|

시장보고서

상품코드

1846279

근접치료 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Brachytherapy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

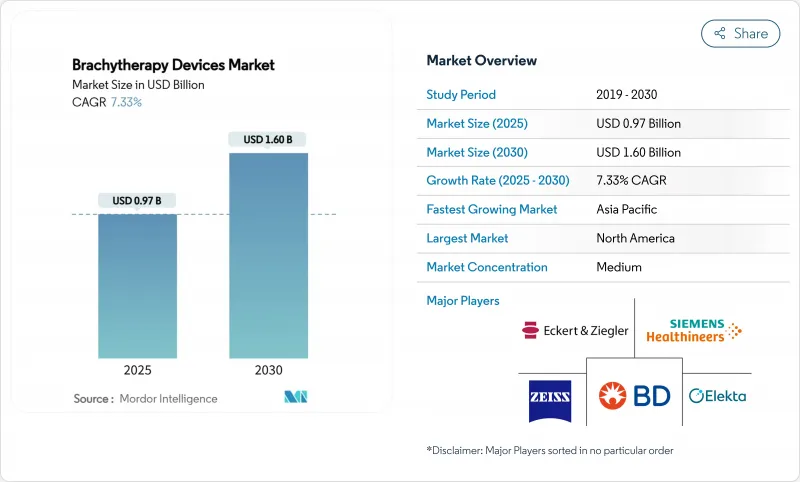

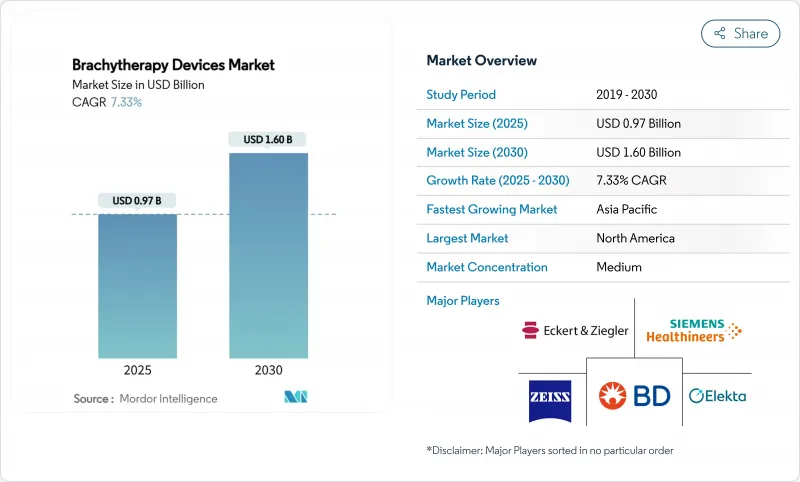

2025년 9억 7,000만 달러, 2030년 16억 달러에 이를 것으로 예상되며, 예측 기간의 CAGR은 7.33%를 나타낼 전망입니다.

암 이환율 증가, 외래 고선량률(HDR) 치료에 대한 유리한 상환, 전자 시스템의 급속한 보급이 수요 전망의 축이 되고 있습니다. 특히 아시아태평양과 라틴아메리카에서는 방사선 치료에 대한 접근을 촉진하는 정부·지불자 프로그램이 더욱 보급을 뒷받침하고 있습니다. 치료 계획을 위한 인공지능(AI)과 전자 애프터 로딩 기술의 병행 진보는 치료 시간을 단축하고, 지역 환경으로의 전개를 확대하며, 아이소토프 공급망을 보호합니다. 새로운 나노스케일 방사성 핵종 캐리어는 장기 온존의 구제 옵션을 풀어주고, 치료의 폭을 넓히고, 세계의 근접치료 기기 시장의 장치 교환 사이클을 길게 할 수 있습니다.

세계의 근접치료 기기 시장 동향과 인사이트

암에 걸린 부담 증가

세계적인 암 진단의 지속적인 증가는 정확하고 국소적인 방사선의 구조적 필요를 뒷받침합니다. 미국 암 협회는 2025년 미국에서 새롭게 204만 1,910명의 암 환자가 발생할 것으로 예측하고 있으며, 전립선암, 유방암, 부인과 암이 브라크테라피의 핵심 임상환경을 형성하고 있습니다. 노화가 진행됨에 따라 종양의사는 근접치료의 높은 적합성과 장기 온존의 이점을 높게 평가했습니다. 간세포암의 임상데이터에서는 고선량률 프로토콜을 이용한 전주효율이 98.5%로 병소확대의 기회를 나타내고 있습니다. 역학과 치료 성적의 증거가 함께 세계의 근접치료 기기 시장에서 장기적인 수요가 강화되고 있습니다.

방사선 치료 접근 확대에 대한 정부 및 지불자의 이니셔티브 증가

정책 입안자는 방사선 치료의 공평성을 공중 보건 우선 순위로 간주합니다. 인도의 National Cancer Grid는 'Karknidon' 원격 애프터 로더와 같은 국산 HDR 플랫폼을 통해 53대의 근접치료 기기의 전국 부족을 해소하고 취득 비용을 낮추고 있습니다. 미국에서는 Medicare의 Transitional Coverage for Emerging Technologies(TCET) 패스웨이를 통해 획기적인 장비의 보험 적용 결정이 가속화되고 매년 5개의 근접치료 후보가 환영받을 수 있습니다. 이러한 움직임은 환자층을 확대하고 세계의 근접치료 기기 시장의 혁신의 위험을 완화합니다.

훈련받은 브라키온 콜로지스트와 의학물리사 부족

미국 의학물리사의 15%가 10년 이내에 퇴직할 의향을 나타내고 있는 한편, 암의 이환율은 매년 2% 상승하고 있어 인재 부족이 심각화하고 있습니다. 레지던시의 책임자는 제한된 사례 수가 실용적인 임상 경험을 쌓기 위한 장벽이 되어 미래의 능력을 저하시키고 있다고 합니다. 호주 및 뉴질랜드 연수의사는 종 이식의 양이 감소하고 있다는 우려를 제기하고 기술의 감소를 예감합니다. 시뮬레이션 워크숍은 숙련도를 높이지만, 인재 파이프라인은 여전히 세계의 근접치료 기기 시장의 발판이 되고 있습니다.

부문 분석

고선량률 시스템은 2024년에 세계의 근접치료 기기 시장에서 55.51%의 점유율을 확보했습니다. 이것은 치료를 여러 번 응축하고 현대 외래 환자의 경제성에 맞는 능력을 반영합니다. ASTRO2024에서 검토된 데이터는 HDR과 낮은 선량률(LDR) 그룹 간에 전체 생존 기간의 절충을 수반하지 않는 선량 증가의 이점을 확인하였습니다. 이 분야의 리더십은 전립선과 부인과의 워크플로우에 있지만, 폐, 간, 두경부의 적응도 받아들여지고 있어 세계의 근접치료 기기 시장의 하드웨어 갱신 사이클을 지원하고 있습니다.

펄스 도즈 레이트(PDR) 기술은 2030년까지 연평균 복합 성장률(CAGR) 9.25%를 나타낼 것으로 예측되어 LDR 방사선 생물학과 HDR 인프라를 융합하여 사례 구성의 유연성을 확대합니다. AI를 활용한 계획은 모달리티 간의 질을 균일화하고 신규 채용자의 학습 곡선을 평탄화합니다. LDR은 한 번에 끝나는 편리성이 환자의 선호와 일치하는 영구 시드 임플란트에서 관련성을 유지합니다. 절차의 다양화를 통해 임상의는 종양 생물학과 선량 역학을 확실하게 일치시키고, 임상적 신뢰성을 강화하고, 치료법의 대체 위험을 완화할 수 있습니다.

씨앗은 2024년에 세계의 근접치료 기기 시장의 43.53%의 점유율을 차지하고, 수십년에 걸친 비뇨기과에서 익숙해지고 합리화된 재고 모델에 의해 지원되었습니다. 그러나 방사성선원을 다루지 않는 전자 근접치료(eBx) 시스템은 2030년까지 연평균 복합 성장률(CAGR)이 15.15%가 될 전망입니다. eBx의 세계적인 근접치료 기기 시장 규모는 특히 피부와 유방 프로토콜에서 차폐실을 사용하지 않는 조작이 소규모 병원이나 외래 센터를 이 치료법에 초대하기 때문에 상승할 것으로 예측되고 있습니다.

애플리케이터와 애프터 로더는 HDR 및 PDR 워크플로우의 기계적 백본으로, 사례 수와 선량률 혁신이 진행됨에 따라 안정적인 교체 수요를 유지하고 있습니다. 구독 모델에 번들로 제공되는 치료 계획 소프트웨어에는 계획 반복을 몇 시간에서 몇 분으로 단축하는 강화 학습 스크립트가 내장되어 통합 벤더의 끈기를 강화하고 세계의 근접치료 기기 시장의 스위칭 비용을 증가시키고 있습니다.

지역 분석

북미는 2024년에 45.32%의 점유율을 유지했는데, 이는 성숙한 보험 상환, 조기 AI 도입, 밀집한 암 의료 네트워크가 치료 건수를 유지하고 있기 때문입니다. TCET와 같은 연방정부 프로그램은 획기적인 근접치료 기기 시장 진입을 가속시키지만, 한편으로 15%의 물리학자 퇴직률이 다가오고 노동력 확보가 과제가 되고 있습니다. Varian-Ballad Health와 같은 파트너십은 장기 장비 및 서비스 계약을 통해 지역 액세스 갭을 채우는 노력을 보여줍니다. 이러한 계약을 통한 공급업체의 서비스 수입은 세계의 근접치료 기기 시장의 지역적 저력을 지원합니다.

유럽은 증거 기반 도입과 국경을 넘은 연구 협력을 통해 안정적인 성장을 이루고 있습니다. 독일, 프랑스, 영국은 MRI 가이드 하에서 적응적 근접치료의 선구자로, AngioDynamics사의 AlphaVac F18 85와 같은 CE 마크를 획득한 혁신이 급속히 보급되어 규제 예측 가능성이 강화되었습니다. EU가 지원하는 아시아와의 교육 교류는 모범 사례의 보급을 강화하고 아시아 대륙 전체에서 일관된 사용을 지원합니다. 세계의 근접치료 기기 시장은 유럽 초기 단계의 임상시험 밀도의 높이로부터 혜택을 받아 세계 구매 결정에 반영됩니다.

2030년까지 연평균 복합 성장률(CAGR)이 가장 높은 것은 아시아태평양이며 종양학의 인프라 정비가 진행될 것으로 예측됩니다. 인도는 연간 100만명 가까운 신규 암 증례를 기록하고 있으며, 자사의 HDR 플랫폼을 통해 53유닛의 근접치료 갭을 다루고 있습니다. 일본은 129대의 Ir-192 원격 애프터 로더를 보유하고 있으며, 48%의 시설이 3D계획을 채용하고 있다고 보고하고 있으며, 선진의료가 침투하고 있음을 나타내고 있습니다. 중국 지역의 장비 조달 프로그램과 중앙 진료 보상 개혁은 환자 접근을 확대하고 있지만 물리적인력 배치는 여전히 제약을 받고 있습니다. Asia Federation of Organizations for Radiation Oncology(아시아 방사선 종양학회 연합)를 통한 지역 협력은 치료의 질을 높이고 세계의 근접치료 기기 시장의 기세를 유지하는 것을 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암 이환율 증가

- 방사선치료 접근 확대를 위한 정부 및 지불자의 이니셔티브 고조

- HDR 및 전자 브럭 테라피 시스템으로의 기술 변화

- 외래 HDR 치료에 대한 상환의 추풍

- AI를 활용한 치료계획의 입안에 의한 워크플로우의 효율화

- 장기 온존 구제 치료를 가능하게 하는 나노 스케일 방사성 핵종 캐리어

- 시장 성장 억제요인

- 훈련을 받은 브라키온 콜로지스트와 의학 물리사의 부족

- 불균일한 아이소토프 공급 체인(i-192, i-125)과 수출 규제

- SBRT나 로봇 수술과의 경쟁에 의한 이용률의 저하

- 전자 브럭 테라피 장치(클래스 III)를 둘러싼 규제의 불확실성

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 기술별

- 고선량률(HDR) 근접치료 기기

- 저선량률(LDR) 근접치료 기기

- 펄스선량률(PDR) 근접치료 기기

- 제품 유형별

- 시

- 어플리케이터 및 애프터로더

- 전자 근접치료 시스템

- 소프트웨어 및 치료 계획 솔루션

- 용도별

- 전립선암

- 부인과 암

- 유방암

- 피부암

- 두경부암

- 기타

- 최종 사용자별

- 병원

- 종양 센터 및 전문 클리닉

- 외래 수술 센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Accuray Inc.

- Argon Medical Devices Inc.

- Becton, Dickinson and Company

- Carl Zeiss Meditec AG

- CIVCO Medical Solutions

- Eckert & Ziegler BEBIG

- Elekta AB

- iCAD Inc.

- Isoray Inc.

- Siemens Healthineers AG

- Theragenics Corporation

- ViewRay Inc.

- Panacea Medical Technologies

- C4 Imaging LLC

- Mevion Medical Systems

- Source Production & Equipment Co.

- IBt Bebig Belgium

- Advanced Oncology Solutions

제7장 시장 기회와 전망

KTH 25.11.10The Global brachytherapy devices market size stands at USD 0.97 billion in 2025 and is projected to reach USD 1.60 billion by 2030, reflecting a 7.33% CAGR over the forecast period.

Intensifying cancer incidence, favorable reimbursement for outpatient high-dose-rate (HDR) procedures, and rapid adoption of electronic systems anchor the demand outlook. Government and payer programs that accelerate radiotherapy access, especially in Asia-Pacific and Latin America, further support uptake. Parallel advances in artificial intelligence (AI) for treatment planning and electronic after-loading technologies shorten procedure times, expand deployment to community settings, and safeguard the isotope supply chain. Emerging nano-scale radionuclide carriers could unlock organ-sparing salvage options, broadening the therapeutic window and lengthening device replacement cycles for the Global brachytherapy devices market.

Global Brachytherapy Devices Market Trends and Insights

Growing Burden of Cancer Incidence

Persistent growth in global cancer diagnoses underpins a structural need for precise, localized radiation. The American Cancer Society projects 2,041,910 new U.S. cases in 2025, with prostate, breast, and gynecologic cancers forming the core clinical settings for brachytherapy. As aging populations swell, oncologists value brachytherapy's high conformality and organ preservation advantages. Clinical data in hepatocellular carcinoma cite 98.5% overall response rates using high-dose-rate protocols, signaling opportunity for disease-site expansion. Together, epidemiology and outcome evidence reinforce long-run demand in the Global brachytherapy devices market.

Rising Government & Payer Initiatives to Expand Radiotherapy Access

Policy makers view radiotherapy equity as public-health priority. India's National Cancer Grid is closing a national shortfall of 53 brachytherapy units through indigenous HDR platforms, such as the 'Karknidon' remote after-loader, lowering acquisition costs. In the United States, Medicare's Transitional Coverage for Emerging Technologies (TCET) pathway accelerates breakthrough device coverage decisions, potentially welcoming five brachytherapy candidates each year. These moves broaden patient pools and de-risk innovation for the Global brachytherapy devices market.

Shortage of Trained Brachy-Oncologists & Medical Physicists

Fifteen percent of U.S. medical physicists signal retirement intentions within 10 years, while cancer incidence climbs 2% annually, magnifying staffing gaps. Residency directors cite limited caseloads as barriers to braid practical exposure, curtailing future competencies. Australian and New Zealand trainees echo concerns over shrinking seed-implant volumes, foreshadowing skills attrition. While simulation workshops raise proficiency, the talent pipeline remains a rate-limiter for the Global brachytherapy devices market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift Toward HDR & Electronic Brachytherapy Systems

- Reimbursement Tail-Winds for Outpatient HDR Procedures

- Uneven Isotope Supply Chain & Export Controls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-dose-rate systems secured 55.51% share of the Global brachytherapy devices market in 2024, reflecting their capacity to condense treatment into few fractions and fit modern outpatient economics. Peer-reviewed data at ASTRO 2024 confirmed dose escalation benefits without overall-survival trade-offs across HDR and low-dose-rate (LDR) arms. The segment's leadership remains anchored in prostate and gynecologic workflows, yet lung, liver, and head-and-neck indications show acceptance, sustaining hardware refresh cycles in the Global brachytherapy devices market.

Pulsed-dose-rate (PDR) technology is projected to record 9.25% CAGR through 2030, blending LDR radiobiology with HDR infrastructure to expand case mix flexibility. AI-enabled planning equalizes quality between modalities, flattening the learning curve for new adopters. LDR retains relevance in permanent seed implants where single-session convenience aligns with patient preference. Technique diversification ensures clinicians match dose kinetics to tumor biology, reinforcing clinical confidence and mitigating modality substitution risk.

Seeds captured 43.53% share of the Global brachytherapy devices market in 2024, bolstered by decades of urology familiarity and streamlined inventory models. Yet electronic brachytherapy (eBx) systems-free of radioactive source handling-are on track for a 15.15% CAGR through 2030. The Global brachytherapy devices market size for eBx is projected to climb as unshielded-room operation invites smaller hospitals and ambulatory centers into the modality, especially for skin and breast protocols.

Applicators and after-loaders represent the mechanical backbone of HDR and PDR workflows, sustaining steady replacement demand as caseloads and dose-rate innovations evolve. Treatment-planning software, increasingly bundled in subscription models, embeds reinforcement learning scripts that cut plan iterations from hours to minutes, driving stickiness for integrated vendors and elevating switching costs across the Global brachytherapy devices market.

The Brachytherapy Devices Market Report is Segmented by Technique (High Dose Rate (HDR) Brachytherapy Devices, and More), Product Type (Seeds, Applicators & Afterloaders, and More), Application (Gynecologic Cancer, Prostate Cancer, Breast Cancer, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 45.32% share in 2024 as mature reimbursement, early AI adoption, and a dense cancer-care network sustain procedure volumes. Federal programs such as TCET speed market access for breakthrough brachytherapy devices, while a looming 15% physicist retirement rate challenges workforce capacity. Partnerships like Varian-Ballad Health illustrate efforts to bridge rural access gaps via long-term equipment and service contracts. Vendor service revenues from these deals underpin regional resilience for the Global brachytherapy devices market.

Europe delivers steady growth through evidence-based adoption and cross-border research collaborations. Germany, France, and the United Kingdom pioneer MRI-guided adaptive brachytherapy, while CE-marked innovations such as AngioDynamics' AlphaVac F18 85 gain rapid uptake, reinforcing regulatory predictability. EU-backed training exchanges with Asia bolster best-practice dissemination and support consistent utilization across the continent. The Global brachytherapy devices market benefits from Europe's early-phase clinical trial density, informing global purchasing decisions.

Asia-Pacific will chart the highest 9.61% CAGR through 2030 as oncology infrastructure scales. India records nearly 1 million new cancer cases annually and addresses a 53-unit brachytherapy gap through indigenous HDR platforms. Japan hosts 129 Ir-192 remote after-loaders and reports 48% of centers employing 3D planning, underscoring advanced practice penetration. China's provincial equipment procurement programs and central reimbursement reforms are expanding patient access, but physics staffing remains constrained. Regional collaboration via the Federation of Asian Organizations for Radiation Oncology aims to elevate treatment quality, sustaining momentum for the Global brachytherapy devices market.

- Accuray

- Argon Medical Devices

- Beckton Dickinson

- Carl Zeiss

- CIVCO Medical solutions

- Eckert & Ziegler

- Elekta

- iCAD Inc.

- IsoRay

- Siemens Healthineers

- Theragenics

- ViewRay Inc.

- Panacea Medical Technologies

- C4 Imaging LLC

- Mevion Medical Systems

- Source Production & Equipment Co.

- IBt Bebig Belgium

- Advanced Oncology Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden Of Cancer Incidence

- 4.2.2 Rising Government & Payer Initiatives To Expand Radiotherapy Access

- 4.2.3 Technological Shift Toward HDR & Electronic Brachytherapy Systems

- 4.2.4 Reimbursement Tail-Winds For Outpatient HDR Procedures

- 4.2.5 AI-Driven Treatment-Planning Improving Workflow Efficiency

- 4.2.6 Nano-Scale Radionuclide Carriers Enabling Organ-Sparing Salvage Therapy

- 4.3 Market Restraints

- 4.3.1 Shortage Of Trained Brachy-Oncologists & Medical Physicists

- 4.3.2 Uneven Isotope Supply Chain (Ir-192, I-125) & Export Controls

- 4.3.3 Declining Utilization Amid Competition From SBRT & Robotic Surgery

- 4.3.4 Regulatory Uncertainty Around Electronic Brachytherapy Devices (Class III)

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technique

- 5.1.1 High Dose Rate (HDR) Brachytherapy Devices

- 5.1.2 Low Dose Rate (LDR) Brachytherapy Devices

- 5.1.3 Pulsed Dose Rate (PDR) Brachytherapy Devices

- 5.2 By Product Type

- 5.2.1 Seeds

- 5.2.2 Applicators & Afterloaders

- 5.2.3 Electronic Brachytherapy Systems

- 5.2.4 Software & Treatment-Planning Solutions

- 5.3 By Application

- 5.3.1 Prostate Cancer

- 5.3.2 Gynecologic Cancer

- 5.3.3 Breast Cancer

- 5.3.4 Skin Cancer

- 5.3.5 Head & Neck Cancer

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Oncology Centers & Specialty Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Accuray Inc.

- 6.3.2 Argon Medical Devices Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Carl Zeiss Meditec AG

- 6.3.5 CIVCO Medical Solutions

- 6.3.6 Eckert & Ziegler BEBIG

- 6.3.7 Elekta AB

- 6.3.8 iCAD Inc.

- 6.3.9 Isoray Inc.

- 6.3.10 Siemens Healthineers AG

- 6.3.11 Theragenics Corporation

- 6.3.12 ViewRay Inc.

- 6.3.13 Panacea Medical Technologies

- 6.3.14 C4 Imaging LLC

- 6.3.15 Mevion Medical Systems

- 6.3.16 Source Production & Equipment Co.

- 6.3.17 IBt Bebig Belgium

- 6.3.18 Advanced Oncology Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment