 증가

- 하이퍼스케일러 클라우드에서 이글레스 요금 상승

- 국경을 넘은 스트림 플로우를 제한하는 데이터 주권 규제

- 레거시한 배치 중심의 아키텍처가 이행 지연 초래(컨센서스)

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 시장에 주는 거시경제 요인의 평가

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 소프트웨어

- 서비스별

- 전개별

- 온프레미스

- 클라우드 기반

- 최종 사용자 업계별

- 미디어 및 엔터테인먼트

- 소매 및 전자상거래

- 제조업

- BFSI

- 헬스케어 및 생명과학

- 운송 및 물류

- 통신업계

- 기타

- 조직 규모별

- 대기업

- 중소기업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Amazon Web Services

- Google(Alphabet)

- Confluent Inc.

- TIBCO Software Inc.

- Software AG

- SAS Institute Inc.

- Striim Inc.

- Impetus Technologies

- Databricks

- Snowflake Inc.

- Apache Software Foundation(Kafka/Flink)

- Cloudera Inc.

- Ververica

- Aiven Ltd.

- Timeplus

- Hazelcast Inc.

- StreamSets Inc.

- Redpanda Data

- Cisco Systems(ThousandEyes)

제7장 시장 기회 및 전망

AJY 25.11.07The streaming analytics market is valued at USD 32.63 billion in 2025 and is forecast to reach USD 138.91 billion by 2030, advancing at a 33.6% CAGR.

Near-instant insights generated from continuously flowing data are becoming a board-room priority as enterprises pivot away from batch practices toward responsive, AI-enhanced decision loops. Generative models embedded directly inside data pipelines, wide availability of edge inference chips, and a growing set of managed cloud services collectively compress the time between data capture and action. Vendors are refining pay-as-you-go pricing and simplifying orchestration so that firms can scale real-time workloads without provisioning burdens. While early adopters focused on fraud detection and recommendation engines, 2025 sees an uptick in industrial reliability use cases, telehealth monitoring, and 5G-enabled network optimization. Heightened sensitivity to data-transfer charges and talent scarcity temper otherwise robust demand, yet the fundamental shift toward event-driven architectures keeps the streaming analytics market on a steep growth path.

Global Streaming Analytics Market Trends and Insights

Generative-AI Infused Data Pipelines

Context-aware models integrated with high-throughput brokers turn raw events into prescriptive actions in milliseconds. Financial institutions combining language models with streaming telemetry report 40% gains in fraud-detection accuracy while slashing false positives. Bidirectional connectors between Confluent Tableflow and Databricks Delta Lake keep models supplied with fresh, lineage-rich data, eliminating manual refresh cycles. Retailers now auto-tune promotion parameters in real time, lifting conversion rates during flash sales. As libraries for vector search and semantic enrichment join core stream engines, predictive maintenance and anomaly triage are shifting from dashboards to closed-loop autonomy. The result is a broader enterprise appetite to operationalize AI without the latency penalties of traditional ETL.

Edge AI Chips Enabling On-Device Processing

NVIDIA's Jetson AGX Thor supplies up to 8 times the prior-generation compute, with 128 GB memory supporting hefty transformer inference at source. Manufacturers deploy the module next to vibration sensors so that models flag bearing wear before costly downtime. Hospitals rely on edge inference to trigger nurse alerts when patient vitals deviate, meeting privacy rules that restrict continuous cloud upload . Emerging accelerators like Groq's LPU push token generation to 300 tokens per second, letting conversational assistants run inside teller kiosks. By sidestepping back-haul latency and bandwidth charges, firms unlock real-time use cases in ships, mines, and rural cell towers where connectivity remains inconsistent. The technology thus widens geographic reach for the streaming analytics market while reinforcing compliance with data-sovereignty codes.

Rising Kafka Skill-Set Shortage and Wage Inflation

Eighty-plus percent of Fortune 100 enterprises rely on Kafka, yet job boards list far more openings than qualified engineers. United States salaries top USD 100,000, squeezing budgets for mid-tier firms. The steep learning curve around brokers, replication factors, and exactly-once semantics deters newcomers, while retaining talent proves challenging as cloud vendors poach senior staff. Managed platforms help but trade flexibility for subscription outlays. Consulting partners expand training bootcamps, though ramp-up times still lag project deadlines. Until educational pipelines catch up, talent scarcity will curb some rollouts, particularly in regulated sectors where outsourcing is constrained.

Other drivers and restraints analyzed in the detailed report include:

- Low-Code/No-Code Streaming Workbenches for Citizen Developers

- Mainstream Adoption of Event-Driven Micro-Services

- Escalating Egress Fees on Hyperscaler Clouds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions provided the structural backbone of the streaming analytics market in 2024 with 65.4% revenue, reflecting wide adoption of brokers, processors, and interactive query engines. Yet services are accelerating at 33.8% CAGR through 2030 as enterprises seek design blueprints, migration aid, and 24/7 SRE support. Architecture assessments, data-quality remediation, and schema governance dominate new statements of work. Confluent and EY formed a strategic alliance in 2025 to bundle implementation accelerators, underscoring demand for outside expertise. As observability and cost-optimization mandates rise, managed services extend from simple hosting to auto-tuning capacity based on event velocity.

Skills shortages push even risk-averse sectors to outsource runtime operations, shifting budgets from capital expenditure to recurring services. Vendor roadmaps show pre-packaged compliance modules for PCI-DSS and HIPAA emerging inside subscription tiers, which lowers the barrier for regulated adopters. Consequently, the streaming analytics market size for professional and managed services is projected to outpace core software revenues, reinforcing a virtuous cycle where know-how, not tool count, differentiates providers.

Cloud claimed 59.5% of 2024 revenue, and its 34.2% CAGR signals continued preference for elastic capacity. Hyperscalers pair auto-scaling stream engines with lakehouses and vector databases, letting teams ingest, enrich, and serve ML features without hardware procurement. Google Cloud stitches Pub/Sub, Dataflow, BigQuery, and Vertex AI into a managed continuum, easing burden for firms lacking distributed-systems talent. The streaming analytics market size for on-premise workloads remains meaningful in defense, fintech, and public health, but growth trails cloud due to refresh cycles and capex hurdles.

Hybrid blueprints mitigate egress costs by processing sensitive telemetry in factories with Azure SQL Edge before forwarding aggregates to cloud ML endpoints. Providers now enable policy-based topic placement so that individual partitions stay inside national borders, satisfying emerging sovereignty rules. Over the forecast, multicloud federation tools that span IAM, lineage, and governance will influence vendor selection as buyers seek exit-cost protection.

Streaming Analytics Market Report is Segmented by Component (Software, Services), Deployment (On-Premise, Cloud-Based), End-User Industry (Media and Entertainment, Retail and ECommerce, Manufacturing, BFSI, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), and by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

North America captured 29.7% revenue in 2024 owing to early hyperscaler ecosystems and a mature cadre of Kafka specialists. Financial services, ride-hailing, and retail pioneers validated ROI, creating reference designs that spread across sectors. Yet saturation tempers incremental growth, and skilled-labor bottlenecks spark wage premiums that influence deployment budgets. Government push for real-time public-sector dashboards-covering weather, wildfire, and mobility-adds steady demand, albeit at rigorous compliance levels.

Asia-Pacific posts the swiftest 34.1% CAGR as 5G rollouts, smart-factory programs, and sovereign cloud initiatives converge. China's AI revenue projections near USD 300 billion by 2030, with edge streaming deemed vital to autonomous manufacturing cells. India's public-digital-infrastructure drive embeds event streams into tax, identity, and payments rails, while Southeast Asian e-commerce platforms rely on real-time personalization to compete for mobile users. Local chipmakers and telcos co-innovate, reducing hardware costs and boosting regional vendor ecosystems, which keeps adoption momentum high.

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Amazon Web Services

- Google (Alphabet)

- Confluent Inc.

- TIBCO Software Inc.

- Software AG

- SAS Institute Inc.

- Striim Inc.

- Impetus Technologies

- Databricks

- Snowflake Inc.

- Apache Software Foundation (Kafka/Flink)

- Cloudera Inc.

- Ververica

- Aiven Ltd.

- Timeplus

- Hazelcast Inc.

- StreamSets Inc.

- Redpanda Data

- Cisco Systems (ThousandEyes)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative-AI infused data pipelines

- 4.2.2 Edge AI chips enabling on-device stream processing

- 4.2.3 Low-code/no-code streaming workbenches for citizen developers

- 4.2.4 Mainstream adoption of event-driven micro-services

- 4.2.5 Growing SME demand for cloud stream analytics (consensus driver)

- 4.2.6 Expansion of IoT and industrial automation (consensus driver)

- 4.3 Market Restraints

- 4.3.1 Rising Kafka skill-set shortage and wage inflation

- 4.3.2 Escalating egress fees on hyperscaler clouds

- 4.3.3 Data-sovereignty regulations limiting cross-border stream flows

- 4.3.4 Legacy batch-centric architectures delaying migration (consensus)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.3 By End-user Industry

- 5.3.1 Media and Entertainment

- 5.3.2 Retail and eCommerce

- 5.3.3 Manufacturing

- 5.3.4 BFSI

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Transportation and Logistics

- 5.3.7 Telecommunications

- 5.3.8 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 Amazon Web Services

- 6.4.6 Google (Alphabet)

- 6.4.7 Confluent Inc.

- 6.4.8 TIBCO Software Inc.

- 6.4.9 Software AG

- 6.4.10 SAS Institute Inc.

- 6.4.11 Striim Inc.

- 6.4.12 Impetus Technologies

- 6.4.13 Databricks

- 6.4.14 Snowflake Inc.

- 6.4.15 Apache Software Foundation (Kafka/Flink)

- 6.4.16 Cloudera Inc.

- 6.4.17 Ververica

- 6.4.18 Aiven Ltd.

- 6.4.19 Timeplus

- 6.4.20 Hazelcast Inc.

- 6.4.21 StreamSets Inc.

- 6.4.22 Redpanda Data

- 6.4.23 Cisco Systems (ThousandEyes)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment