|

시장보고서

상품코드

1846278

다한증 치료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hyperhidrosis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

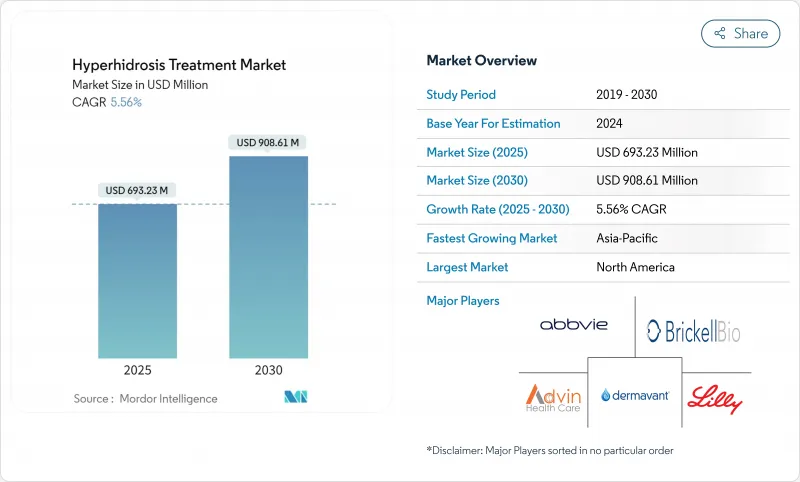

다한증 치료 시장은 2025년에 6억 9,323만 달러로 평가되고, CAGR 5.56%를 나타내 2030년에는 9억 861만 달러에 이를 전망입니다.

마이크로파 열분해, 퍼스트 인 클래스의 국소 항콜린제 브롬화 소프피로늄, 바늘을 사용하지 않는 독소 전달 시스템 등 오래 지속되는 저침습성 옵션에 대한 수요 증가가 새로운 경쟁 압력을 창출하고 있습니다. 미국과 일본의 규제 기세는 제품 출시를 가속화하는 반면 소비자에게 직접 원격 의료 플랫폼은 진단을 정상화하고 액세스를 확대하고 있습니다. 공급자는 또한 효과적인 치료가 초래하는 심리적 완화를 중심으로 제공하는 제품의 위치를 바꾸고 있으며, 이 메시지는 최근의 불안-결과 연구에 의해 지지되고 있습니다. 이러한 힘이 결합되어 다한증 치료 시장 전체의 가격 설정, 보급률, 제품 개척의 우선순위가 재구성되고 있습니다.

세계의 다한증 치료 시장 동향과 인사이트

미국과 일본에서 새로운 국소 항콜린제의 FDA 승인 파

브롬화 소프피로늄 12.45% 겔의 미국에서 2024년 승인 취득은 일본에서 2020년 5% 제제의 승인에 이어 원발성 겨드랑이 질환에 대한 신규 화학물질의 10년에 걸친 가뭄에 종지부를 찍었습니다. 시험 데이터에서 85%의 환자는 심각한 부작용 없이 임상적으로 의미 있는 발한 완화를 달성하고 처방자의 신뢰를 높였습니다. 그 이후로 외용약 파이프라인에 대한 투자가 급증하고 미국에서만 피크시 4억 7,400만 달러의 매출이 예상되기 때문에 라이벌 각사는 가격과 마케팅 메시지를 재검토할 필요가 있습니다.

침습이 낮은 마이크로파 열분해 수요 증가

마이크로파 열 용해는 후보자의 90%에 한 번의 외래 세션에서 땀샘을 제거하고 이전 두 세션의 프로토콜을 절반으로 줄이고 비용 효과를 향상시킵니다. QOL 점수는 현저하게 상승했고, 중앙값인 Dermatology Life Quality Index는 치료 후 3개월 동안 10에서 4로 떨어졌습니다. 임상의는 이 치료법을 지속적인 결과를 원하는 환자에게 보툴리눔툭신(보톡스)의 프리미엄 업그레이드로 간주합니다.

북미의 사회적 스티그마로 인한 치료의 보급과 계발 캠페인

국제다한증학회는 WHO와 동부 버지니아의과대학과의 2024년 파트너십을 통해 다한증을 정신건강문제로 재검토해 환자의 75%가 사회적 장애를 호소하고 있음에도 불구하고 임상의와 증상을 상담한 것은 불과 49%임을 강조했습니다. 이 변화는 원격의료에 의한 자기소개의 급증을 일으키고, 진단 대상자는 과거의 추정을 훨씬 넘어 확대하고 있습니다.

부문 분석

보툴리눔툭신(보톡스) A 주사는 2024년에도 가장 큰 수익원으로 지속되어 다한증 치료 시장 점유율의 32.13%를 차지했습니다. 반복 투여가 안정적인 수익을 제공하는 반면, 환자의 선호도는 내구성있는 결과를 초래하는 치료로 이동하고 있습니다. 따라서 마이크로파 온열 용해는 평균 82%의 땀 감소와 높은 만족도의 증거에 의해 뒷받침되고 CAGR 6.2%를 나타낼 전망입니다. 소프피로늄 브로마이드의 규제 녹색 빛은 국부적인 범주를 부활시키고 OTC 땀 억제제와 침습적 치료의 틈을 메우는 것을 목표로 젤, 크림 및 닦음에 대한 투자를 끌어들입니다.

마이크로파 열분해의 다한증 치료 시장 규모는 한 세션의 프로토콜이 인지 가치를 향상시킬수록 확대될 것으로 예측됩니다. 이온 삼투압 장치는 손바닥과 발바닥 질환에서 안정한 스캐폴드를 유지하며, 보다 부드러운 부작용 프로파일을 가진 경구제는 치료 알고리즘에 다시 참여하고 있습니다. 분수 라디오 주파수 마이크로니들과 무 바늘 보툴리눔스킨에 대한 초기 단계 연구는 10년후에 추가 재구성을 만들 수 있습니다.

원발성 국소 다한증은 발생률이 높고 치료 경로가 확립되어 2024년 매출의 75.35%를 차지했습니다. 환자는 일반적으로 청소년기부터 치료를 시작하고 수십년동안 치료를 계속하기 때문에 연금과 같은 수입원이됩니다. 이차성 전신성 다한증은 약물 치료와 병존 질환으로 인한 경우가 많으며 CAGR 5.9%로 가장 빠르게 성장하는 범주입니다. 전자 의료진의 프롬프트가 개선됨으로써 과도한 발한이 잠재적인 약의 부작용이라고 판단하게 되어, 노인의 폴리파머시 환자를 전문의료로 유도하고 있습니다.

정확한 분류는 2차성 질환의 유인을 제거하기 위한 전신 약물 요법과 1차성의 국소적인 사례에 대한 국소적인 기구나 외용약 등 차별화된 요법의 지침이 되고 있습니다. 그 결과, 다한증 치료 시장 규모는 확대되는 한편, 기기 제조업체는 국부에 특화된 기능을 제공하게 되고 있습니다. 노인 의료 종사자의 의식이 높아짐에 따라 2030년까지 이 분야의 기세는 지속될 것으로 예측됩니다.

지역 분석

북미는 2024년 매출의 42%를 차지했으며 견조한 진단률과 신속한 규제 당국의 승인을 받았습니다. 브롬화 소프피로늄 겔과 나트륨 패치가 2024년에 승인됨으로써, 제1선택 요법이 다양화되어, 이 지역이 기술 혁신의 발사대로서의 역할을 하고 있다고 강조되었습니다. 원격 의료 브랜드를 통해 소비자에게 적극적인 직접 광고는 지금까지 진단되지 않은 환자를 확인하고 치료 기반을 확대하고 있습니다. 보툴리눔툭신(보톡스)의 보험 적용은 여전히 양호하며 임상적으로 정당화되면 마이크로파 열 용해에도 점차 확대되고 있습니다.

유럽은 성숙하지만 환경은 확대되고 있습니다. 이온토포레시스와 보툴리눔툭신(보톡스)요법은 널리 채용되고 있으며, 글리코피로늄 브로마이드 1% 크림은 12개국에서 인가를 받아 비침습적인 선택에 대한 규제 당국의 반응을 반영하고 있습니다. 임상의가 치료법을 선택할 때, 유효한 QOL 지표를 도입하는 경우가 늘어나고, 환자 중심의 케어 모델이 강화되고 있습니다.

아시아태평양의 CAGR은 6.9%로 가장 빠르지만, 이는 일본이 일찍부터 국소 항콜린제를 채용하고 중국이 도시에서 프리미엄 케어에 주력하고 있기 때문입니다. 한국과 호주는 처방전을 가속화하는 원격약국(Telepharmacy)를 시험적으로 도입하고 있습니다. 중동과 남미는 규모가 작은 것, 개인 클리닉이 사회적·직업적인 장면에서 자신감을 요구하는 젊은층을 타겟으로 하고 있기 때문에 1자리대 중반의 견조한 성장을 기록하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미국과 일본에서의 신규 국소 항콜린제 FDA 승인 물결

- 저침습성 마이크로파 열분해 수요 증가

- 북미의 사회적 낙인에 의한 치료 보급과 계발 캠페인

- 이차성 다한증의 유병률 증가

- 소비자에게 직접 진단을 가능하게 하는 디지털 헬스 플랫폼의 성장

- 주사제 및 국소 항콜린제의 파이프라인 증가

- 시장 성장 억제요인

- 보상성 발한과 림프절제 후의 유해사례

- 높은 자본 비용과 한정된 상환

- EU와 미국에서의 글리코피로늄 크로스공급 체인 혼란

- 보툴리누스톡신의 단시간 유효성에 의해 재시술이 필요

- 가치/공급망 분석

- 규제의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액/수량)

- 치료 유형별

- 국소용 발한억제제 및 항콜린제

- 보툴리눔 독소(보톡스) A 주사

- 이온토포레시스 장치

- 마이크로웨이브 열분해술(miraDry)

- 내시경 흉부 교감신경절제술(ETS)

- 레이저 및 에너지 기반 치료

- 경구약

- 기타 치료

- 질환 유형별

- 원발성 국소 다한증

- 이차성 전신 다한증

- 다한증 부위별

- 액와부(겨드랑이)

- 손바닥

- 발바닥

- 두개 안면

- 기타(몸통, 사타구니)

- 최종 사용자별

- 병원

- 피부과 및 미용 클리닉

- 외래 수술 센터(ASC)

- 재택 케어 및 일반의약품(OTC) 채널

- 유통 채널별

- 병원 약국

- 소매 약국 및 드럭스토어

- 전자상거래

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie Inc.(Allergan)

- Sientra Inc./miraDry Inc.

- Eli Lilly and Company(Dermira)

- Merz Pharma GmbH & Co. KGaA

- Brickell Biotech Inc.

- Dermavant Sciences Inc.

- Candesant Biomedical Inc.

- Dermadry Laboratories Inc.

- SweatBlock LLC

- RA Fischer Co.

- Hidrex GmbH

- Hidroxa AB

- GlaxoSmithKline Consumer Healthcare(Certain Dri)

- Carpe Lotions LLC

- Strathspey Crown Holdings(Cynosure)

- Revance Therapeutics Inc.

- Advin Health Care

- Dermata Therapeutics Inc.

- 1315 Capital

제7장 시장 기회와 전망

KTH 25.11.10The hyperhidrosis treatment market is valued at USD 693.23 million in 2025 and on track to reach USD 908.61 million by 2030, reflecting a 5.56% CAGR.

Rising demand for long-lasting, minimally invasive options such as microwave thermolysis, the first-in-class topical anticholinergic sofpironium bromide, and needle-free toxin delivery systems is creating fresh competitive pressure. Regulatory momentum in the United States and Japan has accelerated product launches, while direct-to-consumer telehealth platforms are normalizing diagnosis and expanding access. Providers are also repositioning offerings around the psychological relief that effective therapy delivers, a message endorsed by recent anxiety-outcome studies. Together these forces are reshaping pricing, adoption rates, and product development priorities across the hyperhidrosis treatment market.

Global Hyperhidrosis Treatment Market Trends and Insights

FDA approval wave of novel topical anticholinergics in the US & Japan

The 2024 US clearance of sofpironium bromide 12.45% gel, following Japan's 2020 nod for the 5% formulation, ended a decade-long drought in new chemical entities for primary axillary disease. Trial data showed 85% of patients achieved clinically meaningful sweat reduction without serious adverse events, elevating confidence among prescribers. Investment has since surged into the topical pipeline, and peak-sales forecasts of USD 474 million in the United States alone are prompting rivals to recalibrate prices and marketing messages.

Rising demand for minimally invasive microwave thermolysis

Microwave thermolysis eliminates sweat glands in a single outpatient session for 90% of candidates, cutting the previous two-session protocol in half and improving cost-effectiveness. Quality-of-life scores rise markedly; median Dermatology Life Quality Index fell from 10 to 4 three months post-procedure . Clinicians view the modality as a premium upgrade to botulinum toxin for patients seeking lasting outcomes.

Social-stigma-driven treatment uptake & awareness campaigns in North America

The International Hyperhidrosis Society reframed hyperhidrosis as a mental-wellness issue through 2024 partnerships with WHO and Eastern Virginia Medical School, highlighting that 75% of sufferers report social impairment yet only 49% discuss symptoms with clinicians. This shift has triggered a spike in self-referrals via telehealth, expanding the diagnosed population well beyond historical estimates.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for minimally invasive microwave thermolysis

- Compensatory sweating & adverse events post-sympathectomy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botulinum toxin A injections remained the largest revenue generator in 2024, accounting for 32.13% of the hyperhidrosis treatment market share, supported by broad physician familiarity and consistent short-term efficacy. While repeat dosing drives steady revenue, patient preference is shifting toward treatments with durable outcomes. Microwave thermolysis is therefore climbing at a 6.2% CAGR, propelled by evidence of 82% average sweat reduction and high satisfaction. Regulatory green lights for sofpironium bromide have revived the topical category, attracting investment into gels, creams, and wipes that aim to bridge the gap between OTC antiperspirants and invasive procedures.

The hyperhidrosis treatment market size for microwave thermolysis is projected to widen as single-session protocols improve perceived value. Iontophoresis devices hold a stable foothold in palmar and plantar disease, while oral agents with milder side-effect profiles are re-entering treatment algorithms. Early-stage work on fractional radiofrequency microneedling and needle-free botulinum toxin may create further realignment later in the decade.

Primary focal hyperhidrosis commanded 75.35% of 2024 revenue because of its higher incidence and well-established care pathways. Patients usually begin therapy in adolescence and remain in treatment for decades, providing an annuity-like revenue stream. Secondary generalized hyperhidrosis, often triggered by medication or comorbidity, is the fastest-growing category at 5.9% CAGR. Improved electronic health record prompts now flag excessive sweating as a potential drug side effect, funneling older polypharmacy patients into specialty care.

Precise classification is guiding differentiated regimens: systemic pharmacotherapy to remove triggers in secondary disease and localized devices or topicals for primary focal cases. In turn, the hyperhidrosis treatment market size for systemic drugs is expanding while device makers tailor features to focal areas. Heightened awareness among geriatricians is expected to sustain segment momentum through 2030.

The Hyperhidrosis Treatment Market Report Segments the Industry Into by Treatment Type (Iontophoresis Devices, and More), by Disease Type (Primary Focal Hyperhidrosis, and More), Site of Hyperhidrosis (Palmar and More), End User (Hospitals, and More), Distribution Channel (Hospital Pharmacies, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 42% of 2024 revenue, anchored by robust diagnosis rates and fast regulatory approvals. The 2024 clearances of sofpironium bromide gel and the sodium patch diversified first-line therapy and underscored the region's role as a launch pad for innovation. Aggressive direct-to-consumer advertising by telehealth brands continues to identify previously undiagnosed sufferers, enlarging the treatment base. Payer coverage remains favorable for botulinum toxin and is gradually extending to microwave thermolysis when clinically justified.

Europe presents a mature yet expanding environment. Wide adoption of iontophoresis and toxin therapy persists, while glycopyrronium bromide 1% cream secured authorization across 12 countries, reflecting regulator responsiveness to non-invasive choices. Clinicians increasingly deploy validated quality-of-life indices when selecting therapy, reinforcing patient-centric care models.

Asia-Pacific books the fastest regional CAGR at 6.9%, thanks to Japan's early embrace of topical anticholinergics and China's focus on premium care in urban hubs. South Korea and Australia are piloting tele-pharmacy pathways that could accelerate prescription fulfillment. Middle East and South America, though smaller, register solid mid-single-digit growth as private clinics target youthful demographics seeking confidence in social and professional settings.

- Abbvie

- Sientra Inc. / miraDry Inc.

- Eli Lilly and Company

- Merz Pharma

- Brickell Biotech

- Dermavant Sciences Inc.

- Candesant Biomedical Inc.

- Dermadry Laboratories

- SweatBlock LLC

- RA Fischer Co.

- Hidrex GmbH

- Hidroxa AB

- GlaxoSmithKline Consumer Healthcare (Certain Dri)

- Carpe Lotions LLC

- Strathspey Crown Holdings (Cynosure)

- Revance Therapeutics

- Advin Health Care

- Dermata Therapeutics

- 1315 Capital

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FDA Approval Wave of Novel Topical Anticholinergics in the US & Japan

- 4.2.2 Rising Demand for Minimally-Invasive Microwave Thermolysis

- 4.2.3 Social-Stigma-Driven Treatment Uptake & Awareness Campaigns in North America

- 4.2.4 Increasing Prevalence of Secondary Hyperhidrosis Condition

- 4.2.5 Growth of Digital-Health Platforms Enabling Direct-to-Consumer Diagnosis

- 4.2.6 Increasing Pipeline of Injectables and Topical Anticholinergics

- 4.3 Market Restraints

- 4.3.1 Compensatory Sweating & Adverse Events Post-Sympathectomy

- 4.3.2 High Capital Cost & Limited Reimbursement

- 4.3.3 Supply Chain Disruptions of Glycopyrronium Cloths in EU & US

- 4.3.4 Short-Duration Efficacy of Botulinum Toxin Necessitating Repeat Sessions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value / Volume)

- 5.1 By Treatment Type

- 5.1.1 Topical Antiperspirants & Anticholinergics

- 5.1.2 Botulinum Toxin A Injections

- 5.1.3 Iontophoresis Devices

- 5.1.4 Microwave Thermolysis (miraDry)

- 5.1.5 Endoscopic Thoracic Sympathectomy (ETS) Surgery

- 5.1.6 Laser & Energy-based Therapies

- 5.1.7 Oral Medications

- 5.1.8 Other Treatment Types

- 5.2 By Disease Type

- 5.2.1 Primary Focal Hyperhidrosis

- 5.2.2 Secondary Generalized Hyperhidrosis

- 5.3 By Site of Hyperhidrosis

- 5.3.1 Axillary (Underarms)

- 5.3.2 Palmar (Hands)

- 5.3.3 Plantar (Feet)

- 5.3.4 Craniofacial

- 5.3.5 Others (Trunk, Groin)

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Dermatology & Aesthetic Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Homecare & OTC Channels

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies & Drug Stores

- 5.5.3 E-commerce

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc. (Allergan)

- 6.3.2 Sientra Inc. / miraDry Inc.

- 6.3.3 Eli Lilly and Company (Dermira)

- 6.3.4 Merz Pharma GmbH & Co. KGaA

- 6.3.5 Brickell Biotech Inc.

- 6.3.6 Dermavant Sciences Inc.

- 6.3.7 Candesant Biomedical Inc.

- 6.3.8 Dermadry Laboratories Inc.

- 6.3.9 SweatBlock LLC

- 6.3.10 RA Fischer Co.

- 6.3.11 Hidrex GmbH

- 6.3.12 Hidroxa AB

- 6.3.13 GlaxoSmithKline Consumer Healthcare (Certain Dri)

- 6.3.14 Carpe Lotions LLC

- 6.3.15 Strathspey Crown Holdings (Cynosure)

- 6.3.16 Revance Therapeutics Inc.

- 6.3.17 Advin Health Care

- 6.3.18 Dermata Therapeutics Inc.

- 6.3.19 1315 Capital

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment