|

시장보고서

상품코드

1846287

ELISpot 및 FluoroSpot 어세이 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)ELISpot And FluoroSpot Assay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

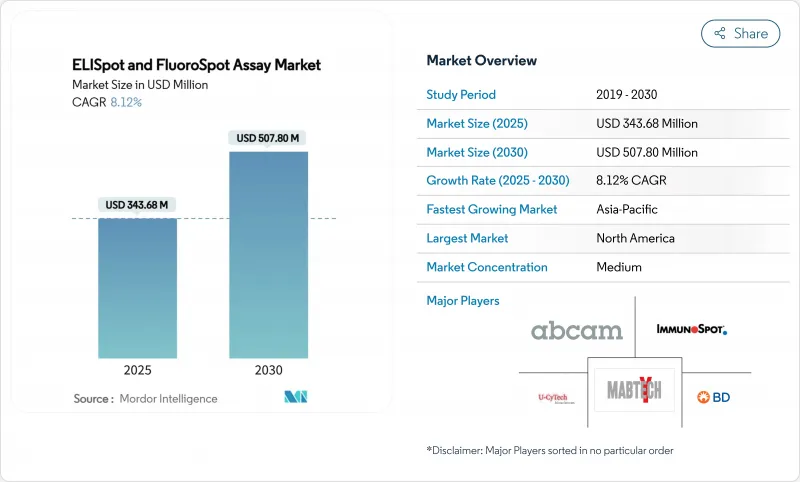

2025년 ELISpot 및 FluoroSpot 어세이 시장 규모는 3억 4,368만 달러로, 2030년에는 CAGR 8.12%로 5억 780만 달러로 확대될 것으로 예측됩니다. 감염증 진단, 백신 개척, 세포 치료 품질 관리 등에서 고감도 세포 면역 측정에 대한 수요가 가속화되고 있습니다.

COVID-19 이후의 백신 파이프라인 강화, 생물제제 승인을 위한 T세포 분석의 임상 채용 확대, 오픈 아키텍처 하드웨어의 꾸준한 비용 저하가 함께 성장세는 힘차게 유지되고 있습니다. 병원 실험실은 기능적 면역 모니터링 패널을 표준화하고 연구 기관은 대량의 분석 작업을 전문 CRO에 위탁하고 규제 당국은 차세대 면역 요법의 승인 패키지에 T 세포 기능 지표를 통합하려고합니다. 자동 이미지 캡처, 머신러닝 기반 스팟 카운팅, 마이크로플루이딕스 칩 포맷 등의 병렬 발전으로 연구실 워크플로우가 재구성되어 세계 액세스가 확대되고 있습니다. 경쟁 역학은 완만하게 남아 있으며, 기존의 분석 리더는 ELISpot 및 FluoroSpot 어세이 시장을 POC(Point-of-Care) 설정으로 밀어 올리는 AI를 강화한 분석 및 휴대용 장치를 제공하는 신규 참가자를 직면하고 있습니다.

세계의 ELISpot 및 FluoroSpot 어세이 시장 동향 및 인사이트

만성·감염증 이환율 상승

결핵, HIV, 바이러스성 간염, 암 환자 수 증가가 정확한 세포성 면역 모니터링 수요를 밀어 올리고 있습니다. T-SPOT.TB 검사는 현재 감도 99%, 특이도 94%로 성장을 지속하고, 기존의 방법을 능가하며 ELISpot 기술을 최전선 진단제로 확고하게 하고 있습니다. 2025년에 FDA가 자동화된 T-SPOT 대응 액체 처리 워크스테이션을 인가함으로써 임상에서의 사용은 더욱 확실해졌습니다. 종양 센터는 체크포인트 억제제 투여에 대한 지침인 새로운 항원 특이적 반응을 추적하기 위해 인터페론-Y 및 IL-2 ELISpot 패널을 일상적으로 사용합니다. WHO의 권고는 높은 부담 지역에서 고품질의 진단제에 대한 광범위한 접근을 요구하고 있으며 ELISpot 및 FluoroSpot 어세이 시장의 확대와 일치합니다. 감염의 위협과 함께 비감염성 질환의 유행이 증가하는 동안, 표준화된 ELISpot 워크플로우의 임상으로의 광범위한 도입은 지속적인 성장의 기둥이 될 것입니다.

COVID-19 후 백신 파이프라인의 급속한 확장

백신 개발자들은 항체 중심의 엔드포인트에서 세포 면역에 초점을 맞추었습니다. BARDA가 후원하는 차세대 COVID-19 백신의 2b 상 디자인은 보다 광범위하고 지속적인 방어를 입증하기 위해 T 세포 분석을 명확하게 통합합니다. 동일한 요건은 현재 주식 특이적인 한계를 극복하려는 계절성 독감 프로그램에도 채택되고 있습니다. 생물 제제 평가 연구센터는 2024년에 승인된 17개의 생물 제제 라이선스가 기능적 면역 데이터를 필요로 한다고 보고했으며, 규제 당국의 신청 서류에서 분석법의 이용을 확고히 했습니다. 그 결과, CRO와 사내 연구소는 이종 계통 간의 교차 반응성 면역을 정량화하는 멀티플렉스 리더를 도입함으로써 ELISpot 및 FluoroSpot 어세이 시장을 확대하고 있습니다. 보존된 에피토프를 표적으로 하는 보편적인 백신 연구는 비색 ELISA에서 밝혀지지 않은 다기능 T 세포 출력을 포획할 필요성을 더욱 강화하고 있습니다.

대체 고 파라미터 유동 세포 계측 및 CyTOF 플랫폼 가용성

45색 풀스펙트럼 세포측정법과 질량세포계측법은 복잡한 면역 랜드스케이프를 단일 세포 해상도로 그릴 수 있으며, 이러한 플랫폼은 깊은 표현형 분석이 기능 판독을 초과할 때 신뢰할 수 있는 대체물로 자리매김합니다. 33 마커 CyTOF와 스펙트럼 흐름 패널을 비교한 연구는 전체 임상 샘플의 면역 서브세트 정량에서 높은 일치성을 보였습니다. 이미 사이토미터를 소유한 실험실은 ELISpot 리더를 별도로 구입하는 대신 초고 파라미터 구성으로 업그레이드할 수 있어 장비 수요 증가를 억제할 수 있습니다. ELISpot은 낮은 빈도의 기능적 반응을 감지하는 이점을 유지하지만 기술 중복은 대규모 참조 센터에서 조달 검토를 격화시킬 것으로 보입니다.

부문 분석

2024년 매출은 1억 8,730만 달러로, 분석 키트가 총 지출의 절반 이상을 차지했습니다. 검사실은 각 검사마다 이러한 소모품을 재주문하여 안정적인 보충 스트림을 확보하고 있습니다. 분석기 수요는 베이스가 작고 자동화와 AI 분석이 높은 처리량 환경에서 일상적으로 이루어지면서 CAGR 14.25%로 키트를 웃도는 것으로 예측되고 있습니다. 지역 클리닉에서 결핵 스크리닝 프로그램을 대상으로 한 휴대용 FluoroSpot 리더는 수량을 더욱 늘립니다. 분석기의 ELISpot 및 FluoroSpot 어세이 시장 규모는 2030년까지 현재 교체 주기에 1억 4,000만 달러를 초과할 수 있으며, 이미지 분석 업그레이드 및 서비스 계약을 위한 비옥한 애프터마켓을 창출합니다. 액세서리(멤브레인 플레이트, 검량선, 머신러닝 라이선스)는 키트의 핵심 판매를 보완하고 AI 소프트웨어 패키지는 공급업체에게 프리미엄 마진 기회를 제공합니다.

분석 키트의 리더십은 싱글 사이토 카인 IFN-Y 키트에서 암 연구에 필수적인 멀티 플렉스 IL-2/Granzyme-B 번들까지 폭넓은 견고한 카탈로그에 지원됩니다. 유행 시대의 SARS-CoV-2 ELISpot 키트는 여전히 부스터 샷 평가를위한 재주문이 많지만 결핵 및 CMV 모니터링과 같은보다 광범위한 이용 사례가 점유율을 확대함에 따라 성장이 완만 해지고 있습니다. 제조업체 각 회사는 검사 당 비용을 15% 가까이 줄이는 유니버설 플레이트 화학을 시도하고 있으며 세계적인 보급을 더욱 확대하고 있습니다. 오픈소스 3D 프린팅 플레이트 홀더의 인기가 높아지고 있는 것은 신흥 국가에서 비용 중심의 솔루션으로의 전환을 뒷받침하는 것이며, ELISpot 및 FluoroSpot 어세이 시장에서 소모품의 지속적인 우위를 강화하는 것입니다.

병원과 임상실은 2024년 결핵, 이식, 원발성 면역 결핍의 대부분의 ELISpot 패널을 루틴으로 처리하여 키트와 서비스 지출로 약 2억 2,500만 달러를 받았습니다. 자동화된 결핵 워크플로우에 대한 규제 당국의 승인은 검사의 표준화와 처리량을 향상시키고 이러한 시설이 리더십을 유지할 수 있도록 합니다. 그럼에도 불구하고, 연구 기관과 CRO는 CAGR 15.85%의 속도로 추이하고 있으며, 대량 및 신속한 세포 분석을 필요로 하는 백신 및 면역요법 프로그램의 아웃소싱으로부터 이익을 얻고 있습니다. 위탁 기관은 ELISpot을 유동 세포 계측법 및 사이토 카인 다중화 방법과 번들하여 바이오 의약품 스폰서에게 매력적인 통합 면역 모니터링 패키지를 제공합니다.

바이오 의약품 및 백신 제조업체는 약사 규제 일정을 준수하기 위해 자사의 역가 측정에 의존하고 있으며, 한 자릿수 중반의 안정적인 성장 틈새 시장이 되고 있습니다. 학술 센터는 기본적인 T 세포 생물학을 추구함으로써 시장의 폭을 넓히고 나중에 임상 사용으로 전환하는 고급 FluoroSpot의 구성을 시험적으로 도입하는 경우가 많습니다. 개인화된 의료 테스트가 활발해짐에 따라 CRO는 ELISpot 및 FluoroSpot 어세이 시장 규모의 더 큰 부분을 차지할 것으로 보입니다. 왜냐하면 CRO의 세계 실험실 네트워크는 지리적으로 다양한 대상을 등록하고 규제 당국의 제출 서류를 위해 조화를 이룬 데이터 세트를 제공할 수 있기 때문입니다.

지역 분석

북미는 2024년에 1억 3,250만 달러의 매출을 올렸으며, 이는 세계 매출의 38.52%에 해당하며, 선진적인 바이오의약품 클러스터, 강력한 상환, 백신 및 세포요법 신청서류에 ELISpot을 명기하는 FDA 지침 등의 혜택을 받았습니다. 대규모 표준 연구소에서는 결핵과 CMV 패널을 대량으로 가동시키고 연구 병원에서는 멀티플렉스 FluoroSpot을 면역 종양학 프로그램에 통합하고 있습니다. 캐나다는 공중보건진단과 세포요법제조 거점 증가를 통해 꾸준한 성장을 이루고 지역 리더십을 강화하고 있습니다.

유럽에서는 제약 기업의 R&D 생태계가 확립되어 기능적 면역 모니터링을 지원하는 EMA의 틀이 정비되어 있습니다. 독일, 영국, 북유럽 국가들은 분석 장치의 설치 대수가 많아, 국경을 넘은 학술 컨소시엄이 AI를 활용한 디지털 리더 수요에 박차를 가하고 있습니다. 또한 표준화된 세포 검정을 필요로 하는 트랜스레이셔널 면역학이나 맞춤형 의료 프로젝트를 맡는 유럽 연합(EU)의 조성금 제도도 채용의 결정수가 되고 있습니다. 유럽 ELISpot 및 FluoroSpot 어세이 시장 규모는 회원국 간의 검증 오버헤드를 줄이는 규제 조화에 힘입어 한자리수 중반의 CAGR로 확대될 것으로 예측됩니다.

아시아태평양은 CAGR 13.61%로 가장 급성장하고 있는 지역으로, 중국에서의 백신 제조 확대, 한국과 일본에서의 견조한 생명공학 투자, 인도의 새로운 수탁 연구 클러스터에 지지되고 있습니다. 결핵 박멸을 목표로 하는 정부 프로그램은 키트의 대량 주문을 생성하고, CAR-T 임상시험 증가는 고가치 분석 장비 및 소프트웨어 시장을 개척합니다. 민간 파트너십은 멀티플렉스 FluoroSpot 시스템을 갖춘 레퍼런스 랩을 설립하여 기술 보급을 가속화합니다. 동남아시아 국가는 마이크로유체 ELISpot-on-chip을 활용하여 원격지에서의 POC(Point of Care) 진단에 나서고, 이 지역의 비용 효율이 뛰어난 기술 혁신에 대한 의욕을 부각하고 있습니다. 아시아태평양을 합치면 2030년까지 세계 매출의 거의 3분의 1을 차지할 수 있으며 ELISpot 및 FluoroSpot 어세이 시장에서 지리적 계층 구조가 재구성됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성질환 및 감염증 증가

- COVID-19 후 백신 파이프라인의 급속한 확대

- 멀티플렉스 플루오로 스팟 리더의 기술적 돌파구

- 세포 치료 QC에서 기능적 T 세포 분석의 규제 강화

- 오픈소스 3D 프린팅 ELISpot 하드웨어에 의한 비용 저하

- PoC 면역 모니터링을 가능하게 하는 마이크로플루이딕스 엘리스포트 온칩

- 시장 성장 억제요인

- 대체 고 파라미터 유동 세포 계측법 및 CyTOF 플랫폼 가용성

- 자동 분석 장치 및 화상 해석 소프트웨어의 높은 자본 비용

- 데이터 분석의 복잡성과 바이오인포매틱스의 스킬셋 부족

- 분석 표준화의 지연에 의한 실험실 간 변동

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자·소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 제품별

- 분석기

- 자동화 플레이트 리더

- 휴대용 플루오로스팟 리더

- 분석 키트

- 사이토카인 특이적 ELISpot 키트

- 멀티플렉스 플루오로스팟 키트

- SARS-CoV-2 T세포 키트

- 보조제품

- 멤브레인 플레이트 및 시약

- 이미지 분석 소프트웨어

- 분석기

- 최종 사용자별

- 병원 및 임상 실험실

- 바이오 의약품 및 백신 제조업체

- 연구기관 및 계약 연구 기관

- 용도별

- 연구

- 백신 개발

- 임상시험 면역 모니터링

- 암 면역요법 조사

- 세포 및 유전자 치료 출시 테스트

- 진단

- 감염성 질환 진단

- 이식 면역학

- 자가면역질환 패널

- 결핵 진단

- 연구

- 기술별

- 비색 ELISpot

- FluoroSpot

- 디지털/AI 강화 ELISpot

- 마이크로플루이딕 ELISpot-on-Chip

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oxford Immunotec

- Cellular Technology Limited(CTL)

- Becton, Dickinson & Company

- Mabtech AB

- U-Cytech Biosciences

- Abcam plc

- AutoImmun Diagnostika GmbH

- Lophius Biosciences GmbH

- Bio-Connect BV

- Bio-Techne Corp.

- Thermo Fisher Scientific

- Merck KGaA

- Siemens Healthineers

- Bio-Rad Laboratories

- PerkinElmer

- Danaher(Beckman Coulter)

- Qiagen

- Agilent Technologies

- AID Diagnostika GmbH

- GenScript Biotech

- Dynex Technologies

제7장 시장 기회와 전망

KTH 25.11.10The ELISpot FluoroSpot Assay market size stands at USD 343.68 million in 2025 and is forecast to expand to USD 507.80 million by 2030 at an 8.12% CAGR, underscoring accelerating demand for high-sensitivity cellular immunoassays across infectious-disease diagnostics, vaccine development and cell-therapy quality-control.

Intensifying vaccine pipelines after COVID-19, wider clinical adoption of T-cell assays for biologics approval and steady cost declines in open-architecture hardware are combining to keep growth momentum strong. Hospital laboratories are standardizing functional immune-monitoring panels, research organizations are outsourcing large volumes of assay work to specialized CROs and regulators are embedding T-cell functionality metrics in licensure packages for next-generation immunotherapies. Parallel advances in automated image capture, machine-learning-based spot counting and microfluidic chip formats are reshaping laboratory workflows and widening global access. Competitive dynamics remain moderate, with incumbent assay leaders facing new entrants offering AI-enhanced analytics and portable devices that push the ELISpot FluoroSpot Assay market into point-of-care settings.

Global ELISpot And FluoroSpot Assay Market Trends and Insights

Rising Incidence of Chronic & Infectious Diseases

Increasing caseloads of tuberculosis, HIV, viral hepatitis and cancer are boosting demand for precise cellular immune-monitoring. The T-SPOT.TB test now registers 99% sensitivity and 94% specificity, outperforming traditional methods and solidifying ELISpot technology as a frontline diagnostic. FDA clearance of automated T-SPOT-compatible liquid-handling workstations in 2025 further validates clinical use. Oncology centres routinely employ interferon-Y and IL-2 ELISpot panels to track neoantigen-specific responses that guide checkpoint-inhibitor dosing. WHO recommendations calling for broader access to quality diagnostics in high-burden regions align with the ELISpot FluoroSpot Assay market expansion because functional assays detect low-frequency T-cells missed by serological tests. As non-communicable disease prevalence rises alongside infectious threats, broad clinical adoption of standardized ELISpot workflows is likely to remain a durable growth pillar.

Rapid Vaccine Pipeline Expansion Post-COVID-19

Vaccine developers are shifting focus from antibody-centric endpoints toward cellular immunity. BARDA-sponsored phase 2b designs for next-generation COVID-19 vaccines explicitly integrate T-cell assays to demonstrate broader and longer-lasting protection. The same requirement now features in seasonal influenza programs attempting to overcome strain-specific limitations. The Center for Biologics Evaluation and Research reported 17 biologics licenses granted in 2024 that necessitated functional immune data, cementing assay use in regulatory dossiers. In turn, CROs and in-house laboratories are scaling the ELISpot FluoroSpot Assay market by installing multiplex readers that quantify cross-reactive immunity across variant lineages. Universal vaccine research targeting conserved epitopes further strengthens the need to capture polyfunctional T-cell outputs that colorimetric ELISA cannot reveal.

Availability of Alternate High-Parameter Flow-Cytometry & CyTOF Platforms

Forty-five-color full-spectrum cytometry and mass cytometry can delineate complex immune landscapes at single-cell resolution, positioning these platforms as credible substitutes where deep phenotyping outweighs functional readouts. Studies comparing 33-marker CyTOF and spectral flow panels demonstrate high concordance in quantifying immune subsets across clinical samples. Laboratories that already own cytometers may upgrade to ultra-high-parameter configurations instead of purchasing separate ELISpot readers, thereby tempering incremental instrument demand. While ELISpot retains an edge in detecting low-frequency functional responses, technology overlap is likely to intensify procurement deliberations in large reference centres.

Other drivers and restraints analyzed in the detailed report include:

- Technological Breakthroughs in Multiplex FluoroSpot Readers

- Regulatory Push for Functional T-Cell Assays in Cell-Therapy QC

- High Capital Cost of Automated Analyzers & Image-Analysis Software

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

At USD 187.3 million revenue in 2024, Assay Kits generated more than half of total spending, echoing the recurring requirement for cytokine-coated wells and detection antibodies. Laboratories reorder these consumables for each run, ensuring steady replenishment streams. Analyzer demand, although forming a smaller base, is projected to outpace kits thanks to a 14.25% CAGR as automation and AI analytics become routine in high-throughput settings. Portable FluoroSpot readers targeting tuberculosis screening programs in community clinics add incremental volume. The ELISpot FluoroSpot Assay market size for analyzers could exceed USD 140 million by 2030 under the current replacement cycle, creating a fertile aftermarket for image-analysis upgrades and service contracts. Ancillary items-membrane plates, calibration standards and machine-learning licenses-complement core kit sales, with AI software packages providing premium margin opportunities for vendors.

Assay Kit leadership rests on a robust catalogue that spans single-cytokine IFN-Y kits to multiplex IL-2/Granzyme-B bundles essential for oncology research. Pandemic-era SARS-CoV-2 ELISpot kits still post reorder volumes for booster-shot evaluation, though growth moderates as broader use cases such as tuberculosis and CMV monitoring gain share. Manufacturers are experimenting with universal plate chemistries that cut per-test cost nearly 15%, further expanding global penetration. The rising popularity of open-source 3D-printed plate holders underscores a shift toward cost-sensitive solutions in developing countries, reinforcing consumables' sustained primacy in the ELISpot FluoroSpot Assay market.

Hospitals and clinical laboratories processed the majority of routine tuberculosis, transplant and primary-immunodeficiency ELISpot panels in 2024, capturing roughly USD 225 million in kit and service spending. Regulatory endorsement of automated TB workflows boosts test standardization and throughput, allowing these sites to retain leadership. Nonetheless, Research Institutes and CROs are on pace for a 15.85% CAGR, benefiting from outsourced vaccine and immunotherapy programs that require high-volume, rapid-turnaround cellular assays. Contract organizations bundle ELISpot with flow cytometry and cytokine multiplexing, offering integrated immune-monitoring packages attractive to biopharma sponsors.

Biopharmaceutical and vaccine manufacturers rely on in-house potency testing to meet regulatory timelines, representing a steady mid-single-digit growth niche. Academic centres extend market breadth by pursuing fundamental T-cell biology, often piloting advanced FluoroSpot configurations that later migrate into clinical use. As personalized medicine trials proliferate, CROs will likely assume a larger slice of the ELISpot FluoroSpot Assay market size because their global lab networks can enrol geographically diverse subjects and deliver harmonized data sets for regulatory dossiers.

The ELISpot & Fluorospot Assay Market Report is Segmented by Product (Analyzers, Assay Kits, and Ancillary Products), End-User (Hospitals & Clinical Laboratories, Biopharmaceutical & Vaccine Manufacturers, and More), Application (Research and Diagnostics), Technology (Colorimetric ELISpot, Fluorospot, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated USD 132.5 million revenue in 2024, equivalent to 38.52% of global sales, and benefits from advanced biopharmaceutical clusters, strong reimbursement and FDA guidance that enshrines ELISpot in vaccine and cell-therapy submissions. Large reference laboratories run high-volume tuberculosis and CMV panels, and research hospitals integrate multiplex FluoroSpot into immuno-oncology programs. Canada contributes steady growth through public-health diagnostics and a rising cell-therapy manufacturing footprint, reinforcing regional leadership.

Europe follows with entrenched pharmaceutical R&D ecosystems and EMA frameworks that support functional immune monitoring. Germany, the United Kingdom and the Nordics exhibit high analyzer installations, while cross-border academic consortia spur demand for AI-enhanced digital readers. Adoption also leans on European Union funding lines that underwrite translational immunology and personalized-medicine projects requiring standardized cellular assays. The ELISpot FluoroSpot Assay market size captured in Europe is projected to expand at a mid-single-digit CAGR, aided by regulatory harmonization that lowers validation overheads across member states.

Asia-Pacific is the fastest-growing territory at 13.61% CAGR, underpinned by expanding vaccine manufacturing in China, robust biotechnology investment in South Korea and Japan and emerging contract-research clusters in India. Government programs targeting tuberculosis elimination generate bulk kit orders, while rising CAR-T clinical trials open a high-value analyzer and software market. Public-private partnerships establish reference labs equipped with multiplex FluoroSpot systems, accelerating technology diffusion. Southeast Asian nations leverage microfluidic ELISpot-on-chip pilots to deliver point-of-care diagnostics in remote areas, underscoring the region's appetite for cost-efficient innovation. Collectively, Asia-Pacific could command nearly one-third of incremental global revenue through 2030, reshaping geographic hierarchy in the ELISpot FluoroSpot Assay market.

- Oxford Immunotec

- Cellular Technology Limited (CTL)

- Beckton Dickinson

- Mabtech

- U-Cytech Biosciences

- Abcam

- AutoImmun Diagnostika GmbH

- Lophius Biosciences

- Bio-Connect

- Bio-Techne Corp.

- Thermo Fisher Scientific

- Merck

- Siemens Healthineers

- Bio-Rad Laboratories

- PerkinElmer

- Danaher

- QIAGEN

- Agilent Technologies

- AID Diagnostika GmbH

- GenScript Biotech

- Dynex Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Chronic & Infectious Diseases

- 4.2.2 Rapid Vaccine Pipeline Expansion Post-COVID-19

- 4.2.3 Technological Breakthroughs In Multiplex Fluorospot Readers

- 4.2.4 Regulatory Push For Functional T-Cell Assays In Cell-Therapy QC

- 4.2.5 Cost Decline Via Open-Source, 3-D-Printed ELISpot Hardware

- 4.2.6 Microfluidic Elispot-On-Chip Enabling PoC Immunomonitoring

- 4.3 Market Restraints

- 4.3.1 Availability Of Alternate High-Parameter Flow-Cytometry & CyTOF Platforms

- 4.3.2 High Capital Cost Of Automated Analyzers & Image-Analysis Software

- 4.3.3 Data-Analysis Complexity And Lack Of Bio-Informatics Skillsets

- 4.3.4 Inter-Lab Variability Due To Weak Assay Standardization

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Analyzers

- 5.1.1.1 Automated Plate Readers

- 5.1.1.2 Portable FluoroSpot Readers

- 5.1.2 Assay Kits

- 5.1.2.1 Cytokine-specific ELISpot Kits

- 5.1.2.2 Multiplex FluoroSpot Kits

- 5.1.2.3 SARS-CoV-2 T-cell Kits

- 5.1.3 Ancillary Products

- 5.1.3.1 Membrane Plates & Reagents

- 5.1.3.2 Image-analysis Software

- 5.1.1 Analyzers

- 5.2 By End-User

- 5.2.1 Hospitals & Clinical Laboratories

- 5.2.2 Biopharmaceutical & Vaccine Manufacturers

- 5.2.3 Research Institutes & Contract Research Organisations

- 5.3 By Application

- 5.3.1 Research

- 5.3.1.1 Vaccine Development

- 5.3.1.2 Clinical Trials Immunomonitoring

- 5.3.1.3 Cancer Immunotherapy Research

- 5.3.1.4 Cell & Gene-Therapy Release Testing

- 5.3.2 Diagnostics

- 5.3.2.1 Infectious Disease Diagnostics

- 5.3.2.2 Transplant Immunology

- 5.3.2.3 Autoimmune Disease Panels

- 5.3.2.4 Tuberculosis Diagnostics

- 5.3.1 Research

- 5.4 By Technology

- 5.4.1 Colorimetric ELISpot

- 5.4.2 FluoroSpot

- 5.4.3 Digital/AI-enhanced ELISpot

- 5.4.4 Microfluidic ELISpot-on-Chip

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Oxford Immunotec

- 6.3.2 Cellular Technology Limited (CTL)

- 6.3.3 Becton, Dickinson & Company

- 6.3.4 Mabtech AB

- 6.3.5 U-Cytech Biosciences

- 6.3.6 Abcam plc

- 6.3.7 AutoImmun Diagnostika GmbH

- 6.3.8 Lophius Biosciences GmbH

- 6.3.9 Bio-Connect B.V.

- 6.3.10 Bio-Techne Corp.

- 6.3.11 Thermo Fisher Scientific

- 6.3.12 Merck KGaA

- 6.3.13 Siemens Healthineers

- 6.3.14 Bio-Rad Laboratories

- 6.3.15 PerkinElmer

- 6.3.16 Danaher (Beckman Coulter)

- 6.3.17 Qiagen

- 6.3.18 Agilent Technologies

- 6.3.19 AID Diagnostika GmbH

- 6.3.20 GenScript Biotech

- 6.3.21 Dynex Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment