|

시장보고서

상품코드

1846288

의료장비 교정 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Medical Equipment Calibration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

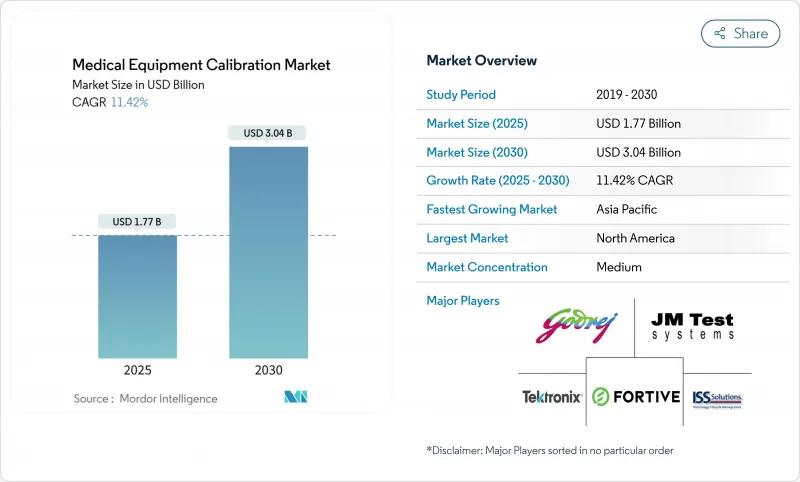

의료장비 교정 시장 규모는 2025년에 17억 7,000만 달러로 예상되며, 예측기간 중(2025-2030년) CAGR은 11.42%로, 2030년에는 30억 4,000만 달러에 달할 것으로 추정되고 있습니다.

수요는 세계적인 품질 규제의 엄격화, 급속한 기술 교체 사이클, 첨단 헬스케어 인프라의 꾸준한 보급이라는 3가지 수렴하는 힘에 추종하고 있습니다. 2026년에 시행되는 새로운 FDA 품질경영시스템 규정 개정은 미국 규정을 ISO 13485 : 2016과 조화시켜 추적 가능한 교정 기록의 필요성을 강화합니다. 인공호흡기, 인공호흡기, 네트워크화된 모니터에 대한 설비투자로 인하여 의료장비 교정 시장이 확대되고 있습니다. 병원은 또한 가치 기반 의료에 따라 의료 보상과 장비 정밀도 지표를 연관시키고 교정을 운영 예산에 추가로 통합합니다.

세계의 의료장비 교정 시장 동향과 인사이트

엄격한 세계 규제가 교정 표준화를 촉진

규제의 조화는 교정 추적성을 품질 감사 및 장비 승인에 통합함으로써 의료장비 교정 시장을 활성화합니다. FDA QMSR은 현재 ISO 13485 : 2016을 반영하고 있으며 이중 컴플라이언스 사일로를 제거하고 문서화 깊이를 넓히고 있습니다. 유럽의 MDR과 IVDR은 기본적인 안전성 검사를 훨씬 능가하는 동등한 파일 보관 의무를 부과하고 있으며 공급업체는 모든 교정 이벤트에 대한 CoC 기록을 유지하도록 요청받고 있습니다. 중국의 NMPA 개혁은 같은 기준에 부합하는 반면 임상시험에 관한 현지 요구사항을 추가하여 국내 및 다국적 검사시설에 새로운 인정업무를 창출하고 있습니다. 규제 당국은 사이버 보안에도 감시 대상을 넓히고 있으며, 미국의 지침 초안에서는 '사이버 기기'에 대한 소프트웨어 부품표를 요구하고 있기 때문에 교정 루틴에 보안 검증 단계가 포함되는 경우가 늘고 있습니다. 이러한 규칙이 얽히면서 조달, 서비스 계약, 기술자 교육의 형태가 크게 바뀝니다.

고부가가치 이미지 & 라이프 서포트 시스템의 설치 대수 증가

병원의 자본 예산은 현재 AI 대응 CT, MRI, 인공호흡기 플랫폼을 중심으로 돌고 있습니다. Philips의 헬륨 프리 MRI 아키텍처는 런닝 비용을 줄이는 한편, 기존의 1,500리터 용기 대신 7리터 용기의 자석을 사용하기 위한 새로운 교정 프로토콜을 필요로 합니다. GE 헬스케어가 엔비디아와 제휴한 자율적인 X선 및 초음파 진단 장치는 소프트웨어 모델에도 기계 부품과 동일한 추적성이 필요하기 때문에 별도의 교정 레이어가 추가됩니다. 이러한 기술 혁신은 장비의 변형을 늘리고 서비스 믹스를 알고리즘 검증, IoT 센서 체크, 멀티 모달 성능 시험으로 이동시킴으로써 의료장비 교정 시장을 확대합니다. 새로운 생명 유지 시스템에는 실시간 피드백 루프가 내장되어 있어 환자의 안전을 보호하고 가치 기반 서비스 계약에서 정해진 가동 시간 보장을 유지하기 위해 보다 빈번한 마이크로 교정이 요구됩니다.

신흥 시장에서 높은 비용과 복잡한 스케줄링

저소득 지역의 건강 관리 시스템은 수명 주기 서비스보다 하드웨어 취득을 선호합니다. 공급망의 혼란으로 인해 2024년에는 물류 비용이 제조업체 수익의 최대 5%까지 상승하여 수입 기준 장비의 교정 비용이 늘어났습니다. 지리적 확산은 엔지니어가 하루에 2일의 이동일을 지출할 수 있음을 의미하며, 이는 정기적인 방문을 억제하고 의료장비 교정 시장을 침체시킵니다. 환율 변동은 하드 캘린시에서 가격이 정해진 다년 계약을 더욱 복잡하게 만듭니다. 선도적인 공급자는 수요를 풀거나 트레스칼과 같은 세계 기업에 지역 허브를 설립함으로써 대응하여 점차 비용 부담을 줄이고 있습니다.

부문 분석

2024년 의료장비 교정 시장의 33.45%를 이미지 플랫폼이 차지하며, 갠트리 얼라인먼트에서 선량 교정에 이르기까지 광범위한 교정 터치 포인트를 반영했습니다. 소프트웨어 개정 및 하드웨어 개조가 이루어질 때마다 서비스 수익이 증가하고 장기 계약이 연결됩니다. 알고리즘 이미지 프로세싱 방법은 기존의 기하학적 검사를 초과하는 비디오 속도 조정을 추가하고 범위를 확대합니다. 이와 대조적으로 바이탈 사인 모니터의 CAGR은 14.01%를 나타낼 전망입니다. 거실에 모니터가 출하될 때마다 의료장비 교정 시장은 비시설 환경으로 확대되어 휴대용 필드 교정 키트가 출시되는 계기가 됩니다. 경사가 없는 헬륨 MRI, AI 대응 초음파, 연결된 주입 펌프는 모두 맞춤형 절차를 필요로 하며 전문가 수요를 둘러싸고 있습니다.

네트워크화된 장비의 급속한 보급은 교정이 센서, 임베디드 펌웨어, 클라우드 API를 일상적으로 다루고 있음을 의미합니다. 주입 펌프는 유량 정확도를 위해 중량 교정에 의존하며 펌웨어 패치는 규정 준수에 대한 시계를 재설정합니다. 인공호흡기의 교정은 유행시에 시각화되어 집중 치료실에서 여전히 중요한 안전 헤지가 되고 있습니다. 수술 및 실험실 분석기는 안정적인 성장을 유지하고 의료장비 교정 시장에서 수익의 다양성을 형성하고 있습니다.

지역 분석

북미는 ISO 13485와 FDA 감시 감사의 조기 정합에 힘입어 2024년 세계 매출의 39.83%를 차지했습니다. 조달팀은 ISO/IEC 17025 인증을 의무화하는 서비스 조항을 통합하여 높은 진입 장벽을 굳히고 규모가 큰 사업자에게 보답합니다. 캐나다의 규제 근대화와 멕시코의 수출 지향 장비 생산이 이 지역의 추풍이 되고 있습니다. 북미의 의료장비 교정 시장 규모는 이미징 진단 오버홀, 원격 ICU 전개, 사이버 보안의 의무화와 보조를 함께 확대할 것으로 예측됩니다.

아시아태평양의 CAGR은 12.52%로 급성장하고 있으며, 중국, 인도, 한국에 있어서 제조업체 거점의 확대나, 동남아시아 전역에서의 새로운 병원 건설에 추진되고 있습니다. 하이엔드 제품의 현지 생산을 장려하는 정부의 인센티브가 공급업체에 의한 국내 교정 능력의 구축에 박차를 가해 국경을 넘은 합작 사업을 자극하고 있습니다. 고령화가 진행되는 일본에서는 화상진단의 이용이 증가하고 ASEAN 의료장비지령은 10개국의 사무작업을 삭감하고 벤더 진입을 가속시킵니다. 이러한 요인은 이 지역 전체의 의료장비 교정 시장의 활성화로 이어지고 있습니다.

유럽에는 대규모 설치 기반과 상세한 규제 플레이북이 있습니다. MDR과 IVDR의 업데이트는 교정을 방사선학에서 체외 진단학으로 확장하고 작업 목록을 늘리고 서비스 계약을 장기화합니다. 독일 수출 파이프라인, 프랑스 병원 투자, 영국 브렉짓 후 조정 노력은 총체적으로 높은 수요를 유지하고 있습니다. 지속가능성을 우선시함으로써 헬륨이 없는 MRI와 같은 보다 새로운 교정 기법에 대응할 수 있는 여지가 넓어져 기존 냉각이나 극저온 체크가 시대 지연될 가능성도 있습니다. 기타에는 중동, 아프리카, 남미가 시대 지연 시설을 개수하고 새로운 3차 의료센터를 건설하고 있기 때문에 상대적인 성장을 급속히 기록하고 있지만, 한정된 기술자 풀과 환율 위험이 섭취를 억제하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 세계 규제

- 고부가가치 이미징·라이프 서포트 시스템의 설치 대수 증가

- 기기의 다운 타임을 삭감하는 예방 보수 계약

- 마이크로 교정을 가능하게 하는 IoT 연동 자기 진단 센서

- 정밀 KPI에 상환을 연결하는 가치 기반 조달

- 현장 교정 키트를 필요로 하는 재택/POC 기기

- 시장 성장 억제요인

- 신흥 시장에서의 고비용과 복잡한 스케줄링

- ISO/IEC 17025 인증기술자 부족

- 원격 교정 액세스를 제한하는 사이버 보안 규칙

- AI 자동 교정 데이터의 무결성에 대한 우려

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측(단위 : 달러)

- 기기 유형별

- 생체 신호 모니터

- 인공호흡기

- 태아 모니터

- 심혈관 모니터

- 영상 장비

- 주입 펌프

- 기타 기기

- 서비스 유형별

- 자사 교정 서비스

- 제3자 교정 서비스

- OEM 교정 서비스

- 최종 사용자별

- 임상 실험실

- 병원

- 기타(재택치료, 외래, OEM 실험실)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Fortive

- Trescal

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Transcat

- Tektronix

- JM Test Systems

- TAG Medical

- BC Group International

- Beamex

- Keysight Technologies

- JPen Medical

- NS Medical Systems

- Medserve Ltd

- Godrej Biomed

- Biomed Technologies(ISS Solutions)

- TBS Group

- Aramark Services

- Pentax Medical Services

- Rigel Medical

제7장 시장 기회와 전망

KTH 25.11.10The Medical Equipment Calibration Market size is estimated at USD 1.77 billion in 2025, and is expected to reach USD 3.04 billion by 2030, at a CAGR of 11.42% during the forecast period (2025-2030).

Demand tracks three converging forces: stricter global quality mandates, rapid technology replacement cycles, and the steady spread of advanced healthcare infrastructure. New FDA Quality Management System Regulation amendments taking effect in 2026 will harmonize United States rules with ISO 13485:2016 and reinforce the need for traceable calibration records. Capital spending on AI-enabled imaging, ventilators, and networked monitors expands the medical equipment calibration market because every new device shipped carries a downstream calibration requirement. Hospitals also link reimbursement to device accuracy metrics under value-based care, further embedding calibration into operating budgets.

Global Medical Equipment Calibration Market Trends and Insights

Stringent Global Regulations Drive Calibration Standardization

Regulatory harmonization elevates the medical equipment calibration market by embedding calibration traceability into quality audits and device approvals. The FDA QMSR now mirrors ISO 13485:2016, eliminating dual compliance silos and expanding documentation depth. Europe's MDR and IVDR impose comparable file-keeping obligations that reach far beyond basic safety checks and push suppliers to maintain chain-of-custody records for every calibration event. China's NMPA reforms dovetail with the same standards while adding local clinical-trial demands, creating new accreditation work for domestic and multinational laboratories. Regulators also extend oversight to cybersecurity, with draft U.S. guidance requiring a software bill of materials for "cyber devices," so calibration routines increasingly include security-verification steps. Collectively, these intertwined rules reshape procurement, service contracting, and technician training.

Growing Installed Base of High-Value Imaging & Life-Support Systems

Hospital capital budgets now revolve around AI-ready CT, MRI, and ventilator platforms. Philips' helium-free MRI architecture trims running costs yet requires new calibration protocols for a 7-liter magnet in place of traditional 1,500-liter vessels. GE HealthCare's alliance with NVIDIA for autonomous x-ray and ultrasound adds another calibration layer because software models need the same traceability as mechanical parts. These innovations multiply device variants and expand the medical equipment calibration market by shifting the service mix toward algorithm validation, IoT sensor checks, and multi-modal performance tests. Emerging life-support systems embed real-time feedback loops that demand more frequent micro-calibrations to guard patient safety and maintain uptime guarantees negotiated in value-based service contracts.

High Cost & Scheduling Complexity in Emerging Markets

Healthcare systems in lower-income regions prioritize hardware acquisition over lifecycle services. Supply-chain disruptions raised logistics costs by up to 5% of manufacturer revenue in 2024, inflating calibration expenses for imported reference instruments. Geographic sprawl means a technician may spend two travel days for every service day, which deters routine visits and dampens the medical equipment calibration market. Currency swings further complicate multiyear contracts priced in hard currencies. Large providers respond by pooling demand or inviting global firms like Trescal to set up regional hubs, slowly easing cost burdens.

Other drivers and restraints analyzed in the detailed report include:

- Preventive-Maintenance Contracts to Cut Device Downtime

- IoT-Linked Self-Diagnostic Sensors Enabling Micro-Calibration

- Scarcity of ISO/IEC 17025-Accredited Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Imaging platforms accounted for 33.45% of the medical equipment calibration market in 2024, reflecting extensive calibration touchpoints from gantry alignment to dose calibration. Each software revision and hardware retrofit drives incremental service revenue and anchors long-term contracts. Algorithmic imaging methods add video-rate adjustments that go beyond classical geometric checks, enlarging scope. Vital-sign monitors, by contrast, post a 14.01% CAGR because home-care adoption multiplies unit volume. Every monitor shipped into a living room extends the medical equipment calibration market to non-institutional settings and triggers portable field-calibration kits. Gradient-free helium MRI, AI-enabled ultrasound, and connected infusion pumps all require bespoke procedures, locking in specialist demand.

Rapid uptake of networked devices means calibration now routinely covers sensors, embedded firmware, and cloud APIs. Infusion pumps rely on gravimetric calibration for flow accuracy, and any firmware patch resets the clock on compliance. Ventilator calibration gained visibility during the pandemic and remains a critical safety hedge in intensive-care units. Surgical tools and laboratory analyzers sustain steady growth, rounding out revenue diversity within the medical equipment calibration market.

The Medical Equipment Calibration Market Report Segments the Industry Into by Equipment Type (Vital Sign Monitors, Ventilators, Fetal Monitors, and More), Type of Service (In-House Calibration Services, and More ), End User (Clinical Laboratories, Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.83% of global revenue in 2024, supported by early alignment with ISO 13485 and routine FDA surveillance audits. Procurement teams embed service clauses that mandate ISO/IEC 17025 accreditation, cementing a high-entry barrier and rewarding scale operators. Canada's regulatory modernization and Mexico's export-oriented device production add regional tailwinds. The medical equipment calibration market size for North America is projected to advance in lockstep with imaging overhauls, tele-ICU rollouts, and cybersecurity mandates.

Asia-Pacific grows at a brisk 12.52% CAGR, propelled by expanding manufacturer hubs in China, India, and South Korea and by fresh hospital construction across Southeast Asia. Government incentives to localize high-end production spur suppliers to build domestic calibration capability, stimulating cross-border joint ventures. Japan's aging population drives heavy imaging utilization, while the ASEAN Medical Device Directive trims paperwork across 10 countries and speeds vendor onboarding. These factors converge to embed the medical equipment calibration market across the region.

Europe commands a large installed base and a detailed regulatory playbook. MDR and IVDR updates extend calibration from radiology into in vitro diagnostics, inflating task lists and lengthening service contracts. Germany's export pipeline, France's hospital investments, and the United Kingdom's post-Brexit alignment efforts collectively keep demand high. Sustainability preferences open space for newer calibration methods-for instance, helium-free MRI-and render traditional cooling and cryogen checks obsolete. Elsewhere, the Middle East, Africa, and South America register quicker relative growth as they retrofit outdated fleets and build new tertiary centers, though limited technician pools and currency risk temper uptake.

- Fortive

- Trescal

- GE Healthcare

- Siemens Healthineers

- Koninklijke Philips

- Transcat

- Tektronix

- JM Test Systems

- TAG Medical

- BC Group International

- Beamex

- Keysight Technologies

- JPen Medical

- NS Medical Systems

- Medserve Ltd

- Godrej Biomed

- Biomed Technologies (ISS Solutions)

- TBS Group

- Aramark Services

- Pentax Medical Services

- Rigel Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global Regulations

- 4.2.2 Growing Installed Base of High-Value Imaging & Life-Support Systems

- 4.2.3 Preventive-Maintenance Contracts to Cut Device Downtime

- 4.2.4 IoT-Linked Self-Diagnostic Sensors Enabling Micro-Calibration

- 4.2.5 Value-Based Procurement Tying Reimbursement to Accuracy KPIs

- 4.2.6 Home/POC Devices Needing Field-Calibration Kits

- 4.3 Market Restraints

- 4.3.1 High Cost & Scheduling Complexity in Emerging Markets

- 4.3.2 Scarcity of ISO/IEC 17025-Accredited Technicians

- 4.3.3 Cyber-Security Rules Limiting Remote Calibration Access

- 4.3.4 AI Autocalibration Data-Integrity Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Equipment Type

- 5.1.1 Vital Sign Monitors

- 5.1.2 Ventilators

- 5.1.3 Fetal Monitors

- 5.1.4 Cardiovascular Monitors

- 5.1.5 Imaging Equipment

- 5.1.6 Infusion Pumps

- 5.1.7 Other Equipment

- 5.2 By Type of Service

- 5.2.1 In-house Calibration Services

- 5.2.2 Third-party Calibration Services

- 5.2.3 OEM Calibration Services

- 5.3 By End User

- 5.3.1 Clinical Laboratories

- 5.3.2 Hospitals

- 5.3.3 Others (Home-care, Ambulatory, OEM Labs)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Fortive

- 6.3.2 Trescal

- 6.3.3 GE Healthcare

- 6.3.4 Siemens Healthineers

- 6.3.5 Philips Healthcare

- 6.3.6 Transcat

- 6.3.7 Tektronix

- 6.3.8 JM Test Systems

- 6.3.9 TAG Medical

- 6.3.10 BC Group International

- 6.3.11 Beamex

- 6.3.12 Keysight Technologies

- 6.3.13 JPen Medical

- 6.3.14 NS Medical Systems

- 6.3.15 Medserve Ltd

- 6.3.16 Godrej Biomed

- 6.3.17 Biomed Technologies (ISS Solutions)

- 6.3.18 TBS Group

- 6.3.19 Aramark Services

- 6.3.20 Pentax Medical Services

- 6.3.21 Rigel Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment