|

시장보고서

상품코드

1846191

동물용 초음파 장치 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Veterinary Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

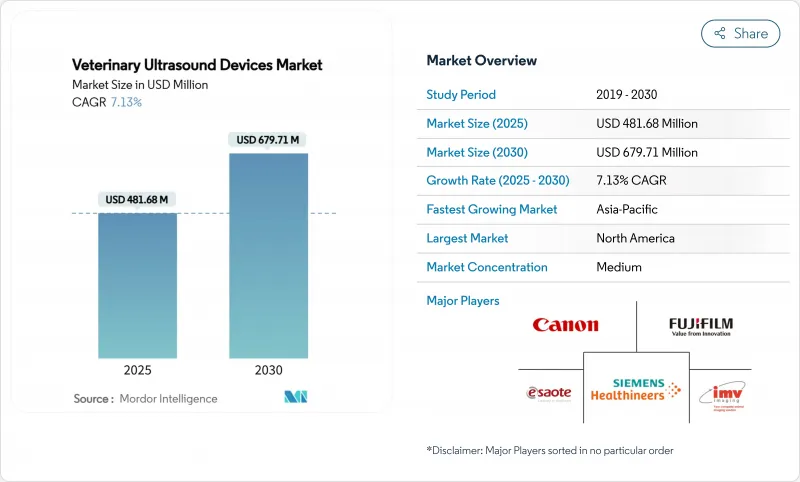

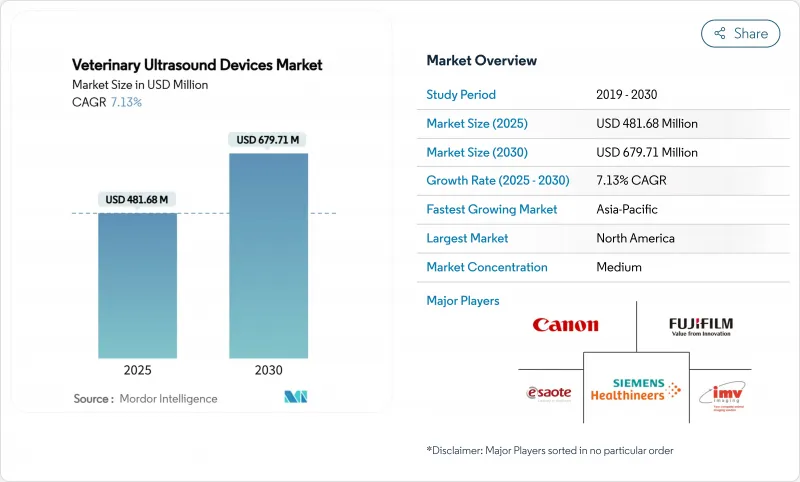

동물용 초음파 장치 시장 규모는 2025년에 4억 8,168만 달러로 추계되며, 예측 기간(2025-2030년)의 CAGR은 7.13%로, 2030년에는 6억 7,971만 달러에 달할 것으로 예상됩니다.

반려동물 사육 증가, 반려동물의 인간화, 가축과 동반자 종에서의 생식 및 심장 영상 진단에 대한 수요가 증가함에 따라 공급업체에게 대응할 수있는 기초가 확대되고 있습니다. 핸드헬드 무선 스캐너, 3D/4D 모달리티, AI 대응 독영이 경쟁적인 포지셔닝을 재구성하고 있으며, 클라우드 기반 아카이빙이 지방의 용량 제약을 완화하고 있습니다. 제조업체 각사는 초음파 훈련을 받은 수의사의 부족을 보완하고 동물종을 넘어 일관된 진단을 제공하기 위해 워크플로우의 자동화를 목표로 하고 있습니다. 자금 부담이 가벼운 가입 모델과 원격 의료 통합은 이전에는 이미징 기능이 없었던 클리닉에 새로운 수입원을 제공합니다. 그러나 소규모 클리닉에서는 장비 초기 비용과 대형 동물 스캔에 대한 상환의 일관성이 없으며 신흥 경제 국가의 단기 보급이 늘어났습니다.

세계의 동물용 초음파 장치 시장 동향과 인사이트

반려동물 웰빙 스크리닝 프로그램의 급증으로 초음파 장치 조달 가속화

예방 의료 패키지는 현재 복부 및 심장 스캔을 정기적인 구성 요소로 통합하고 있으며, 이는 인간 수준의 진단을 원하는 주인의 요구를 반영합니다. 자동화된 알고리즘은 임상의가 치료 시점에서 놓칠 수 있는 저에코 간 병변 및 판막증 이상을 검출하여 조기 치료 프로토콜의 신뢰성을 향상시킵니다. 2024년 8월에 실시된 연구에서는 AI에 의한 개 스크리닝으로 겉보기 건강한 개의 86%에 잠재적인 문제가 발견되었습니다. 3명 이상의 수의사가 있는 병원에서는 시니어 반려동물 초음파 검사 프로토콜이 67% 채용되고 있다고 보고되고 있으며, 소셜 채널을 통해 인지가 넓어짐에 따라 아시아태평양의 도시 클리닉에서의 채용률이 상승하고 있습니다. 구독 기반 영상 진단 번들은 소규모 클리닉이 표준화된 연례 검진을 제공하면서 장비 비용을 회수하는 데 도움이 됩니다. 이 촉진요인은 반복 수입을 보장하는 회원제 웰니스 플랜에 영상 진단을 통합함으로써 동물용 초음파 장치 시장에 기세를 주고 있습니다.

휴대용 무선 스캐너가 모바일 형 혼합 동물 수의사에게 빠르게 확산

스마트폰에 연결된 경량 프로브를 통해 수의사는 축사, 안정, 야생 동물 재활센터 등에서 이미지를 얻을 수 있습니다. 2024년에 실시한 비교 테스트에서 Vscan Air는 미드레인지 카트 시스템에 필적하는 복부의 선명도를 얻어 최고의 사용성 점수를 얻은 것으로 확인되었습니다. 현지 임상의는 클라우드 PACS를 통해 추천 전문가에게 스캔을 보낼 수 있으며, 긴급 숙마와 소 난산 사례의 판단 시간을 단축할 수 있습니다. 장비 제조업체의 무선 스캐너 가격은 2,800달러에서 4,500달러로 예산이 제한된 한 명의 수의사의 액세스를 늘리고 있습니다. 이 급속한 보급은 청진 전용 진단에서 데이터가 풍부한 영상 진단으로 대체하여 더 높은 서비스 비용을 정당화하고 동물 초음파 장치 시장을 활성화합니다.

지방에서는 초음파 훈련을받은 수의사가 제한되어 있습니다.

넓은 지역에서 진료를 하는 수의사는 종종 동물 종을 가로질러 회전할 수 있으며, 고급 이미지 훈련에 시간을 할애할 수 없습니다. 2024년 7월에 실시된 노동력 조사에서는 지방의 임상의가 한정된 진단 자원을 위해서 안락사나 소개를 추천한 사례가 강조되어, 액세스 갭이 부조가 되었습니다. 원격지도 프로그램과 AI 오버레이는 지식 부족을 완화하지만 여전히 기본적인 프로브 기술에 의존합니다. 지속적인 능력 부족은 동물용 초음파 장치 시장에 무거워지며, 환자 수가 많으면 투자가 정당화되어야 하는 하드웨어의 도입을 늦추고 있습니다.

부문 분석

2024년 동물용 초음파 장치 시장 점유율은 소개 병원에서의 이용이 정착되어 있기 때문에 카트/트롤리 시스템이 49.13%로 최대 점유율을 유지했습니다. 그러나 핸드헬드 스캐너는 팜 콜 효율성과 유지 보수 오버헤드를 줄임으로써 CAGR 9.21%에서 전체 성장을 능가할 것으로 예측됩니다. 핸드헬드로 인한 동물용 초음파 장치 시장 규모는 구독 가격 프로브가 진입 장벽을 낮추기 때문에 2030년까지 두배로 될 것으로 예측됩니다.

Wi-Fi 또는 Bluetooth로 작동하는 무선 프로브는 DICOM 호환 이미지를 태블릿으로 스트리밍하여 PACS에 즉시 업로드할 수 있습니다. 클리닉은 모바일 영상 진단을 통해 현장에서 진단을 받고 환자의 운반 스트레스를 최소화하므로 고객의 컴플라이언스가 향상된다고 보고합니다. 연결성이 향상됨에 따라 핸드헬드의 채택은 기존 브랜드와 과제 브랜드 모두에게 동물용 초음파 장치 시장의 확대 전략이 필요합니다.

2차원 초음파는 범용성과 유리한 가격 성능으로 2024년에는 57.46%의 점유율을 차지했습니다. 심혈관 평가에 중요한 도플러 모달리티는 CAGR 9.65%로, 2030년까지 동물용 초음파 장치 시장 전체에 대한 기여를 확대할 예정입니다. AI 오버레이는 현재 유속을 정량화하고 역류 제트를 자동으로 분류하여 심장병의 워크플로우를 간소화합니다.

과거에는 학술 센터에 한정되어 있던 3D/4D 이미징이 말의 근골격계의 평가나 단두종의 개의 두개골 매핑에 새로운 견인력을 발견하고 있습니다. 초해상도 조사는 미세혈관 묘사를 10배 향상시키고 종양의 병기 분류 정확도를 향상시켰습니다. 동물용 초음파 장치 시장은 클리닉이 펌웨어를 업그레이드함으로써 기본 하드웨어를 교체하지 않고 이러한 기능을 이용할 수 있게 되어 라이프사이클 가치가 높아진다는 장점이 있습니다.

지역 분석

북미는 정교한 수의학 인프라와 급속한 AI 도입으로 2024년 매출의 38.51%를 차지하고 선도했습니다. 미국은 반려동물 보험의 보급과 광범위한 전문가 소개 네트워크에 의해 지원,이 지역의 동물 초음파 장치 시장에서 주요 수익 엔진입니다. 캐나다는 원격 진료의 확대가 성장의 원동력이며, 멕시코는 혼합 진료의 확대에 따라 핸드헬드의 매출이 증가하고 있습니다.

아시아태평양은 도시화에 의해 반려동물의 소유율이 상승하고 가축의 집약화에 의해 번식 모니터링이 가속되기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 10.32%를 나타낼 것으로 예측됩니다. 중국에서는 대규모 낙농 사업에 대한 투자가 인도에서는 동물 위생 서비스 개선을 정부가 뒷받침하고 있으며 스캐너 수요를 높이고 있습니다. 일본과 한국은 1인당 반려동물 지출액이 높고, 호주는 가축과 동반 동물의 이중 수익원으로부터 이익을 얻고 있습니다. 국경을 넘어선 전자상거래 플랫폼은 중급 기종 조달을 간소화하고 이 지역의 동물용 초음파 장치 시장 규모를 확대하고 있습니다.

유럽은 성숙한 기반을 유지하고 있지만 여전히 확대되고 있습니다. 독일, 영국, 프랑스는 수요의 중심이며 남유럽에서의 꾸준한 보급과 동유럽 시장에서의 새로운 관심도 수반하고 있습니다. 그러나 EU의 동물 복지에 관한 법령이 조화를 이루고 있기 때문에 장비의 갱신 주기는 유지됩니다. 브라질의 중요한 목축 산업이 견인하는 남미와 GCC에 의한 고급 클리닉에 대한 투자가 증가하는 중동 및 아프리카가 세계적인 공헌의 끝을 장식합니다. 이 나라들은 인프라 과제에도 불구하고 세계의 동물 초음파 장치 시장에 새로운 볼륨을 추가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 반려동물 웰니스 스크리닝 프로그램의 급증에 의한 초음파 기기 조달 촉진

- 핸드헬드·무선·스캐너의 이동식 혼합 동물 수의사에게의 급속한 보급

- 동물 사육률과 동물 의료비 증가

- 동물의 건강 상태의 진단에 대한 수요 증가와 기술의 진보

- 가축 사육과 번식 모니터링 요구의 확대

- 수의사 영상 진단에 있어서의 AI와 원격 의료의 통합

- 시장 성장 억제요인

- 지방에서의 초음파 훈련을 받은 수의사의 부족

- 소규모 진료소에서의 프리미엄 도플러 및 4D 플랫폼의 초기 투자 부담

- 신흥 경제국에서의 대형 동물 화상 진단에 대한 일관성이 없는 진료 보상

- 고급 초음파 장치의 고비용

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액 기준)

- 휴대성별

- 휴대용 초음파

- 탁상형 초음파

- 카트/트롤리형 초음파

- 기술별

- 2차원 초음파

- 도플러 초음파

- 3D/4D 초음파

- 조영제 강화 초음파

- 용도별

- 산부인과

- 심장학

- 근골격계

- 복부 및 내과

- 응급 및 중환자 치료

- 동물유형별

- 반려동물

- 개

- 고양이

- 기타 작은 동물

- 축산동물

- 말

- 소

- 기타 가축

- 기타 동물

- 반려동물

- 최종 사용자별

- 동물병원

- 동물진료소

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Esaote SpA

- Shenzhen Mindray Bio-Medical Electronics Co. Ltd

- Canon Inc.

- FUJIFILM Sonosite Inc.

- Samsung Medison Co. Ltd

- DRAMINSKI SA

- IMV Imaging

- Siemens Healthineers GmbH

- Sonostar Technologies Co. Ltd

- SonoScape Medical Corp.

- Chison Medical Technologies Co. Ltd

- Clarius Mobile Health Corp.

- EI Medical Imaging

- Butterfly Network Inc.

- Edan Instruments Inc.

- Kaixin Electronic Instrument Co. Ltd

- Healcerion Co. Ltd

- Telemed Medical Systems

- Xuzhou Palmary Electronics Co. Ltd

- Heska Corporation

제7장 시장 기회와 전망

KTH 25.10.31The Veterinary Ultrasound Devices Market size is estimated at USD 481.68 million in 2025, and is expected to reach USD 679.71 million by 2030, at a CAGR of 7.13% during the forecast period (2025-2030).

Growing pet ownership, the humanization of companion animals, and rising demand for reproductive and cardiology imaging in livestock and companion species are broadening the addressable base for vendors. Handheld wireless scanners, 3D/4D modalities, and AI-enabled interpretation are reshaping competitive positioning, while cloud-based archiving relieves capacity constraints in rural settings. Manufacturers are targeting workflow automation to offset the shortage of ultrasound-trained veterinarians and to deliver consistent diagnoses across species. Capital-light subscription models and telemedicine integrations are opening new revenue streams for practices that previously lacked imaging capabilities. However, small clinics still face up-front equipment costs and inconsistent reimbursement for large-animal scans, which curb near-term penetration in developing economies.

Global Veterinary Ultrasound Devices Market Trends and Insights

Surge in Companion-Animal Wellness Screening Programs Accelerating Ultrasound-Device Procurement

Preventive care packages now embed abdominal and cardiac scans as routine components, reflecting owners' desire for human-grade diagnostics. Automated algorithms flag hypoechoic liver lesions or valvular anomalies that clinicians might miss at the point of care, boosting confidence in early treatment protocols. Studies in August 2024 showed AI-assisted canine screenings identifying subclinical issues in 86% of apparently healthy dogs. Hospitals with more than three veterinarians report 67% adoption of senior-pet ultrasound protocols, and uptake is rising in urban Asia-Pacific clinics as awareness spreads through social channels. Subscription-based imaging bundles help smaller practices recover equipment costs while offering standardized annual check-ups. The driver adds momentum to the veterinary ultrasound devices market by embedding imaging into membership wellness plans that lock in repeat revenue.

Rapid Diffusion of Handheld Wireless Scanners Among Mobile Mixed-Animal Veterinarians

Lightweight probes tethered to smartphones let practitioners acquire images in barns, equine stables, and wildlife rehabilitation centers. Comparative testing in 2024 confirmed that the Vscan Air yielded abdominal-view clarity on par with mid-range cart systems, winning highest ease-of-use scores. Rural clinicians can transmit scans to referral specialists via cloud PACS, shortening decision time for emergency foaling or bovine dystocia cases. Device makers price wireless scanners between USD 2,800 and USD 4,500, widening access for solo veterinarians with tight budgets. The rapid uptake elevates the veterinary ultrasound devices market by replacing auscultation-only visits with data-rich imaging consults that justify higher service fees.

Limited Ultrasound-Trained Veterinarians in Rural Regions

Practitioners servicing wide geographic areas often rotate across species and cannot devote time to advanced imaging training. A July 2024 workforce study highlighted cases where rural clinicians recommended euthanasia or referrals due to limited diagnostic resources, underscoring the access gap. Tele-mentoring programs and AI overlays alleviate knowledge deficits but still rely on baseline probe skills. The enduring competence shortfall weighs on the veterinary ultrasound devices market by slowing hardware uptake where patient densities would otherwise justify investment.

Other drivers and restraints analyzed in the detailed report include:

- Increase in Animal Adoption and Health Expenditure

- Rise in Demand for Diagnosis of Animal Health Conditions and Technological Advancements

- Up-front Capital Burden of Premium Doppler & 4D Platforms for Small Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cart/trolley systems retained the largest slice of the veterinary ultrasound devices market share at 49.13% in 2024, reflecting entrenched use in referral hospitals. Yet handheld scanners are forecast to outpace overall growth at 9.21% CAGR, propelled by farm-call efficiency and reduced maintenance overhead. The veterinary ultrasound devices market size attributable to handhelds is expected to double by 2030 as subscription-priced probes lower entry barriers.

Advances in battery life, probe cooling, and AI-driven presets now deliver cart-like performance in devices weighing under 300 g. Wireless probes operating on Wi-Fi or Bluetooth stream DICOM-compatible images to tablets, enabling instant uploads to PACS. Practices report that mobile imaging increases client compliance because diagnoses occur on-site, minimizing patient transport stress. As connectivity improves, handheld adoption forms a cornerstone of the veterinary ultrasound devices market expansion strategy for both incumbent and challenger brands.

Two-dimensional ultrasound dominated revenue with a 57.46% stake in 2024 owing to versatility and favorable price-performance. Doppler modalities, crucial for cardiovascular assessments, are slated for a 9.65% CAGR, widening their contribution to the overall veterinary ultrasound devices market size by 2030. AI overlays now quantify flow velocities and auto-classify regurgitant jets, streamlining cardiology workflows.

3D/4D imaging, once limited to academic centers, finds new traction in equine musculoskeletal evaluations and canine skull mapping for brachycephalic breeds. Super-resolution research demonstrates ten-fold gain in microvascular depiction, elevating oncologic staging accuracy. The veterinary ultrasound devices market benefits as clinics upgrade firmware to unlock such features without swapping base hardware, extending lifecycle value.

The Veterinary Ultrasound Devices Market is Segmented by Product (Handheld Ultrasound, and More), Technology (2-Dimensional Ultrasound, and More), Application (Obstetrics & Gynecology, and More), Animal Type (Companion Animals, and More), End User (Veterinary Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 38.51% of 2024 revenue owing to sophisticated veterinary infrastructure and rapid AI adoption. The United States remains the primary revenue engine within the regional veterinary ultrasound devices market, supported by pet-insurance penetration and widespread specialty referral networks. Canada's growth is driven by telemedicine extensions into remote provinces, while Mexico experiences upticks in handheld sales linked to expanding mixed-animal practices.

Asia-Pacific is forecast to record the fastest 10.32% CAGR through 2030 as urbanization lifts companion-animal ownership and livestock intensification accelerates reproductive monitoring. China's investment in large-scale dairy operations and India's government push for improved animal health services bolster scanner demand. Japan and South Korea exhibit high per-capita pet spending, whereas Australia benefits from dual livestock and companion-animal revenue streams. Cross-border e-commerce platforms simplify procurement of mid-tier devices, enlarging the regional veterinary ultrasound devices market size.

Europe maintains a mature yet still expanding base. Germany, the United Kingdom, and France anchor demand, accompanied by steady adoption in Southern Europe and emerging interest in Eastern markets. Variability in veterinary service pricing across the continent affects scan uptake, yet harmonized EU animal-welfare statutes sustain equipment renewal cycles. South America, led by Brazil's significant cattle industry, and the Middle East & Africa, where GCC investments in premium clinics rise, round out global contribution. Together they add incremental volumes to the worldwide veterinary ultrasound devices market despite infrastructural challenges.

- Esaote

- Mindray

- Canon

- FUJIFILM Sonosite Inc.

- Samsung Group

- DRAMINSKI SA

- IMV Imaging

- Siemens Healthineers

- Sonostar Technologies Co. Ltd

- SonoScape Medical Corp.

- Chison Medical Technologies Co. Ltd

- Clarius Mobile Health Corp.

- E.I. Medical Imaging

- Butterfly Network Inc.

- Edan Instruments Inc.

- Kaixin Electronic Instrument Co. Ltd

- Healcerion Co. Ltd

- Telemed Medical Systems

- Xuzhou Palmary Electronics Co. Ltd

- Heska

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Companion-Animal Wellness Screening Programs Accelerating Ultrasound-Device Procurement

- 4.2.2 Rapid Diffusion of Handheld Wireless Scanners Among Mobile Mixed-Animal Veterinarians

- 4.2.3 Increase in Animal Adoption and Animal Health Expenditure

- 4.2.4 Rise in Demand for Diagnosis of Animal Health Conditions and Technological Advancements

- 4.2.5 Expansion of Livestock Farming & Reproductive Monitoring Needs

- 4.2.6 Integration of AI & Telemedicine in Veterinary Imaging

- 4.3 Market Restraints

- 4.3.1 Limited Ultrasound-Trained Veterinarians in Rural Regions

- 4.3.2 Up-front Capital Burden of Premium Doppler & 4D Platforms for Small Practices

- 4.3.3 Inconsistent Reimbursement for Large-Animal Diagnostic Imaging in Emerging Economies

- 4.3.4 High Cost of Advanced Ultrasound Equipment

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Portability

- 5.1.1 Handheld Ultrasound

- 5.1.2 Table-top Ultrasound

- 5.1.3 Cart/Trolley-based Ultrasound

- 5.2 By Technology

- 5.2.1 2-Dimensional Ultrasound

- 5.2.2 Doppler Ultrasound

- 5.2.3 3D/4D Ultrasound

- 5.2.4 Contrast-Enhanced Ultrasound

- 5.3 By Application

- 5.3.1 Obstetrics & Gynecology

- 5.3.2 Cardiology

- 5.3.3 Musculoskeletal

- 5.3.4 Abdominal & Internal Medicine

- 5.3.5 Emergency & Critical Care

- 5.4 By Animal Type

- 5.4.1 Companion Animals

- 5.4.1.1 Dogs

- 5.4.1.2 Cats

- 5.4.1.3 Other Small Companion Animals

- 5.4.2 Livestock Animals

- 5.4.2.1 Horse

- 5.4.2.2 Cattle

- 5.4.2.3 Other Livestock Animals

- 5.4.3 Other Animals

- 5.4.1 Companion Animals

- 5.5 By End User

- 5.5.1 Veterinary Hospitals

- 5.5.2 Veterinary Clinics

- 5.5.3 Other End Users

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Esaote SpA

- 6.3.2 Shenzhen Mindray Bio-Medical Electronics Co. Ltd

- 6.3.3 Canon Inc.

- 6.3.4 FUJIFILM Sonosite Inc.

- 6.3.5 Samsung Medison Co. Ltd

- 6.3.6 DRAMINSKI SA

- 6.3.7 IMV Imaging

- 6.3.8 Siemens Healthineers GmbH

- 6.3.9 Sonostar Technologies Co. Ltd

- 6.3.10 SonoScape Medical Corp.

- 6.3.11 Chison Medical Technologies Co. Ltd

- 6.3.12 Clarius Mobile Health Corp.

- 6.3.13 E.I. Medical Imaging

- 6.3.14 Butterfly Network Inc.

- 6.3.15 Edan Instruments Inc.

- 6.3.16 Kaixin Electronic Instrument Co. Ltd

- 6.3.17 Healcerion Co. Ltd

- 6.3.18 Telemed Medical Systems

- 6.3.19 Xuzhou Palmary Electronics Co. Ltd

- 6.3.20 Heska Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment