|

시장보고서

상품코드

1846281

관절통 주사 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Joint Pain Injections - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

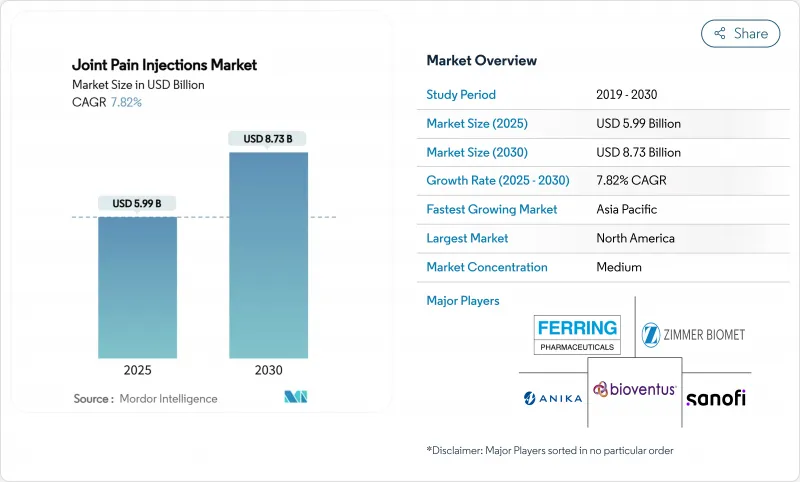

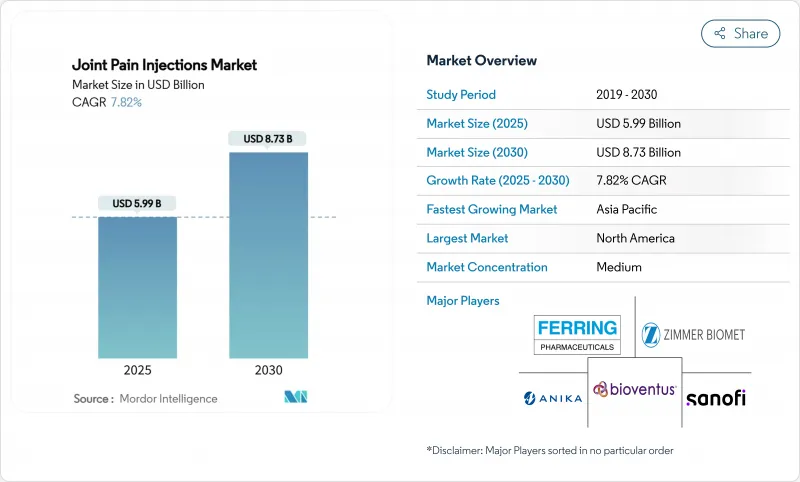

관절통 주사 시장 규모는 2025년에 59억 9,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 7.82%로, 2030년에는 87억 3,000만 달러에 이를 것으로 예상됩니다.

이 성장은 골관절염의 유병률 급증, 재생 의료에 대한 상환 확대, 합병증 발생률을 낮추는 영상 유도로 치료의 꾸준한 개선과 일치합니다. 히알루론산(HA)은 여전히 중심적인 치료법이지만, 혈소판이 풍부한 혈장(PRP) 및 기타 자기생물학적 제형은 지불자가 보험 적용을 공식화함에 따라 실험적 치료에서 주류 치료로 전환하고 있습니다. 치료 환경에서는 외래 수술 센터(ASC)가 40-60% 낮은 에피소드 비용으로 병원에서 수술 건수를 탈취하고 있으며, 또한 AI화된 초음파가 패스트 패스 주입의 정확도를 90% 이상으로 밀어 올리고 있습니다. 이러한 힘이 결합되어 의자 시간을 최적화하고 관절 치환술을 지연시키는 단일 용량 또는 3주기 요법으로 의사를 향하게 하여 환자 만족도와 의료 시스템 마진을 모두 향상시킵니다.

세계의 관절통 주사 시장 동향과 인사이트

골관절염 증가와 노화

세계 골관절염 환자 수는 15-64세이며, 일하는 성인의 생산성을 유지하기 위한 저침습적 개입에 자금을 제공하도록 지불자에게 직접적인 압력을 가하고 있습니다. 일본은 10만명당 1만 2,610.12례로 유병률이 높은 편에 위치하고 있으며, 선진 아시아 전체의 치료 수요의 지표가 되고 있습니다. 폐경 후 여성은 2045년까지 절반 가까이 골관절염을 일으킬 것으로 예상되며 치료량 증가를 견인하고 있습니다. 이러한 역학은 인공 관절 치환술을 연기하거나 회피하고 노동 참여를 유지하는 주사 요법에 장기적인 유예를 가져옵니다.

관절 내 보충 요법(HA)의 가속화 된 보급

HA 단일 주사 프로토콜은 다중 주사 요법의 효능에 필적하는 반면, 경과 관찰 횟수를 줄이고 시스템 사용 및 환자 이동 비용을 절감합니다. 한국의 15만명의 수혜자를 분석한 결과, 단회 투여 후 인공 슬관절 전치환술의 위험은 미치료의 코호트에 비해 44% 낮음을 나타내며 지불측의 신뢰가 높아졌습니다. BD는 프리필러블 주사기의 생산량을 7배로 늘려 예상 수요를 충족했습니다. 미국, 독일, 일본에서는 공급자가 적은 약속을 획득함으로써 포뮬러리에 통합이 가속화되어 관절통 주사 시장에 중기적으로 긍정적인 호를 그립니다.

보험 가입하지 않은 환자에서 고액의 자기 부담액

임상적 가치 논쟁에 근거한 관절내 보충요법의 보험 적용 거부로 인해 일부 미국 환자들은 주사 1회당 1,100-1,800달러의 전액 부담을 강요하고 있습니다. Cigna사는 정형외과적 줄기세포 치료를 '의료상 필요하지 않다'고 분류하고 있습니다. 국제적으로도 많은 신흥 시장의 납부자는 수술에는 보험이 적용되지만 생물학적 제제의 주사에는 보험이 적용되지 않고 임상적 필요성에도 불구하고 그 이용을 제한하고 있습니다. 명확한 비용 효율적인 데이터가 공공 보험 규칙을 만드는 데 영향을 미칠 때까지 자기 부담은 계속 보험 도입을 억제하는 것으로 보입니다.

부문 분석

히알루론산의 관절통 주사 시장 규모는 2024년 총 매출의 48.18%에 해당했습니다. 장기적인 안전성, 광범위한 지불자에게 받아 들여지고, 단일 투여로 사용이 증가함에 따라, 히알루 론산은 무릎 관절과 발 관절의 적응증으로 정착하고 있습니다. PRP의 수익 예측은 CAGR 9.01%로 무작위화 연구가 12개월 후 WOMAC와 VAS 점수의 우위성을 뒷받침함으로써 견인력을 늘리고 있습니다.

HA와 콜라겐 트리펩티드 또는 링커를 결합한 조합 제품은 심각한 골관절염 환자에게 호소하여 선택의 폭을 넓힐 수 있습니다. 그러나 Medicare & Medicaid Services(메디케어 및 메디케이드 서비스 센터)가 2024년에 태반 생물학적 제제의 보험 적용 제외를 결정함으로써 가까운 미래의 확대 노선은 좁아졌습니다. 예측 기간 동안, 입증된 효능의 끝점과 지불자의 무결성으로부터, PRP는 관절통 주사 시장에서의 제1선택의 지위로부터 완전히 이탈하지 않고, HA의 우위성을 깎아 갈 것이라고 생각됩니다.

단일 사이클 요법은 2024년 시장 가치의 58.63%를 차지했으며, 이는 의사가 한 번에 완료하는 복용의 편의성을 받아들였기 때문입니다. 현재는 3회의 PRP 주사가 단회 투여보다 통계적으로 큰 통증 완화를 초래한다는 근거가 나타나고, 이 부문의 2030년까지의 CAGR이 12.39%가 되는 근거가 되고 있습니다.

5사이클 프로그램은 세 번째 투여로 효과가 두드러지기 때문에 여전히 심각한 경우에 국한되어 있습니다. 따라서 제조업체는 3사이클용 멀티 챔버 키트 등 포장의 설계를 재검토하고, 조제 실수를 없애고, 준비 시간을 단축함으로써 관절통 주사 시장에서의 중간 정도의 투여 횟수의 성장을 뒷받침하고 있습니다.

지역 분석

북미는 2024년 매출의 36.74%를 차지하며, 메디케어 어드밴티지가 특정 CPT 코드로 PRP를 환불하고, 고용주의 MSK 프로그램이 회원 1인당 월평균 52달러를 지불하는 미국이 그 중심이 되었습니다. 캐나다의 단일 지불 모델은 더 이른 병기의 HA에 자금을 제공하기 시작했으며 8%의 기술 성장에 박차를 가하고 있습니다. 멕시코는 잠재적인 수요를 보여주지만, 여전히 불균일한 장비 등록 일정과 자기 부담의 장벽에 시달리고 단기적인 섭취를 제한하고 있습니다.

유럽은 HA 주사기의 안전 기준을 명확히 하는 의료기기 규제의 동조의 혜택을 받고 있습니다. 독일과 프랑스는 견고한 외래 환자 네트워크를 통해 지역 수술 건수를 홍보하는 반면 영국의 국민 보건 서비스는 상환을 기능적 결과 임계 값으로 연결하는 위험 공유 계약을 시험적으로 도입했습니다. 스페인과 이탈리아와 같은 남유럽 국가들은 AI 가이드 하의 초음파 검사를 지방 클리닉으로 확대하여 접근성을 높입니다.

아시아태평양은 CAGR 11.13%로 가장 급성장하고 있는 지역으로 일본의 뛰어난 변형성 관절증의 부담과 확립된 이미지 인프라가 뒷받침하고 있습니다. 중국의 국가 의약품 감독 관리국은 150일로 장비 승인 일정을 단축하고 단일 용량 HA 브랜드 시장 진입을 가속화하고 있습니다. 호주, 인도, 한국은 ASC 건설에 많은 투자를 하고 있으며 미국의 진료 패턴을 반영하고 치료 능력을 높이고 있습니다. 아시아 아시아 시장은 정부가 지원하는 원격 초음파 프로그램에 의한 조기 도입 행동을 보여주며, 새로운 주입 방식의 보급 곡선을 압축할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 골관절염의 이환율 증가와 인구의 고령화

- 단회투여 관절내 보충요법(HA)의 가속적 보급

- PRP 및 재생요법에 대한 지불자의 지지 확대

- 통증 중심의 외래 수술 센터(ASC)의 급증

- 진찰실내에서의 정밀도를 높이는 AI 주도의 초음파 검사 등장

- 고용주가 자금 제공하는 MSK 이니셔티브가 주사의 이용을 촉진

- 시장 성장 억제요인

- 보험 미가입층에 있어서 환자의 높은 자기 부담액

- 진료 보수와 수속 코딩의 편차

- 적응외의 스테로이드 사용을 둘러싼 임상적 우려

- 대규모 페인클리닉의 규제 감독

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(단위 : 달러)

- 주사 유형별

- 스테로이드 관절 주사

- 히알루론산(HA) 주사

- 다혈소판 혈장(PRP) 주사

- 태반 조직 매트릭스(PTM) 및 중간엽 줄기세포(MSC) 주사

- 기타 생물학적/복합 주사

- 주사 사이클별

- 단일 주기

- 3회 주기

- 5회 주기

- 용도별

- 무릎 및 발목

- 어깨 및 팔꿈치

- 고관절

- 척추 관절면 및 천장관절

- 기타 소관절

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 정형외과/통증 클리닉

- 스포츠 의학 센터

- 재택치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Anika Therapeutics

- Bioventus

- Ferring Pharmaceuticals

- Sanofi

- Pfizer

- Eli Lilly

- Flexion Therapeutics

- Teva Pharmaceuticals

- Zimmer Biomet

- Seikagaku Corporation

- Arthrex

- Stryker Corporation

- Sequent Scientific

- Seaspine Holdings

- Chugai Pharma

- Sequoia Medical

- Meda AB

- LG Life Science

- Terumo BCT

- Johnson & Johnson(DePuy Synthes)

제7장 시장 기회와 전망

KTH 25.11.10The Joint Pain Injections Market size is estimated at USD 5.99 billion in 2025, and is expected to reach USD 8.73 billion by 2030, at a CAGR of 7.82% during the forecast period (2025-2030).

This growth aligns with a sharp rise in osteoarthritis prevalence, wider reimbursement for regenerative medicine, and steady improvements in image-guided delivery that lower complication rates. Hyaluronic acid (HA) remains the anchor therapy, yet platelet-rich plasma (PRP) and other autologous biologics are moving from experimental status to mainstream care as payers formalize coverage. Within care settings, ambulatory surgery centers (ASCs) are capturing procedure volume from hospitals thanks to 40-60% lower episode costs, while AI-enabled ultrasound drives first-pass injection accuracy above 90%. Collectively, these forces push physicians toward single-dose or three-cycle regimens that optimize chair time and delay joint-replacement surgery, improving both patient satisfaction and health-system margins.

Global Joint Pain Injections Market Trends and Insights

Increasing Osteoarthritis Incidence and Aging Population

Global osteoarthritis cases among people aged 15-64 exerting direct pressure on payers to finance minimally invasive interventions that keep working adults productive. Japan sits at the high end of prevalence with 12,610.12 cases per 100,000, an indicator of treatment demand across industrialized Asia. Post-menopausal women are driving incremental volume: nearly one-half are projected to develop osteoarthritis by 2045. These dynamics create a long-duration runway for injection therapies that defer or avoid joint replacement and maintain labor participation.

Accelerated Uptake of Single-Dose Viscosupplementation (HA)

Single-injection HA protocols cut follow-up visits while matching the efficacy of multi-injection regimens, reducing system utilization and patient travel costs. Analysis of 150,000 Korean beneficiaries showed a 44% lower total knee arthroplasty risk after single doses versus untreated cohorts, bolstering payer confidence. Industrial response is robust; BD lifted prefillable-syringe output sevenfold to satisfy anticipated demand. The operational win for providers fewer appointments has accelerated formulary placement in the United States, Germany and Japan, setting a medium-term positive arc for the joint pain injections market.

High Patient Out-of-Pocket Costs in Uninsured Segments

Coverage denials for viscosupplementation based on contested clinical value have forced some US patients to absorb the full USD 1,100-USD 1,800 per injection episode. Cigna still classifies orthopedic stem-cell therapies as "not medically necessary," creating uneven benefit structures that suppress uptake. Internationally, many emerging-market payers reimburse surgery but not biologic injections, limiting access despite clinical need. Until definitive cost-effectiveness data influence public insurance rule-making, out-of-pocket exposure will continue to curb uptake.

Other drivers and restraints analyzed in the detailed report include:

- Wider Payer Support for PRP and Regenerative Therapies

- Proliferation of Pain-Centric Ambulatory Surgery Centers (ASCs)

- Variability in Reimbursement and Procedural Coding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The joint pain injections market size for hyaluronic acid stood equal to 48.18% of total revenue in 2024. Long-term safety, broad payer acceptance, and rising single-dose use keep HA entrenched across knee and ankle indications. PRP revenue is forecasted for a 9.01% CAGR, gaining traction as randomized studies corroborate superior WOMAC and VAS scores at 12 months.

Combination products that merge HA with collagen tripeptides or linkers appeal to severe osteoarthritis patients and could widen choice. However, the Centers for Medicare & Medicaid Services' 2024 non-coverage determination for placental biologics narrows near-term expansion pathways. Over the forecast window, proven efficacy endpoints and payer alignment suggest PRP will chip away at HA's dominance without dislodging it entirely from first-line status in the joint pain injections market.

Single-cycle regimens represented 58.63% of market value in 2024 as physicians embraced the convenience of one-and-done dosing. Evidence now shows three PRP injections deliver statistically greater pain relief than a single dose, forming the rationale for a 12.39% CAGR through 2030 for this segment.

Five-cycle programs remain confined to severe cases because the incremental benefit plateaus after the third dose; consequently, payer willingness to reimburse beyond three sessions is waning. Manufacturers are therefore redesigning packaging-multi-chamber kits for three cycles-to remove compounding errors and shorten prep time, a move that reinforces the growth of mid-range dosing frequencies within the joint pain injections market.

The Joint Pain Injections Market Report is Segmented by Injection Type (Steroid Joint Injections, Hyaluronic Acid Injections, and More), Injection Cycle (Single-Cycle, Three-Cycle, Five-Cycle), Application (Knee & Ankle, Shoulder & Elbow, and More), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 36.74% of 2024 sales, anchored by the United States where Medicare Advantage now reimburses PRP under specified CPT codes and employer MSK programs average USD 52 per member per month. Canada's single-payer model has begun funding HA in earlier disease stages, spurring 8% procedural growth. Mexico shows latent demand but still contends with uneven device registration timelines and out-of-pocket barriers, limiting near-term uptake.

Europe benefits from synchronized Medical Device Regulation that clarifies safety benchmarks for HA syringes. Germany and France drive regional procedure volume through robust outpatient networks, while the United Kingdom's National Health Service pilots risk-share contracts tying reimbursement to functional-outcome thresholds. Southern European countries such as Spain and Italy are scaling AI-guided ultrasound to rural clinics, boosting accessibility.

Asia-Pacific is the fastest-growing territory at 11.13% CAGR, propelled by Japan's exceptional osteoarthritis burden and well-established imaging infrastructure. China's National Medical Products Administration has slashed device approval timelines to 150 days, accelerating market entry for single-dose HA brands. Australia, India and South Korea invest heavily in ASC construction, mirroring US practice patterns and unlocking procedural capacity. Rest-of-Asia markets exhibit early-adoption behavior with government-backed tele-ultrasound programs that may compress the diffusion curve for newer injection modalities.

- Anika Therapeutics

- Bioventus

- Ferring Pharmaceuticals

- Sanofi

- Pfizer

- Eli Lilly and Company

- Flexion Therapeutics

- Teva Pharmaceutical Industries

- Zimmer Biomet

- Seikagaku

- Arthrex

- Stryker

- Sequent Scientific

- Seaspine Holdings

- Chugai Pharma

- Sequoia Medical

- Meda AB

- LG Life Science

- Terumo

- Johnson & Johnson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Osteoarthritis Incidence and Aging Population

- 4.2.2 Accelerated Uptake of Single-Dose Viscosupplementation (HA)

- 4.2.3 Wider Payer Support for PRP and Regenerative Therapies

- 4.2.4 Proliferation of Pain-Centric Ambulatory Surgery Centers (ASCs)

- 4.2.5 Emergence of AI-Driven Ultrasound for In-Office Precision

- 4.2.6 Employer-Funded MSK Initiatives Steering Utilization of Injections

- 4.3 Market Restraints

- 4.3.1 High Patient Out-of-Pocket Costs in Uninsured Segments

- 4.3.2 Variability in Reimbursement and Procedural Coding

- 4.3.3 Clinical Concerns Surrounding Off-Label Steroid Usage

- 4.3.4 Regulatory Oversight of High-Volume Pain Clinics

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Injection Type

- 5.1.1 Steroid Joint Injections

- 5.1.2 Hyaluronic Acid (HA) Injections

- 5.1.3 Platelet-Rich Plasma (PRP) Injections

- 5.1.4 Placental Tissue Matrix (PTM) & MSC Injections

- 5.1.5 Other Biologic / Combination Injections

- 5.2 By Injection Cycle

- 5.2.1 Single-cycle

- 5.2.2 Three-cycle

- 5.2.3 Five-cycle

- 5.3 By Application

- 5.3.1 Knee & Ankle

- 5.3.2 Shoulder & Elbow

- 5.3.3 Hip Joint

- 5.3.4 Spinal Facet & SI Joints

- 5.3.5 Other Small Joints

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers (ASCs)

- 5.4.3 Orthopedic / Pain Clinics

- 5.4.4 Sports Medicine Centers

- 5.4.5 Home-Care Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Anika Therapeutics

- 6.3.2 Bioventus

- 6.3.3 Ferring Pharmaceuticals

- 6.3.4 Sanofi

- 6.3.5 Pfizer

- 6.3.6 Eli Lilly

- 6.3.7 Flexion Therapeutics

- 6.3.8 Teva Pharmaceuticals

- 6.3.9 Zimmer Biomet

- 6.3.10 Seikagaku Corporation

- 6.3.11 Arthrex

- 6.3.12 Stryker Corporation

- 6.3.13 Sequent Scientific

- 6.3.14 Seaspine Holdings

- 6.3.15 Chugai Pharma

- 6.3.16 Sequoia Medical

- 6.3.17 Meda AB

- 6.3.18 LG Life Science

- 6.3.19 Terumo BCT

- 6.3.20 Johnson & Johnson (DePuy Synthes)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment