|

시장보고서

상품코드

1846313

항문 세척 시스템 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anal Irrigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

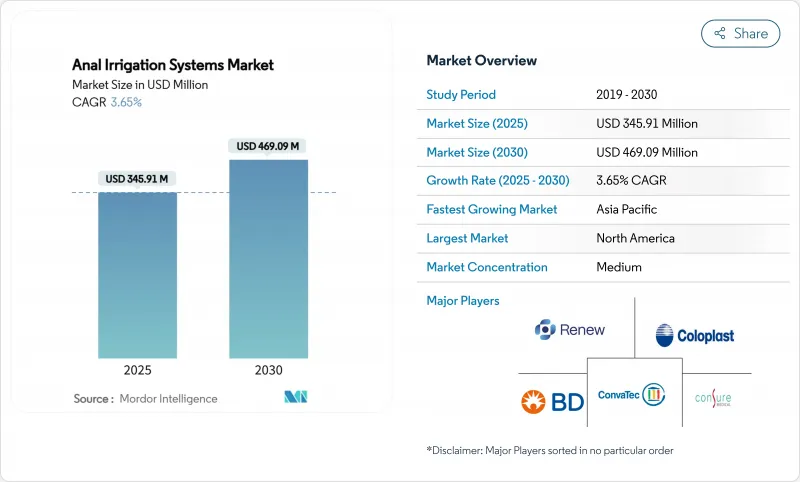

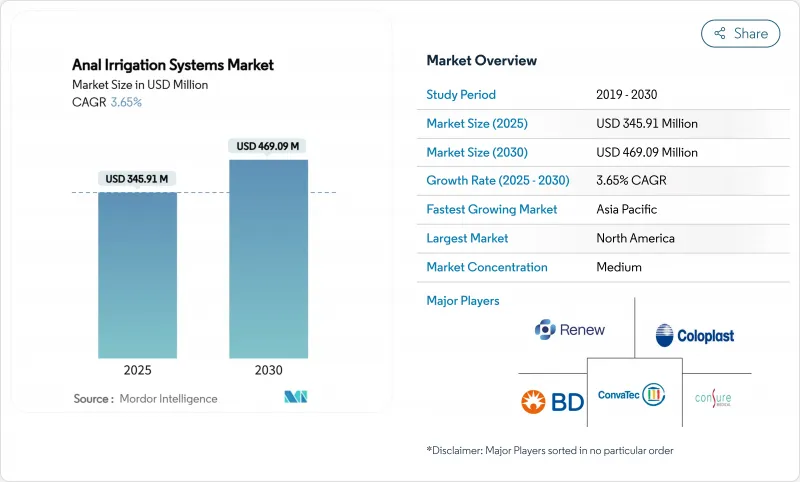

항문 세척 시스템 시장 규모는 2025년에 3억 4,591만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 3.65%로 성장할 전망이며, 2030년에는 4억 6,909만 달러에 달할 것으로 예측됩니다.

성장의 배경은 의료비 지급자가 보수적인 장관 관리를 대체하는 비용 절감 방법으로 경항문 세척을 수락하는 것과 가정에서 장비를 사용하고 모니터링하는 것을 용이하게 하는 기술 변화입니다. 꾸준히 진행되는 고령화, 대장암의 조기 발병, 신경인성 장기능 장애에 대한 상환 코드의 확대에 의해 예측 가능한 수요 기준선이 확보됩니다. 제조업체 각사는 압력과 양의 제어를 자동화하는 전자 펌프 시스템으로 대응하고 있어 임상의가 간호 시간을 확보하면서 유해 사건을 억제할 수 있도록 지원하고 있습니다. 아시아태평양의 의료 시스템이 장기적인 콘티넨스케어를 현대화함에 따라 지리적 다양화가 더욱 확대를 추진하고 있습니다.

세계의 항문 세척 시스템 시장 동향 및 인사이트

대장암 및 IBD 발생률 증가

대장암의 조기 진단과 60세 이상의 염증성 장 질환 증가는 경항문적 항문 세척 대상 환자를 꾸준히 늘리고 있습니다. 수술 후 생존자는 구조화된 세장을 이용하여 배변을 회복하고 보존적인 완하제 치료에 비해 긴급시 진찰을 40-60% 삭감하고 있습니다. 고령화와 조기 발병이라는 두 가지 인구통계학적 압력으로 병원은 수술 직후의 필요와 평생에 걸친 증상 조절의 균형을 맞추어야 합니다. 이러한 패턴에서는 자동화된 전자 펌프가 유리합니다. 이 기술은 수작업을 최소화하고 감염 위험의 터치 포인트를 줄이기 때문입니다. 환자 코호트가 확대됨에 따라, 지불자는 관개가 고액의 오스토미를 회피하는 예산 감축의 테코가 될 것을 발견하고 있습니다.

저침습 장관 관리에 대한 선호도 증가

헬스케어 전문가는 경항문적 세장을 영구적 인공 항문 조설술을 연장하거나 부정하는 교량요법으로 자리매김하고 있습니다. 원격 환자 모니터링 플랫폼은 2023년까지 미국 임상의의 81%를 다루며 멀리 떨어진 곳에서 재택 세장 세션을 감독할 수 있도록 합니다. 지불자의 경우, 재택 관리는 시설 비용을 30% 절감하고 만족도를 높여 보험 적용 결정에 박차를 가합니다. 환자 조사에 의하면, 신경인성 장 기능 장애 환자의 85%가 치료 결과를 알면 수술보다 세장을 선택한다고 응답하고 있습니다. 이분 척추와 관련 이상에 대한 비침습적 관리를 간병인이 추구함에 따라 소아과에 대한 도입이 급속히 진행되고 있으며, 지속적인 유닛 수요가 지적되고 있습니다.

장 천공 및 기타 부작용의 위험

심각한 합병증은 수술의 불과 0.1-0.3% 밖에 일어나지 않지만, 특히 전문의의 감시가 어려운 지역에서는 책임 추궁의 공포가 일부 병원을 망설이고 있습니다. 미국 FDA의 2024년 지침은 시판 후 감시를 강화하고 조직 손상 위험을 줄이는 멀티 센서 압력 차단을 통합하도록 벤더를 촉구했습니다. 일반 진료소에 대한 보급이 진행되면, 3차 의료기관 이외의 의료 종사자는 미묘한 프로토콜에 익숙하지 않기 때문에 트레이닝의 필요성이 높아집니다. 따라서, 엄격한 환자 스크리닝은 해부학적으로 적절한 후보자에게 치료를 제한하는 매우 중요한 안전망으로 계속됩니다.

부문 분석

2025-2030년 CAGR은 전자 펌프가 가장 빨리 5.74%로 성장할 전망이지만, 콘 디바이스는 2024년 매출의 31.41%를 차지했습니다. 자동화된 압력과 양의 알고리즘은 일관성을 높이고, 수작업의 필요성을 줄이며, 표준화된 결과를 찾는 임상의의 요구에 부합합니다. 콜로플라스트가 2024년 7월에 발표한 디지털 누출 알림은 모바일 연결을 통해 세장을 단일 도구에서 실시간 컨티넨스 플랫폼으로 승화시켰음을 나타냅니다. 풍선 카테터는 특히 허약한 노인과 소아와 같은 부드러운 압력 조절이 필요한 고위험 인구에 의해 뒷받침됩니다. 소형 기구는 신중함을 우선시함으로써 활동적인 라이프 스타일을 만족시키지만, 침대에 설치하는 유형의 기구는 장기 요양 병동의 비품으로 남아 있습니다. 리튬 이온의 에너지 밀도와 피에조식 마이크로 펌프의 개량에 의해 배터리 구동의 장치는 장치의 중량을 증가시키지 않고, 보다 높은 유량을 공급할 수 있게 되어, 성인 재택 간호의 적격성이 확대되었습니다. 센서 퓨전 기술은 라이브 피드백 루프를 통해 천공 위험을 더욱 완화합니다.

임상 결과의 증거가 이 기세를 지원합니다. 연구에서 전자 시스템은 수동 콘에 비해 세척 시간을 20% 단축하고 불완전한 배수를 15% 감소시켜 확실한 어드레싱 비율로 이어진다고 합니다. 병원 인력 부족이 심각해짐에 따라 관리자는 전자 장치가 제공하는 시간 절약과 원격 모니터링 대시보드를 높이 평가합니다. 이러한 가치 제안은 북미와 유럽 연합(EU)에서의 조달에 직접적인 영향을 미칩니다. 저소득층이 많은 지역에서는 가격에 민감하기 때문에 1세대 콘은 여전히 주류이지만 공급업체 금융 프로그램은 펌프 기반 키트의 구매 장애물을 낮추고 있습니다. 이러한 경쟁 역학의 결과로 공급업체는 포트폴리오를 확장하여 안전을 희생하지 않고 어떤 의료 현장에서도 적절한 의료기기에 액세스할 수 있습니다.

300-1000mL급 용량이 2024년 세계 매출의 52.94%를 유지한 것은 효능과 환자의 쾌적성의 균형이 오랫동안 유지되어 왔음을 반영합니다. 그러나 세척량이 1,000mL를 넘으면 배설물 배출이 감소한다는 데이터로 2030년까지의 CAGR은 6.43%에 달할 전망입니다. 의료기관에서는 환자를 중등량으로 시작하고 내약성이 향상되면 보다 대량의 투여에 스텝 업하도록 케어 패스를 개정하고 있습니다. 전자 펌프는 펌웨어가 경련을 방지하는 점진적인 유량 램프를 설정하므로 이행을 용이하게 합니다. 강력한 세척이 폐색과 관련된 재입원을 줄이는 증거가 있기 때문에 고용량 투여는 지불 측의 경제성으로 이어집니다.

300 mL 이하의 프로토콜은 직장 용량에 제한이 있는 소아과 및 성인에게는 여전히 필수적입니다. 이러한 경우에는 풍선 카테터가 선호되고 사용되는 경우가 많지만 정밀한 씰이 저용량에서 역행성 누출을 방지하기 때문입니다. 수익 성장은 둔화되고 있으며, 이 층에서는 카테터 슬리브 및 밸브와 같은 소모품 매출이 정기적으로 계상됩니다. 따라서 디바이스 제조업체는 용량 구분을 상호 배타적인 사일로가 아닌 환자의 페인트 셰저니의 이정표로 취급하고 300mL에서 1,000mL의 요법으로 전환할 때 노즐 교체 및 펌웨어 업데이트가 가능한 키트를 설계합니다. 이러한 모듈화 된 경로는 성숙한 경쟁 분야에서 무형이지만 매우 중요한 차별화 요소인 브랜드 충성도를 유지하는 데 도움이 됩니다.

지역 분석

북미 점유율 39.74%는, 2024년에 시행된 메디케어 코드의 확대로 환자의 자기부담액이 줄어 임상의 처방이 활발해졌습니다. 2025년에는 2.7%의 재택 치료비 지불이 증가해, 케어 매니저는 압박, 지속시간, 누출의 지표를 추적하는 원격 대시보드에 지지 받으면서, 적절한 증례를 병동에서 거실로 이행시키는 인센티브가 더욱 높아집니다. 인력 부족은 연결 펌프의 보급을 촉진하고 세션 당 간호사 시간을 15% 줄일 수 있습니다. 지불자는 이것을 잔업대 증가나 잠재적인 노동조합과의 마찰에 대항한다고 생각합니다.

유럽에서는 각국의 의료제도가 경항문적 세척을 신경인성 장질환의 필수 치료법으로 정식으로 지정하여 1차의료부터 3차의 의료까지 장비와 소모품의 자금을 확보하고 있습니다. 유럽권의 지속가능성 의제는 생분해성 플라스틱의 연구개발에 박차를 가해 고분자 화학자와 기기 OEM의 기업 제휴가 격화되고 있는 분야입니다. 병원에서는 환자 1인당 1일 34파운드의 폐기물이 발생하기 때문에 의료기기 제조업체 각사는 규제나 호평에 노출되어 일회용 용기의 삭감을 촉구하고 있습니다. 북유럽 국가들은 살아있는 연구소의 역할을 합니다. : 스웨덴의 전자 처방전 포털 사이트는 이미 세척 데이터 피드를 통합하고 있으며, 연결된 장비가 진료 보상의 필수 요건이 될 가능성을 신속하게 시사하고 있습니다.

아시아태평양의 CAGR 6.06%는 인구 고령화 및 정책적 인프라 정비라는 두 가지 힘 때문입니다. 시장 조사에서는 2030년까지 이 지역의 의료 기술 분야가 2,250억 달러에 달할 것으로 예측되고 있으며, 그 중 장관 관리는 증가의 일도를 따랐습니다. 중국 종양의 부담만으로 수백만 명의 오스트메이트 회피 후보자가 태어납니다. 그러나 상업적 성공에는 스티그마를 극복하기 위해 문화적으로 민감한 교육 캠페인이 필요합니다. 장비 대여 패키지에 교육을 번들로 제공하는 현지 대행사는 하드웨어 전용 판매보다 높은 재주문률을 달성했습니다. 정부는 또한 재입원 감소를 기록한 펌프를 제공하는 공급업체에게 보상을 제공하여 데이터 분석 모듈의 통합을 강화하고 성과 기반 조달로 축족을 옮깁니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 대장암 및 IBD의 이환율 증가

- 저침습성 장관 관리에 대한 기호의 고조

- 신경인성 장 기능 장애에 대한 보험 상환 확대

- 재택 케어 및 원격 간호 제공 모델로의 시프트

- 디바이스의 소형화 및 전자 펌프의 통합

- '디지털 트윈' 임상 훈련 시뮬레이터의 등장

- 시장 성장 억제요인

- 장 천공 및 기타 부작용의 위험

- 중저소득국에서의 저질환 인식

- 일회용으로 높은 환자 단가

- 일회용 플라스틱에 대한 지속가능성에 대한 압력

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품 유형별

- 미니 디바이스

- 콘형 디바이스

- 풍선 카테터 시스템

- 침대 및 거치형 시스템

- 전자 펌프 시스템

- 세척량별

- 300 mL 미만

- 300-1000 mL

- 1000 mL 초과

- 환자 연령별

- 소아

- 성인

- 고령자

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 재택 치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Coloplast A/S

- Wellspect HealthCare AB

- ConvaTec Group PLC

- Becton, Dickinson, and Company

- B. Braun Melsungen AG

- MBH-International A/S(Qufora)

- Renew Medical Pty Ltd.(Aquaflush Medical Limited)

- Consure Medical Pvt Ltd.

- Emerson(ProSys Intl.)

- ABC Medical Inc.

- Dentsply Sirona

- Uromed Kurt Drews KG

- MacGregor Healthcare Ltd.

- Albert Waeschle Ltd.

- CleanColon Italy Srl

- DTA Medical

- Shenzhen CleanColon Tech.

- Medegen Medical Products

- Avanos Medical Inc.

- Qufora Bed Systems ApS

제7장 시장 기회 및 전망

AJY 25.11.10The Anal Irrigation Systems Market size is estimated at USD 345.91 million in 2025, and is expected to reach USD 469.09 million by 2030, at a CAGR of 3.65% during the forecast period (2025-2030).

Growth rests on healthcare payers embracing transanal irrigation as a cost-saving alternative to conservative bowel care, alongside technological shifts that make devices easier to use and monitor at home. A steadily ageing population, earlier onset of colorectal cancer, and expanding reimbursement codes for neurogenic bowel dysfunction ensure a predictable demand baseline. Manufacturers are responding with electronic pump systems that automate pressure and volume control, helping clinicians curb adverse events while freeing nursing time. Geographic diversification further underpins expansion as Asia-Pacific health systems modernize long-term continence care.

Global Anal Irrigation Systems Market Trends and Insights

Growing Incidence of Colorectal Cancer & IBD

Earlier-age colorectal cancer diagnoses and rising inflammatory bowel disease prevalence among citizens aged 60 years and above are steadily enlarging the eligible patient pool for transanal irrigation. Post-surgical survivors rely on structured irrigation to regain continence, cutting emergency visits by 40-60% when compared with conservative laxative regimens. The dual demographic pressures of ageing and earlier disease onset force hospitals to balance immediate postoperative needs with lifelong symptom control. These patterns favor automated electronic pumps because the technology minimizes manual handling and lowers infection-risk touchpoints. As patient cohorts broaden, payers find irrigation a budget-relief lever that averts costly ostomies.

Rising Preference for Minimally-Invasive Bowel Management

Healthcare professionals frame transanal irrigation as a bridge therapy that can defer or even negate permanent colostomy procedures. Remote patient-monitoring platforms covered 81% of US clinicians by 2023, making it straightforward to supervise home irrigation sessions from a distance. For payers, at-home care shaves 30% off facility costs and raises satisfaction scores, thus spurring coverage decisions. Patient surveys reveal 85% of neurogenic bowel dysfunction sufferers would choose irrigation over surgery once educated on outcomes. Pediatric uptake quickens as caregivers pursue non-invasive management for spina bifida and related anomalies, pointing to sustained unit demand.

Risk of Bowel Perforation & Other Adverse Events

Although serious complications occur at merely 0.1-0.3% of procedures, fear of liability deters some hospitals, especially in regions lacking specialist oversight. The US FDA's 2024 guidance tightened post-market surveillance, nudging vendors to integrate multi-sensor pressure shut-offs that cut tissue-damage risk. Broader dissemination into general practice amplifies training requirements because operators outside tertiary centers may be unfamiliar with nuanced protocols. Rigorous patient screening therefore remains a pivotal safety net, limiting therapy to anatomically suitable candidates.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Expansion for Neurogenic Bowel Dysfunction

- Shift Toward Home-Care & Tele-Nursing Delivery Models

- Low Disease Awareness in Low- & Middle-Income Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronic pumps registered the quickest 5.74% CAGR from 2025-2030, even as cone devices retained a 31.41% slice of 2024 revenue. Automated pressure and volume algorithms enhance consistency and lower manual dexterity needs, aligning with clinician mandates for standardized outcomes. Coloplast's July 2024 digital leakage notification release illustrates how mobile connectivity elevates irrigation from a stand-alone tool into a real-time continence platform. Balloon catheters persist in high-risk cohorts needing gentle pressure regulation, particularly frail geriatric and pediatric groups. Mini devices satisfy active lifestyles by prioritizing discretion, while bed-mounted rigs remain fixtures in long-term care wards. Improvement in lithium-ion energy density and piezoelectric micropumps allows battery-powered units to deliver higher flow volumes without inflating device weight, thus widening adult home-care eligibility. Sensor fusion technologies further mitigate perforation risk through live feedback loops, an advance that calms provider liability concerns and ultimately spurs wider prescribing.

Clinical outcomes evidence underpins this momentum. Studies link electronic systems to 20% shorter irrigation sessions and 15% fewer incomplete evacuations versus manual cones, translating into robust adherence rates. As hospital staffing shortages intensify, administrators appreciate the time savings and remote-monitoring dashboards that electronic units supply. These value propositions directly influence procurement in North America and the European Union, markets that collectively account for most global device tenders. In lower-income geographies, first-generation cones still dominate owing to price sensitivity, yet vendor finance programs are lowering acquisition hurdles for pump-based kits. The resulting competitive dynamic pushes suppliers to broaden portfolios, ensuring that every care setting can access an appropriate device tier without sacrificing safety.

Volumes in the 300-1000 mL bracket maintained 52.94% of global revenue during 2024, a reflection of long-standing balance between efficacy and patient comfort. However, data correlating exceeding 1,000 ml irrigation with steeper reductions in fecal impaction episodes is driving a measurable 6.43% CAGR in that bracket through 2030. Institutions are revising care pathways to start patients on moderate dosages before stepping up to larger volumes once tolerance improves. Electronic pumps facilitate that transition, as firmware sets graduated flow ramps preventing cramping. Higher-dosage uptake also ties into payer economics, given evidence that robust cleansing cuts readmissions tied to obstruction.

Sub-300 mL protocols remain vital for pediatrics and adults with limited rectal capacity. Clinicians frequently favor balloon catheters in these cases because precision seals prevent retrograde leakage at low volumes. Despite slower revenue growth, this cohort offers recurring consumable sales, particularly catheter sleeves and valves. Device makers thus treat volume segmentation not as mutually exclusive silos but as patient-journey milestones, designing kits that allow nozzle swaps or firmware updates when advancing from 300 mL to 1 000 mL regimens. Such modular pathways help preserve brand loyalty, an intangible yet crucial differentiator in a maturing competitive field.

The Anal Irrigation Systems Market Report is Segmented by Product Type (Mini Devices, Cone Devices, Balloon Catheter Systems, and More), Irrigation Volume (300-1000 Ml, and More), Patient Age (Paediatric, and More), End User (Hospitals, Ambulatory Surgical Centres, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 39.74% share traces to Medicare code expansions enacted in 2024 that sliced patient copayments and galvanized clinician prescriptions. A 2.7% home-health payment bump in 2025 further incentivizes care managers to transition suitable cases from hospital wards to living rooms, supported by remote dashboards that track pressure, duration, and leakage metrics. Staffing shortages amplify uptake of connected pumps, which can cut nurse time per session by 15%. Payers consider this a lever against rising overtime costs and potential union friction.

In Europe, national health systems formally designate transanal irrigation an essential neurogenic bowel therapy, ensuring device and consumable funding across primary and tertiary care. The bloc's sustainability agenda spurs R&D into biodegradable plastics, an area where corporate alliances between polymer chemists and device OEMs are intensifying. Hospitals generate 34 pounds of waste per patient daily, putting device makers under regulatory and reputational pressure to cut single-use content. Nordic countries serve as living laboratories: Sweden's e-prescription portals are already integrating irrigation data feeds, an early signal that connected devices could become reimbursement prerequisites.

Asia-Pacific's 6.06% CAGR springs from two forces ageing populations and policy-backed infrastructure upgrades. Market research forecasts a USD 225 billion regional med-tech arena by 2030, of which bowel management will claim a rising slice. China's oncology burden alone creates millions of ostomy-avoidance candidates. Yet commercial success demands culturally sensitive education campaigns to overcome stigma. Local distributors that bundle training with device rental packages achieve higher reorder rates than those selling hardware alone. Governments also pivot towards outcome-based procurement, rewarding vendors whose pumps document reduced readmissions, thereby reinforcing integration of data analytics modules.

- Coloplast

- Wellspect

- Convatec

- Beckton Dickinson

- B. Braun

- MBH-International A/S (Qufora)

- Renew Medical

- Consure Medical Pvt Ltd.

- Emerson (ProSys Intl.)

- ABC Medical Inc.

- Dentsply Sirona

- Uromed

- MacGregor Healthcare Ltd.

- Albert Waeschle Ltd.

- CleanColon Italy Srl

- DTA Medical

- Shenzhen CleanColon Tech.

- Medegen Medical Products

- Avanos Medical

- Qufora Bed Systems ApS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Incidence of Colorectal Cancer & IBD

- 4.2.2 Rising Preference for Minimally-Invasive Bowel Management

- 4.2.3 Reimbursement Expansion for Neurogenic Bowel Dysfunction

- 4.2.4 Shift Toward Home-Care & Tele-Nursing Delivery Models

- 4.2.5 Device Miniaturisation & Electronic Pump Integration

- 4.2.6 Emergence Of "Digital-Twin" Clinician Training Simulators

- 4.3 Market Restraints

- 4.3.1 Risk of Bowel Perforation & Other Adverse Events

- 4.3.2 Low Disease Awareness in Low- & Middle-Income Countries

- 4.3.3 High Per-Patient Cost from Single-Use Disposables

- 4.3.4 Sustainability Pressure on Single-Use Plastics

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Mini Devices

- 5.1.2 Cone Devices

- 5.1.3 Balloon Catheter Systems

- 5.1.4 Bed / Stationary Systems

- 5.1.5 Electronic Pump Systems

- 5.2 By Irrigation Volume

- 5.2.1 <300 mL

- 5.2.2 300-1000 mL

- 5.2.3 >1000 mL

- 5.3 By Patient Age

- 5.3.1 Paediatric

- 5.3.2 Adult

- 5.3.3 Geriatric

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Specialty Clinics

- 5.4.4 Home-Care Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Coloplast A/S

- 6.3.2 Wellspect HealthCare AB

- 6.3.3 ConvaTec Group PLC

- 6.3.4 Becton, Dickinson, and Company

- 6.3.5 B. Braun Melsungen AG

- 6.3.6 MBH-International A/S (Qufora)

- 6.3.7 Renew Medical Pty Ltd. (Aquaflush Medical Limited)

- 6.3.8 Consure Medical Pvt Ltd.

- 6.3.9 Emerson (ProSys Intl.)

- 6.3.10 ABC Medical Inc.

- 6.3.11 Dentsply Sirona

- 6.3.12 Uromed Kurt Drews KG

- 6.3.13 MacGregor Healthcare Ltd.

- 6.3.14 Albert Waeschle Ltd.

- 6.3.15 CleanColon Italy Srl

- 6.3.16 DTA Medical

- 6.3.17 Shenzhen CleanColon Tech.

- 6.3.18 Medegen Medical Products

- 6.3.19 Avanos Medical Inc.

- 6.3.20 Qufora Bed Systems ApS

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment