|

시장보고서

상품코드

1846239

인지 보안 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cognitive Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

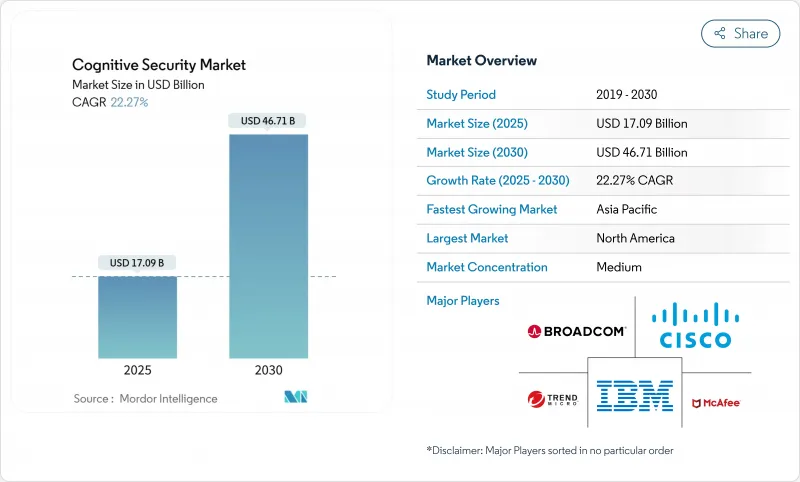

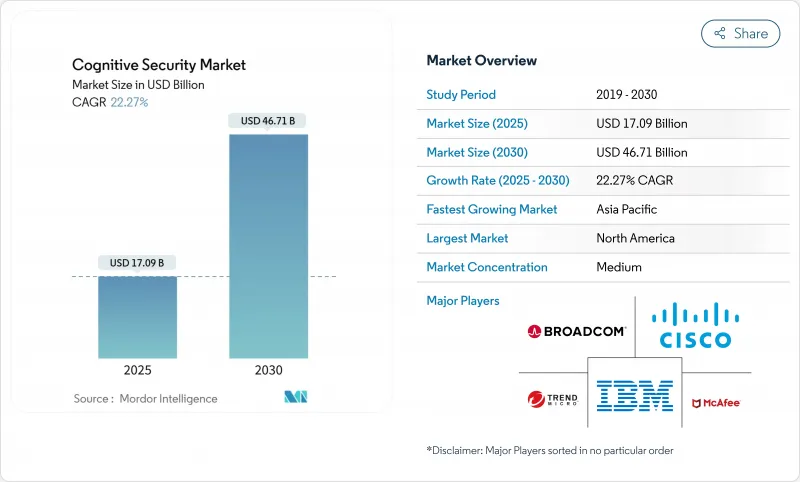

인지 보안 시장은 2025년에 170억 9,000만 달러에 이르고, 2030년에는 467억 1,000만 달러에 달할 것으로 예상되며, CAGR은 22.27%를 나타낼 전망입니다.

AI를 이용한 지속적인 위협, 클라우드 도입에 의한 공격 대상의 확대, 규제 당국의 감시 강화 등이 이 성장을 뒷받침하고 있습니다. 기업은 기존의 툴이 모델 포이즈닝, 적대적인 프롬프트, 합성 데이터의 유출 등 AI 특유의 취약성을 놓치고 있음을 발견한 후, 다액의 투자를 실시해, 고급 분석과 자율적인 방어에 대한 축족을 가속화했습니다. 엔터프라이즈 워크플로우 내에 대규모 언어 모델을 도입하는 움직임이 병렬로 진행되는 경우, 발전 AI를 도입할 때마다 새로운 진입점이 발생하기 때문에 지속적으로 모니터링하고 견고하게 해야 합니다. 벤더는 자기 학습 알고리즘을 사고 대응 플레이북에 통합함으로써 대응하고, 침해를 검출하여 봉쇄할 때까지의 평균 시간을 수시간에서 수분으로 단축하는 동시에, 인간의 애널리스트를 압도하는 오감지 노이즈를 축소합니다. 이러한 역학을 통해 인지 보안 시장은 보다 광범위한 사이버 보안 지출 중 가장 빠르게 확장되는 부문 중 하나로 자리매김하고 있습니다.

세계의 인지 보안 시장 동향과 인사이트

비정형 엔터프라이즈 데이터의 급격한 증가

전자 메일, 협업 파일, 센서 판독값 및 멀티미디어 급증은 시각화 문제와 공격 대상을 모두 확대합니다. 인지 엔진은 테라바이트 단위의 미처리 로그를 캡처하고, 사용자 행동의 일탈을 핀 포인트로 특정함으로써 오감지 경고를 95% 삭감하는 것과 동시에, 룰 베이스의 시스템을 회피하는 스텔스적인 옆의 움직임을 돋보이게 합니다. 그러나 공격자도 마찬가지로 풍부한 정보로부터 이익을 얻고 있으며, 컨텐츠를 스크래핑하여 컨텍스트를 의식한 스피어 피싱 캠페인을 마련하고 있습니다. 따라서 보안 팀은 자체 학습 분석을 데이터 레이크에 직접 통합하고 ID, 기기 및 네트워크 원격 측정을 거의 실시간으로 연결하여 이전에 잠들었던 아카이브를 실용적인 인텔리전스로 바꾸어 침해 감지의 정확성을 높입니다. 인지 보안 시장은 모든 산업에 걸쳐 지속적으로 확장될 수 있습니다.

IoT 어두운 데이터 급증

산업용 및 소비자용 IoT의 도입으로 수십억 대의 관리되지 않은 엔드포인트가 추가되었으며 표준 SIEM 플랫폼에서는 분석할 수 없는 운영 원격 측정의 흐름이 발생했습니다. 인지 엔진은 각 디바이스 클래스의 베이스라인 동작을 모델링하고, 펌웨어의 비정상적인 변경이나 예기치 않은 동서 트래픽 등의 일탈에 플래그를 세웁니다. 에너지 그리드와 스마트 팩토리 플로어에서이 기능은 생명 안전 시스템을 보호하면서 다운 타임 위험을 직접 완화합니다. OT 네트워크가 IT 백본과 융합함에 따라 보안 격차가 확대되고 있으며, 제조업 및 유틸리티 회사는 엄격한 대기 시간 제약 하에서 작동하는 에지 상주형 AI 분석에 투자를 촉구하고 있습니다. 그 결과, 인지 보안 시장 내부에서는 확장 가능하고 디바이스에 의존하지 않는 플랫폼에 대한 수요가 2030년까지 계속 가속화되고 있습니다.

AI/ML 사이버 애널리틱스 인력 부족

강화 학습형 방어의 코딩, 프롬프트 실드 모델의 조정, 위협 텔레메트리 해석을 할 수 있는 전문가에 대한 수요는 세계적인 공급량을 크게 웃돌고 있습니다. 조직은 관리 서비스 전문가에게 아웃소싱하거나 적은 엔지니어로 대규모 자산 기반을 보호할 수 있는 로우코드 오케스트레이션 계층에 투자함으로써 대응하고 있습니다. 레벨 1 트리어지는 자동화에 의해 처리되며, 레벨 2 및 레벨 3 에스컬레이션에는 수학, 보안 코딩, 규제 해석과 같은 하이브리드 기술 세트가 여전히 필요합니다. 그 결과 임금 인플레이션이 프로젝트의 TCO를 팽창시켜 일부 중소기업은 맞춤형 구축이 아닌 소비 기반 클라우드 구독 모델을 목표로 합니다.

부문 분석

On-Premise 솔루션이 2024년 인지 보안 시장의 60.40% 점유율을 유지한 이유는 방위기관, 금융기관, 중요 인프라 사업자가 지역 데이터의 상주와 에어 갭 환경을 계속 의무화했기 때문입니다. 하지만 하이퍼스케일러가 전용으로 구축된 원격 측정 컬렉터와 모델 무결성 검증을 플랫폼에 통합하여 진입 비용을 낮추기 때문에 클라우드 도입은 27.10%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 클라우드 기반 인지 보안 시장 규모는 구독 가격과 지속적인 위협 피드 업데이트로 조달 주기가 단축되고 자본 지출이 운영 예산으로 이전되기 때문에 급증할 것으로 예측됩니다.

현재, 에지 추론 노드와 세계 위협 인텔그래프를 공급하는 중앙 클라우드 분석을 결합한 하이브리드 아키텍처가 새로운 구현의 주류가 되고 있습니다. 벤더는 On-Premise와 퍼블릭 클라우드 영역 간에 페더레이션된 학습을 위한 안전한 컴퓨팅 엔클레이브를 가능하게 하는 한편, 정지시 학습 데이터를 암호화하는 레퍼런스 블루프린트를 미리 패키징하고 있습니다. 보안 운영 센터는 환경 간의 검색 결과를 정규화하고 워크플로가 여러 호스팅 모델에 걸쳐 있는 경우 공격자가 악용하는 가시성의 격차를 메우는 통합 대시보드에서 이점을 얻을 수 있습니다. 이러한 기능을 통해 클라우드 변종은 2030년까지 인지 보안 시장의 주요 확장 엔진으로 자리매김합니다.

인지 컨트롤이 가치를 제공하기 전에 기업은 맞춤형 데이터 파이프라인, 모델 검증 프레임워크 및 규제 매핑이 필요하기 때문에 컨설팅 및 통합 업무는 2024년 60.40%의 수익 공유를 획득했습니다. 관리형 서비스로 인한 인지 보안 시장 규모는 조직이 24시간 시스템 모니터링, 모델 재교육 및 적대적 시뮬레이션 연습을 아웃소싱하기 때문에 CAGR 28.40%를 나타낼 것으로 예측됩니다.

전문 공급자는 현재 각 고객의 진화하는 위험 프로파일에 맞게 동적 기준선을 유지하기 위해 위협 사냥부대와 MLOps 엔지니어를 번들로 제공합니다. GovCIO에 주문된 20억 달러의 NSIN 작업 주문과 같은 정부 계약은 공공 기관이 기밀 인증 요구 사항을 충족하면서 외부 전문 지식을 활용하여 취득 일정을 단축하는 방법을 보여줍니다. 상업 구매자는 이 패턴을 반영하고 예산을 인원으로부터 감지 정밀도의 서비스 수준 계약을 보장하는 성과 기반 구독으로 이동합니다. 따라서 매니지드 서비스 붐은 인지 보안 시장의 성장 궤도를 지원하는 일시적이지 않고 구조적인 현상입니다.

인지 보안 시장은 배포, 서비스(프로페셔널 서비스, 관리 서비스), 용도(인지 위협 인텔리전스, 예지보전 등), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 의료 및 생명 과학 등), 구성요소(솔루션 및 서비스), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 여전히 가장 규모가 큰 지역 클러스터이며 2024년 인지 보안 시장 점유율 35.70%를 차지했습니다. 국방부의 NSIN 태스크 주문(20억 달러)과 F-35 사이버 보안 지원 계약(1억 8,500만 달러)으로 대표되는 바와 같이, 국가 및 연방 기관은 중요 인프라를 보호하기 위해 수십억 달러의 예산을 할당합니다. 기업도 마찬가지로 복잡한 환경에 직면하고 있습니다. AI 특유의 리스크 관리 규칙이 기존의 데이터 프라이버시 법령과 나란히 등장해, 컴플라이언스의 오버헤드가 증대하는 것과 동시에, 플랫폼 벤더에 있어서 대처 가능한 지출도 확대하고 있습니다. 벤처기업의 자금조달은 여전히 윤택하며, 즉석주입시험과 자율적 레드팀 등 틈새 기능을 상업화하는 신흥기업의 파이프라인을 유지하고 있습니다. 그럼에도 불구하고 포춘 1000개 기업이 이미 1세대 AI 보안 프로그램을 실시하고 있으며, 현재는 그린필드의 전개보다 단계적인 최적화에 중점을 두고 있기 때문에 신흥지역과 비교하면 성장률은 완만합니다.

아시아태평양은 CAGR 25.66%로 가장 빠른 속도를 기록하고 있습니다. 중국, 싱가포르, 한국의 정부 프로그램은 국내외 기술을 조달하는 국가 사이버 보안 센터에 투자하면서 AI 채용을 촉진하고 있습니다. 급속한 디지털 결제 확대와 스마트 시티 배포는 방대한 양의 원격 측정을 생성하고 머신러닝 주도 방어를위한 비옥 한 데이터를 제공 할뿐만 아니라 자동 정찰을 무기로하는 사이버 범죄 조직을 유치합니다. 따라서 기업은 AI 네이티브 보안을 뒷받침하는 것이 아니라 처음부터 우선적으로 도입하여 풀 스택 플랫폼의 판매 사이클을 단축하고 있습니다. 언어의 다양성과 규제의 이질성은 통합의 장애물이지만, 하이퍼스케일러의 지역적인 실적의 확대는 인프라의 제약을 완화하고 확장 가능한 인지 컨트롤에 대한 수요를 강화하고 있습니다.

유럽에서는 EU의 AI법이 애매함을 투명성, 견고성, 데이터 거버넌스에 관한 규정적 의무로 바꾸어 꾸준히 진보하고 있습니다. 컴플라이언스 비용은 프로젝트의 복잡성을 높일 수 있지만 법률이 명확해짐에 따라 설명 가능한 AI 보안에 대한 장기 투자에 대한 이사회 수준의 승인이 촉진됩니다. 공급업체는 대시보드 및 감사 추적을 지역화하여 지역별 보고 스키마를 지원하며, 대부분은 인증된 데이터센터에서 호스팅되는 소블린 클라우드 옵션을 제공하여 국경을 넘는 이전 제한을 존중합니다. 특히 독일 제조업의 중심지나 프랑스의 항공우주 및 방위 섹터에서는 사이버 피지컬 리스크와 지적 재산권 보호의 요청이 엇갈리고 있기 때문에 도입이 진행되고 있습니다. 이러한 요인들이 합쳐져 성장률이 아시아태평양의 격렬한 페이스에 미치지 못하더라도 유럽은 인지 보안 시장의 전략적 수익의 기둥이 되고 있다는 것이 확실합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비구조화된 엔터프라이즈 데이터의 급격한 증가

- IoT/커넥티드 디바이스의 다크 데이터 급증

- 클라우드 네이티브 AI 툴체인에 의한 진입 장벽의 저하

- 오픈소스 및 클라우드 스택에 대한 사이버 위협 증가

- 시장 성장 억제요인

- AI/ML 및 사이버 분석 인력 부족

- 여러 법역에 걸친 데이터 거버넌스의 복잡성

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 배포별

- On-Premise

- 클라우드 기반

- 서비스별

- 전문 서비스

- 매니지드 서비스

- 용도별

- 인지 위협 인텔리전스

- 예측 유지보수

- 교차 조사 분석

- 자동화된 컴플라이언스 관리

- 기타 용도

- 최종 사용자 업계별

- BFSI

- 헬스케어 및 생명과학

- 소매 및 E-Commerce

- 정부 및 방위

- 통신 및 IT

- 제조

- 구성 요소별

- 솔루션

- 서비스

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Microsoft Corp.(Azure)

- Amazon Web Services Inc.

- SAP SE

- Cisco Systems Inc.

- Trend Micro Inc.

- Broadcom Inc.(Symantec)

- Darktrace plc

- McAfee LLC

- LogRhythm Inc.

- Fortinet Inc.

- SAS Institute Inc.

- Splunk Inc.

- Google LLC

- Oracle Corp.

- Micro Focus Intl.

- Dell Technologies(EMC)

- Palantir Technologies

- CrowdStrike Holdings

- SAS Institute Inc.

제7장 시장 기회와 전망

KTH 25.11.07The cognitive security market stands at USD 17.09 billion in 2025 and is forecast to reach USD 46.71 billion by 2030, translating into a robust 22.27% CAGR.

Persistent AI-enabled threats, expanding attack surfaces created by cloud adoption, and mounting regulatory scrutiny combine to fuel this growth. Enterprises invested heavily after discovering that conventional tools miss AI-specific vulnerabilities such as model poisoning, adversarial prompts, and synthetic data leakage, prompting an accelerated pivot toward advanced analytics and autonomous defense. Parallel advances in large-language-model deployments inside corporate workflows further sharpen demand, because every generative-AI rollout creates new entry points that must be continuously monitored and hardened. Vendors respond by embedding self-learning algorithms into incident-response playbooks, reducing mean time to detect and contain breaches from hours to minutes while simultaneously shrinking false-positive noise that overwhelms human analysts. These dynamics position the cognitive security market as one of the fastest-expanding segments within broader cybersecurity spending.

Global Cognitive Security Market Trends and Insights

Exponential Rise of Unstructured Enterprise Data

Massive growth in emails, collaboration files, sensor readings, and multimedia escalates both the visibility challenge and the attack surface. Cognitive engines ingest terabytes of raw logs to pinpoint deviations in user behavior, cutting false-positive alerts by 95% while surfacing stealthy lateral movements that bypass rule-based systems. However, attackers benefit from the same information richness, scraping content to craft context-aware spear-phishing campaigns. Security teams therefore integrate self-learning analytics directly into data-lakes to correlate identity, device, and network telemetry in near real time, turning previously dormant archives into actionable intelligence that enhances breach-detection accuracy. The net result is an elevated baseline for analytic depth that positions the cognitive security market for sustained expansion across all verticals.

Surge in IoT Dark Data

Industrial and consumer IoT deployments add billions of unmanaged endpoints, creating a torrent of operational telemetry that standard SIEM platforms cannot parse. Cognitive engines model baseline behavior for each device class and flag deviations such as anomalous firmware changes or unexpected east-west traffic. In energy grids and smart-factory floors, this functionality directly mitigates downtime risks while protecting life-safety systems. The security gap widens as OT networks converge with IT backbones, prompting manufacturing and utilities firms to invest in edge-resident AI analytics that operate under stringent latency constraints. Consequently, demand for scalable, device-agnostic platforms inside the cognitive security market continues to accelerate through 2030.

Scarcity of AI/ML Cyber-Analytics Talent

Demand for practitioners able to code reinforcement-learning defenses, tune prompt-shield models, and interpret threat telemetry vastly exceeds global supply. Organizations counter by outsourcing to managed-service specialists and by investing in low-code orchestration layers that let fewer engineers protect larger asset bases. Although automation handles level one triage, level two and level three escalations still require hybrid skill sets spanning mathematics, secure coding, and regulatory interpretation. The resulting wage inflation inflates project TCO, nudging some smaller firms toward consumption-based cloud subscription models instead of bespoke builds.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native AI Toolchains Democratizing Cognitive Security

- Escalating Threats on Open-Source and Cloud Stacks

- Multi-Jurisdictional Data Governance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises solutions retained 60.40% cognitive security market share in 2024 because defense agencies, financial institutions, and critical-infrastructure operators continue to mandate local data residency and air-gapped environments. However, cloud deployments are expanding at a 27.10% CAGR as hyperscalers integrate purpose-built telemetry collectors and model-integrity validation into their platforms, lowering entry cost. The cognitive security market size for cloud-based offerings is projected to rise steeply as subscription pricing and continuous threat-feed updates shorten procurement cycles and transfer capital expenditure into operating budgets.

Hybrid architectures now dominate new implementations, pairing edge inference nodes with central cloud analytics that feed global threat-intel graphs. Vendors pre-package reference blueprints that encrypt training data at rest while enabling secure compute enclaves for federated learning between on-prem and public-cloud zones. Security-operations centers benefit from unified dashboards that normalize detections across environments, closing visibility gaps that attackers exploit when workflows straddle multiple hosting models. These capabilities collectively position cloud variants as the principal expansion engine within the cognitive security market through 2030.

Consulting and integration engagements captured 60.40% revenue share in 2024 because enterprises require customized data pipelines, model-validation frameworks, and regulatory mappings before cognitive controls deliver value. The cognitive security market size attributed to managed services is forecast to grow at a 28.40% CAGR as organizations outsource round-the-clock monitoring, model retraining, and adversarial-simulation exercises.

Specialist providers now bundle threat-hunting squads with MLOps engineers to maintain dynamic baselines tuned to each client's evolving risk profile. Government contracts such as the USD 2 billion NSIN task order awarded to GovCIO illustrate how public agencies leverage external expertise to accelerate acquisition timelines while meeting classified accreditation requirements. Commercial buyers mirror this pattern, shifting budget from headcount to outcome-based subscriptions that guarantee detection-accuracy service-level agreements. The managed-services boom is therefore a structural, not temporary, phenomenon underpinning the growth trajectory of the cognitive security market.

Cognitive Security Market Segmented by Deployment, Service (Professional Services, Managed Services), Application (Cognitive Threat Intelligence, Predictive Maintenance, and More), End-User Industry (BFSI, Healthcare and Life Sciences and More), Component (Solutions and Services) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest regional cluster, holding 35.70% cognitive security market share in 2024. State and federal agencies allocate multibillion-dollar budgets to safeguard critical infrastructure, exemplified by the USD 2 billion Department of Defense NSIN task order and the USD 185 million F-35 cybersecurity support contract. Enterprises face an equally complex environment as AI-specific risk-management rules emerge alongside existing data-privacy statutes, raising compliance overhead yet simultaneously expanding addressable spend for platform vendors. Venture funding remains abundant, sustaining a pipeline of startups that commercialize niche capabilities such as prompt-injection testing and autonomous red-teaming. Nevertheless, growth rates moderate relative to emerging regions because many Fortune 1000 firms have already executed first-generation AI-security programs and now focus on incremental optimization rather than green-field rollouts.

Asia-Pacific records the fastest trajectory at a 25.66% CAGR. Government programs in China, Singapore, and South Korea promote AI adoption while investing in national cybersecurity centers that procure local and international technology. Rapid digital-payment expansion and smart-city rollouts generate enormous telemetry volumes, providing fertile data for machine-learning-driven defenses but also luring cybercriminal syndicates that weaponize automated reconnaissance. Enterprises therefore prioritize AI-native security from the outset rather than layering it later, shortening sales cycles for full-stack platforms. Linguistic diversity and regulatory heterogeneity pose integration hurdles, yet hyperscalers' growing regional footprints alleviate infrastructure constraints, reinforcing demand for scalable cognitive controls.

Europe advances steadily as the EU AI Act transforms ambiguity into prescriptive obligations around transparency, robustness, and data governance. While compliance costs elevate project complexity, the legislative clarity encourages board-level approval for long-term investments in explainable-AI security. Vendors localize dashboards and audit trails to meet region-specific reporting schemas, and many offer sovereign-cloud options hosted in accredited data centers to respect cross-border transfer restrictions. Uptake is especially strong in Germany's manufacturing heartland and France's aerospace and defense sector, where cyber-physical risks intersect with intellectual-property protection imperatives. Together these factors ensure Europe remains a strategic revenue pillar for the cognitive security market, even if growth percentages trail Asia-Pacific's breakneck pace.

- IBM Corporation

- Microsoft Corp. (Azure)

- Amazon Web Services Inc.

- SAP SE

- Cisco Systems Inc.

- Trend Micro Inc.

- Broadcom Inc. (Symantec)

- Darktrace plc

- McAfee LLC

- LogRhythm Inc.

- Fortinet Inc.

- SAS Institute Inc.

- Splunk Inc.

- Google LLC

- Oracle Corp.

- Micro Focus Intl.

- Dell Technologies (EMC)

- Palantir Technologies

- CrowdStrike Holdings

- SAS Institute Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential rise of unstructured enterprise data

- 4.2.2 Surge in IoT / connected-device dark data

- 4.2.3 Cloud-native AI toolchains lowering entry barrier

- 4.2.4 Escalating cyber-threats on open-source and cloud stacks

- 4.3 Market Restraints

- 4.3.1 Scarcity of AI/ML and cyber-analytics talent

- 4.3.2 Multi-jurisdictional data-governance complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud-Based

- 5.2 By Service

- 5.2.1 Professional Services

- 5.2.2 Managed Services

- 5.3 By Application

- 5.3.1 Cognitive Threat Intelligence

- 5.3.2 Predictive Maintenance

- 5.3.3 Cross-Investigation Analytics

- 5.3.4 Automated Compliance Management

- 5.3.5 Other Applications

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and eCommerce

- 5.4.4 Government and Defense

- 5.4.5 Telecom and IT

- 5.4.6 Manufacturing

- 5.5 By Component

- 5.5.1 Solutions

- 5.5.2 Services

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Israel

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 United Arab Emirates

- 5.6.5.1.4 Turkey

- 5.6.5.1.5 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corp. (Azure)

- 6.4.3 Amazon Web Services Inc.

- 6.4.4 SAP SE

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Trend Micro Inc.

- 6.4.7 Broadcom Inc. (Symantec)

- 6.4.8 Darktrace plc

- 6.4.9 McAfee LLC

- 6.4.10 LogRhythm Inc.

- 6.4.11 Fortinet Inc.

- 6.4.12 SAS Institute Inc.

- 6.4.13 Splunk Inc.

- 6.4.14 Google LLC

- 6.4.15 Oracle Corp.

- 6.4.16 Micro Focus Intl.

- 6.4.17 Dell Technologies (EMC)

- 6.4.18 Palantir Technologies

- 6.4.19 CrowdStrike Holdings

- 6.4.20 SAS Institute Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment