|

시장보고서

상품코드

1846235

전자 피부 패치 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Electronic Skin Patches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

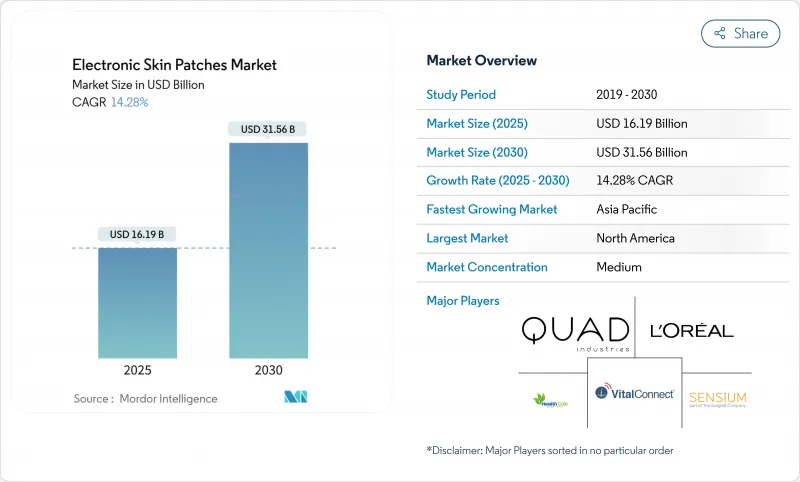

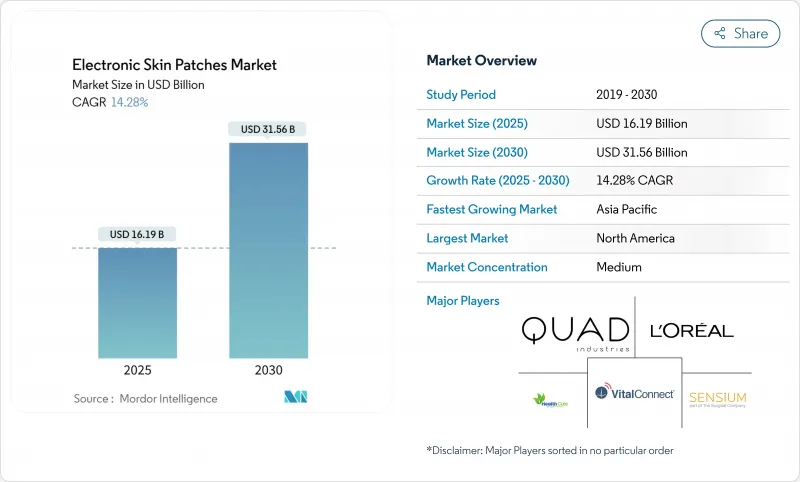

전자 피부 패치 시장은 2025년 161억 9,000만 달러로 평가되었으며, 2025-2030년 CAGR 14.28%를 나타내 2030년에는 315억 6,000만 달러에 이를 것으로 예상됩니다.

센싱 및 진단 패치는 2024년 최대 46%의 수익 점유율을 차지했으며 배터리가 없는 전력 아키텍처에 의해 실현되는 에너지 수확 스마트 패치는 21.8%의 연평균 복합 성장률(CAGR) 전망에서 가장 강합니다. 심혈관 모니터링은 38.2% 점유율로 모든 애플리케이션을 이끌고 있지만 여성의 건강과 불임은 가정에서 유방 초음파 검사와 호르몬 추적 패치가 새로운 사용자를 유치하기 때문에 가장 빠른 19.51%의 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 지역별로는 북미가 Dexcom과 Abbott에 의한 시판되는 지속 포도당 모니터(CGM)의 FDA 인가(2024년)를 배경으로 37.9%의 점유율을 차지하는 반면, 아시아태평양은 대규모 전자기기 제조와 지원적인 기술 혁신 프로그램에 힘입어 CAGR 16.5%로 가속화하고 있습니다. VitalConnect와 Biolinq는 각각 대량 생산과 규제 당국에 대한 신청을 확대하기 위해 2025년에 1억 달러의 라운드를 확보하고, 자금 조달 채널이 임상적으로 검증된 센서와 소비자 등급의 사용성을 융합시킨 플랫폼에 보상하고 있음을 보여줍니다.

세계의 전자 피부 패치 시장 동향과 인사이트

지속 혈당 측정(CGM) 패치 채용 급증

2024년 Dexcom Stelo와 Abbott Lingo의 FDA 허가는 처방전 장벽을 없애고 인슐린을 투여하지 않은 미국 2형 당뇨병 환자 2,500만 명에게 CGM 카테고리를 개방했습니다. Dexcom의 Simplera와 같은 일회용 올인원 디자인은 지불자와 의료 제공업체의 교육 비용을 낮추고 약국 채널에서 신속한 보급을 촉진합니다. Dexcom은 Stelo의 첫해 매출을 4,000만 달러로 예상하고, 이는 새로운 대응이 가능한 부문에서 강력한 탄력성을 보여줍니다. 제약 회사는 현재 CGM 데이터 스트림을 체중 감량 및 대사 증후군 프로그램에 통합하고 있으며, 중심 당뇨병 집단 외에도 장비 수요를 확대하고 있습니다. 성장은 세계적이지만 북미는 유리한 상환으로 조기에 대수를 획득하고 있습니다. 공급업체는 포도당 원격 측정을 폐쇄형 루프 치료 생태계에 통합하기 위해 경쟁하고 있으며 가정 환경에서 손가락 측정기에서 교체를 가속화하고 있습니다.

재택 심장 텔레메트리 상환 확대

메디케어, 미국 주요 민간보험사 및 EU의 일부 지급자는 기존의 원격 측정에 비해 재입원률이 최대 30% 낮은 이유로 14일 및 30일 패치 ECG 서비스에 현재 상환금을 지불하고 있습니다. 바이탈커넥트는 2025년 1억 달러의 자금조달로 재택병원과의 계약용으로 바이탈패치의 출력을 3배로 늘렸습니다. 전복 예방 DRG의 대상이 되는 LEAF Patient Monitoring System과 같은 보완적인 플랫폼은 다중 매개변수 패치가 심장병 및 안전 이용 사례를 어떻게 묶을 수 있는지 보여줍니다. 상환이 명확하기 때문에 의료 시스템 조달 예산이 모여 노인 환자에게 부피가 큰 홀터 모니터보다 패치가 선호됩니다. 현재 미국에서의 확대는 가장 강력하지만 독일, 프랑스, 일본은 파일럿 코드를 도입하고 있으며, 중기적으로는 유럽과 아시아에서의 확대가 전망됩니다.

데이터 보안 및 개인 정보 보호 준수 비용

의료기기와 소비자 웰빙 카테고리가 모호한 패치는 단편적 규제에 직면합니다. HIPAA는 많은 소비자용 웨어러블 단말기를 면제하고 있지만, GDPR(EU 개인정보보호규정)은 엄격한 동의, 암호화, 데이터 최소화 의무를 부과하고 있습니다. 두 프레임워크를 모두 충족할 수 있는 듀얼 스택 아키텍처를 구축하면 소규모 제조업체의 R&D 예산에 15-20%를 추가할 수 있습니다. 웨어러블 데이터에 대한 명확한 법률은 미국의 20개 주에서만 법적 불확실성이 보수적인 보안 투자를 촉진하고 있습니다. 대규모의 기존 기업들은 기존의 SOC-2와 ISO-27001 프로그램을 이용하여 컴플라이언스의 고정비를 분산시켜 경쟁력의 격차를 넓히고 있습니다.

부문 분석

에너지 수확형 스마트 패치는 CAGR 21.8%를 나타내 수요 속도로 기존의 전지식 센싱 플랫폼을 추구합니다. 이 하위 카테고리의 전자 피부 패치 시장 규모는 전력 자율 설계가 환경 폐기물 및 주간 센서 교환과 관련된 사용자 불편을 모두 제거하기 때문에 2025년에서 2030년 사이에 3배 이상이 될 것으로 예측됩니다. 센싱·진단용 패치는 성숙하고 있는 것, 2024년 매출의 46%를 차지해 임상의가 정확함과 확립된 상환을 우선하는 규제된 케어 경로에서는 필수적이었습니다. 약물전달 패치는 통증 치료와 호르몬 치료로 안정적인 보급을 계속하고 있지만, 에너지 수확형이 즐기는 성장 억양에는 부족합니다. 코스메틱 & 웰니스 패치는 안티 에이징과 수분 보급 분석에 소비자의 주목을 받고 있으며, 데이터 풍부한 개인화에 열성적인 미용 관계자를 끌어들이는 속삭이지만 상승 중인 수익 라인을 형성하고 있습니다.

최근의 산학 연계에 의해 6분간의 충전으로 20 mA cm-2를 출력하는 땀으로 움직이는 마이크로 슈퍼커패시터가 제조되어, 연구실의 프로토타입을 넘은 실세계에서의 즉응성이 검증되었습니다. 워털루 대학의 연구자들은 열전사를 생체 적합성 기판에 직접 편성하여 두께를 추가하지 않고 전력과 센서 어레이를 통합했습니다. 이러한 진보는 더 얇고 유연한 스택을 중심으로 하우징을 재설계하고 팔꿈치와 무릎과 같은 움직임이 심한 해부학적 부위에 장치를 맞추는 OEM 로드맵과 일치합니다. IP가 성숙함에 따라 칩 제조업체, 접착제 제조업체, 소비자 헬스 브랜드 간의 라이선싱 거래가 가속화되어 외래 환자의 프로토콜과 라이프 스타일 부문에서의 전자 피부 패치 시장의 침투가 더욱 촉진되어야 합니다.

심혈관 모니터링은 2024년에 38.2%의 전자 피부 패치 시장 점유율을 차지하고 리듬 모니터링을 통해 재입원을 줄이는 지불자의 초점에 의해 지지되었습니다. 그러나 CAGR19.51%로 예측되는 여성의 건강과 불임의 응용은 오랫동안 방치되어 온 임상 요구가 벤처 기업의 지원을 받게 되어 현재 가장 역동적인 벡터를 보여주고 있습니다. 매사추세츠 공과대학(MIT)의 휴대용 유방 초음파 패치는 자기 완결형 이미징이 병원에서 거실로 어떻게 이동하는지를 보여줍니다. 수태능 추적기업은 호르몬을 감지하는 하이드로겔을 활용하여 황체형성 호르몬을 지속적으로 측정하고, 기초 체온표보다 정확한 주기 예측을 사용자에게 제공합니다.

통증과 근골격계 관리는 신경 신호를 게이트하는 전기 자극 패치를 활용하여 오피오이드를 사용하지 않는 진통을 제공합니다. 당뇨병 관리는 CGM의 수에 따라 여전히 큰 규모를 유지하고 있지만, 인슐린 의존 코호트에서는 보급이 포화에 가까워지고 성장이 완만해지고 있습니다. 신경 정신 건강은 아직 시작되었지만 유망합니다. 전기 피부 활동 패치는 머신러닝 분류기와 결합되어 불안 에피소드를 스크리닝하고 적시에 행동 신호를 가능하게합니다. 애플리케이션의 다양화는 수익의 순환성을 줄이고 전자 피부 패치 산업이 충분한 서비스를받지 못한 사람들에게 축발을 옮길 수있는 능력을 강조합니다.

전자 피부 패치 시장 보고서는 제품 유형(센싱 및 진단 패치, 약물 전달 패치 등), 용도(심혈관 모니터링, 약물 전달 등), 기술(전기 화학 바이오 센서, MEMS 및 미세 유체 공학, 기타), 접착 재료(실리콘 기반, 아크릴 기반, 기타), 최종 사용자(병원 및 클리닉, 홈 건강 관리, 기타)

지역 분석

북미는 2024년 37.9%의 전자 피부 패치 시장 점유율을 차지해 FDA(미국 식품의약품국)가 OTC CGM을 약국 선반에 늘어놓게 했기 때문에 내분비 클리닉 이외의 진료소에서도 판매량이 확대됐습니다. 병원 - 재택 상환 코드를 사용하면 원격 모니터링이 공급자의 예측 가능한 수입원이 되고 유통의 최고점 이후에도 구매 주문이 유지됩니다. 캐나다에서는 주마다의 원격 심장 질환 프로그램이 시행되고, 멕시코의 마키라도라에서는 USMCA에 의한 관세가 걸리지 않는 물류가 OEM의 조립을 유치해, 육상 비용을 8-10% 삭감합니다.

아시아태평양의 CAGR은 가장 빠른 16.5%를 나타내며, 이는 중국의 'Healthy China 2030'계획에 의한 디지털 헬스 파일럿에의 자금 공급과 일본의 실버 이코노미 수요의 급증에 의한 것입니다. 한국의 ODM 공장은 플렉스 PCB의 에칭으로부터 무균 포장까지의 수직 통합을 판매하고 있어, 이 지역에 진입하는 구미 브랜드의 리드 타임을 단축하고 있습니다. 인도의 National Digital Health Mission은 시험적인 당뇨병 프로그램에서 Bluetooth LE 대응 패치를 환불했습니다.

유럽은 GDPR(EU 개인정보보호규정) 마찰에도 불구하고 꾸준히 성장 : 엄격한 데이터 관리는 온패치 암호화 ASIC에 대한 투자를 촉진하고 프리미엄 ASP를 요구할 수 있는 차별화된 제품을 생산합니다. 2027년에 시행되는 유럽권의 전지 규제는 에코 설계의 인센티브에 따르는 형태로, 제조업체를 바이오연료전지로 향하게 합니다. 독일은 바덴 뷔르템베르크의 관민 클러스터를 활용하여 폴리머 연구를 진행하고 영국 NHS는 2026년까지 5,000개의 급성기 병상을 해방하는 목표 병동 목표에 패치를 통합합니다. 북유럽 전자 처방전 네트워크는 CGM 데이터를 자동으로 연결하여 기본 치료에서 알고리즘을 통해 인슐린 투여를 가능하게 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 지속 혈당 측정(CGM) 패치 채용 급증

- 재택 심장 텔레메트리 상환의 확대

- 고령화와 만성기 의료의 분산화

- 유연한 바이오연료전지 전원의 양산화

- 커넥티드 패치의 재택 CPT 코드화

- 디지털 치료 플랫폼과의 API 레벨에서의 통합

- 시장 성장 억제요인

- 데이터 보안 및 개인 정보 보호 규정 준수 비용

- 점착성/피부 자극성의 실패율

- 전지 폐기 및 전자 폐기물 규제의 압력

- 신흥국에서의 패치 상환 갭

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 투자와 자금 동향

제5장 시장 규모와 성장 예측

- 제품 유형별

- 감지 및 진단 패치

- 약물전달 패치

- 전기 자극 패치

- 화장품 및 웰니스 패치

- 에너지 수확 스마트 패치

- 용도별

- 심혈관 모니터링

- 당뇨병 관리

- 통증/근골격계

- 감염증 및 발열

- 여성 건강 및 불임

- 신경 및 정신 건강

- 스포츠 및 피트니스

- 약물전달

- 기술별

- 전기화학 바이오센서

- 광학/PPG 센서

- MEMS 및 마이크로유체학

- RFID/NFC 스마트 패치

- 에너지 수확 및 배터리 불필요

- 접착재별

- 실리콘계

- 아크릴계

- 하이드로겔계

- 기타(PU, 하이브리드)

- 최종 사용자별

- 병원 및 진료소

- 재택 헬스케어

- 스포츠 및 피트니스 센터

- 군사 및 응급 서비스

- 미용 및 피부과 클리닉

- 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- UAE

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- DexCom Inc.

- iRhythm Technologies Inc.

- VitalConnect Inc.

- Medtronic plc

- Insulet Corporation

- Leaf Healthcare Inc.

- Sensium Healthcare Ltd.

- MC10 Inc.

- Quad Industries SA

- L-Or-al SA

- Philips Healthcare

- GE Healthcare

- Nemaura Medical

- VivaLNK

- Masimo Corporation

- Blue Spark Technologies

- G-Tech Medical

- Omron Healthcare

- Nutromics

제7장 시장 기회와 전망

KTH 25.11.07The electronic skin patch market is valued at USD 16.19 billion in 2025 and is forecast to reach USD 31.56 billion by 2030, reflecting a 14.28% CAGR over 2025-2030.

Sensing and Diagnostic Patches hold the largest 46% revenue share in 2024, while Energy-Harvesting Smart Patches, enabled by battery-less power architectures, post the strongest 21.8% CAGR outlook. Cardiovascular Monitoring leads all applications at 38.2% share, but Women's Health and Fertility registers the fastest 19.51% CAGR as at-home breast ultrasound and hormone tracking patches attract new users. Regionally, North America commands 37.9% share, backed by FDA clearance of over-the-counter continuous glucose monitors (CGMs) from Dexcom and Abbott in 2024, whereas Asia Pacific accelerates at 16.5% CAGR underpinned by large-scale electronics manufacturing and supportive innovation programs. Investment momentum remains high: VitalConnect and Biolinq each secured USD 100 million rounds in 2025 to expand high-volume manufacturing and regulatory submissions, illustrating how funding channels reward platforms that blend clinically validated sensors with consumer-grade usability.

Global Electronic Skin Patches Market Trends and Insights

Continuous Glucose-Monitoring (CGM) Patch Adoption Surge

FDA clearance of Dexcom Stelo and Abbott Lingo in 2024 removed prescription barriers and opened the CGM category to 25 million U.S. type 2 diabetics not on insulin, while also legitimizing consumer-grade biosensing for preventive metabolic health. Disposable, all-in-one designs such as Dexcom's Simplera lower training costs for payers and providers, fostering rapid uptake in pharmacy channels. Dexcom projects USD 40 million first-year revenue from Stelo, signaling strong elasticity in the newly addressable segment. Pharmaceutical firms are now embedding CGM data streams into weight-loss and metabolic-syndrome programs, expanding device demand beyond the core diabetes cohort. Growth is global, yet North America captures early volumes due to favorable reimbursement. Vendors are racing to integrate glucose telemetry into closed-loop therapy ecosystems, accelerating replacement of finger-stick meters in home settings.

Home-Based Cardiac Telemetry Reimbursement Expansion

Medicare, major U.S. commercial insurers, and several EU payers now reimburse 14-day and 30-day patch ECG services, citing up to 30% lower readmission rates compared with traditional telemetry. VitalConnect earmarked its 2025 USD 100 million raise to triple VitalPatch output for Hospital-at-Home contracts. Complementary platforms such as the LEAF Patient Monitoring System, covered under fall-prevention DRGs, illustrate how multiparameter patches can bundle cardiology and safety use-cases. Reimbursement clarity attracts health-system procurement budgets, which favor patches over bulky holter monitors for elderly patients. Expansion is strongest in the United States today, yet Germany, France, and Japan have introduced pilot codes that should unlock medium-term European and Asian volume.

Data-Security and Privacy Compliance Costs

Patches that blur medical-device and consumer-wellness categories face fragmented regulation. HIPAA exempts many direct-to-consumer wearables, while GDPR imposes strict consent, encryption, and data-minimization obligations. Building dual-stack architectures capable of satisfying both frameworks can add 15-20% to R&D budgets for small manufacturers. Only 20 U.S. states have explicit wearable data laws, creating legal uncertainty that drives conservative security investments. Larger incumbents use existing SOC-2 and ISO-27001 programs to spread compliance fixed costs, widening the competitiveness gap.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population and Chronic-Care Decentralisation

- Flexible Biofuel-Cell Power Sources Hit Mass Production

- Adhesion / Skin-Irritation Failure Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Energy-Harvesting Smart Patches are growing at a 21.8% CAGR, overtaking traditional, battery-powered sensing platforms in demand velocity. The electronic skin patch market size for this sub-category is projected to more than triple between 2025 and 2030 as power-autonomous designs remove both environmental waste and user inconvenience linked to weekly sensor swaps. Sensing and Diagnostic Patches, while mature, still control 46% 2024 revenue and remain essential in regulated care pathways where clinicians prioritize accuracy and established reimbursement. Drug-Delivery Patches keep steady adoption in pain and hormone therapy, but lack the growth inflection energy-harvesting variants enjoy. Cosmetic and Wellness Patches, driven by consumer focus on anti-aging and hydration analytics, form a modest but rising revenue line that attracts beauty majors eager for data-rich personalization.

Recent academic-industry collaboration produced sweat-powered micro-supercapacitors that output 20 mA cm-2 after a six-minute charge, validating real-world readiness beyond lab prototypes. University of Waterloo researchers knit thermoelectric yarns directly into biocompatible substrates, integrating power and sensor arrays without added thickness. Such advances align with OEM roadmaps to re-engineer housings around thinner, more flexible stacks, allowing devices to conform to high-motion anatomical sites like elbows and knees. As IP matures, licensing deals between chipmakers, adhesive formulators, and consumer-health brands should accelerate, further boosting electronic skin patch market penetration in outpatient protocols and lifestyle segments alike.

Cardiovascular Monitoring held a commanding 38.2% electronic skin patch market share in 2024, upheld by payer focus on reducing readmissions through rhythm surveillance. Yet Women's Health and Fertility applications, projected at 19.51% CAGR, now represent the most dynamic vector as long-neglected clinical needs receive venture backing. MIT's portable breast ultrasound patch exemplifies how self-contained imaging can transition from hospitals to living rooms. Fertility-tracking companies leverage hormone-sensing hydrogels for continuous luteinizing hormone readouts, empowering users with cycle predictions more precise than basal-temperature charts.

Pain and Musculoskeletal management harnesses electrical-stimulation patches that gate nerve signals, offering opioid-free analgesia. Diabetes Management remains sizeable due to CGM volume, yet its growth moderates as penetration approaches saturation in insulin-dependent cohorts. Neuro-mental health remains nascent but promising: electrodermal-activity patches, coupled with machine-learning classifiers, screen for anxiety episodes, enabling timely behavioral cues. The diversification across applications reduces revenue cyclicality and underscores the electronic skin patch industry's ability to pivot toward underserved populations.

The Electronic Skin Patches Market Report is Segmented by Product Type (Sensing and Diagnostic Patches, Drug-Delivery Patches, and More), Application (Cardiovascular Monitoring, Drug-Delivery, and More), Technology (Electrochemical Biosensors, MEMS and Microfluidics, and More), Adhesive Material (Silicone-Based, Acrylic-Based, and More), End-User (Hospitals and Clinics, Home Healthcare, and More), and Geography.

Geography Analysis

North America commands 37.9% electronic skin patch market share in 2024, benefited by FDA pathways that brought OTC CGMs to pharmacy shelves, thus expanding unit volumes beyond endocrinology clinics. Hospital-at-Home reimbursement codes convert remote monitoring into predictable revenue streams for providers, sustaining purchase orders even after pandemic peaks. Canada experiments with provincial remote-cardiac programs, while Mexican maquiladoras attract OEM assembly due to tariff-free USMCA logistics, shaving 8-10% off landed costs.

Asia Pacific delivers the fastest 16.5% CAGR, powered by China's Healthy China 2030 blueprint that funds digital-health pilots and by Japan's Silver Economy demand spike. South Korea's ODM fabs tout vertical integration-from flex-PCB etching to sterile packaging-slashing lead times for Western brands entering the region. India's National Digital Health Mission reimburses Bluetooth LE-enabled patches in pilot diabetes programs, albeit with price caps that favor energy-harvesting models over battery-heavy imports.

Europe grows steadily despite GDPR friction: stringent data controls catalyze investments in on-patch encryption ASICs, yielding differentiated products able to command premium ASPs. The bloc's Battery Regulation, effective 2027, pushes manufacturers toward biofuel-cell power, aligning with eco-design incentives. Germany leverages public-private clusters in Baden-Wurttemberg for polymer research, while the U.K. NHS integrates patches into virtual-ward targets aimed at freeing 5,000 acute beds by 2026. Nordic e-prescription networks automatically link CGM data, enabling algorithmic insulin dosing in primary care.

- Abbott Laboratories

- DexCom Inc.

- iRhythm Technologies Inc.

- VitalConnect Inc.

- Medtronic plc

- Insulet Corporation

- Leaf Healthcare Inc.

- Sensium Healthcare Ltd.

- MC10 Inc.

- Quad Industries SA

- L-Or-al SA

- Philips Healthcare

- GE Healthcare

- Nemaura Medical

- VivaLNK

- Masimo Corporation

- Blue Spark Technologies

- G-Tech Medical

- Omron Healthcare

- Nutromics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Continuous glucose-monitoring (CGM) patch adoption surge

- 4.2.2 Home-based cardiac telemetry reimbursement expansion

- 4.2.3 Ageing population and chronic-care decentralisation

- 4.2.4 Flexible biofuel-cell power sources hit mass production

- 4.2.5 Hospital-at-home CPT codes for connected patches

- 4.2.6 API-level integration with digital-therapeutics platforms

- 4.3 Market Restraints

- 4.3.1 Data-security and privacy compliance costs

- 4.3.2 Adhesion / skin-irritation failure rates

- 4.3.3 Battery-disposal and e-waste regulation pressure

- 4.3.4 Patch reimbursement gaps in emerging economies

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment and Funding Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Sensing and Diagnostic Patches

- 5.1.2 Drug-Delivery Patches

- 5.1.3 Electrical-Stimulation Patches

- 5.1.4 Cosmetic and Wellness Patches

- 5.1.5 Energy-Harvesting Smart Patches

- 5.2 By Application

- 5.2.1 Cardiovascular Monitoring

- 5.2.2 Diabetes Management

- 5.2.3 Pain / Musculoskeletal

- 5.2.4 Infectious-Disease and Fever

- 5.2.5 Women's Health and Fertility

- 5.2.6 Neuro and Mental Health

- 5.2.7 Sports and Fitness

- 5.2.8 Drug-Delivery

- 5.3 By Technology

- 5.3.1 Electrochemical Biosensors

- 5.3.2 Optical / PPG Sensors

- 5.3.3 MEMS and Microfluidics

- 5.3.4 RFID / NFC Smart Patches

- 5.3.5 Energy-Harvesting and Battery-less

- 5.4 By Adhesive Material

- 5.4.1 Silicone-based

- 5.4.2 Acrylic-based

- 5.4.3 Hydrogel-based

- 5.4.4 Others (PU, Hybrid)

- 5.5 By End-User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Home Healthcare

- 5.5.3 Sports and Fitness Centres

- 5.5.4 Military and Emergency Services

- 5.5.5 Cosmetic and Dermatology Clinics

- 5.5.6 Research Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 DexCom Inc.

- 6.4.3 iRhythm Technologies Inc.

- 6.4.4 VitalConnect Inc.

- 6.4.5 Medtronic plc

- 6.4.6 Insulet Corporation

- 6.4.7 Leaf Healthcare Inc.

- 6.4.8 Sensium Healthcare Ltd.

- 6.4.9 MC10 Inc.

- 6.4.10 Quad Industries SA

- 6.4.11 L-Or-al SA

- 6.4.12 Philips Healthcare

- 6.4.13 GE Healthcare

- 6.4.14 Nemaura Medical

- 6.4.15 VivaLNK

- 6.4.16 Masimo Corporation

- 6.4.17 Blue Spark Technologies

- 6.4.18 G-Tech Medical

- 6.4.19 Omron Healthcare

- 6.4.20 Nutromics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment