|

시장보고서

상품코드

1846256

적응광학 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Adaptive Optics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

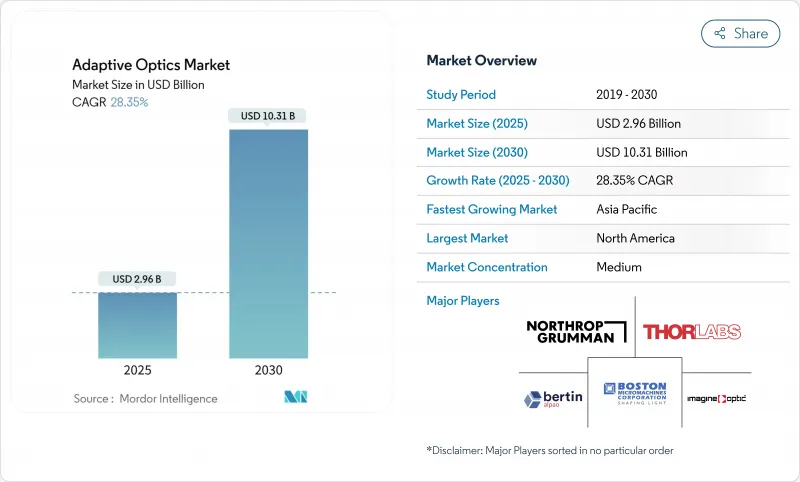

적응광학 시장 규모는 2025년에 29억 6,000만 달러, 2030년에는 103억 1,000만 달러에 이르고, CAGR 28.35%를 나타낼 것으로 예측됩니다.

수요의 원동력은 지향 에너지 프로그램에 대한 정부 지출, 서브 나노미터 정밀도의 반도체 검사 요구, AR/VR 도파로 디스플레이 등의 민생 일렉트로닉스 용도의 대두. 유럽의 대구경 망원경 업그레이드와 아시아 우주 상황 인식 프로그램의 확대가 이 기술의 관련성을 강화하고 있습니다. 차세대 제어 시스템에서 매우 중요한 머신러닝 기반 파면 재구성은 교정 대기 시간을 단축하고 상업적 매력을 넓혀줍니다. 또한 FDA 분류 변경으로 첨단 안과용 플랫폼 승인 일정이 단축되었기 때문에 적응광학 기기 시장은 망막 이미징 장치에 대한 급속한 채용으로도 혜택을 누리고 있습니다.

세계의 적응광학 시장 동향과 인사이트

고해상도 망막 이미징에 대한 적응광학계의 급속한 채용

안과 장비 제조 업체는 현재 다중 공액 적응광학 시스템을 통합하여 세포 수준의 망막 이미지를 촬영하여보다 조기 질병 감지를 가능하게하고 있습니다. FDA는 2024년 초음파 사이클로 디스트럭티브 디바이스를 클래스 III에서 클래스 II로 재분류하여 고급 이미징 플랫폼이 보다 예측 가능한 경로를 보여주었습니다. 알콘의 Unity VCS와 Unity CS의 허가는 상업적 준비가 진행 중임을 보여주며, 인공지능이 있는 파면 알고리즘은 의자 시간 교정을 줄입니다. Profundus Imaging과 같은 신흥 기업은 여러 변형 가능한 거울로 보정 시야를 넓히는 프로토타입을 개발하고 있습니다. 이러한 진보는 주요 학술 센터 이외의 클리닉 소유의 장애물을 낮추고 적응광학 시장의 건강 관리에 도달하는 것을 가속화합니다.

지향성 에너지 & 자유 공간 레이저 통신 프로그램으로의 전개

미국 국방부는 매년 10억 달러 이상을 고에너지 레이저 시스템에 투입하고 있으며, 록히드 마틴은 장거리 빔 품질을 적응광학에 의존하는 300kW 장치까지 확장하고 있습니다. 우주개발청의 증식 전투기 우주 아키텍처에서는 2029년까지 350억 달러의 예산이 짜여져 있으며, 정확한 파면 제어를 필요로 하는 레이저 크로스 링크가 내장되어 있습니다. 오타와 대학의 TAROQQO와 같은 AI 대응 난류 예측 도구는 현재 실시간으로 자유 공간 양자 채널을 개선하고 있습니다. 이러한 프로그램은 개발 사이클을 단축하고 공급망을 강화하며 군용 및 안전 통신용 적응광학 시장을 확대합니다.

높은 액추에이터 변형 미러의 높은 설비 투자액

120 x 120 액추에이터가있는 디포마블 미러는 단가가 높고 소규모 제조업체에게는 정당화하기가 어렵습니다. 게르마늄과 갈륨의 수출 규제를 포함한 공급망의 압력은 광학 기판의 원재료 가격을 상승 시켰습니다. BDNL4와 같은 대체 칼코게나이드 물질은 제한된 금속에 대한 의존도를 낮추지만 재투어가 필요하며 단기 비용이 증가합니다. 플랫 포토닉스 레이저 시장은 2024년에 230억 달러로 평가되어 공급업체의 자본 지출을 흡수하는 능력을 좁혔습니다. 이러한 요인은 가격에 민감한 수직 분야의 성장을 억제하고 적응광학 시장에 진입 희망자에게 관심을 촉구하고 있습니다.

부문 분석

파면 센서는 2024년 적응광학 시장 점유율의 38%를 차지하고 실시간 수차 데이터를 하류 제어에 공급하는 샬하르트만 어레이가 그 중심이 되었습니다. 샤크하르트만의 단순함이 비용을 낮게 억제하는 한편, 피라미드 센서가 극단적인 적응광학 천문학으로 지지를 모으고 있습니다. 제어 시스템 및 소프트웨어는 CAGR 31.44%의 성장이 예상됩니다. 시공간 가우시안 프로세스 모델은 비예측 루프에 대한 파면 위상 변동을 최대 3.5배 줄입니다. 기계적 주력 제품인 변형 가능한 미러는 MEMS 아키텍처로 전환하고 있으며, 소비자를 위한 가격대를 지원하는 기술 점유율은 42%에 달할 전망입니다. 칩 틸트 미러를 포함한 다른 구성 요소는 레이저 통신의 특수 미세 조정 작업을 지원합니다.

제어 소프트웨어는 현재 난류 조건 하에서 이득 일정을 최적화하고 대역폭을 유지하면서 오버 슛을 줄이는 향상된 학습 에이전트를 통합하고 있습니다. SPHERE의 SAXO 업그레이드로 테스트된 주파수 기반 데이터 구동 컨트롤러는 볼록 최적화를 통해 시스템 안정성을 보호합니다. 개발 회사는 모듈식 하드웨어에 AI 지원 펌웨어를 번들로 통합자 개발 사이클을 단축합니다. 예측 제어가 보급됨에 따라 제어 플랫폼을 위한 적응광학 시장 규모는 2030년까지 큰 수익 슬라이스를 획득할 것으로 예측됩니다.

방위& 보안은 2024년에 31.4%의 수익 점유율을 차지하고 레이저 빔 코히런스를 유지하기 위해 적응광학에 의존하는 국방부 프로그램에 의해 지원되었습니다. AR/VR 헤드셋이나 스마트폰 카메라가 소형 파면 변조기를 필요로 하기 때문입니다. Apple의 헤드 마운트 디스플레이는 높은 픽셀 밀도의 마이크로 OLED 패널을 보급했지만, 이는 제조 시 적응광학 테스트에 의존합니다.

산업용 제조업에서는 반도체 계측 라인에서 MEMS 미러를 활용하여 검사 스테이션에서 서브 나노미터의 편차를 측정하고 있습니다. 의료 및 생명 과학은 세포 수준의 망막 진단 플랫폼에서 기세를 늘리고 적응광학 시장을 더욱 다양화하고 있습니다. 설문 연구 및 학술은 메타서피스 기반 파면 센서와 같은 혁신을 지속적으로 개척하여 지적 재산의 안정적인 파이프라인을 확보하고 있습니다.

지역 분석

북미는 2024년 매출의 37.9%를 차지하며, 국방부의 10억 달러 지향성 에너지 예산과 NASA의 레이저 통신 이니셔티브를 중심으로 했습니다. Northrop Grumman의 Xinetics와 같은 공급업체는 납 마그네슘 - 니오브 산염의 변형 가능한 거울을 여러 군사 부서에 제공합니다. 우주개발청은 350억 달러의 아키텍처 프로그램 중에서 위성의 크로스 링크에 적응 미러를 통합하고 있습니다. 대기 왜곡에 대한 캐나다 조사는 미국 프로그램을 보완하고 북미의 적응광학 시장을 강화하고 있습니다.

아시아태평양은 CAGR 30.80%로 가장 급성장하고 있는 지역으로 일본의 우주 전략 기금이 로켓과 컨스텔레이션 프로그램을 자극하고 중국은 우주 상황 인식 위성의 광학 페이로드를 확대하고 있습니다. 중국의 원격 감지 분야는 2033년까지 550억-680억 달러로 확대될 것으로 예측되고 있으며, 정밀 광학 부품 수요가 확대되고 있습니다. JAXA의 XRISM 미션은 적응 미러에 의존하는 연 X선 센서의 검증을 실시해, 우주 탑재 기기에 있어서 지역의 능력을 나타내고 있습니다.

유럽의 대구경 망원경과 방위 연구 컨소시엄이 지속적인 주문을 견인하고 있습니다. ESO를 통한 ELT 조달은 대륙 공급업체의 장기 계약을 보장합니다. 남미와 중동, 아프리카는 지역 우주 개발 계획이 성숙하고 있기 때문에 개발 도상이지만 유망합니다. 이러한 역학을 종합하면 적응광학 시장은 단일 지역에 지나치게 의존하지 않고 다지역 성장 궤도를 유지합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 고해상도 망막 이미징에 대한 적응광학의 급속한 채용

- 미국 국방부에 의한 지향성 에너지 및 자유 공간 레이저 통신 프로그램에의 전개

- 대구경 망원경 업그레이드(ELT, TMT)가 유럽에서 수요를 가속

- 서브 나노미터 정밀도가 요구되는 상용 반도체 웨이퍼 및 EUV 마스크 검사

- AO 인핸스드 계측을 이용한 AR/VR 도파로 디스플레이 제조의 출현

- 우주 파편 추적을 위한 국가 우주 기관의 자금 조달(아시아와 중동)

- 시장 성장 억제요인

- 고액추에이터 변형가능 미러의 고액설비투자에 의한, 보다 광범위한 산업에의 채용의 제한

- 신흥 시장에서의 복잡한 클로즈드 루프 설계와 캘리브레이션의 기술 격차

- 방위 분야에 있어서 AO 탑재 광학 페이로드의 긴 인정 사이클

- 민생 그레이드 모듈(구경 5mm 미만)의 소형화의 과제

- 가치/공급망 분석

- 규제와 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

- 산업 밸류체인 분석

제5장 시장 규모와 성장 예측

- 구성 요소별

- 웨이브프론트 센서

- 변형 가능한 미러

- 제어 시스템 및 소프트웨어

- 기타(빔 익스팬더, 팁 틸트 미러)

- 최종 사용자 산업별

- 국방 및 보안

- 의료 및 생명과학

- 산업 제조

- 소비자 일렉트로닉스 브랜드 및 OEM

- 연구 및 학술기관

- 기타 최종 사용자

- 용도별

- 천문학 및 우주 관측

- 안과/망막 이미징

- 레이저 통신 및 지향성 에너지

- 반도체 검사 및 계측

- AR/VR 광학 테스트

- 기타(현미경, 자유 공간 광학 연구개발)

- 기술별

- MEMS 기반 변형 거울

- 압전(PZT) 변형 거울

- 액정 공간 광 변조기

- 자기/보이스 코일 거울

- 기타(하이브리드 및 신개념 구동 방식)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 걸프 협력 회의(GCC) 국가

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 자금 조달, 파트너십)

- 시장 점유율 분석

- 기업 프로파일

- Northrop Grumman Corp.(AOA Xinetics)

- Thorlabs Inc.

- Boston Micromachines Corp.

- ALPAO SAS

- Imagine Optics SA

- Flexible Optical BV

- Iris AO Inc.

- Phasics SA

- CILAS(ArianeGroup)

- Active Optical Systems

- Optos Plc

- AKA Optics SAS

- Trex Enterprises Corp.

- MKS Instruments Inc.(Newport)

- HOLOEYE Photonics AG

- Jenoptik AG

- Teledyne e2v

- Wavefront Dynamics LLC

- Physik Instrumente(PI)GmbH

- Sacher Lasertechnik GmbH

- Ophir Optronics Solutions Ltd.

- First Light Imaging SAS

- OptoCraft GmbH

제7장 시장 기회와 전망

KTH 25.11.10The adaptive optics market size is valued at USD 2.96 billion in 2025 and is forecast to reach USD 10.31 billion by 2030, advancing at a 28.35% CAGR.

Demand is powered by government spending on directed-energy programs, semiconductor inspection needs at sub-nanometer precision, and rising consumer electronics applications such as AR/VR waveguide displays. Large-aperture telescope upgrades in Europe and Asia's expanding space-situational-awareness programs reinforce the technology's relevance. Machine-learning-based wavefront reconstruction, pivotal in next-generation control systems, is reducing calibration latency and broadening commercial appeal. The adaptive optics market is also benefitting from rapid adoption in retinal imaging devices as FDA classification changes shorten approval timelines for advanced ophthalmic platforms.

Global Adaptive Optics Market Trends and Insights

Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging

Ophthalmic device makers now integrate multi-conjugate adaptive optics to capture cellular-level retinal images, enabling earlier disease detection. FDA reclassification of ultrasound cyclodestructive devices from Class III to Class II in 2024 signals a more predictable pathway for advanced imaging platforms. Alcon's Unity VCS and Unity CS clearances illustrate growing commercial readiness, while AI-powered wavefront algorithms reduce chair-time calibration. Start-ups such as Profundus Imaging are developing prototypes that widen corrected fields of view through multiple deformable mirrors. These advances lower ownership hurdles for clinics beyond major academic centers and accelerate the adaptive optics market's healthcare reach.

Deployment in Directed-Energy & Free-Space Laser Communication Programs

The U.S. Department of Defense channels more than USD 1 billion annually into high-energy laser systems, with Lockheed Martin scaling to 300 kW devices that rely on adaptive optics for beam quality over long distances. The Space Development Agency's Proliferated Warfighter Space Architecture budgets USD 35 billion through 2029, embedding laser cross-links that need precise wavefront control. AI-enabled turbulence-forecasting tools such as TAROQQO from the University of Ottawa now refine free-space quantum channels in real time. Together these programs shorten development cycles, reinforce supply chains, and enlarge the adaptive optics market for military and secure-communication uses.

High CapEx of High-Actuator Deformable Mirrors

Deformable mirrors with 120 X 120 actuators raise unit costs that small manufacturers struggle to justify. Supply chain pressures, including export restrictions on germanium and gallium, inflate raw-material pricing for optical substrates. Alternative chalcogenide materials, such as BDNL4, lower dependence on restricted metals but require re-tooling that adds near-term expenses. The flat photonics-laser market, valued at USD 23 billion in 2024, narrows suppliers' ability to absorb capital outlays. These factors trim growth in price-sensitive verticals and impose caution on prospective entrants to the adaptive optics market.

Other drivers and restraints analyzed in the detailed report include:

- Large-Aperture Telescope Upgrades (ELT, TMT)

- Commercial Semiconductor Wafer & EUV Mask Inspection

- Complex Closed-Loop Design & Calibration Skills Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wavefront Sensors dominated 38% of the adaptive optics market share in 2024, anchored by Shack-Hartmann arrays that feed real-time aberration data to downstream controls. Shack-Hartmann's simplicity keeps cost low, while pyramid sensors gain traction for extreme adaptive optics astronomy. Control Systems & Software are projected to grow at 31.44% CAGR; spatiotemporal Gaussian process models cut wavefront phase variance by up to 3.5X versus non-predictive loops. Deformable Mirrors, the mechanical workhorses, are shifting toward MEMS architectures with 42% technology share that supports consumer price points. Other components, including tip-tilt mirrors, address specialized fine-pointing tasks in laser communications.

Control software now embeds reinforcement-learning agents that optimize gain schedules under turbulent conditions, reducing overshoot while preserving bandwidth. Frequency-based data-driven controllers, tested on SPHERE's SAXO+ upgrade, safeguard system stability through convex optimization. Suppliers bundle AI-ready firmware within modular hardware, shortening development cycles for integrators. As predictive control proliferates, the adaptive optics market size for control platforms is forecast to capture a larger revenue slice through 2030.

Defense & Security held 31.4% revenue share in 2024, underpinned by DoD programs that depend on adaptive optics to maintain laser-beam coherence. Government purchases remain sizable, but the fastest growth comes from Consumer Electronics, which will advance at 32.50% CAGR as AR/VR headsets and smartphone cameras require compact wavefront modulators. Apple's head-mounted displays have popularized high-pixel-density micro-OLED panels that rely on adaptive optics testing during fabrication.

Industrial Manufacturing leverages MEMS mirrors in semiconductor metrology lines, with inspection stations measuring sub-nanometer deviations. Medical & Life Sciences gain momentum from cellular-level retinal diagnosis platforms, further diversifying the adaptive optics market. Research & Academia continue to pioneer innovations such as metasurface-based wavefront sensors, ensuring a steady pipeline of intellectual property.

The Adaptive Optics Market Report is Segmented by Component (Wavefront Sensors, Deformable Mirrors, and More), End-User (Defense, Medical, Industrial, Consumer Electronics, and More), Application (Astronomy, Ophthalmology, Laser Communication, Semiconductor, AR/VR, and More), Technology (MEMS DMs, Piezoelectric DMs, LC SLMs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 37.9% of 2024 revenue, anchored by the DoD's billion-dollar directed-energy budget and NASA laser-communications initiatives. Suppliers such as Northrop Grumman's Xinetics deliver lead-magnesium-niobate deformable mirrors for multiple military branches. The Space Development Agency integrates adaptive mirrors into satellite cross-links within its USD 35 billion architecture program. Canadian research on atmospheric distortion complements United States programs, jointly reinforcing the North American adaptive optics market.

Asia-Pacific is the fastest-growing region at 30.80% CAGR as Japan's Space Strategy Fund stimulates launch-vehicle and constellation programs, and China expands optical payloads for space-situational-awareness satellites. China's remote-sensing sector is projected to escalate toward USD 55-68 billion by 2033, magnifying demand for precision optics. JAXA's XRISM mission validates soft-X-ray sensors that depend on adaptive mirrors, illustrating regional competence in space-borne instrumentation.

Europe's large-aperture telescopes and defense research consortia drive sustained orders. ESO's procurements for the ELT secure long-term contracts for continental suppliers. South America and the Middle East & Africa are nascent but promising as local space programs mature, yet limited technical talent and capital budgets slow adoption relative to leading regions. Collectively, these dynamics keep the adaptive optics market on a multi-regional growth path without over-reliance on a single geography.

- Northrop Grumman Corp. (AOA Xinetics)

- Thorlabs Inc.

- Boston Micromachines Corp.

- ALPAO SAS

- Imagine Optics SA

- Flexible Optical B.V.

- Iris AO Inc.

- Phasics SA

- CILAS (ArianeGroup)

- Active Optical Systems

- Optos Plc

- AKA Optics SAS

- Trex Enterprises Corp.

- MKS Instruments Inc. (Newport)

- HOLOEYE Photonics AG

- Jenoptik AG

- Teledyne e2v

- Wavefront Dynamics LLC

- Physik Instrumente (PI) GmbH

- Sacher Lasertechnik GmbH

- Ophir Optronics Solutions Ltd.

- First Light Imaging SAS

- OptoCraft GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging in North America

- 4.2.2 Deployment in Directed-Energy and Free-Space Laser Communication Programs by U.S. DoD

- 4.2.3 Large-Aperture Telescope Upgrades (ELT, TMT) Accelerating Demand in Europe

- 4.2.4 Commercial Semiconductor Wafer and EUV Mask Inspection Requiring Sub-Nanometer Precision

- 4.2.5 Emergence of AR/VR Waveguide Display Manufacturing Using AO-Enhanced Metrology

- 4.2.6 National Space Agencies Funding for Space Debris Tracking (Asia and Middle East)

- 4.3 Market Restraints

- 4.3.1 High CapEx of High-Actuator Deformable Mirrors Limiting Wider Industrial Adoption

- 4.3.2 Complex Closed-Loop Design and Calibration Skills Gap in Emerging Markets

- 4.3.3 Long Qualification Cycles for AO-Enabled Optical Payloads in Defense Sector

- 4.3.4 Miniaturization Challenges for Consumer-Grade Modules (less than 5 mm Aperture)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Wavefront Sensors

- 5.1.2 Deformable Mirrors

- 5.1.3 Control Systems and Software

- 5.1.4 Others (Beam Expanders, Tip-Tilt Mirrors)

- 5.2 By End-User Industry

- 5.2.1 Defense and Security

- 5.2.2 Medical and Life Sciences

- 5.2.3 Industrial Manufacturing

- 5.2.4 Consumer Electronics Brands and OEMs

- 5.2.5 Research and Academia

- 5.2.6 Other End-Users

- 5.3 By Application

- 5.3.1 Astronomy and Space Observation

- 5.3.2 Ophthalmology / Retinal Imaging

- 5.3.3 Laser Communication and Directed Energy

- 5.3.4 Semiconductor Inspection and Metrology

- 5.3.5 AR/VR Optical Testing

- 5.3.6 Others (Microscopy, Free-Space Optics RandD)

- 5.4 By Technology

- 5.4.1 MEMS-Based Deformable Mirrors

- 5.4.2 Piezoelectric (PZT) Deformable Mirrors

- 5.4.3 Liquid-Crystal Spatial Light Modulators

- 5.4.4 Magnetic / Voice-Coil Mirrors

- 5.4.5 Others (Hybrid and Novel Actuation)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Gulf Co-operation Council (GCC) Countries

- 5.5.5.2 Turkey

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Northrop Grumman Corp. (AOA Xinetics)

- 6.4.2 Thorlabs Inc.

- 6.4.3 Boston Micromachines Corp.

- 6.4.4 ALPAO SAS

- 6.4.5 Imagine Optics SA

- 6.4.6 Flexible Optical B.V.

- 6.4.7 Iris AO Inc.

- 6.4.8 Phasics SA

- 6.4.9 CILAS (ArianeGroup)

- 6.4.10 Active Optical Systems

- 6.4.11 Optos Plc

- 6.4.12 AKA Optics SAS

- 6.4.13 Trex Enterprises Corp.

- 6.4.14 MKS Instruments Inc. (Newport)

- 6.4.15 HOLOEYE Photonics AG

- 6.4.16 Jenoptik AG

- 6.4.17 Teledyne e2v

- 6.4.18 Wavefront Dynamics LLC

- 6.4.19 Physik Instrumente (PI) GmbH

- 6.4.20 Sacher Lasertechnik GmbH

- 6.4.21 Ophir Optronics Solutions Ltd.

- 6.4.22 First Light Imaging SAS

- 6.4.23 OptoCraft GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment