|

시장보고서

상품코드

1846303

상처 치료용 생물제제 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Wound Care Biologics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

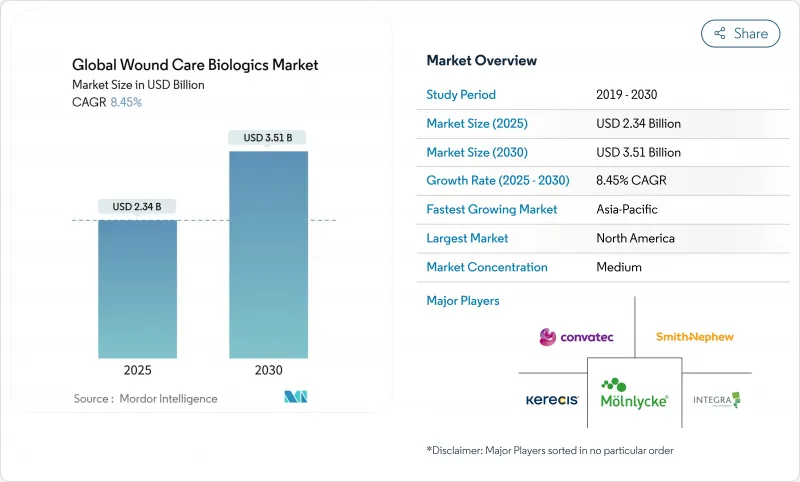

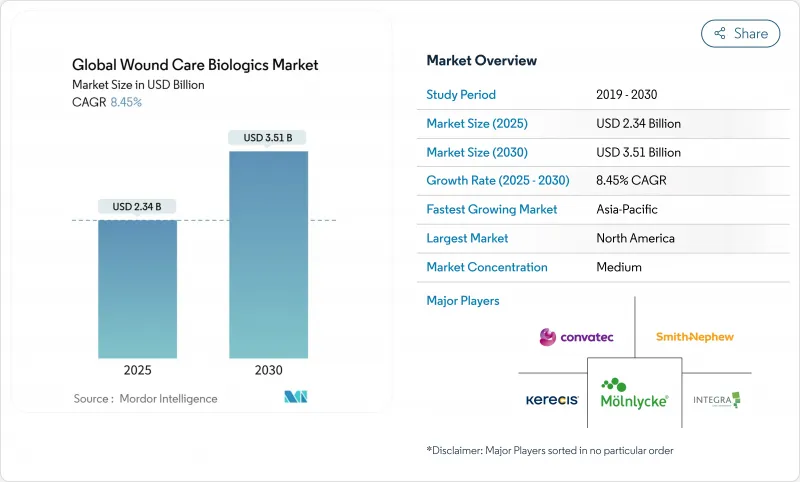

상처 치료용 생물제제 시장은 2025년에 23억 4,000만 달러로 추정되고, 2030년에는 CAGR 8.45%로 성장할 전망이며, 35억 1,000만 달러로 확대될 것으로 예측됩니다.

이 기세는 생물학적 매트릭스, 이종이식편, 성장인자 드레싱재가 기존의 드레싱재에 비해 치유 기간을 단축하고 감염 위험을 감소시키는 임상 증거의 확대에 기인하고 있습니다. 2025년 4월 메디케어 및 메디케이드 서비스 센터(CMS)가 발행한 강제 적용 판정(LCD)은 상환이 승인되기 전에 4주 이내에 상처 면적이 50% 감소했음을 입증해야 합니다. FDA가 항균성 드레싱재를 보다 엄격한 기기 클래스로 다시 분류할 계획이기 때문에 제조업체 각사는 내성을 완화하는 기능을 우선하게 되어 제품의 기술 혁신이 격화하고 있습니다. 한편, 미국 국방부의 16억 6,000만 달러의 화학 및 생물학적 방위 프로그램 예산은 외상용 생물 제제의 전장에서 침대 사이드로의 이행을 가속화하고 있습니다.

세계의 상처 치료용 생물제제 시장 동향 및 인사이트

당뇨병성 발궤양의 유병률 증가

당뇨병 이환율이 증가함에 따라 만성 궤양은 납부자와 의료 제공업체에게 항상 가장 중요한 과제가 되고 있습니다. CMS는 현재 생물제제에 의한 드레싱 재료를 보험 적용하기 전에 표준 치료 4주 후 면적이 50% 감소한 것을 증명할 것을 요구하고 있으며, 생물제제를 단계적 치료 프로토콜에 통합하여 무작위화 시험 데이터가 있는 제형에 보상을 주고 있습니다. 혈소판 유래 성장 인자 겔은 기존의 드레싱재의 25%에 비해 48%의 완전 치유율을 나타내고 있으며, 이 차이는 가치 기반의 구매에 영향을 미치고 있습니다. 염기성 섬유아세포 증식 인자를 재빨리 채용한 일본은 규제와 상환이 수렴했을 때의 상업적인 돌연변이를 보강하고 있습니다. 아시아태평양은 고령화가 진행되고 있으며, 당뇨병이 급증하고 있기 때문에 수요 곡선은 더욱 강해지고 있습니다. 외래 상처 센터의 병행 성장은 치유가 빠른 생물제제를 구입하여 외래 처방을 보장합니다.

화상 및 교통사고 발생률 증가

노동재해 및 기후 관련 재해 증가에 의해 열상은 2030년까지 CAGR 9.75%로 가장 급속하게 성장이 전망되는 상처 유형이 되고 있습니다. 응급 부문은 감염 위험을 줄이고 육아 형성을 촉진하는 생물학적 매트릭스로 전환하고 있습니다. 전장 외상에 대한 식물 유래 Traumagel의 FDA 인가는 방위 주도 생명 공학이 민간에서 채택되고 있음을 뒷받침합니다. 구리 함침 매트릭스는 상처 폐쇄 속도로 기존의 실버 드레싱 재료를 초과하여 25개국 이상에서 승인되었습니다. 신흥 시장의 외상 치료 기기에서는 콜드체인 물류를 최소화하면서 높은 상피화율을 실현하는 비용 효율적인 이종 이식편이 선호되고 있습니다.

높은 수술 비용 및 제품 비용

미국에서는 매년 968억 달러가 만성 상처의 치료에 소비되고 있지만, 진료 보수의 상한이 있기 때문에 임상의는 환자 간에 생물제제의 배분을 결정해야 합니다. LCD는 12-16주간의 에피소드로 최대 8회 사용으로 제한되어 있기 때문에 그 기간 내에 완전히 치유될 가능성에 따라 제품을 선택할 수밖에 없습니다. 2024년 상반기 컨버텍 상처 케어 사업의 매출 성장률 6.7%는 예산이 압박되는 가운데 경쟁 가격의 생물제제가 점유율을 획득할 수 있음을 보여줍니다. 신흥 시장에서는 현지 구매력에 맞는 가격 설정 모델이 시장 진입에 필수적입니다.

부문 분석

2024년 상처 치료용 생물제제 시장 점유율은 37.78%로, 외과의사의 보급과 재건 요구에 대한 지불자 부담에 지지되고 있습니다. 케레시스 등 어피의 개척자가 추진하는 이종이식편은 CAGR 10.82%로 확대되어 다른 모든 카테고리를 능가하고 있습니다. 태반과 양막은 조직 은행의 감시가 강화되고 처방위원회가 안정적인 공급을 약속하는 합성 비계로 방향타를 끊었기 때문에 일시적인 부족에 직면하고 있습니다. FDA가 인가한 성장 인자 제제는 1유형(Regranex)만으로 새로운 항균 기준을 충족하면서 고감도 단백질을 안정화할 수 있는 차세대 캐리어가 요구되고 있습니다.

성장 인자 스프레이는 삼출성 상처에서 생물학적 활성을 연장시키기 위해 폴리머 마이크로캡슐을 사용하여 재조합되고 있습니다. 하이브리드 생합성 드레싱 소재는 실리콘 배킹과 물고기 스킹 래프트를 결합하여 수분 균형을 희생하지 않고 신속한 배수를 가능하게 합니다. 병원의 가치분석위원회는 생물학적 매트릭스를 조기에 사용함으로써 재원 일수를 단축할 수 있어 보다 고액의 구입가격에 대한 정당성을 증명합니다. 이종이식편 공급업체는 당뇨병성 발궤양, 욕창, 종양절제와 같은 질병별 프로토콜을 중시하고 증거 기반 구매에 공명하는 표적 클리니컬 경로를 제공합니다. 지급측의 감사가 강화됨에 따라 4주 이내에 50%의 면적 축소를 증명할 수 있는 제품이 코딩 우선순위를 확보하게 되어 상처 치료용 생물제제 시장의 부문 계층이 강화되고 있습니다.

궤양은 2024년 상처 치료용 생물제제 시장 규모의 62.94%를 차지했으며, 상처 치료용 생물제제 시장에서의 우위성이 확인되었습니다. 그 중에서도 당뇨병성 발궤양은 세계적인 당뇨병 증가로 최대 환자수를 차지하고 있습니다. CMS의 LCD는 표준 치료가 과거에 효과가 없었음을 증명할 필요가 있기 때문에 생물제제는 난치성 궤양 환자군에 효과적으로 사용됩니다. 이와는 대조적으로, 열상 CAGR은 9.75%로 상처 치료용 생물제제 업계에서 가장 급속한 성장을 보이고 있습니다.

외상 센터가 제1선택 프로토콜에 생물제제를 통합하기 때문에 화상을 적응시키는 상처 치료용 생물제제 시장 규모는 2030년까지 두배로 될 것으로 예측됩니다. 구리를 배합한 매트릭스는 은의 드레싱재보다 상피화성 시간이 짧아, 이 지견은 현재 25의 규제 당국에서 재현되고 있습니다. 가혹한 환경에 적합한 군용 하이드로겔이 지역의 ER에 보급되어 열상 분야의 기세를 강화하고 있습니다. 반대로 장기 요양 환경에서의 욕창은 비용 감쇠형의 생물학적 제형을 필요로 하고, 공급업체는 간병 시설 네트워크와의 수량 기준 계약을 추진하고 있습니다.

상처 치료용 생물제제 시장은 제품 유형별(생물학적 피부대용제, 외용제), 상처 유형별(궤양, 수술창, 외상창, 열상), 최종 사용자별(병원 및 진료소, 외래수술센터, 기타 최종 사용자), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 구분됩니다.

지역 분석

2024년 상처 치료용 생물제제 시장 규모의 44.92%를 북미가 차지한 것은 성숙한 지불자 틀과 생물제제에 대한 폭넓은 임상 지식이 배경에 있습니다. 그러나 보급이 한계 수준에 가까워짐에 따라 예측 성장률은 CAGR 8.15%로 감속합니다. VA와 KCI USA 간의 3억 4,000만 달러의 계약은 공식 형성에서 정부의 힘을 강조합니다. 캐나다에서는 캐나다 보건부(Health Canada)와 미국 식품의약국(FDA)의 상호 협정을 활용하여 승인을 가속화하고, 멕시코 민간 병원에서는 미국에서 승인된 어피 이식편을 수입하여 자비 진료 환자에 대응하고 있습니다.

유럽은 통일된 신청서를 이용해 27개 주에서 판매할 수 있는 CE 마크의 하모나이제이션에 지지되어 CAGR 8.46%로 성장을 지속하고 있습니다. 독일과 영국은 여전히 판매량의 중심이지만 긴축 재정 예산이 완화됨에 따라 남유럽은 더 빠른 성장률을 보이고 있습니다. 가치 기반 조달 컨소시엄은 단가보다 폐쇄에 드는 총 비용을 비교하고 임상시험을 뒷받침하는 치유율이 높은 생물 제제를 선호합니다. 스칸디나비아의 의료제도는 2년마다 상환의 재조정을 실시하는 실임상 등록을 선도하고 있습니다.

아시아태평양은 CAGR 10.29%로 성장을 이끌었습니다. 중국은 건강 중국 2030 계획의 일환으로 수백 개의 현립 병원에 이종 이식을 위한 화상 치료실을 설치합니다. 일본에서는 염기성 섬유아세포 성장 인자의 오랜 역사가 새로운 생물제제의 수용을 용이하게 하고, 인도에서는 다단계 가격 콜리도가 콜라겐 매트릭스의 국내 생산을 장려하고 있습니다. 호주 Medicare Benefits Schedule은 새롭게 외래 생물제제의 드레싱 검토에 적용되어 지역에서의 사용을 확대하고 있습니다. 이러한 움직임을 종합하면 향후 수익의 비중이 아시아로 이동하여 상처 치료용 생물제제 시장의 지리적 확산이 다양해질 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당뇨병성 발궤양의 유병률 증가

- 첨단 상처 치료에 대한 정부의 상환제도 확대

- 화상 및 교통사고 발생률 증가

- 어피 이종이식편의 채용 증가

- 전장 및 재해 대응에 있어서 생물제제의 조달 급증

- 입원 환자로부터 외래 환자로의 상처 센터 시프트가 생물제제 처방에 대한 도입 촉진

- 시장 성장 억제요인

- 높은 절차 비용 및 제품 비용

- 엄격한 조직은행 규제

- 태반 및 양막 원료 공급망 취약성

- 생물제제 드레싱에 대한 항균제 내성의 향상

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 세포성 진피 매트릭스

- 양막 및 태반막

- 이종이식편

- 합성 및 생합성 스캐폴드

- 성장 인자 및 세포 기반 외용제

- 기타 제품

- 상처 유형별

- 궤양

- 당뇨병성 발궤양

- 정맥성 궤양

- 욕창

- 기타 궤양

- 수술창 및 외상창

- 열상

- 궤양

- 판매 채널별

- 온라인

- 오프라인

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 재택치료

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Avita Medical

- B. Braun Melsungen AG

- Bioventus Inc.

- Coloplast A/S

- Convatec Group plc

- Essity AB

- Grifols SA

- Integra LifeSciences

- Kerecis Ehf

- Lynch Biologics

- Marine Polymer Technologies

- Medline Industries

- MiMedx Group Inc.

- Molnlycke AB

- MTF Biologics

- Organogenesis Holdings

- Skye Biologics Holdings

- Smith & Nephew plc

- Solventum Corporation

- Stryker Corporation

제7장 시장 기회 및 전망

AJY 25.11.10The wound care biologics market reached USD 2.34 billion in 2025 and is set to rise to USD 3.51 billion by 2030, reflecting an 8.45% CAGR.

Momentum stems from expanding clinical evidence that biologic matrices, xenografts, and growth-factor dressings shorten healing time and reduce infection risk compared with conventional dressings. Mandatory Local Coverage Determinations (LCDs) issued by the Centers for Medicare & Medicaid Services (CMS) in April 2025 require proof of 50% wound-area reduction within four weeks before reimbursements are approved, which weeds out marginal products and redirects budgets toward options with published outcomes. Product innovation is intensifying, guided by FDA plans to reclassify antimicrobial dressings into stricter device classes, prompting manufacturers to prioritize resistance-mitigation features. Meanwhile, the U.S. Department of Defense's USD 1.66 billion Chemical and Biological Defense Program budget accelerates battlefield-to-bedside translation of trauma-oriented biologics.

Global Wound Care Biologics Market Trends and Insights

Growing Prevalence of Diabetic Foot Ulcers

Escalating diabetes incidence keeps chronic ulcers front-of-mind for payers and providers. CMS now requires a documented 50% area reduction after four weeks of standard care before covering biologic dressings, anchoring biologics in step-therapy protocols, and rewarding formulations with randomized-trial data. Platelet-derived growth-factor gels show 48% complete-healing rates versus 25% with conventional dressings, a difference that resonates in value-based purchasing. Japan's early adoption of basic fibroblast growth factor reinforces the commercial payoff when regulation and reimbursement converge. Asia-Pacific's population is aging, and surging diabetes prevalence intensifies demand curves. Parallel growth of outpatient wound centers channels purchasing toward biologics with quick-healing properties, ensuring formulary placement in ambulatory settings.

Increasing Incidence of Burns & Road-Traffic Injuries

Rising industrial accidents and climate-related disasters have pushed burns to the fastest-growing wound type at a 9.75% CAGR to 2030. Emergency departments are moving toward biologic matrices that lower infection risk and accelerate granulation. FDA clearance of plant-based Traumagel for battlefield trauma underscores civilian adoption of defense-driven biotech. Copper-impregnated matrices outpace traditional silver dressings in wound-closure speed and have earned approvals in more than 25 countries. Emerging-market trauma units favor cost-efficient xenografts that require minimal cold-chain logistics yet deliver high epithelialization rates.

High Procedure & Product Cost

The United States spends USD 96.8 billion each year treating chronic wounds, yet reimbursement caps force clinicians to ration biologics across patients. LCDs restrict usage to eight applications within 12-to-16-week episodes, compelling product selection based on probability of full closure within that window. ConvaTec's 6.7% wound-care revenue growth in the first half of 2024 shows that competitively priced biologics can still win share amid budget pressure. In emerging markets, tiered-pricing models that align with local purchasing power are becoming critical for market entry.

Other drivers and restraints analyzed in the detailed report include:

- Government Reimbursement Expansions for Advanced Wound Care

- Surge in Battlefield & Disaster-Response Procurement of Biologics

- Stringent Tissue-Bank Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acellular dermal matrices retained a 37.78% wound care biologics market share in 2024, buoyed by widespread surgeon familiarity and payer coverage for reconstructive needs. Xenografts-propelled by fish-skin pioneers such as Kerecis-are expanding at a 10.82% CAGR, outpacing all other categories. Placental and amniotic membranes face episodic shortages as tissue-bank scrutiny intensifies, steering formulary committees toward synthetic scaffolds that promise consistent supply. FDA clearance of only one growth-factor product (Regranex) leaves a white space for next-generation carriers able to stabilize sensitive proteins while meeting new antimicrobial standards.

Growth-factor sprays are being reformulated with polymer micro-capsules to prolong bioactivity in exudative wounds. Hybrid biosynthetic dressings combine silicone backings with fish-skin grafts, enabling rapid drainage without sacrificing moisture balance. Within hospital value-analysis committees, total cost-of-care calculators highlight shorter length-of-stay when biologic matrices are deployed early, helping justify higher acquisition prices. Xenograft suppliers emphasize disease-specific protocols-diabetic foot ulcers, pressure injuries, and oncology excisions-providing targeted clinical pathways that resonate with evidence-based purchasing. As payer audits intensify, products capable of delivering documented 50% area reduction within four weeks will secure coding priority, reinforcing the segment hierarchy inside the wound care biologics market.

Ulcers represented 62.94% of the wound care biologics market size in 2024, confirming their primacy in the wound care biologics market. Within that group, diabetic foot ulcers account for the largest patient pool owing to global diabetes escalation. CMS's LCD requires proof of prior standard-care failure, effectively channeling biologic spend toward refractory ulcer cohorts. In contrast, burns are on a 9.75% CAGR trajectory-the swiftest within the wound care biologics industry-driven by rising factory incidents in Asia and heat-related disasters elsewhere.

The wound care biologics market size for burn indications is expected to double by 2030 as trauma centers integrate biologics into first-line protocols. Copper-infused matrices deliver shorter epithelialization times against silver dressings, a finding now replicated across 25 regulatory jurisdictions. Military-origin hydrogels suitable for austere settings have migrated to community ERs, reinforcing the burn segment's momentum. Conversely, pressure ulcers in long-term care settings require cost-attenuated biologics, pushing suppliers toward volume-based contracts with nursing-home networks.

The Wound Care Biologics Market is Segmented by Product (Biological Skin Substitutes and Topical Agents), Wound Type (Ulcers, Surgical and Traumatic Wounds and Burns), End User (Hospitals/Clinics, Ambulatory Surgical Centers and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America).

Geography Analysis

North America's 44.92% of the wound care biologics market size in 2024 rested on mature payer frameworks and broad clinical familiarity with biologics. Yet forecast growth moderates to an 8.15% CAGR as penetration approaches ceiling levels. The VA's USD 340 million contract with KCI USA underscores government muscle in shaping formularies. Canada leverages Health Canada-FDA reciprocity to accelerate approvals, while Mexico's private hospitals import U.S.-cleared fish-skin grafts to serve self-pay patients.

Europe is tracking an 8.46% CAGR, supported by CE-mark harmonization that lets manufacturers sell across 27 states using a unified dossier. Germany and the United Kingdom remain volume anchors, but Southern Europe shows quicker percentage growth as austerity budgets loosen. Value-based procurement consortia compare total cost of closure rather than unit price, favoring biologics with trial-backed healing rates. Scandinavian health systems spearhead real-world registries that feed reimbursement recalibration every two years.

Asia-Pacific leads on growth at 10.29% CAGR. China upgrades hundreds of county hospitals with burn units equipped for xenograft application as part of its Healthy China 2030 plan. Japan's long history with basic fibroblast growth factor eases acceptance of new biologics, while India's multi-tier price corridors encourage domestic production of collagen matrices. Australia's Medicare Benefits Schedule newly covers outpatient biologic dressing reviews, expanding rural uptake. Collectively, these forces shift future revenue weight toward Asia, diversifying the wound care biologics market's geographic footprint.

- Avita Medical

- B. Braun

- Bioventus Inc.

- Coloplast

- Convatec Group plc

- Essity

- Grifols

- Integra LifeSciences

- Kerecis Ehf

- Lynch Biologics

- Marine Polymer Technologies

- Medline Industries

- MiMedx Group Inc.

- Molnlycke AB

- MTF Biologics

- Organogenesis Holdings

- Skye Biologics Holdings

- Smiths Group

- Solventum Corporation

- Stryker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Diabetic Foot Ulcers

- 4.2.2 Government Reimbursement Expansions for Advanced Wound Care

- 4.2.3 Increasing Incidence of Burns & Road-Traffic Injuries

- 4.2.4 Rising Adoption of Fish-Skin Xenografts

- 4.2.5 Surge in Battlefield & Disaster-Response Procurement of Biologics

- 4.2.6 Shift from Inpatient to Outpatient Wound Centers Driving Biologic Formulary Inclusion

- 4.3 Market Restraints

- 4.3.1 High Procedure & Product Cost

- 4.3.2 Stringent Tissue-Bank Regulations

- 4.3.3 Supply-Chain Fragility For Placental / Amniotic Raw Material

- 4.3.4 Growing Antimicrobial-Resistance Scrutiny on Biologic Dressings

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Acellular Dermal Matrices

- 5.1.2 Amniotic & Placental Membranes

- 5.1.3 Xenografts

- 5.1.4 Synthetic & Biosynthetic Scaffolds

- 5.1.5 Growth-Factor & Cell-based Topical Agents

- 5.1.6 Other Products

- 5.2 By Wound Type

- 5.2.1 Ulcers

- 5.2.1.1 Diabetic Foot Ulcers

- 5.2.1.2 Venous Ulcers

- 5.2.1.3 Pressure Ulcers

- 5.2.1.4 Other Ulcers

- 5.2.2 Surgical & Traumatic Wounds

- 5.2.3 Burns

- 5.2.1 Ulcers

- 5.3 By Distribution Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Home-Care Settings

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Avita Medical

- 6.4.2 B. Braun Melsungen AG

- 6.4.3 Bioventus Inc.

- 6.4.4 Coloplast A/S

- 6.4.5 Convatec Group plc

- 6.4.6 Essity AB

- 6.4.7 Grifols S.A.

- 6.4.8 Integra LifeSciences

- 6.4.9 Kerecis Ehf

- 6.4.10 Lynch Biologics

- 6.4.11 Marine Polymer Technologies

- 6.4.12 Medline Industries

- 6.4.13 MiMedx Group Inc.

- 6.4.14 Molnlycke AB

- 6.4.15 MTF Biologics

- 6.4.16 Organogenesis Holdings

- 6.4.17 Skye Biologics Holdings

- 6.4.18 Smith & Nephew plc

- 6.4.19 Solventum Corporation

- 6.4.20 Stryker Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment