|

시장보고서

상품코드

1846192

마이크로캐리어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Microcarrier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

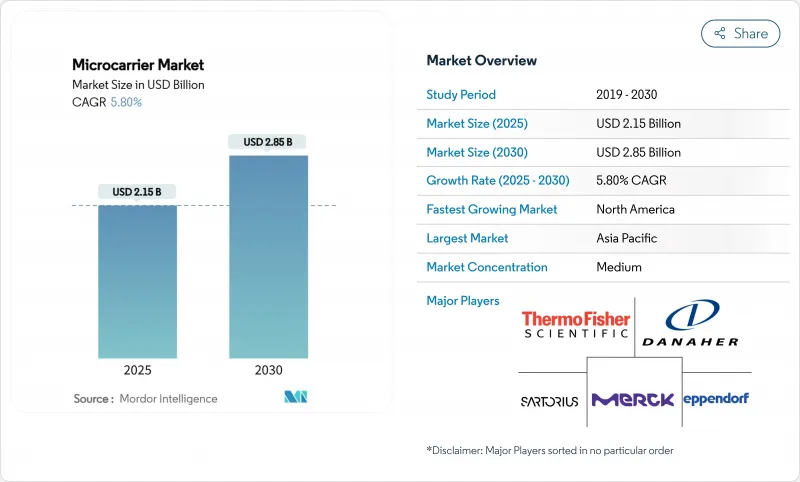

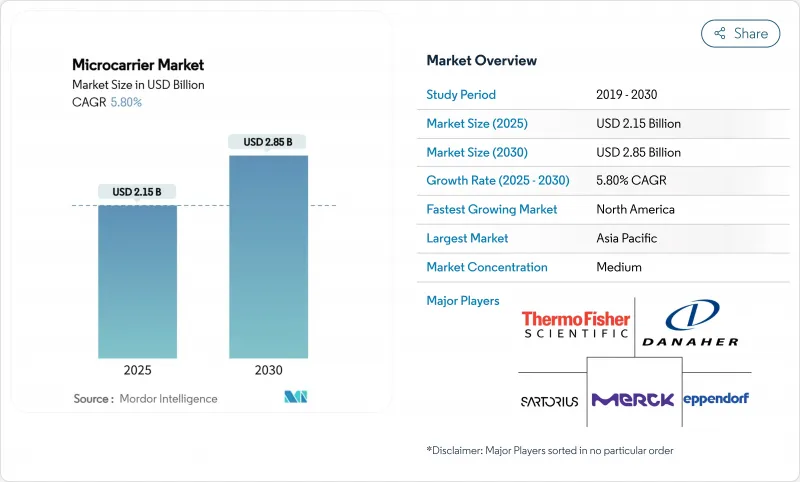

마이크로캐리어 시장 규모는 2025년에 21억 5,000만 달러, 2030년에는 28억 5,000만 달러에 이르고, CAGR 5.80%를 나타낼 것으로 예측됩니다.

세포 기반 백신, 광범위한 생물학적 제형 파이프라인, 더 높은 세포 밀도, 더 작은 시설 면적, 더 적은 유틸리티 소비를 가능하게 하는 연속 제조 플랫폼으로의 전환이 수요를 뒷받침하고 있습니다. 배양식육의 연구개발에 대한 투자 증가는 식용으로 생분해성 기질에 대한 관심을 가속화하고 있는 반면, 싱글유스 바이오리액터와 통합 프로세스 분석 기술은 배치간의 일관성을 향상시키고 전환 시간을 단축하고 있습니다. 자동화, 자기 분리 및 열 응답성 재료는 필요한 노동력을 최대 40%까지 줄이고 상업 운영에서 비용 억제 전략을 지원합니다. 생물 제제의 가격 압력과 규모 업의 복잡성과 같은 역풍에도 불구하고 마이크로캐리어 시장은 안정적인 성장 궤도를 유지하고 있습니다.

세계의 마이크로캐리어 시장 동향과 인사이트

세포 기반 백신 및 치료제에 대한 수요

가속화하는 mRNA 및 바이러스 벡터 프로그램에는 현탁 배양의 일반적인 500만-800만 세포/mL를 훨씬 웃도는 2,000만 세포/mL 이상의 접착 세포 배양 시스템이 필요합니다. 규제의 합리화로 일부 치료법은 개발 기간을 7-10년으로 단축하여 확장 가능한 마이크로캐리어 플랫폼의 지속적인 주문을 자극하고 있습니다. 팬데믹 시대의 국내 백신 생산 능력에 대한 투자는 반응기의 설치 면적을 70%나 줄여 중소기업의 자본 제약을 완화하는 최적화 마이크로캐리어의 역할을 확고히 했습니다. 개인화된 의료 파이프라인은 유연한 소량 생산 바이오리액터를 요구하며 마이크로캐리어 채택을 더욱 강화하고 있습니다. 이러한 요인을 종합하면 마이크로캐리어 시장 예측 CAGR은 1.2포인트 상승합니다.

생물제제 및 바이오시밀러 제조 확대

생물제제 매출은 2025년 3,000억 달러를 돌파했고, 중국과 인도 정부는 지난 2년간 150억 달러 이상을 바이오 의약품의 그린필드 생산 능력에 투입했습니다. 연속 관류 시스템은 10배 부피 생산성과 50% 배지 절약을 달성하지만, 높은 세포 밀도 조작은 지속적인 전단을 견디는 견고한 마이크로캐리어에 의존합니다. 바이오시밀러 개발자는 오리지네이터의 배양 조건을 충실히 재현하는 담체 화학을 요구하고, 표면 수식 정밀도의 장애물을 올리고 있습니다. BIOSECURE법은 서양의 아웃소싱을 인도의 CDMO로 향하게 하고, 2024년에는 인계량이 40% 이상 급증해, 마이크로캐리어 시장의 세계적인 발자취를 확대했습니다.

생물 제제 및 세포 치료의 높은 비용

세포 치료제에서는 최종 사용자 가격의 40-60%가 제조 비용으로 차지하고 있으며, 저분자 의약품의 일반적인 10-15%를 훨씬 웃돌고 있습니다. 따라서 신흥 시장 지급자는 상환을 제한하고, 시설의 건설을 억제하고, 마이크로캐리어의 신규 도입 수요를 억제하고 있습니다. 스케일업은 규모의 경제를 약속하는 한편, 중소기업이 흡수하는 데 어려움을 겪는 검증 비용을 도입해 상업화 일정을 늦춥니다. 광범위한 경력 특성화는 규제 당국 신청에 200만 달러에서 500만 달러를 추가할 수 있어 신규 재료의 진입을 막아 마이크로캐리어 시장의 성장을 억제합니다.

부문 분석

폴리스티렌 캐리어는 바이러스 백신과 단일클론항체 라인의 오랜 주력 제품으로 2024년 마이크로캐리어 시장 규모의 43.31%의 점유율을 유지했습니다. 그 표면 화학적 성질은 잘 이해되고 있으며, 로트간의 일관성도 높고, 규제 파일도 성숙하고 있기 때문에 적격성 평가의 허들도 낮습니다. 그러나 바이오파마의 환경문제에 대한 관심 증가와 배양육생산자의 대두로 연구개발예산은 생분해성 알긴산, 키토산, 셀룰로오스의 변종에 돌이켜지고 있습니다. 알긴산은 식용에 적합하고, 배양육의 근섬유의 발판으로 진중되는 Ca2 구배하에서 겔화하는 능력을 가지기 때문에 CAGR이 6.64%로 소재 클래스 중 가장 빠른 것을 기록하고 있습니다.

하이브리드 제형은 현재 경질 합성 코어와 생물활성 외층을 융합시켜 고전단 관류시의 기계적 탄력성을 실현하는 동시에 섬세한 줄기세포에 천연 리간드를 제공합니다. 콜라겐 단편으로 코팅된 자성 폴리스티렌 코어는 자동 분리와 부드러운 박리를 가능하게 하고 상업 플랜트에서 수확 시간을 30-40% 단축합니다. 열 반응성 폴리-N-이소프로파일-아크릴아미드 껍질은 5℃의 온도 강하에서 세포를 방출하여 효소의 모욕을 받지 않고 세포 치료의 효능에 필수적인 막 결합 단백질을 보유합니다. 화학적으로 정의된 동물성분이 없는 공정에 대한 규제의 뒷받침은 합성 식물 하이브리드 수요를 더욱 자극하고 마이크로캐리어 시장의 성장세를 유지하고 있습니다.

인플루엔자, 소아마비 및 최근에는 mRNA 기반 플랫폼이 항원 및 바이러스 증식을 위해 부착 균주에 의존하기 때문에 백신 제조는 2024년 마이크로캐리어 시장 규모의 38.99%를 흡수했습니다. 수십 년에 걸친 공정 최적화는 과제 진입 장벽을 높게 유지하고 안정적인 수요를 보장합니다. 그러나 CAR-T, 간엽계 간질세포, 인공다능성 줄기세포, NK세포 등의 세포 치료 파이프라인은 CAGR 6.45%로 다른 모든 이용 사례를 능가하고 있습니다. 동종 면역요법의 "기성품"에 대한 규제 당국의 승인을 위해서는 로트당 수십억 개의 세포를 은행하고 로트 릴리스 타임라인을 2주 미만으로 할 수 있는 반응기가 필요하며, 이 벤치마크는 강화된 마이크로캐리어 배양에서만 달성 가능합니다.

센서가 풍부한 수확 스키드를 통합한 자동화 스위트는 현재 인라인 세척, 농축, 충전 마무리 작업을 지원하여 CAR-T 후보의 정맥에서 정맥까지의 시간을 20일에서 12일 이하로 단축하고 있습니다. 하류에서는 식감이나 맛을 바꾸지 않고 분해되거나 소비가능해야 하는 배양육 캐리어에 있어서 식용성이 중요한 설계 파라미터가 되고 있습니다. 조직 공학과 장기 온칩을 포함한 연구 개발 분야에서는 확장 가능한 개념 실증 연구에 마이크로캐리어가 계속 채용되고 있으며, 마이크로캐리어 시장의 응용 범위가 점차 퍼지고 있습니다.

지역 분석

북미는 2024년 매출의 42.78%를 차지하며, 성숙한 GMP 인프라, 왕성한 벤처 자금, 세계적인 밸리데이션의 벤치마크를 설정하는 경우가 많은 규제 당국에의 근접성 등에 지지되었습니다. 숙련 노동자의 부족과 비싼 운영 비용이 기업을 듀얼 쇼어 모델로 향하게 하고 있지만, 이 지역은 고가치의 세포 및 유전자 치료에 있어서 리더십을 유지해, 마이크로캐리어의 혁신 파이프라인이 가장 밀집하고 있는 지역의 하나입니다.

아시아태평양은 CAGR 6.78%로 가장 급성장하고 있는 지역으로 정부 보조금, 인건비 저하, 바이오시밀러 수출 확대에 지지되고 있습니다. 중국은 2024년에 바이오 의약 산업 단지에 80억 달러 이상을 할당하고 시드 트레인에서 수확까지의 마이크로캐리어 프로세스를 표준화하는 전용 일회용 스위트를 특징으로 했습니다. 인도의 CDMO 컴플렉스에서는 미국공급망 법제화를 받아 인바운드 프로젝트 인수가 40% 이상 급증하여 하이데라바드와 방갈로르의 능력 확장을 촉구했습니다. 일본과 한국은 재생의료와 세포치료의 상업화에 주력하고 있으며, 엄격한 약국방 기준을 충족하기 위해 트레이서블한 공급망을 가지는 고급 캐리어를 요구하고 있습니다.

유럽은 생분해성 담체와 폐쇄 루프 물 시스템을 장려하는 순환 경제 지령으로 환경에 초점을 맞춘 꾸준한 성장을 보여줍니다. 산업 정책은 독일, 네덜란드 및 아일랜드의 연속 제조 파일럿 플랜트를 지원하고 에너지 비용이 상승하는 동안 마이크로캐리어 시장의 기세를 유지하고 있습니다. 중동 및 아프리카, 남미의 신흥 지역은 기술 이전 계약과 모듈식 GMP 스위트를 통해 기초 능력을 구축하고 있으며, 마이크로캐리어 시장의 밑단을 점차 넓혀가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세포 기반 백신과 치료제 수요

- 생물제제 및 바이오시밀러 제조의 확대

- 세포 및 유전자 치료의 연구 개발에 대한 세계의 자금 조달 급증

- 일회용 바이오프로세싱 플랫폼으로의 변화

- 식용담체를 필요로 하는 배양육산업의 성장

- 자기·열 응답성 캐리어에 의한 프로세스 강화

- 시장 성장 억제요인

- 생물 제제와 세포 기반 치료제의 높은 비용

- 담체 배양에 있어서 전단 응력과 응집의 문제

- 규제 당국에 인가된 생분해성 마이크로캐리어의 부족

- 특수 폴리머와 코팅 공급망의 불안정성

- 규제 상황

- 기술적 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 재료 유형별

- 폴리스티렌 기반

- 덱스트란 기반

- 알지네이트 기반

- 콜라겐/젤라틴 기반

- 기타

- 용도별

- 백신 제조

- 세포 치료

- 기타

- 최종 사용자별

- 바이오의약품 및 바이오테크놀러지 기업

- CRO 및 CDMO

- 학술 및 연구 기관

- 기타

- 사업 규모별

- 실험실 규모

- 파일럿 규모

- 상업적 규모

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Sartorius AG

- Danaher(Cytiva & Pall)

- Corning Inc.

- Lonza Group Ltd.

- Eppendorf SE

- VWR International LLC

- Becton Dickinson & Co.

- Getinge AB

- Greiner Bio-One GmbH

- Matrix FT

- Gelatex Technologies

- CelVivo ApS

- CELLTREAT Scientific

- HiMedia Laboratories

- Microcarriers Labs(China)

- Esco Aster

- Nanofiber Solutions

- PBS Biotech

제7장 시장 기회와 전망

KTH 25.11.07The microcarrier market size stood at USD 2.15 billion in 2025 and is projected to reach USD 2.85 billion by 2030, advancing at a 5.80% CAGR.

Demand is propelled by cell-based vaccines, the wider biologics pipeline, and the shift toward continuous manufacturing platforms that enable higher cell densities, smaller facility footprints, and lower utility consumption. Growing investment in cultivated-meat R&D is accelerating interest in edible, biodegradable substrates, while single-use bioreactors and integrated process-analytical technologies are improving batch-to-batch consistency and shortening changeover times . Automation, magnetic separation, and thermo-responsive materials are reducing labor requirements by up to 40%, supporting cost-containment strategies in commercial operations. Collectively, these factors keep the microcarrier market on a steady growth trajectory despite headwinds linked to biologics price pressure and scale-up complexities.

Global Microcarrier Market Trends and Insights

Demand for Cell-Based Vaccines & Therapeutics

Accelerated mRNA and viral-vector programs need adherent cell culture systems capable of exceeding 20 million cells/mL, well above the 5-8 million cells/mL typical of suspension cultures. Regulatory streamlining now shortens development timelines to 7-10 years for select modalities, stimulating sustained orders for scalable microcarrier platforms. Pandemic-era investment in domestic vaccine capacity cemented the role of optimized microcarriers that shrink reactor footprints by as much as 70%, easing capital constraints for smaller firms. Personalized-medicine pipelines demand flexible, small-batch bioreactors, further reinforcing microcarrier adoption. Collectively, these factors add 1.2 percentage points to the forecast CAGR of the microcarrier market.

Expansion of Biologics & Biosimilar Manufacturing

Biologics revenue surpassed USD 300 billion in 2025, while governments in China and India injected over USD 15 billion into green-field biopharma capacity over the past two years. Continuous perfusion systems achieve 10-fold volumetric productivity and 50% media savings, but their high cell-density operation depends on rugged microcarriers that tolerate sustained shear. Biosimilar developers seek carrier chemistries that faithfully replicate originator culture conditions, raising the bar for surface-modification precision. The BIOSECURE Act is redirecting Western outsourcing toward India's CDMOs, where inquiry volumes jumped more than 40% in 2024, expanding the global footprint of the microcarrier market.

High Cost of Biologics & Cell-Based Therapies

Manufacturing accounts for 40-60% of end-user prices in cell therapies, far above the 10-15% typical for small-molecule drugs. Emerging-market payers therefore restrict reimbursement, curbing facility builds and muting demand for new microcarrier installations. While scale-up promises economies of scale, it also introduces validation costs that smaller firms struggle to absorb, delaying commercialization timelines. Extensive carrier characterization can add USD 2-5 million to regulatory filings, deterring novel-material entrants and tempering growth in the microcarrier market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Global Funding for Cell & Gene Therapy R&D

- Shift Toward Single-Use Bioprocessing Platforms

- Shear-Stress & Aggregation Issues in Carrier Cultures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polystyrene carriers retained a 43.31% share of the microcarrier market size in 2024 as the long-standing workhorse for viral vaccine and monoclonal-antibody lines. Their surface chemistry is well understood, lot-to-lot consistency is high, and regulatory files are mature, lowering qualification hurdles. However, the growing environmental focus of biopharma and the ascent of cultivated-meat producers are redirecting R&D budgets toward biodegradable alginate, chitosan, and cellulose variants. The alginate cohort is charting a 6.64% CAGR, the fastest across material classes, benefiting from its edible profile and ability to gel under Ca2+ gradients, a prized attribute for muscle-fiber scaffolding in cultured meat.

Hybridformulations now merge rigid synthetic cores with bio-active outer layers, delivering mechanical resilience during high-shear perfusion runs while presenting natural ligands for delicate stem cells. Magnetic polystyrene cores coated in collagen fragments enable auto-separation and gentle detachment, trimming harvest times by 30-40% in commercial plants . Thermo-responsive poly-N-isopropyl-acrylamide shells release cells upon a 5 °C temperature drop without enzymatic insult, preserving membrane-bound proteins vital to cell-therapy potency. The regulatory push toward chemically defined, animal-component-free processes further stimulates demand for synthetic-plant hybrids, upholding growth momentum in the microcarrier market.

Vaccine production absorbed 38.99% of the microcarrier market size in 2024 as influenza, polio, and more recently mRNA-based platforms rely on adherent lines for antigen or virus propagation. Decades of process optimization keep barrier-to-entry high for challengers, ensuring stable demand. Yet cell-therapy pipelines-spanning CAR-T, mesenchymal stromal cells, induced pluripotent stem cells, and NK cells-are driving a 6.45% CAGR, outpacing every other use case. Regulatory approvals for allogeneic "off-the-shelf" immunotherapies demand reactors that can bank billions of cells per lot with lot-release timelines under two weeks, a benchmark achievable only with intensified microcarrier cultures.

Automation suites integrating sensor-rich harvest skids now support inline washing, concentration, and fill-finish activities, slashing vein-to-vein time for CAR-T candidates from 20 days to under 12 days. Downstream, edibility is becoming a critical design parameter for cultured-meat carriers that must degrade or remain consumable without altering texture or taste. R&D segments, including tissue engineering and organ-on-chip, continue to adopt microcarriers for scalable proof-of-concept studies, gradually widening the microcarrier market application base.

The Microcarrier Market Report is Segmented by Material Type (Polystyrene-Based, Dextran-Based, Alginate-Based, and More), Application (Vaccine Manufacturing, Cell Therapy, Others), End User (Biopharma and Biotechnology Firms, and More), Scale of Operation (Laboratory Scale, Pilot Scale, Commercial Scale), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 42.78% of 2024 revenue, supported by mature GMP infrastructure, robust venture funding, and proximity to regulators that often set global validation benchmarks. Skilled-labor shortages and premium operating costs are nudging firms toward dual-shore models, yet the region retains leadership in high-value cell-and-gene therapies and maintains one of the densest clusters of microcarrier innovation pipelines.

Asia-Pacific is the fastest-growing territory at a 6.78% CAGR, underpinned by government subsidies, lower labor overhead, and expanding biosimilar exports. China allocated more than USD 8 billion to biopharma industrial parks in 2024, featuring purpose-built single-use suites that standardize microcarrier processes from seed train to harvest. India's CDMO complex saw inbound project inquiries soar by over 40% following U.S. supply-chain legislation, prompting capacity expansions in Hyderabad and Bangalore. Japan and South Korea focus on regenerative medicine and cell-therapy commercialization, demanding advanced carriers with traceable supply chains to satisfy strict pharmacopoeial standards.

Europe shows steady, environmentally focused growth, with circular-economy directives incentivizing biodegradable carriers and closed-loop water systems. Industrial policy supports continuous manufacturing pilot plants in Germany, the Netherlands, and Ireland, ensuring that the microcarrier market maintains momentum amid rising energy costs. Emerging regions in the Middle East, Africa, and South America are building foundational capability, often through technology-transfer agreements and modular GMP suites, gradually enlarging the microcarrier market footprint.

- Thermo Fisher Scientific

- Merck

- Sartorius

- Danaher (Cytiva & Pall)

- Corning

- Lonza Group Ltd.

- Eppendorf

- VWR International

- Becton Dickinson & Co.

- Getinge

- Greiner Bio-One GmbH

- Matrix F.T.

- Gelatex Technologies

- CelVivo ApS

- CELLTREAT Scientific

- HiMedia Laboratories

- Microcarriers Labs (China)

- Esco Aster

- Nanofiber Solutions

- PBS Biotech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for cell-based vaccines & therapeutics

- 4.2.2 Expansion of biologics & biosimilar manufacturing

- 4.2.3 Surge in global funding for cell & gene therapy R&D

- 4.2.4 Shift toward single-use bioprocessing platforms

- 4.2.5 Growth of cultivated-meat industry demanding edible carriers

- 4.2.6 Process-intensification via magnetic & thermo-responsive carriers

- 4.3 Market Restraints

- 4.3.1 High cost of biologics & cell-based therapies

- 4.3.2 Shear-stress & aggregation issues in carrier cultures

- 4.3.3 Lack of regulatory-cleared biodegradable microcarriers

- 4.3.4 Supply-chain volatility for specialty polymers & coatings

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Polystyrene-based

- 5.1.2 Dextran-based

- 5.1.3 Alginate-based

- 5.1.4 Collagen-/Gelatin-based

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Vaccine Manufacturing

- 5.2.2 Cell Therapy

- 5.2.3 Others

- 5.3 By End User

- 5.3.1 Biopharma and Biotechnology Firms

- 5.3.2 CROs and CDMOs

- 5.3.3 Academic & Research Institutes

- 5.3.4 Others

- 5.4 By Scale of Operation

- 5.4.1 Laboratory Scale

- 5.4.2 Pilot Scale

- 5.4.3 Commercial Scale

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Merck KGaA

- 6.3.3 Sartorius AG

- 6.3.4 Danaher (Cytiva & Pall)

- 6.3.5 Corning Inc.

- 6.3.6 Lonza Group Ltd.

- 6.3.7 Eppendorf SE

- 6.3.8 VWR International LLC

- 6.3.9 Becton Dickinson & Co.

- 6.3.10 Getinge AB

- 6.3.11 Greiner Bio-One GmbH

- 6.3.12 Matrix F.T.

- 6.3.13 Gelatex Technologies

- 6.3.14 CelVivo ApS

- 6.3.15 CELLTREAT Scientific

- 6.3.16 HiMedia Laboratories

- 6.3.17 Microcarriers Labs (China)

- 6.3.18 Esco Aster

- 6.3.19 Nanofiber Solutions

- 6.3.20 PBS Biotech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment