|

시장보고서

상품코드

1846223

성인 악성 신경교종 치료제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Adult Malignant Glioma Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

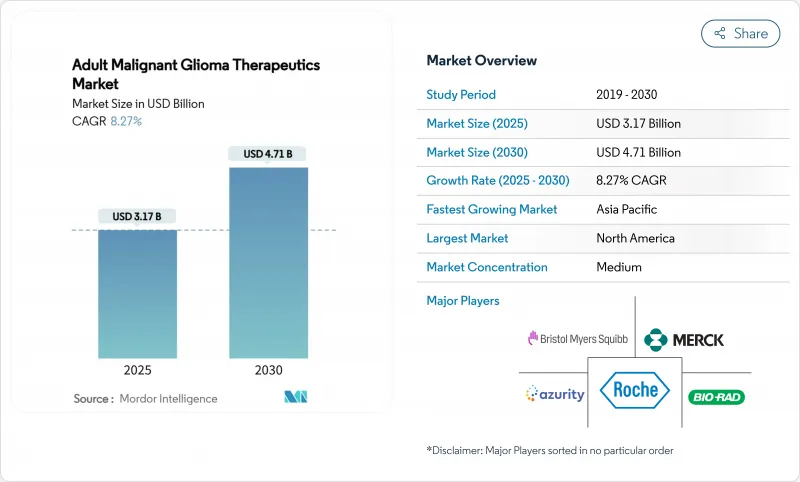

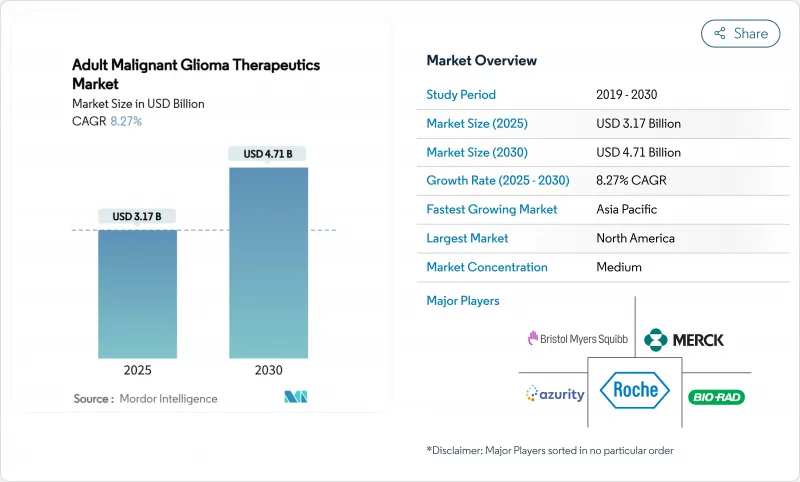

성인 악성 신경교종 치료제 시장 규모는 2025년에 31억 7,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 8.27%로 47억 1,000만 달러에 이를 것으로 예상됩니다.

파이프라인의 기세는 LP-184와 같은 퍼스트 인 클래스 자산의 심사 기간을 단축하는 FDA 패스트 트랙 프로그램과 획기적인 프로그램, 그리고 종양 특성화와 치료법의 매칭을 개선하는 AI 주도 진단 도구에 기인합니다. 벤처 캐피탈은 고정밀 플랫폼에 계속 유입되고 있으며, 주요 제약 회사는 테모졸로미드 내성과 혈액 뇌 장벽 전달의 과제를 상쇄하기 위해 표적 포트폴리오를 통합하고 있습니다. 지역적으로는 북미가 상환 지원을 통해 상업적인 보급을 지지하고 있지만, 아시아태평양에서는 병원망의 확대와 규제의 조화가 다음 수요의 물결을 일으키고 있습니다. 병행하여 Tumor Treating Fields(TTFields)와 같은 장치 기반 치료법, 바이오시밀러 베바시주맙의 상시, 초기 연구에서 양호한 안정 발병률을 기록한 세포 기반 치료법에도 성장 기회가 발생하고 있습니다.

세계의 성인 악성 신경교종 치료제 시장 동향과 인사이트

악성 신경교종의 발생률 상승

역학적 예측에 따르면 아시아의 신경교종 증례는 2040년까지 39.3% 급증하고 성인 악성 신경교종 치료제 시장은 신흥 경제권으로 근본적으로 이동합니다. 이미징의 인프라가 개선됨에 따라 종양이 조기에 발견되고 이전에 기록되지 않은 환자들이 전국 등록에 참여하게 되었습니다. 또한 아시아 청소년 코호트는 치료 내성이 높기 때문에 지역에 특화된 임상시험과 지역 특유의 프로토콜 조정이 촉진됩니다. 중국의 주요 시설에서의 생존율은 이미 많은 서양 벤치마크를 능가하고 있으며 생물학적 또는 치료 경로의 차이 가능성을 시사하고 있습니다. 따라서 의약품 개발 기업은 유전적으로 다양한 집단에서 분자 표적 치료 요법을 검증하기 위해 중국, 인도, 한국에서 임상시험 발자국을 늘려야 합니다.

지속적인 공적 R&D 자금

성인 악성 신경교종 치료제 시장은 초기 단계의 위험을 상쇄하는 정부 지출의 혜택을 받고 있습니다. 캘리포니아 재생 의료 연구소(California Institute for Regenerative Medicine)는 UCSF의 CAR-T 교아종 프로그램에 1,100만 달러를 할당하고 뇌종양을 대상으로 한 NIH와 국방부의 항목을 보완하고 있습니다. 유럽에서는 Horizon Europe의 보조금으로 11개국의 43개 시설에서 411명의 환자가 등록된 LEGATO 연구가 이 궤적을 반영합니다. 공적 조성금은 직접적인 조성금뿐만 아니라 세제상의 우대조치나 산학협동의 인큐베이터에도 퍼져 있어, 시노노치 세포요법이나 나노입자 전달 비히클 등 퍼스트 인 클래스의 컨셉에 대한 자본 장벽을 낮추고 있습니다.

후기 임상시험의 성공률이 낮음

3상 교모세포종 프로그램의 성공률은 여전히 5% 미만이며, 투자자의 신뢰를 훼손하고 필요한 자본을 부풀리고 있습니다. 따라서 성인 악성 신경교종 치료제 시장에서는 각 회사가 위험이 높은 중추 신경계 질환과 고형 종양 프랜차이즈의 균형을 맞추면서 포트폴리오의 다양화를 추진하고 있습니다. 실패의 대부분은 오프 타겟 독성, 혈액 뇌 장벽으로의 불충분한 침투, 또는 대조군의 아웃퍼폼에 기인합니다. 실패할 때마다 5억 달러의 썽크 비용이 발생하기 때문에 재무적 익스포저를 공유하는 제휴가 추진됩니다. 벤처 신디케이트는 엄격한 이정표 기반의 트랜시 금융을 삽입함으로써 대응하여 소규모 진출 기업의 스케줄을 길게 하고 있습니다.

부문 분석

2024년 성인 악성 신경교종 치료제 시장 점유율은 다형 교모세포종이 58.38%로 최상위를 차지했으며, 스폰서는 혈액뇌 장벽 투과화학과 적응 시험 디자인에 중점을 두었습니다. 퇴형성 빈곤돌기 교종은 보라시데닙과 같은 IDH를 표적으로 하는 획기적인 약물에 도움이 되며, 2030년까지의 CAGR은 9.41%로 성장을 지속하고, 절대 기준으로는 성인 악성 신경교종 치료제 시장 규모에의 기여를 높이는 방향에 있습니다. 퇴형성 성세포종은 병용 요법에 안정적인 자금을 모으고, 퇴형성 빈돌기 세포종은 환자를 돌연변이 특이적 프로토콜로 유도하는 정교한 WHO 재분류로부터 이익을 얻고 있습니다.

무증상 생존 기간 중앙값이 위약의 11.1개월에 비해 27.7개월이었던 보라시데닙의 성공은 유전형으로 유도된 디자인이 어떻게 조직형 중심 접근법보다 더 우수한가를 보여줍니다. 패널 시퀀싱이 일상적으로 이루어지면 개발자는 소분자 라이브러리를 명확하게 정의된 하위 집단에 맞추어 임상시험에서 통계적 감지력을 향상시키고 조건부 승인을 용이하게 합니다. 따라서 성인 악성 신경교종 치료제 시장은 소규모의 신속한 시험으로 이동하여 자본 효율성을 고 응답 코호트로 향하게합니다.

지역 분석

북미는 2024년 성인 악성 신경교종 치료제 시장 규모의 41.84%를 차지하며, 견고한 상환제도, NCI 지정 시험 네트워크, 높은 진단률에 지지되었습니다. 미국은 고속 트럭 지정으로 선도하고 있으며, 보라시데닙과 같은 제품이 1년 이내에 중요한 데이터에서 승인으로 전환할 수 있습니다. 캐나다는 주 의료 기술 평가를 통합하고 있으며 캐나다 보건부의 결정이 FDA 판례와 일치하면 상환이 촉진됩니다.

아시아태평양은 CAGR 11.92%로 가장 급성장하고 있어 현대적인 방사선치료실을 증설하고 중국, 일본, 한국의 센터를 세계 프로토콜에 추가하는 것을 가속화하고 있습니다. 베이징과 상하이의 대규모 3차 병원에서 보고된 뛰어난 생존 지표는 프로토콜의 차이를 해독하기 위한 비교 효과 공동 연구의 방아쇠가 되었습니다. ASEAN 상호 승인 계약 하에서 조화를 이룬 규칙은 장비 기반 치료에 대한 장벽을 더욱 줄이고, 이 지역을 양과 기술 혁신의 허브로 자리잡고 있습니다.

EMA의 Project Orbis가 시장 진입의 격차를 줄이고 유럽은 안정된 기세를 유지했습니다. 독일, 프랑스, 영국이 시험 시작의 대부분을 차지하는 반면, 남유럽과 동유럽 국가들은 범 지역적 윤리 심사 조정의 혜택을 받고 있습니다. Horizon Europe의 보조금은 LEGATO와 같은 다자간 데이터 세트에 자금을 제공하고 NICE 및 G-BA 결정에 직접 반영되는 의사 중심의 증거 생성을 강화하고 있습니다. 따라서 성인 악성 신경교종 치료제 시장은 대륙 전체 플랫폼의 조화를 누리고 매우 중요한 등록에서 스폰서의 ROI를 향상시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 악성 신경교종의 발생률의 상승

- 공적 연구 개발 자금 유지

- 신규 디바이스의 퍼스트 트랙 및 브레이크 스루 지정

- AI에 의한 조기 진단과 치료 계획

- 벤처캐피탈에 의한 BNCT 플랫폼에 대한 투자 급증

- 베바시주맙·바이오시밀러의 입수 가능성

- 시장 성장 억제요인

- 성공률이 낮은 후기 임상시험

- 테모졸로미드 내성의 급속한 출현

- 붕소 10 아이소토프공급 체인의 병목

- 발생률이 높은 종양으로 전환된 종양학 연구개발 자본

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측(금액 기준)

- 질환 유형별

- 다형성 교모세포종

- 역형성 성상세포종

- 역형성 올리고교세포종

- 역형성 올리고성상세포종

- 기타 고등급 신경교종

- 치료법별

- 항암요법

- 테모졸로미드

- 로무스틴

- 카무스틴

- 베바시주맙

- 기타 알킬화제

- 표적 치료

- EGFR 억제제

- VEGF/VEGFR 억제제

- IDH 억제제

- 면역요법

- 체크포인트 억제제

- CAR-T/NK 세포 치료

- 종양용해 바이러스

- 기기 기반 치료

- 방사선 치료

- 유전자 및 세포 치료

- 항암요법

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche

- Merck & Co.

- Pfizer

- Novocure

- Bristol-Myers Squibb

- Amgen

- AbbVie

- AstraZeneca

- Chimerix

- DelMar Pharma

- Sumitomo Heavy Industries

- TAE Life Sciences

- Bluebird Bio

- Immunomic Therapeutics

- Ono Pharma

- GlaxoSmithKline

- Novartis

- Boehringer Ingelheim

- Servier

- Sun Pharma

제7장 시장 기회와 전망

KTH 25.10.31The Adult Malignant Glioma Therapeutics Market size is estimated at USD 3.17 billion in 2025, and is expected to reach USD 4.71 billion by 2030, at a CAGR of 8.27% during the forecast period (2025-2030).

Pipeline momentum stems from the FDA's fast-track and breakthrough programs, which shorten review timelines for first-in-class assets such as LP-184, and from AI-driven diagnostic tools that improve tumor characterization and treatment matching. Venture capital continues to flow into precision platforms, while large pharmaceutical firms consolidate targeted portfolios to offset temozolomide resistance and the blood-brain-barrier delivery challenge. Regionally, North America anchors commercial uptake through reimbursement support, yet hospital network expansion and regulatory harmonization in Asia Pacific are catalyzing the next demand wave. Parallel growth opportunities arise in device-based modalities like Tumor Treating Fields (TTFields), biosimilar bevacizumab launches, and cell-based therapies that register favorable stable-disease rates in early studies.

Global Adult Malignant Glioma Therapeutics Market Trends and Insights

Rising Incidence of Malignant Gliomas

Epidemiological projections indicate that Asian glioma cases will jump 39.3% by 2040, fundamentally shifting the Adult malignant glioma therapeutics market toward emerging economies. Improved imaging infrastructure now detects tumors earlier, adding previously undocumented patients to national registries. Younger Asian cohorts also present higher treatment tolerance, encouraging localized clinical trials and region-specific protocol adjustments. Survival rates from leading Chinese centers already surpass many Western benchmarks, implying potential biological or care-pathway differences. Drug developers therefore increase trial footprints in China, India, and South Korea to validate molecularly targeted regimens in genetically diverse populations.

Sustained Public-Sector R&D Funding

The adult malignant glioma therapeutics market benefits from government spending that offsets early-stage risk. The California Institute for Regenerative Medicine has allocated USD 11 million to UCSF's CAR-T glioblastoma program, complementing NIH and DoD line items aimed at brain cancer. Europe mirrors this trajectory through Horizon Europe grants that underpin the LEGATO study, which enrolls 411 patients at 43 sites across 11 countries. Public co-funding stretches beyond direct grants to include tax incentives and academic-industry incubators, thereby lowering capital barriers for first-in-class concepts such as synNotch cell therapies and nanoparticle delivery vehicles.

Low Late-Stage Trial Success Rates

Success rates in phase 3 glioblastoma programs remain below 5%, eroding investor confidence and inflating capital requirements. The Adult malignant glioma therapeutics market therefore witnesses portfolio diversification as companies balance high-risk CNS assets with solid-tumor franchises. Failures often stem from off-target toxicity, insufficient blood-brain-barrier penetration, or control-arm outperformance. Each setback can wipe USD 500 million in sunk costs, driving partnerships that share financial exposure. Venture syndicates react by inserting stringent milestone-based tranched financing, prolonging timelines for smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

- Fast-Track & Breakthrough Designations for Novel Devices

- AI-Enabled Early Diagnosis & Treatment Planning

- Rapid Emergence of Temozolomide Resistance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glioblastoma multiforme led with 58.38% of the adult malignant glioma therapeutics market share in 2024, a level that steered sponsor focus toward blood-brain-barrier penetration chemistry and adaptive trial designs. Anaplastic oligodendroglioma, aided by IDH-targeted breakthroughs such as vorasidenib, is registering a 9.41% CAGR to 2030 and is on course to raise its contribution to the Adult malignant glioma therapeutics market size in absolute terms. Anaplastic astrocytoma garners steady funding for combination regimens, while anaplastic oligoastrocytoma benefits from refined WHO re-classification that funnels patients into mutation-specific protocols.

The success of vorasidenib, which delivered 27.7-month median progression-free survival against 11.1 months for placebo, illustrates how genotype-guided design outperforms histology-centric approaches. As panel sequencing becomes routine, developers can match small-molecule libraries to well-defined subpopulations, improving statistical power in trials and facilitating conditional approvals. The Adult malignant glioma therapeutics market therefore shifts toward smaller, faster studies that direct capital efficiency toward high-response cohorts.

The Adult Malignant Glioma Therapeutics Market Report is Segmented by Disease Type (Glioblastoma Multiforme, Anaplastic Astrocytoma, Anaplastic Oligodendroglioma, and More), Therapy (Chemotherapy, Targeted Therapy, Immunotherapy, Device-Based Therapy, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 41.84% of the Adult malignant glioma therapeutics market size in 2024, supported by robust reimbursement schemes, NCI-designated trial networks, and high diagnosis rates. The United States leads in fast-track designations, enabling products like vorasidenib to move from pivotal data to approval within a year. Canada integrates provincial health technology assessments that expedite reimbursement once Health Canada decisions align with FDA precedents.

Asia Pacific is the fastest-growing theatre at an 11.92% CAGR, adding modern radiotherapy suites and accelerating inclusion of Chinese, Japanese, and South Korean centers in global protocols. Superior survival metrics reported by large tertiary hospitals in Beijing and Shanghai have triggered comparative-effectiveness collaborations to decode protocol differences. Harmonized rules under the ASEAN Mutual Recognition Arrangement further reduce barriers for device-based therapies, positioning the region as a volume and innovation hub.

Europe posts stable momentum as EMA's Project Orbis shortens market entry gaps. Germany, France, and the United Kingdom dominate trial starts, while Southern and Eastern European countries benefit from pan-regional ethical-review alignment. Horizon Europe grants finance multi-national datasets such as LEGATO, reinforcing investigator-initiated evidence generation that feeds directly into NICE and G-BA decisions. The Adult malignant glioma therapeutics market thus enjoys continent-wide platform harmonization, improving sponsor ROI on pivotal enrollment.

- Roche

- Merck

- Pfizer

- Novocure

- Bristol-Myers Squibb

- Amgen

- Abbvie

- AstraZeneca

- Chimerix

- DelMar Pharma

- Sumitomo Heavy Industries

- TAE Life Sciences

- Bluebird Bio

- Immunomic Therapeutics

- Ono Pharma

- GlaxoSmithKline

- Novartis

- Boehringer Ingelheim

- Servier

- Sun Pharmaceuticals Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Malignant Gliomas

- 4.2.2 Sustained Public-Sector R&D Funding

- 4.2.3 Fast-Track & Breakthrough Designations for Novel Devices

- 4.2.4 Ai-Enabled Early Diagnosis & Treatment Planning

- 4.2.5 Venture Capital Surge into BNCT Platforms

- 4.2.6 Availability of Bevacizumab Biosimilars

- 4.3 Market Restraints

- 4.3.1 Low Late-Stage Trial Success Rates

- 4.3.2 Rapid Emergence of Temozolomide Resistance

- 4.3.3 Boron-10 Isotope Supply-Chain Bottlenecks

- 4.3.4 Oncology R&D Capital Diverted to Higher-Incidence Tumors

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Disease Type

- 5.1.1 Glioblastoma Multiforme

- 5.1.2 Anaplastic Astrocytoma

- 5.1.3 Anaplastic Oligodendroglioma

- 5.1.4 Anaplastic Oligoastrocytoma

- 5.1.5 Other High-Grade Gliomas

- 5.2 By Therapy

- 5.2.1 Chemotherapy

- 5.2.1.1 Temozolomide

- 5.2.1.2 Lomustine

- 5.2.1.3 Carmustine

- 5.2.1.4 Bevacizumab

- 5.2.1.5 Other Alkylating Agents

- 5.2.2 Targeted Therapy

- 5.2.2.1 EGFR Inhibitors

- 5.2.2.2 VEGF/VEGFR Inhibitors

- 5.2.2.3 IDH Inhibitors

- 5.2.3 Immunotherapy

- 5.2.3.1 Checkpoint Inhibitors

- 5.2.3.2 CAR-T/NK Cell Therapy

- 5.2.3.3 Oncolytic Viruses

- 5.2.4 Device-Based Therapy

- 5.2.5 Radiation Therapy

- 5.2.6 Gene & Cell Therapy

- 5.2.1 Chemotherapy

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche

- 6.3.2 Merck & Co.

- 6.3.3 Pfizer

- 6.3.4 Novocure

- 6.3.5 Bristol-Myers Squibb

- 6.3.6 Amgen

- 6.3.7 AbbVie

- 6.3.8 AstraZeneca

- 6.3.9 Chimerix

- 6.3.10 DelMar Pharma

- 6.3.11 Sumitomo Heavy Industries

- 6.3.12 TAE Life Sciences

- 6.3.13 Bluebird Bio

- 6.3.14 Immunomic Therapeutics

- 6.3.15 Ono Pharma

- 6.3.16 GlaxoSmithKline

- 6.3.17 Novartis

- 6.3.18 Boehringer Ingelheim

- 6.3.19 Servier

- 6.3.20 Sun Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment