|

시장보고서

상품코드

1846311

결찰기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ligation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

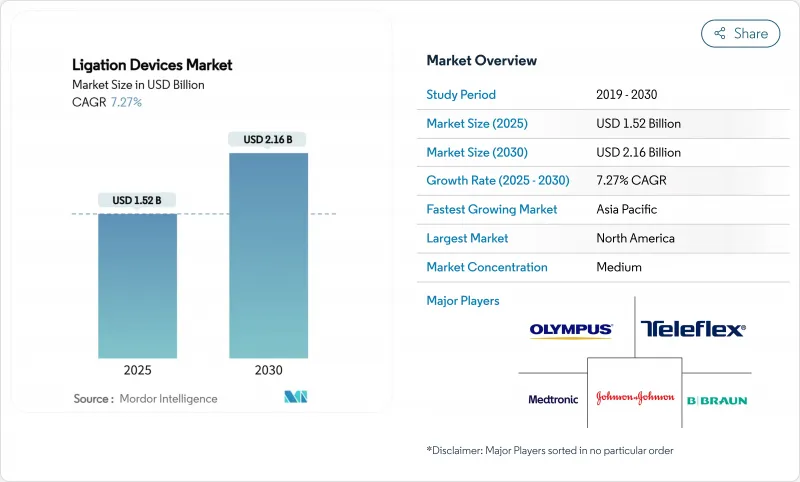

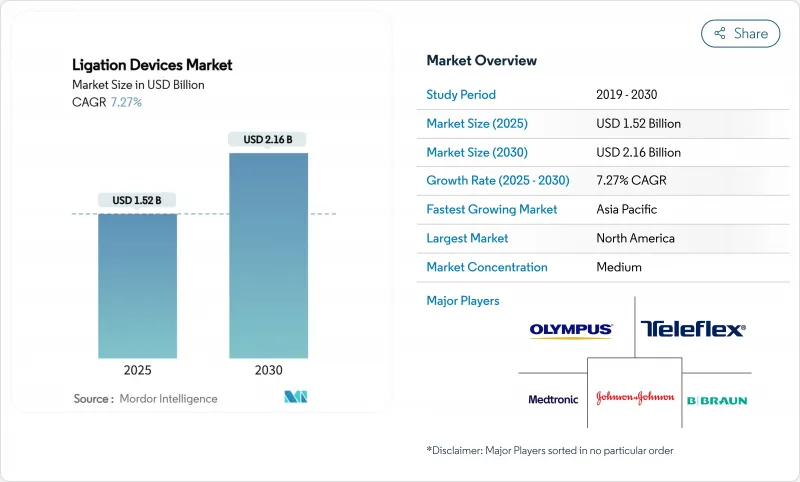

결찰기 시장 규모는 2025년에 15억 2,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 7.27%로 성장할 전망이며, 2030년에는 21억 6,000만 달러에 달할 것으로 예측됩니다.

이 기세는 저침습 수술의 급속한 보급, 심장 혈관 및 비뇨기과의 증례 수 증가, 파열 압력 강도를 높이면서 밀봉 시간을 단축하는 에너지 기반 혈관 밀봉 시스템의 지속적인 개선으로 인해 발생합니다. 재원 일수의 단축을 중시하는 병원의 자세가 강해짐과 동시에, 주술기의 합병증 발생률 저하에 보답하는 지불측의 인센티브도 더해져, 프리미엄 실링 플랫폼에 대한 구매 의욕은 더욱 강해지고 있습니다. 경쟁사와의 차별화는 현재 AI를 활용한 에너지 조절, 인체공학에 근거한 핸드 기구, 수술 성능 및 지속가능성 모두의 의무에 대응하는 친환경 클립 소재 등이 중심이 되고 있습니다.

세계의 결찰기 시장 동향 및 인사이트

심혈관 질환 및 비뇨기 질환의 유병률 상승

심장 전문의 및 비뇨기과 의사는 봉합사에 비해 수술 중 출혈량을 줄이면서 최대 7mm까지 동맥을 고정할 수 있는 고급 혈관 봉쇄 플랫폼에 점점 주목을 받고 있습니다. UroLift와 같은 시스템은 기계적 조직 리프팅을 사용하여 전립선 비대증을 완화하고, 성 기능을 유지하며, 외과 의사의 선호도를 높입니다. 세계적인 노화로 수술 건수가 증가하고, 가치 기반 결제 프로그램은 수혈률을 줄이고, ICU 체류를 단축하는 기술에 보답합니다. 이러한 요인은 취약하고 석회화되거나 염증이 있는 혈관을 최소한의 열 확산으로 관리할 수 있는 최고급 실링 솔루션에 대한 장기적인 수요가 예상됩니다.

저침습 수술의 성장

외래센터의 증례 수는 연간 5.7%의 성장을 나타내며, 병원의 외래 유닛에 비해 25-50%의 비용 절감의 혜택을 받고 있습니다. 동시에 로봇 플랫폼은 정밀한 혈관 밀봉 하드웨어를 추가합니다. Intuitive의 커브 실러의 FDA 허가를 통해 다빈치 시스템에서 제한된 공간에서 작업할 수 있습니다. 소절개는 퇴원을 가속화하고 직장으로의 조기 복귀를 촉진하기 때문에 지불자는 복강경과 로봇 접근법을 권장합니다. 따라서 외과의사는 5mm의 포트에 적합하고 360mmHg 이상의 파열압을 유지하는 밀봉 기구를 요구하고 있습니다. 이러한 역학으로 결찰기 시장은 저침습 생태계의 중심에 위치하고 있습니다.

고급 결찰 시스템의 고비용

자본 집약적인 발전기 및 일회용 핸드피스는 소규모 병원에서 설비 예산을 초과하는 경우가 많으며, 가치위원회는 전환을 인정하기 전에 엄격한 비용 효과 데이터를 요구합니다. 일괄 지불 계약은 한층 더 이폭을 압박해, 에피소드 오브 케어 테두리내에서 실증 가능한 보상이 없는 기술의 구입을 마음에 머물게 합니다. 저소득국에서는 공공 입찰로 성능보다 가격이 평가되기 때문에 AI에 의한 밀봉 장치의 보급이 늦어져 결찰기 시장 당면의 수익이 감소합니다.

부문 분석

2024년 결찰기 시장 규모의 63.88%는 액세서리가 차지했습니다. 감염 관리 정책과 재처리 비용 절감으로 인해 이 범주는 병원 공급망에 필수적입니다. 한편, 핸드헬드 기구는 보다 스마트한 에너지 공급과 외과의의 피로를 경감하는 경량인 인체공학에 지지되어, 2030년까지 CAGR 9.07%로 성장할 전망입니다.

마그네슘 합금으로 만든 2세대 클립 어플라이어는 MRI에 아티팩트가 없으며 인장 강도를 유지하면서 12개월 이내에 완전히 흡수됩니다. 밴드 결찰기는 내시경 정맥류 결찰술로 링을 안정적으로 배치하기 위해 토크 제한 트리거를 내장했습니다. 반면에 AI 지원 발전기는 실시간으로 조직 유형을 감지하고 전압 범위를 교정합니다.

저침습 수술은 2024년 결찰기 시장의 71.61%를 차지했습니다. 외과의사는 회복 시간을 단축하고 당일 퇴원을 가능하게 하는 소형 포트 접근법을 선호합니다. 로봇 사례는 다빈치 5가 촉각 피드백과 mm 이하의 열 마진이 가능한 새로운 커브 실러를 추가했기 때문에 CAGR은 12.24%로 설정되었습니다.

복강경 팀은 시각화 플랫폼의 업그레이드를 계속하고 있으며, 적외선 오버레이에 의해 숨어 있던 혈관계가 밝혀지고, 보다 안전한 밀봉이 가능하게 됩니다. 자기압박 장치를 내시경적으로 사용하는 것으로, 스테이플을 사용하지 않고 파우치에서 사지로의 문합을 촉진하고, 흉터가 없는 재수술에 의한 비만 수술에 새로운 경지를 열고 있습니다. 개복 수술은 여전히 외상과 종양에 필수적이며 결찰기 시장의 높은 처리량 클립 카트리지에 대한 기본적인 수요를 지원합니다.

지역 분석

북미는 가처분 소득이 높은 환자와 견조한 상환을 배경으로 2024년 결찰기 시장 규모의 41.81%를 차지했습니다. 대규모 GPO 계약은 클립 및 발전기의 번들 계약에 유리하며 기존 브랜드는 더욱 강화됩니다.

2030년까지 연평균 복합 성장률(CAGR)이 8.58%로 가장 빠른 것은 아시아태평양이며, 이는 중국이 병원 인가를 합리화하고 인도가 보험 적용을 확대했기 때문입니다. EziSurg와 같은 국내 제조업체는 현지 예산에 맞는 경쟁 가격 실러를 도입합니다. 일본의 초고령화 사회는 로봇 어시스트의 꾸준한 보급을 지지하고, 한국의 입찰 개혁은 프리미엄 제너레이터를 위한 민간 루트를 엽니다.

유럽에서는 규율 있는 기술 회전이 유지되고 임상 의사는 열 확산에 대한 검토된 데이터가 있는 CE 마크 실러를 선호합니다. 지속가능성에 관한 지침은 병원을 흡수성 폴리머 클립으로 향하게 합니다. 라틴아메리카와 중동 및 아프리카는 가격에 민감하면서 대량의 비만 치료 센터에 투자하고 있으며 결찰기 시장은 점차 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- CV 및 비뇨기 질환의 유병률 상승

- 저침습 수술의 성장

- 비만 수술 및 미용 수술의 급증

- 혈관 봉쇄 에너지 디바이스의 급속한 기술 진보

- 자석 보조 문합의 채용

- 흡수성 폴리머제 클립으로의 시프트

- 시장 성장 억제요인

- 고도 결찰 시스템의 고비용

- 규제 및 상환의 장애물

- 봉합사 불필요한 생체 접착성 실란트의 출현

- 일회용 클립에 대한 지속가능성의 추진

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품 유형별

- 핸드헬드 기구

- 결찰 클립 어플라이어

- 내시경용 밴드 리게이터

- 혈관 밀봉 제너레이터

- 액세서리

- 핸드헬드 기구

- 수기별

- 저침습 수술

- 복강경하

- 내시경 수술

- 로봇 지원

- 개복 수술

- 저침습 수술

- 용도별

- 소화기 및 복부

- 심장혈관

- 부인과

- 비뇨기과

- 비만 및 대사

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson

- Medtronic

- Teleflex Inc.

- Olympus Corporation

- Applied Medical

- CONMED Corp.

- CooperSurgical Inc.

- B. Braun Melsungen AG

- Boston Scientific

- Intuitive Surgical

- AngioDynamics

- Kangji Medical

- Grena Ltd.

- Welfare Medical

- Progressive Medical

- LiVac Medical

- GI Windows

- Mellon Medical

- LaproSurge

- Smiths Medical

제7장 시장 기회 및 전망

AJY 25.11.10The Ligation Devices Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 2.16 billion by 2030, at a CAGR of 7.27% during the forecast period (2025-2030).

This momentum stems from rapid uptake of minimally invasive surgery, rising cardiovascular and urological caseloads, and continuous improvements in energy-based vessel-sealing systems that shorten seal time while boosting burst-pressure strength. Intensifying hospital emphasis on reduced length of stay, alongside payer incentives that reward lower peri-operative complication rates, further strengthens purchasing appetite for premium sealing platforms. Competitive differentiation now revolves around AI-enabled energy modulation, ergonomic hand instruments, and eco-friendly clip materials that address both surgical performance and sustainability mandates.

Global Ligation Devices Market Trends and Insights

Rising Prevalence of CV & Urologic Diseases

Cardiologists and urologists are increasingly turning to advanced vessel-sealing platforms that can secure arteries up to 7 mm while lowering intra-operative blood loss compared with sutures. Urology has moved beyond excisional methods; systems such as UroLift use mechanical tissue lifting to relieve benign prostatic hyperplasia, sustaining sexual function and driving surgeon preference. An aging global population intensifies procedure volume, and value-based payment programs reward technology that trims transfusion rates and shortens ICU stays. These factors lock in long-term demand for premium sealing solutions able to manage fragile, calcified or inflamed vessels with minimal thermal spread.

Growth in Minimally Invasive Procedures

Ambulatory centers are posting 5.7% annual growth in case counts, benefiting from 25-50% cost savings over hospital outpatient units. Concurrently, robotic platforms add precise vessel-sealing hardware; FDA clearance for Intuitive's curved sealer now allows confined-space work on da Vinci systems. Smaller incisions speed discharge and promote quicker return to work, encouraging payers to endorse laparoscopic and robotic approaches. Surgeons, in turn, demand sealing instruments that fit through 5-mm ports yet maintain burst pressures above 360 mmHg. These dynamics place the ligation devices market at the center of the minimally invasive ecosystem.

High Cost of Advanced Ligation Systems

Capital-intensive generators and disposable handpieces often exceed equipment budgets in smaller hospitals, prompting value committees to demand rigorous cost-effectiveness data before granting conversion. Bundled-payment contracts further squeeze margins, discouraging purchase of technology that lacks demonstrable return within the episode-of-care window. In lower-income economies, public tenders rate price over performance, delaying penetration of AI-directed sealing units and dampening near-term revenue for the ligation devices market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Bariatric & Aesthetic Surgeries

- Rapid Tech Advances in Vessel-Sealing Energy Devices

- Regulatory / Reimbursement Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accessories generated 63.88% of the ligation devices market size in 2024 as single-use clips, bands and cartridges drove repeat purchasing. Infection-control policies and elimination of reprocessing overhead keep this category essential to hospital supply chains. Hand-held instruments, however, are on track for a 9.07% CAGR through 2030, underpinned by smarter energy delivery and lighter ergonomics that reduce surgeon fatigue.

Second-generation clip appliers fashioned from magnesium alloys appear artifact-free on MRI and fully absorb within 12 months while maintaining tensile strength. Band ligators now incorporate torque-limiting triggers for consistent ring placement in endoscopic variceal ligation. Meanwhile, AI-ready generators sense tissue type in real time and calibrate voltage ranges, an advance that keeps hand-held sales brisk in the ligation devices market.

Minimally invasive surgery accounted for 71.61% of the ligation devices market in 2024. Surgeons favor small-port approaches that shorten recovery times and permit same-day discharge. Robotic cases are set for a 12.24% CAGR as da Vinci 5 adds haptic feedback and new curved sealers capable of sub-millimeter thermal margins.

Laparoscopic teams continue to upgrade visualization platforms, with infrared overlays unveiling otherwise hidden vasculature for safer sealing. Endoscopic use of magnetic compression devices accelerates pouch-to-limb anastomosis without staples, opening new frontiers in scarless revision bariatrics. Open surgery remains vital for trauma and oncology, sustaining baseline demand for high-throughput clip cartridges within the ligation devices market.

The Ligation Devices Market Report is Segmented by Product Type (Hand-Held Instruments, Accessories), Procedure (Minimally Invasive Surgery, Open Surgery), Application (Gastrointestinal & Abdominal, Cardiovascular, and More), End User (Hospitals, Ambulatory Surgical Centres, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.81% of the ligation devices market size in 2024 on the strength of high disposable-income patients and robust reimbursement. Large GPO contracts favor bundled clip-and-generator deals, further entrenching incumbent brands.

Asia-Pacific posts the fastest 8.58% CAGR to 2030 as China streamlines hospital licensing and India expands insurance coverage. Domestic manufacturers such as EziSurg introduce competitively priced sealers tailored to local budgets. Japan's super-aged society underpins steady robotic-assisted adoption, while South-Korean tender reforms open private-sector routes for premium generators.

Europe maintains disciplined technology rotation, with clinicians prioritizing CE-marked sealers that carry peer-reviewed data on thermal spread. Sustainability directives push hospitals toward absorbable polymer clips. Latin America and the Middle East & Africa remain price-sensitive yet invest in high-volume bariatric centers, slowly broadening the addressable ligation devices market.

- Johnson & Johnson

- Medtronic

- Teleflex

- Olympus

- Applied Medical Resources

- CONMED Corp.

- The Cooper Companies

- B. Braun

- Boston Scientific

- Intuitive Surgical

- AngioDynamics

- Kangji Medical

- Grena

- Welfare Medical

- Progressive Medical

- LiVac Medical

- GI Windows

- Mellon Medical

- LaproSurge

- Smiths Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of CV & Urologic Diseases

- 4.2.2 Growth in Minimally Invasive Procedures

- 4.2.3 Surge In Bariatric & Aesthetic Surgeries

- 4.2.4 Rapid Tech Advances in Vessel-Sealing Energy Devices

- 4.2.5 Magnet-Assisted Anastomosis Adoption

- 4.2.6 Shift to Absorbable Polymer Clips

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Ligation Systems

- 4.3.2 Regulatory / Reimbursement Hurdles

- 4.3.3 Emergence of Suture-Less Bio-Adhesive Sealants

- 4.3.4 Sustainability Push Vs Single-Use Clips

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Hand-held Instruments

- 5.1.1.1 Ligating clip appliers

- 5.1.1.2 Endoscopic band ligators

- 5.1.1.3 Vessel-sealing generators

- 5.1.2 Accessories

- 5.1.1 Hand-held Instruments

- 5.2 By Procedure

- 5.2.1 Minimally Invasive Surgery

- 5.2.1.1 Laparoscopic

- 5.2.1.2 Endoscopic

- 5.2.1.3 Robotic-assisted

- 5.2.2 Open Surgery

- 5.2.1 Minimally Invasive Surgery

- 5.3 By Application

- 5.3.1 Gastrointestinal & Abdominal

- 5.3.2 Cardiovascular

- 5.3.3 Gynecology

- 5.3.4 Urology

- 5.3.5 Bariatric / Metabolic

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Specialty Clinics

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Johnson & Johnson

- 6.3.2 Medtronic

- 6.3.3 Teleflex Inc.

- 6.3.4 Olympus Corporation

- 6.3.5 Applied Medical

- 6.3.6 CONMED Corp.

- 6.3.7 CooperSurgical Inc.

- 6.3.8 B. Braun Melsungen AG

- 6.3.9 Boston Scientific

- 6.3.10 Intuitive Surgical

- 6.3.11 AngioDynamics

- 6.3.12 Kangji Medical

- 6.3.13 Grena Ltd.

- 6.3.14 Welfare Medical

- 6.3.15 Progressive Medical

- 6.3.16 LiVac Medical

- 6.3.17 GI Windows

- 6.3.18 Mellon Medical

- 6.3.19 LaproSurge

- 6.3.20 Smiths Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment