|

시장보고서

상품코드

1846292

생명과학 시약 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Life Science Reagents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

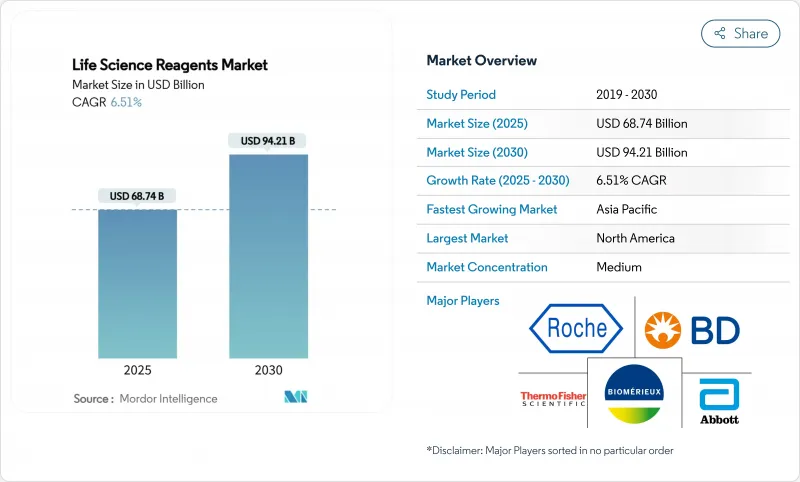

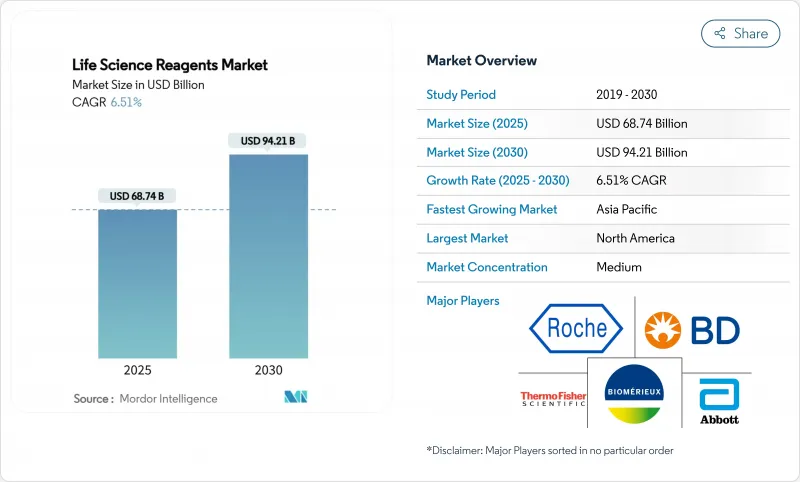

생명과학 시약 시장 규모는 2025년에 687억 4,000만 달러로 추정되고, 2030년에는 CAGR 6.51%로 성장할 전망이며, 942억 1,000만 달러에 이를 것으로 예측됩니다.

정밀진단, 싱글셀 멀티오믹스, 자동화된 실험실 워크플로우가 견조하게 추이해, 규제 당국이 품질 요건을 엄격하게 해도 수요는 계속 확대되고 있습니다. 병원 검사실이 계속해서 최대 주문을 하고 있지만, 생물제제 파이프라인이 복잡해짐에 따라 제약회사와 생명공학 회사는 자사 이용을 확대하고 있습니다. AI에 의한 시약 선택의 급속한 도입, 지속가능한 동물 프리 제형에 대한 투자 확대, 제조 능력의 재조달은 장기적인 공급망 리스크로부터 성장 전망을 지키고 있습니다. 신흥 디스래프터는 분산형 마이크로플루이딕스 카트리지 생산을 벌크 공급을 대체할 수 있는 대안으로 바꾸고 있으며, 디지털 물류를 갖춘 민첩한 공급업체를 선도하는 새로운 가격과 서비스 모델을 창출하고 있습니다.

세계의 생명과학 시약 시장 동향 및 인사이트

높은 감염증 부담

세계적인 탈주로 인해 분자 시약과 면역 측정 시약의 양은 증가의 길을 따릅니다. FDA의 유연한 긴급 지침은 검증된 신속 대응 키트 시장 진입을 가속화하고 곧바로 사용할 수 있는 규모의 생산 플랫폼을 갖춘 공급업체에게 이점을 제공합니다. 자원이 부족한 지역에서의 포인트 오브 케어 시스템의 보급은 액세스를 확대하고 있지만, 물류와 가격 설정의 장애물은 여전히 높습니다. 컴팩트한 검출 장치에 시약을 번들할 수 있는 제조업체는 현장에서의 전개를 간소화함으로써 점유율을 확대합니다. 항균제 내성 감시의 지속은 새로운 병원체 검출에 적합한 높은 처리량 PCR 마스터 믹스 및 선택 배지에 대한 수요를 더욱 증가시킵니다.

유전체학 및 단백질체학의 기술적 진보

단일 셀 시퀀싱 및 공간 단백질체학는 새로운 시약 성능 벤치마크를 설정하고 있습니다. 일루미나의 Fluent BioSciences사 인수는 확장 가능한 멀티 오믹 워크 플로우에 대한 전략적 베팅을 명확히 하고 공급업체에게 일관된 로트 간 역학을 갖는 초저 입력 효소를 제공하도록 촉구합니다. 자율주행 실험실과 통합된 자동화 지원 버퍼 시스템은 연구개발 사이클을 500일 이상 단축하고 시약 낭비를 없애며 프리미엄 SKU를 높이고 있습니다. 장비 제조업체와 키트를 공동 개발할 수 있는 공급업체는 설치 기반을 확장하는 우선 공급업체로 자리매김하고 있습니다.

특수 시약의 높은 비용 및 가격 압력

GMP 등급의 CRISPR 구성 요소는 연구 동등품의 5-10배 비용이 들기 때문에 예산이 제한된 생명공학 기업에서는 채용이 제한됩니다. Casgevy 치료의 220만 달러의 가격은 시약 비용이 최종 치료 비용으로 어떻게 연결되는지를 보여줍니다. 로터스에서 고원까지의 가격 역학은 대량 구매를 촉구하지만, 효소 및 항체 벤더의 통합은 소규모 구매자의 협상력을 저하시킵니다. 인간 혈소판 용해액의 90%를 대체하는 새로운 식물 기반 세포 배양 보충제는 비용 절감 경로를 제안하지만, 보다 광범위한 검증이 필요합니다.

부문 분석

세포 및 조직 배양 시약은 2024년에 생명과학 시약 시장 점유율의 29.92%를 차지했으며, 바이오매뉴팩처링 워크플로우에 필수적인 존재로 선도하고 있습니다. 이 분야는 화학적으로 정의되고 변동 및 면역 원성을 억제하는 제노 프리 배지로의 지속적인 업그레이드로부터 이익을 얻고 있습니다. 로트 제약과 같은 기업은 제품 간 드리프트를 최소화하는 무혈청 줄기 세포 배지를 개발하고 있으며, 재생 의료 파이프라인에서 프리미엄 정가를 획득했습니다. 크로마토그래피 시약은 항체 정제 수요에 힘입어 안정적인 수익을 올리고 임상 화학 패널은 검사실의 자동화에 의해 판매량을 늘리고 있습니다. 분자 진단 시약은 CAGR 7.22%를 예측하고 리퀴드 바이옵시, NGS 라이브러리 준비, 마이크로 RNA 검출 프로토콜의 규모가 확대됨에 따라 동업자를 능가하고 있습니다.

분자진단제의 급증은 정밀 종양학이 시약의 복잡성을 어떻게 증가시키는지를 보여줍니다. 시퀀싱 비용이 낮아 소규모 병원과 레퍼런스 랩이 새로운 고객이 됩니다. 단일 튜브 라이브러리 구축을 위한 결합 효소 믹스는 작업 시간을 단축하고 오류율을 줄이고 브랜드 차별화를 촉진합니다. 신흥 CRISPR, 마이크로바이옴, 공간 생물학 키트는 '기타 제품 유형'의 테두리에 들어가 생명 과학 시약 업계에서 얼마나 빠른 연구 개발이 기존의 카탈로그 구조를 능가하는지 보여줍니다.

2024년에는 병원과 진단실이 생명과학 시약 시장 규모의 54.39%를 차지했지만, 2025-2030년 CAGR은 제약 및 바이오테크놀러지 기업이 가장 빠른 7.31%를 기록합니다. 격화하는 생물 제제 파이프라인은 지금까지 외주했던 분석의 내제화에 박차를 가하여 고순도 성장 인자, 수지 세트, 동반진단 키트의 구입을 촉진합니다. 아비의 2,177억 4,000만 달러의 연구개발비 배분은 업스트림 시약에 대한 헌신이 어떻게 치료에 대한 야망과 병행하는지를 명확하게 보여줍니다. 자동화를 중시하는 병원 실험실에서는 조달과 품질 감시를 통합한 시약 및 기기 번들이 선호되고 있습니다.

학술 기관은 국가 보조금에 의해 지원되는 신뢰할 수 있는 고객으로 남아 있습니다. NIH는 연간 410억 달러를 투자하고 있으며, 탐색 등급의 프라이머, 항체, 리포터 염료에 대한 기준선 수요를 유지하고 카탈로그의 폭을 확보하고 있습니다. '기타' 계약 연구 기관은 유연한 로트 크기와 신속한 리드 타임을 요구함으로써 대응 가능한 양을 확대하고 민첩한 재고 알고리즘으로 판매자에게 보상하고 있습니다.

지역 분석

2024년 생명과학 시약 시장 규모는 북미가 39.21%의 점유율로 선도했으며, 제약 메이저, 일류 연구 대학, 벤처 기업의 집적이 그 원동력이 되고 있습니다. ElevateBio의 13억 달러의 자금 조달로 대표되는 바와 같이, 대규모 시리즈 C 라운드는 거시 경제의 변화 하에서도 세포 치료 제품군에서 시약의 처리 능력을 유지합니다. FDA에 의한 규제의 예측가능성 및 강력한 지적재산권의 집행으로 다국적 공급업체는 대량 생산을 이 땅에서 유지하고 있습니다.

아시아태평양은 중국, 일본, 한국의 국가적 생명공학 계획을 배경으로 CAGR 7.55%로 확대될 전망이며, 가장 빠른 속도로 움직이고 있습니다. 까다로운 세액 공제와 공원 수준의 인프라가 대용량의 배지나 정제 수지를 현지 조달하는 개발 및 제조 수탁 기업을 매료하고 있습니다. ICH 가이드라인과의 정합은 이 지역에서 제조된 시약의 서유럽 고객에 대한 수출을 용이하게 하며, 역사적인 품질 인식의 갭을 해소합니다.

유럽은 Horizon Europe의 보조금이 선진 오믹스와 그린 케미스트리 시약 연구에 자금을 돌리기 때문에 한 자릿수 중반의 성장을 유지합니다. 그러나 체외진단용 의약품규제(In Vitro Diagnostic Regulation) 하에서의 컴플라이언스 강화가 소규모 실험실 예산을 압박하고 CE와 FDA의 기대를 동시에 충족하는 이중 인증 제품에 대한 구매 결정을 촉구하고 있습니다.

중동 및 아프리카에서는 각국 정부가 새로운 임상 유전체학 센터를 정비함에 따라 수주가 증가하고, 라틴아메리카에서는 브라질의 바이오시밀러 확대가 GMP 등급의 배지 및 크로마토그래피 솔루션에 대한 수요를 높이고 있습니다. 신흥 지역 전체에서는 온도 변화에 견디는 동결건조 키트가 인기를 끌고 생명과학 시약 시장 형식의 다양화 동향을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 감염증 부담의 증대

- 유전체학 및 단백질체학의 기술적 진보

- 연구개발 자금 증가 및 관민 파트너십

- 정밀 진단 및 맞춤형 의료에 대한 수요 증가

- AI를 활용한 시약의 전자상거래 및 온디맨드 합성

- 미세 유체 카트리지 기반 분산 시약 제조

- 시장 성장 억제요인

- 특수 시약의 고비용 및 가격 압력

- 엄격한 여러 지역의 규제 준수

- 중요한 효소 및 완충액의 업스트림 공급망의 불안정성

- PFAS 프리 제제를 향한 지속가능성의 추진에 의한 비용 및 복잡성의 증대

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 세포 및 조직 배양 시약

- 크로마토그래피 시약

- 임상 화학 시약

- 면역 측정 시약

- 분자진단 시약

- 미생물학 시약

- 단백질체학 및 단백질 분석 시약

- 차세대 시퀀싱(NGS) 시약

- 기타 제품 유형

- 최종 사용자별

- 병원 및 진단 실험실

- 학술기관 및 연구기관

- 제약 및 바이오테크놀러지 기업

- 기타

- 용도별

- 임상 진단

- 창약 및 의약품 개발

- 정밀 및 맞춤형 의료

- 법의학 및 보안 검사

- 기타

- 형태별

- 액체 시약

- 동결건조 시약

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche Ltd

- Thermo Fisher Scientific Inc.

- Becton, Dickinson and Company

- Abbott Laboratories

- bioMerieux SA

- Merck KGaA

- Danaher Corporation

- Siemens Healthineers

- DiaSorin SpA

- Sysmex Corporation

- Bio-Rad Laboratories

- Promega Corporation

- Agilent Technologies Inc.

- QIAGEN NV

- Illumina Inc.

- New England Biolabs

- PerkinElmer Inc.

- Lonza Group AG

- GenScript Biotech Corporation

- Takara Bio Inc.

- Waters Corporation

- Bruker Corporation

- Corning Incorporated

- Charles River Laboratories

제7장 시장 기회 및 전망

AJY 25.11.10The life science reagents market size stands at USD 68.74 billion in 2025 and is forecast to reach USD 94.21 billion by 2030, advancing at a 6.51% CAGR.

Robust uptakes in precision diagnostics, single-cell multiomics and automated laboratory workflows keep demand buoyant even as regulators tighten quality requirements. Hospital laboratories continue to place the largest orders, but pharmaceutical and biotechnology companies are expanding in-house usage as biologics pipelines become more complex. Rapid adoption of AI-guided reagent selection, growing investment in sustainable animal-free formulations and the reshoring of manufacturing capacity collectively protect the growth outlook against lingering supply-chain risks. Emerging disruptors are turning decentralised microfluidic cartridge production into a viable alternative to bulk supply, creating new price and service models that favour agile suppliers with digital logistics .

Global Life Science Reagents Market Trends and Insights

High Burden of Infectious Diseases

Global outbreaks keep molecular and immunoassay reagent volumes elevated. The FDA's flexible emergency-use guidance accelerates market entry for validated rapid-response kits, giving an edge to suppliers with ready-to-scale production platforms . Uptake of point-of-care systems in resource-limited regions is widening access, yet logistics and pricing hurdles persist. Manufacturers able to bundle reagents with compact detection devices gain share by simplifying field deployment. Continuing antimicrobial-resistance surveillance furthers demand for high-throughput PCR mastermixes and selective culture media suited to novel pathogen detection.

Technological Advancements in Genomics & Proteomics

Single-cell sequencing and spatial proteomics are setting new reagent performance benchmarks. Illumina's acquisition of Fluent BioSciences underscores strategic bets on scalable multiomics workflows, pushing suppliers to deliver ultra-low-input enzymes with consistent lot-to-lot kinetics . Automation-ready buffer systems that integrate with self-driving labs have shortened R&D cycles by more than 500 days, cutting reagent wastage and elevating premium SKUs. Vendors able to co-develop kits with instrument makers enjoy preferred-supplier status in expanding install bases.

High Cost & Pricing Pressure of Specialty Reagents

GMP-grade CRISPR components can cost 5-10 times their research-use equivalents, constraining adoption in budget-limited biotechs. Casgevy therapy's USD 2.2 million price tag demonstrates how reagent expenses cascade into final treatment costs. Lotus-to-plateau pricing dynamics encourage bulk purchasing, but consolidation among enzyme and antibody vendors narrows bargaining power for smaller buyers. Emerging plant-based cell-culture supplements that replace 90% of human platelet lysate hint at cost-relief pathways yet need broader validation.

Other drivers and restraints analyzed in the detailed report include:

- Rising R&D Funding & Public-Private Partnerships

- Growing Demand for Precision Diagnostics & Personalised Medicine

- Stringent Multi-Regional Regulatory Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cell and tissue culture reagents retained 29.92% of the life science reagents market share in 2024, a lead anchored in their indispensability to biomanufacturing workflows. The segment benefits from continuous upgrades toward chemically defined, xeno-free media that curb variability and immunogenicity. Companies such as Rohto Pharmaceutical are advancing serum-free stem-cell media that minimise product-to-product drift, commanding premium list prices in regenerative-medicine pipelines. Chromatography reagents post steady revenue underpinned by antibody purification demand, while clinical chemistry panels gain volume through laboratory automation. Molecular diagnostic reagents, projecting a 7.22% CAGR, outpace peers as liquid biopsy, NGS library prep, and microRNA detection protocols scale.

The molecular diagnostics surge illustrates how precision oncology elevates reagent complexity. Declining sequencing costs unlock smaller hospitals and reference labs as new customers. Coupled enzyme mixes for single-tube library construction slash hands-on time and shrink error rates, amplifying brand differentiation. Emerging CRISPR, microbiome and spatial biology kits populate the "other product types" bracket, showcasing how rapid R&D outpaces traditional catalog structures in the life science reagents industry.

While hospitals and diagnostic laboratories consumed 54.39% of the life science reagents market size in 2024, pharmaceutical and biotechnology companies will register the fastest 7.31% CAGR over 2025-2030. Intensifying biologics pipelines spur firms to internalise previously outsourced analytics, driving purchases of high-purity growth factors, resin sets and companion-diagnostic kits. AbbVie's USD 217.74 billion R&D allocation underscores how upstream reagent commitments parallel therapeutic ambitions. Automation-heavy hospital labs favour integrated reagent-instrument bundles that consolidate procurement and quality monitoring.

Academic institutes remain reliable customers backed by national grants. NIH's yearly USD 41 billion spend maintains baseline demand for discovery-grade primers, antibodies and reporter dyes, ensuring catalogue breadth retention. Contract research organisations within the "others" cohort widen addressable volumes by requesting flexible lot sizes and fast lead times, rewarding distributors with agile stocking algorithms.

The Life Science Reagents Market Report is Segmented by Product Type (Cell and Tissue Culture Reagents, Chromatography Reagents, and More), End User (Hospitals and Diagnostic Laboratories, and More), Application (Clinical Diagnostics, Drug Discovery and Development, and More), Form (Liquid Reagents, Lyophilized Reagents, Others), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the life science reagents market size with a 39.21% share in 2024, fuelled by a dense cluster of pharma majors, top-tier research universities and venture-backed start-ups. Substantial Series C rounds, exemplified by ElevateBio's USD 1.3 billion raise, maintain reagent throughput in cell-therapy suites even amid macroeconomic fluctuations. Regulatory predictability under the FDA and strong IP enforcement keep multinational suppliers anchoring bulk production here.

Asia-Pacific is the fastest mover, expanding at a 7.55% CAGR on the back of national biotech blueprints in China, Japan and South Korea. Generous tax credits and park-level infrastructure attract contract development-and-manufacturing organisations that source large-volume media and purification resins locally. Harmonisation with ICH guidelines eases export of region-made reagents to Western clients, closing historical quality-perception gaps.

Europe sustains mid-single-digit growth as Horizon Europe grants channel funds into advanced omics and green-chemistry reagent research. However, incremental compliance layers under the In Vitro Diagnostic Regulation stretch smaller laboratory budgets, nudging purchasing decisions toward dual-certified products that satisfy CE and FDA expectations simultaneously.

Middle East & Africa register rising orders as governments equip new clinical genomics centres, while Latin America benefits from Brazil's biosimilar expansion that raises demand for GMP-grade media and chromatography solutions. Across emerging regions, lyophilised kits capable of withstanding temperature excursions gain traction, underlining format diversification trends in the life science reagents market.

- Roche

- Thermo Fisher Scientific

- Beckton Dickinson

- Abbott Laboratories

- bioMerieux

- Merck

- Danaher

- Siemens Healthineers

- DiaSorin

- Sysmex

- Bio-Rad Laboratories

- Promega

- Agilent Technologies

- QIAGEN

- Illumina

- New England Biolabs

- PerkinElmer

- Lonza Group

- Genscript

- Takara Bio

- Waters Corporation

- Bruker

- Corning

- Charles River

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High burden of infectious diseases

- 4.2.2 Technological advancements in genomics & proteomics

- 4.2.3 Rising R&D funding & public-private partnerships

- 4.2.4 Growing demand for precision diagnostics & personalized medicine

- 4.2.5 AI-enabled reagent e-commerce & on-demand synthesis

- 4.2.6 Microfluidic cartridge-based decentralized reagent manufacturing

- 4.3 Market Restraints

- 4.3.1 High cost & pricing pressure of specialty reagents

- 4.3.2 Stringent multi-regional regulatory compliance

- 4.3.3 Upstream supply-chain volatility for critical enzymes & buffers

- 4.3.4 Sustainability push toward PFAS-free formulations increases cost & complexity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Cell and Tissue Culture Reagents

- 5.1.2 Chromatography Reagents

- 5.1.3 Clinical Chemistry Reagents

- 5.1.4 Immunoassay Reagents

- 5.1.5 Molecular Diagnostic Reagents

- 5.1.6 Microbiology Reagents

- 5.1.7 Proteomics and Protein Analysis Reagents

- 5.1.8 Next-Generation Sequencing (NGS) Reagents

- 5.1.9 Other Product Types

- 5.2 By End User

- 5.2.1 Hospitals and Diagnostic Laboratories

- 5.2.2 Academic and Research Institutes

- 5.2.3 Pharmaceutical and Biotechnology Companies

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Drug Discovery and Development

- 5.3.3 Precision and Personalized Medicine

- 5.3.4 Forensic and Security Testing

- 5.3.5 Others

- 5.4 By Form

- 5.4.1 Liquid Reagents

- 5.4.2 Lyophilized Reagents

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Abbott Laboratories

- 6.3.5 bioMerieux SA

- 6.3.6 Merck KGaA

- 6.3.7 Danaher Corporation

- 6.3.8 Siemens Healthineers

- 6.3.9 DiaSorin SpA

- 6.3.10 Sysmex Corporation

- 6.3.11 Bio-Rad Laboratories

- 6.3.12 Promega Corporation

- 6.3.13 Agilent Technologies Inc.

- 6.3.14 QIAGEN N.V.

- 6.3.15 Illumina Inc.

- 6.3.16 New England Biolabs

- 6.3.17 PerkinElmer Inc.

- 6.3.18 Lonza Group AG

- 6.3.19 GenScript Biotech Corporation

- 6.3.20 Takara Bio Inc.

- 6.3.21 Waters Corporation

- 6.3.22 Bruker Corporation

- 6.3.23 Corning Incorporated

- 6.3.24 Charles River Laboratories

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment