|

시장보고서

상품코드

1846301

동물용 치과 장비 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Veterinary Dental Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

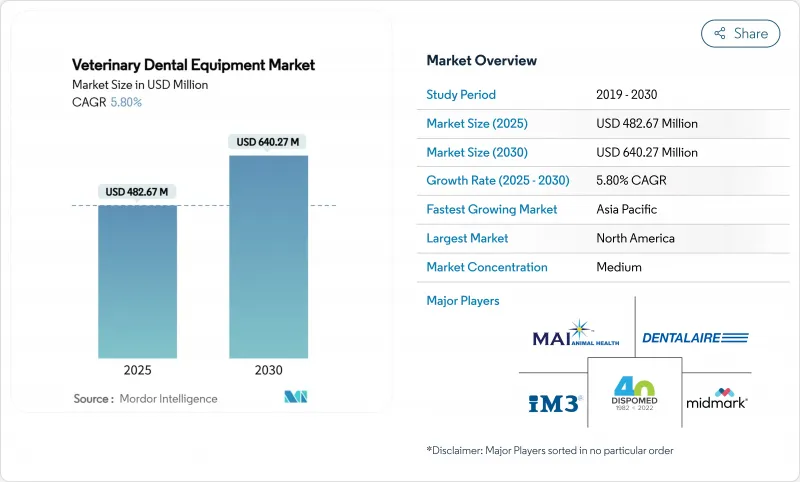

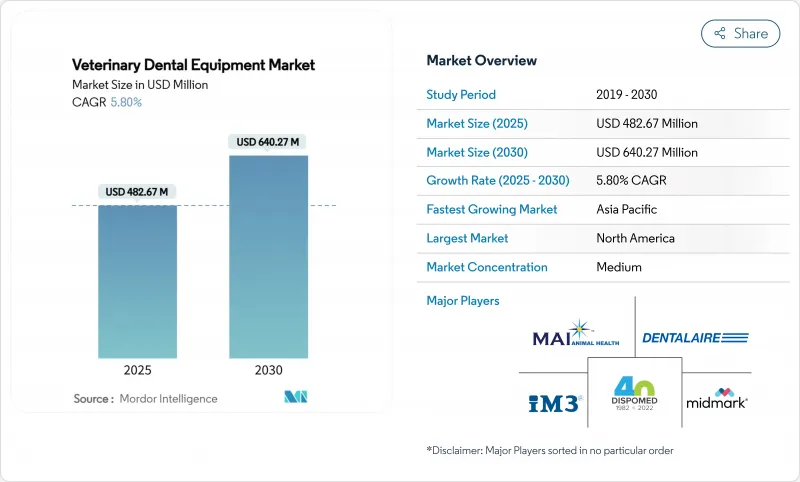

동물용 치과 장비 시장 규모는 2025년에 4억 8,267만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.80%로 성장할 전망이며, 2030년에는 6억 4,027만 달러에 달할 것으로 예측됩니다.

반려동물의 장수화, 치주병에 대한 의식의 고조, 예방 치과의 상시화가, 안정된 기기 판매를 지지하는 내구성이 있는 수요 패널을 형성하고 있습니다. 클리닉에서는 의자의 수용 대수를 늘리고 워크플로우를 중시한 레이아웃을 채용함으로써 처치 시간을 단축하고 기기의 평균 지출액을 밀어 올리고 있습니다. 청소, 발치, 치아 치료에도 보험이 적용된 반려동물 보험은 고가의 디지털 X선 촬영 장치 및 전동 핸드피스의 교체 사이클을 가속화하고 있습니다. 동시에 신흥 시장에서 집단 예방 접종을 목적으로 한 휴대용 필드 키트는 처음 구매하는 사람의 구매 파이프라인을 확장하고 있습니다.

세계의 동물용 치과 장비 시장 동향 및 인사이트

공인 수의사 치과 진료소 급증

2024년에는 미국 수의치과대학의 디플로메이트 지역 클러스터가 220개를 넘어 일반 진료소가 화상 처리와 고속 계기를 업그레이드하는 동기가 되는 도입의 흐름이 증가합니다. 기업 공급업체는 핸즈온 워크숍을 장비 번들에 통합하여 임상 습득이 하드웨어 수요를 유발하는 선순환을 창출하고 있습니다. 이 촉진요인의 영향은 2차 도시에서 가장 강하며, 조기 도입자가 인근의 5-7채의 치과 진료소에 신속하게 영향을 미치고 점차 동물용 치과 장비 시장이 활성화됩니다.

말 병원에서 디지털 치과 래디오그래피 보급 확산

대형 두개골을 위해 설계된 직접 디지털 플레이트는 즉각적인 진단과 재촬영률을 줄여 말 병원의 필름 시스템으로부터 철수를 촉구합니다. 2025년 연구에서는 일반적인 병변을 확인할 때 인공지능 소프트웨어가 공인 치과의사와 높은 평가자 간 일치를 보였습니다. 감도는 아직 인간의 전문 지식에 미치지 못하지만, 이 기술은 치료 계획을 충실히 해, 독영 시간을 단축하기 위해, 동물용 치과 장비 시장에서의 디지털 센서와 콘솔의 이용률을 높이고 있습니다.

Tier 1 도시 이외에서 전문 치과 의사 부족

대도시권의 허브 도시 이외에서는 전문의의 존재가 한정되어 있기 때문에 고도의 기술에 접할 기회가 적고, 프리미엄 유닛의 도입이 늦어지고 있습니다. 지리적 접근에 관한 조사는 반도시 지역의 클리닉에서 장비의 도입을 억제하는 심각한 케어 갭을 보여줍니다. 공급업체는 단순화된 통제와 원격 코칭으로 대응하고 있지만, 전문의의 지속적인 부족은 여전히 광범위한 동물용 치과 장비 시장의 발을 끌고 있습니다.

부문 분석

수기구는 동물용 치과 장비 시장의 39.7%를 차지했으며, 개업의가 종 특이적인 병리학에 대응하기 위해 색으로 구분된 스케일러, 큐렛, 날개 부착 엘리베이터를 채용함에 따라 CAGR 7.0%로 진전하고 있습니다. 3세 이상의 개의 80-90% 이상에 치주 병변이 보이기 때문에 첨단 미세 기구가 불가결합니다. 공급업체는 현재 운영자의 피로를 완화하는 인체 공학적 실리콘 핸들을 제공하고 있으며, 클리닉은 레거시 세트를 더 자주 교체합니다. 조명기구와 돋보기는 인간의 치과 치료에서 마이크로 서젤리 기술로의 전환으로 견조한 증가 수요를 유지하고 있습니다. 한편, 폐기물 관리 액세서리는 동물용 치과 장비 시장 전반에 걸쳐 감염 관리 기준이 강화되어 규제를 훈풍을 받고 있습니다.

디지털 엑스레이 콘솔, 센서, 위치 결정 보조 장치는 판매의 약 1/4을 차지하며 필름 사용자의 꾸준한 전환으로 이익을 얻고 있습니다. 반려동물 보험과 전문의의 도입이 겹치는 곳에서는 시프트가 가속되어, 수술의 복잡성 및 화상 투자의 관련성이 부각되고 있습니다. 최근에는 교합압에 강한 동물 전용 구강내 센서가 출시되어 장기 내구성에 대한 신뢰가 높아지고 동물용 치과 장비 시장의 반복 구매가 촉진되고 있습니다.

화상 진단은 2024년 매출의 34%를 차지했으며, 진료소에서는 실시간으로 주인과 상담할 수 있는 체어사이드 모니터가 내장되어 있습니다. 성견에서는 견치의 유병률이 80%를 초과하기 때문에 최대 사례수를 유지하는 치주병 치료는 피드백 루프에 의해 보다 높은 수용성을 촉진합니다. 파워 엘리베이터와 정밀 버서를 갖춘 발치 키트는 외상이 적고 치유가 빠르기 때문에 일반 개업의에게도 널리 사용되고 있습니다. 예방용 폴리싱 헤드, 불소 젤, 실란트는 경상적인 소모품 수입이 되어 동물용 치과 장비 시장에서 장기적인 고객 유지를 지원합니다.

복구 치료 및 치내 치료는 한때 도입 센터에 국한되었지만 교육 자료가 신뢰할 수있는 결과를 보이면서 지지를 얻었습니다. 인간의 치과 치료에서 전용된 복합 주사기와 광중합 핸드피스는 주인의 감정을 따르는 치아 보존 치료를 가능하게 합니다. 이국적인 동물의 치과 치료는 특수 마이크로 바의 필요성을 강조합니다. 2024년에 실시된 토끼의 연구에서는 구강내 수술 중 합병증 발생률이 41%였기 때문에 혁신가가 현재 타겟으로 하고 있는 기기의 갭이 부각되고 있습니다. 이러한 각 하위 부문은 동물용 치과 장비 시장을 지원하는 서비스의 범위를 확장하고 있습니다.

세계의 동물용 치과 장비 시장은 장비 유형별(치과용 스테이션, 치과용 엑스레이 시스템, 치과용 전동 유닛, 치과용 레이저, 치과용 전기 수술 유닛 등), 소모품별(치과용품, 프로파일 제품 등), 지역별(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)로 구분됩니다. 위 부문의 금액은 달러로 표시됩니다.

지역별 분석

북미는 매출 점유율 42.3%로 선두를 유지하며 클리닉당 기기 밀도는 평균을 웃돌았습니다. 전문의 집적, 보험 보급, 장비 인증의 의무화로 인해 유리한 수요 프로파일이 형성됩니다. 2021-2031년 치과 의사 자격 취득 후 기술자 등록률은 20% 상승할 것으로 예측되며 수술실 증설을 정당화하는 숙련 노동력이 추가됩니다. 클리닉은 의자를 1대에서 2대로 업그레이드하여 부동산을 확대하지 않고 실질적으로 생산 능력을 두배로 늘려 동물용 치과 장비 시장에 대한 설비 투자를 뒷받침하고 있습니다.

아시아태평양은 CAGR 7.3%와 가장 빠른 성장을 이루며 가처분 소득 상승 및 반려동물 사육이 대도시에 집중하는 급속한 도시화에 힘쓰고 있습니다. 중국, 일본, 한국은 프리미엄 구매의 중심이며 인도와 동남아시아 국가들은 혼합 진료 환경에 적합한 휴대용 키트의 첫 번째 파도 채택을 보여줍니다. 정부가 자금을 제공하는 광견병 캠페인은 경구 검진을 통합하여 현장 수의사에게 장비의 이점을 알렸습니다. 이 경험은 미래의 민간 수요의 씨앗이 되고 동물용 치과 장비 시장이 확대될 것입니다.

유럽은 성숙하면서도 혁신 지향적인 지역이며, 엄격한 안전 기준이 공인 공급업체를 지지하고 있습니다. 가격의 투명성은 다양합니다. 2024년 여러 국가에 의한 조사는 수수료 흔들림이 크고 새로운 하드웨어의 투자 회수 모델에 영향을 미치는 것으로 기록되었습니다. 수수료가 많은 지역의 클리닉은 더 빨리 프리미엄 이미징을 도입하고 요금이 낮은 지역은 점차적으로 도입되고 있습니다. 라틴아메리카와 중동 및 아프리카의 점유율은 전반적으로 소폭이지만 도시 지역에서는 고성장을 볼 수 있습니다. 라틴아메리카에서는 위조품의 만연과 불균일한 단속이 확대를 억제하고 있습니다. 한편, 아프리카에서는 엘리트 소유자가 소규모 수요 클러스터를 유지하고 있으며, 인프라 제약이 많은 하위 시장을 제약하고 있습니다. 이러한 역학을 종합하면 세계 동물용 치과 장비 시장의 성숙도가 다양하다는 것을 알 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 성장 촉진요인

- 북미의 인정 수의 치과 진료소 급증

- 말 병원에서 디지털 덴탈 X선 촬영의 보급(미국 및 영국)

- 유럽에서 치과 치료를 커버하는 반려동물 보험 확대

- 정부 주최의 광견병 집단 예방 운동이 아시아에서의 정기적 구강 체크 유발

- 고양이 전용의 저침습 치과 기구 라인 발매

- 지방의 반려동물 클리닉을 위한 원격 치과 트리아지 플랫폼의 성장

- 시장 성장 억제요인

- 신흥 시장에서 CBCT와 고도의 화상 처리의 높은 초기 비용

- Tier-1 도시 이외의 수의사 부족

- 라틴아메리카에서의 그레이 마켓 수입 및 비인증 기기

- 북유럽에서 말 치과 진료의 상환 제한

- 밸류체인 및 공급망 분석

- 규제 및 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액 및 수량)

- 제품별

- 기기

- 치과용 X선 시스템

- 덴탈 스테이션 및 딜리버리 유닛

- 초음파 및 압전 스케일러

- 고속 및 저속 핸드피스

- 전기 수술 및 레이저 유닛

- 기타 기기(구강내 카메라, 컴프레서)

- 핸드 기구

- Extraction(엘리베이터, 럭셔터)

- 치주 기구(스케일러, 큐렛, 프로브)

- 수복 기구

- 교정 기구

- 보조제 및 액세서리

- 기구 카세트 및 멸균 트레이

- 조명 및 확대 시스템

- 배설 관리 및 흡입 액세서리

- 기기

- 동물 유형별

- 반려동물

- 개

- 고양이

- 말

- 기타 반려동물

- 가축

- 소

- 돼지

- 반려동물

- 최종 사용자별

- 동물병원

- 수의 전문 및 도입 센터

- 동물 클리닉

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- iM3 Veterinary Dentistry

- Midmark Corporation

- Henry Schein, Inc.

- Dentalaire International

- Patterson Companies, Inc.

- Acteon Group Ltd.

- Planmeca Oy

- Integra LifeSciences Holdings Corp.

- Jorgen Kruuse A/S

- Eickemeyer Veterinary Equipment

- B. Braun Vet Care GmbH

- Covetrus, Inc.

- Dispomed Ltd.

- Heska Corporation

- DRE Veterinary

- Summit Veterinary Pharmacy

- Accesia AB

- Avante Animal Health

- Cislak

- VetDent

제7장 시장 기회 및 전망

AJY 25.11.10The Veterinary Dental Equipment Market size is estimated at USD 482.67 million in 2025, and is expected to reach USD 640.27 million by 2030, at a CAGR of 5.80% during the forecast period (2025-2030).

Rising pet longevity, growing awareness of periodontal disease, and the normalization of preventive dentistry have created a durable demand funnel that sustains steady equipment sales. Clinics are enlarging chair capacity and adopting workflow-centric layouts, which shortens procedure times and pushes average equipment spend higher. Pet insurance policies that now reimburse cleanings, extractions, and even endodontics are accelerating the replacement cycle for high-value digital radiography and powered handpieces. At the same time, portable field kits aimed at mass vaccination initiatives in emerging markets widen the intake pipeline for first-time buyers.

Global Veterinary Dental Equipment Market Trends and Insights

Surge in Board-Certified Veterinary Dentistry Practices

Regional clusters of American Veterinary Dental College diplomates surpassed 220 in 2024, multiplying referral flows that incentivize general practices to upgrade imaging and high-speed instrumentation. Corporate suppliers integrate hands-on workshops with equipment bundles, creating a virtuous loop where clinical mastery fuels hardware demand. The driver's impact is strongest in secondary cities, where early adopters quickly influence five to seven neighboring clinics to follow suit, gradually lifting the veterinary dental equipment market.

Rising Uptake of Digital Dental Radiography in Equine Hospitals

Direct digital plates engineered for large skulls enable immediate diagnostics and lower retake rates, encouraging equine practices to retire film systems. A 2025 study showed artificial-intelligence software reached high inter-rater agreement with board-certified dentists when identifying common lesions. Although sensitivity still trails human expertise, the technology enriches treatment planning and shortens reading times, raising utilization of digital sensors and consoles within the veterinary dental equipment market.

Shortage of Diplomate Dentists Beyond Tier-1 Cities

Limited specialist presence outside metropolitan hubs curbs exposure to advanced techniques, slowing adoption of premium units. Research on geographic access indicates significant care gaps that suppress equipment uptake in semi-urban clinics. Suppliers respond with simplified controls and remote coaching, but sustained specialist scarcity still drags on the broader veterinary dental equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Pet Insurance Policies Covering Dental Procedures

- Government-Sponsored Mass Rabies Drives

- Grey-Market Imports & Non-Certified Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hand instruments represent 39.7% of the veterinary dental equipment market and are advancing at a 7.0% CAGR as practitioners adopt color-coded scalers, curettes, and winged elevators for species-specific pathology. Over 80-90% of dogs older than three years present periodontal lesions, making fine-tip instruments indispensable. Vendors now offer ergonomic silicone handles that reduce operator fatigue, prompting clinics to replace legacy sets more frequently. Lighting and magnification tools maintain robust incremental demand due to the migration of microsurgical techniques from human dentistry, while waste-management accessories enjoy regulatory tailwinds as infection-control standards tighten across the veterinary dental equipment market.

Digital X-ray consoles, sensors, and positioning aids comprise roughly one-quarter of revenue and benefit from steady conversion of film users. The shift accelerates where pet insurance and specialist referrals overlap, underscoring the linked nature of procedural complexity and imaging investment. Recent launches of veterinary-specific intra-oral sensors hardened against bite pressure amplify confidence in long-term durability, fostering repeat purchases in the veterinary dental equipment market.

Diagnostic imaging accounts for 34% of 2024 revenue, with clinics integrating chairside monitors that allow real-time owner consultations. The feedback loop drives higher acceptance of periodontal therapy, which retains the largest case volume because canine prevalence exceeds 80% in adult dogs. Extraction kits featuring power elevators and precision burs deliver less trauma and faster healing, encouraging broader use even among general practitioners. Preventive polishing heads, fluoride gels, and sealants add recurring consumable revenue, anchoring long-term client retention within the veterinary dental equipment market.

Restorative and endodontic procedures, once confined to referral centers, gain traction as training materials demonstrate reliable outcomes. Composite syringes and light-curing handpieces adapted from human dentistry allow tooth-saving therapies that align with owner sentiment. Exotic-animal dentistry underscores the need for specialized micro-burs; a 2024 rabbit study cited 41% complication rates during intra-oral surgeries, highlighting equipment gaps that innovators now target. Each of these sub-segments keeps broadening the scope of services that underpin the veterinary dental equipment market.

Global Veterinary Dental Equipment Market is Segmented by Equipment Type (Dental Stations, Dental X-Ray Systems, Dental Powered Units, Dental Lasers, Dental Electrosurgical Units, and Others), Consumables (Dental Supplies, Prophy Products, Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The Value is Provided in (USD Million) for the Above Segments.

Geography Analysis

North America retains leadership with 42.3% revenue share and records above-average equipment density per practice. Specialist clusters, widespread insurance coverage, and mandatory device certifications create a favorable demand profile. Technician enrollment in dental post-certificates is projected to climb 20% from 2021-2031, adding skilled labor that justifies expanded operatory footprints. Clinics upgrade from single to dual chairs, effectively doubling capacity without enlarging real estate, which boosts capital investment in the veterinary dental equipment market.

Asia-Pacific posts the fastest growth, at a 7.3% CAGR, propelled by rising disposable incomes and rapid urbanization that concentrates pet ownership in megacities. China, Japan, and South Korea anchor premium purchases, while India and Southeast Asian nations exhibit first-wave adoption of portable kits suited to mixed-practice environments. Government-funded rabies campaigns integrate oral screenings, exposing field veterinarians to equipment benefits. This experience seeds future private-sector demand, expanding the veterinary dental equipment market.

Europe remains a mature yet innovation-oriented region where stringent safety standards favor certified suppliers. Price transparency varies: a 2024 multi-country study recorded wide fee swings, affecting payback models for new hardware. Clinics in higher-fee territories adopt premium imaging sooner, while lower-fee zones phase in gradually. Latin America and the Middle East-Africa collectively hold a modest share but display pockets of high growth in urban hubs. Counterfeit penetration and uneven enforcement temper expansion in Latin America, whereas infrastructure limitations constrain many African sub-markets, though elite owners sustain small clusters of demand. Collectively, these dynamics underscore the varied maturity levels across the global veterinary dental equipment market.

- iM3 Veterinary Dentistry

- Midmark

- Henry Schein

- Dentalaire International

- Patterson Companies

- Acteon Group Ltd.

- Planmeca

- Integra LifeSciences Holdings Corp.

- Jorgen Kruuse A/S

- Eickemeyer Veterinary Equipment

- B. Braun

- Covetrus

- Dispomed

- Heska

- DRE Veterinary

- Summit Veterinary Pharmacy

- Accesia AB

- Avante Health Solutions

- Cislak

- VetDent

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Surge in Board-Certified Veterinary Dentistry Practices in North America

- 4.1.2 Rising Uptake of Digital Dental Radiography in Equine Hospitals (U.S. & U.K.)

- 4.1.3 Expansion of Pet Insurance Policies Covering Dental Procedures in Europe

- 4.1.4 Government-Sponsored Mass Rabies Drives Triggering Routine Oral Check-ups in Asia

- 4.1.5 Launch of Feline-Specific Minimally-Invasive Dental Instrument Lines

- 4.1.6 Growth of Tele-Dentistry Triage Platforms for Rural Companion-Animal Clinics

- 4.2 Market Restraints

- 4.2.1 High Up-Front Cost of CBCT & Advanced Imaging in Emerging Markets

- 4.2.2 Shortage of Diplomate Veterinary Dentists Beyond Tier-1 Cities

- 4.2.3 Grey-Market Imports & Non-Certified Equipment in Latin America

- 4.2.4 Limited Reimbursement for Equine Dental Services in the Nordics

- 4.3 Value/ Supply-Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Product

- 5.1.1 Equipment

- 5.1.1.1 Dental X-ray Systems

- 5.1.1.2 Dental Stations & Delivery Units

- 5.1.1.3 Ultrasonic & Piezo Scalers

- 5.1.1.4 High- & Low-Speed Handpieces

- 5.1.1.5 Electrosurgical & Laser Units

- 5.1.1.6 Other Equipment (Intra-oral Cameras, Compressors)

- 5.1.2 Hand Instruments

- 5.1.2.1 Extractions (Elevators, Luxators)

- 5.1.2.2 Periodontal Instruments (Scalers, Curettes, Probes)

- 5.1.2.3 Restorative Instruments

- 5.1.2.4 Orthodontic Instruments

- 5.1.3 Adjuvants/Accessories

- 5.1.3.1 Instrument Cassettes & Sterilization Trays

- 5.1.3.2 Lighting & Magnification Systems

- 5.1.3.3 Waste Management & Suction Accessories

- 5.1.1 Equipment

- 5.2 By Animal Type

- 5.2.1 Companion Animals

- 5.2.1.1 Canines

- 5.2.1.2 Felines

- 5.2.1.3 Equines

- 5.2.1.4 Other Companion Animals

- 5.2.2 Livestock

- 5.2.2.1 Bovines

- 5.2.2.2 Swine

- 5.2.1 Companion Animals

- 5.3 By End User

- 5.3.1 Veterinary Hospitals

- 5.3.2 Veterinary Specialty & Referral Centers

- 5.3.3 Veterinary Clinics

- 5.3.4 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Rest of Asia-Pacific

- 5.4.2.1 China

- 5.4.2.2 Japan

- 5.4.2.3 India

- 5.4.2.4 South Korea

- 5.4.2.5 Australia

- 5.4.2.6 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 iM3 Veterinary Dentistry

- 6.3.2 Midmark Corporation

- 6.3.3 Henry Schein, Inc.

- 6.3.4 Dentalaire International

- 6.3.5 Patterson Companies, Inc.

- 6.3.6 Acteon Group Ltd.

- 6.3.7 Planmeca Oy

- 6.3.8 Integra LifeSciences Holdings Corp.

- 6.3.9 Jorgen Kruuse A/S

- 6.3.10 Eickemeyer Veterinary Equipment

- 6.3.11 B. Braun Vet Care GmbH

- 6.3.12 Covetrus, Inc.

- 6.3.13 Dispomed Ltd.

- 6.3.14 Heska Corporation

- 6.3.15 DRE Veterinary

- 6.3.16 Summit Veterinary Pharmacy

- 6.3.17 Accesia AB

- 6.3.18 Avante Animal Health

- 6.3.19 Cislak

- 6.3.20 VetDent

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment