|

시장보고서

상품코드

1846318

비침습적 인공호흡기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Non-invasive Ventilators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

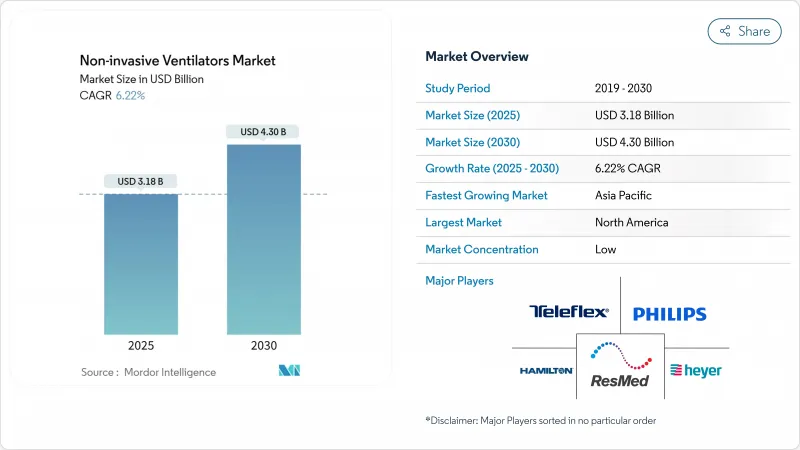

비침습적 인공호흡기 시장은 2025년 31억 8,000만 달러로 추정되고, 2030년 43억 달러에 이를 전망이며, CAGR 6.22%로 성장할 것으로 예측됩니다.

수요는 팬데믹(세계적 유행병)에 의한 급증에서 만성 호흡기 질환 관리, 노인 케어의 필요성, 재택 요법의 채용 증가 등을 배경으로 하는 항상적 성장으로 이행하고 있습니다. 압력 공급을 미세 조정하는 인공지능 알고리즘은 제한된 자원 환경을 위한 간소화된 음압 개념과 함께 비침습성 인공호흡기 시장의 임상적 발자취를 확대하고 있습니다. 장비 제조업체는 환자가 치료를 계속할 수 있도록 편안함에 중점을 둔 인터페이스, 소음 감소 및 클라우드 연결에 주력하는 반면 미국과 일부 유럽 연합(EU) 국가의 지불자는 예산 제약을 완화하기 위해 상환을 확대하고 있습니다. 아시아태평양 헬스케어 구축, 반도체 공급망 안정화, 휴대용 플랫폼에 대한 FDA의 신속한 승인은 전통적인 병원 벽을 넘어서는 비침습적 인공호흡기 시장의 견고한 전망을 지원합니다.

세계의 비침습적 인공호흡기 시장 동향 및 인사이트

COPD 및 천식 환자의 급증

세계에는 3억 9,000만 명 이상의 COPD 환자와 2억 6,200만 명 이상의 천식 환자가 살고 있으며, 고급 환기 지원에 대한 안정적인 수요가 발생하고 있습니다. 메타 분석은 폐쇄성 수면 무호흡 증후군과 고호흡성 COPD의 코호트에서 장기 비침습적 인공호흡기가 사망률을 감소시키는 것으로 나타났습니다. 2025년 GOLD 보고서는 심혈관 위험 통제 및 기후 관련 악화 관리를 치료 경로에 추가하여 변동하는 생리 기능에 적응하는 지능형 환기를 지원합니다. 경피적 CO2 모니터링과 결합된 평균 체적 확보 압력 지원은 48시간의 재삽관 위험을 감소시키고 급성기에서 만성기의 COPD 사례의 입원 기간을 단축합니다. 실시간 분석 플랫폼은 추가 치료를 개별화하고 체중 감소 이벤트를 예측하여 예정되지 않은 입원을 줄입니다.

노인 ICU 입실 증가

65세 이상의 성인의 집중치료실로의 입실이 증가하고 있어 호흡 부전이나 복수의 합병증을 동반하는 경우가 많습니다. 비침습적인 환기는 고 유량의 비강 산소와 비교하여 노인 환자의 흡기 노력을 감소시키고 조용량을 향상시킵니다. 장치의 프로토콜에는 근력 저하에 맞추어 낮은 트리거 임계값이나 동기 기능이 내장되어, 발관 실패의 확률이 저하하고 있습니다. 의료 시스템은 ICU의 침대 수를 늘리면서도 침습적인 기도 합병증을 회피하고 재원 일수를 단축하기 위해 NIV를 선호하고 사용하고 있으며, 예산을 지키면서 퀄리티 점수를 올리고 있습니다.

인공호흡기 관련 폐렴의 위험

인공호흡기 관련 폐렴(VAP)의 발생률은 기계적 인공호흡을 실시하는 코호트에서는 9.2%에서 30%이며, VAP를 하지 않는 환자와 비교하면 증례당 약 54만 4,467달러가 병원 비용에 올라갑니다. 진단의 편차가 예방을 복잡하게 하고 있기 때문에 세계적인 감염 학회에서는 침대 상지 거상, 회로 위생, 조기 동원을 조합한 번들의 표준화를 촉진하고 있습니다. NIV는 삽관을 피하지만 마스크 누출이나 분비물의 축적은 여전히 감염의 원인이 되므로 분비물의 자동 배출이나 항균성 표면 등 설계 상의 궁리가 필요합니다. 중저소득 국가의 교육 캠페인에 따르면 번들 어드레싱은 VAP 발생률을 최대 35%까지 줄이고 취약한 예산을 보호할 수 있음을 보여줍니다.

부문 분석

양압 장치의 비침습적 인공호흡기 시장 규모는 2025년 19억 8,000만 달러로 급성기 및 만성기 의료 현장에서의 역할 확립을 반영한 62.36%의 매출 점유율에 해당합니다. 지속적인 양압 호흡기 및 바이레벨 PAP는 폐쇄성 수면 무호흡 증후군과 COPD 악화를 위한 골드 표준이며, 5밀리초 사이클에서 압력을 보정하는 자동 조정 알고리즘의 이점을 누리고 있습니다. 제조업체는 가습 컨트롤과 노이즈 감쇠 챔버를 추가하여 치료 개시 후 90일간의 복약 준수를 80% 이상으로 끌어올리고 있습니다. 클라우드 네이티브 대시보드는 임상가에게 인공 호흡 매개변수를 푸시하고 후속 방문을 줄이는 원격 증가를 허용합니다. 환자용 모바일 앱은 매일 밤의 사용을 게임화하고 마스크 맞춤 문제에 실시간으로 플래그를 지정합니다.

음압식 인공호흡기는 기술적 르네상스를 경험하고 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 7.15%로 성장할 전망입니다. 최신 쉘은 경량 복합재와 소형 진공 펌프를 사용하여 환자가 치료를 중단하지 않고 정좌, 대화, 음식을 섭취할 수 있습니다. 급성 호흡 곤란 증후군의 임상 연구는 양압 모드에 비해 PaO2/FiO2 비율이 15% 높은 것으로 보고되어 폐 보호상의 이점을 시사하고 있습니다. 자선 단체의 컨소시엄은 저자원 지역의 지구 병원을 대상으로 하는 오픈소스 설계에 자금을 제공하고 있으며, 규제 당국은 필수적인 안전 기능을 검증하기 위한 신속한 지침을 발표하고 있습니다.

지역 분석

북미는 2024년 비침습적 인공호흡기 시장 매출의 43.45%를 차지했으며, 그 배경에는 높은 질병 유병률, 정교한 상환, 신속한 기기 승인이 있습니다. FDA는 2024년 6월에 Servo-air 휴대용 인공호흡기에 510(k) 인가를 주었고 외래 환자 프로그램의 선택을 늘렸습니다. 재택 NIV 요법에 대한 CMS의 전국적 적용 분석은 2025년 후반에 수혜자의 접근을 확대하고 클라우드 생태계에 공급업체의 투자를 자극할 것으로 예측됩니다. 데이터 통합의 의무화는 인공 호흡기, 전자 의료 기록 및 지불자 포털 간의 상호 운용성을 촉진하여 증거 창출과 상환 강화의 선순환을 제공합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 8.14%를 기록할 전망입니다. 중국의 헬스케어 지출은 2022년에 8조 5,000억 위안을 돌파하였고, 2030년에는 20조 5,000억 위안에 이를 것으로 예측되어 3차 의료 네트워크의 업그레이드가 가능해집니다. 정부는 부족한 집중 치료 침대에 의존하지 않고 급성 폐렴의 발생을 해결하기 위해 지방 클리닉에 음압 환기 키트의 시험 계획을 도입합니다. 현지 조립 라인은 리드 타임을 단축하고 통화 변동으로부터 조달을 보호합니다. 지역 학술 제휴는 결핵과 공존하는 COPD에서 NIV의 효능에 대한 데이터를 제공하고 맞춤형 프로토콜을 안내합니다.

유럽은 보편적인 의료제도 및 엄격한 안전 기준에 힘입어 한 자리대 중반의 성장을 안정시킵니다. 유럽 호흡기 학회의 최신 지침은 수술 후 호흡 부전에서 NIV의 조기 적용을 지원하고 고 유량 대응 장비의 조달 파이프라인을 지원합니다. ESG 이니셔티브는 공급업체에게 재활용 가능한 회로를 설계하고 인공호흡기의 수명 주기 전반에 걸쳐 탄소 실적를 측정하도록 촉구합니다.

중동, 아프리카와 남미는 베이스 이펙트의 완만한 확대에 기여합니다. 브라질의 민간 파트너십은 2차 병원과 도시의 호흡기 내과 허브를 연결하는 원격 환기 프로젝트에 자금을 제공합니다. 개발 은행은 높은 수입 관세를 피하기 위해 장비 임대 풀을 지원하고 액세스의 민주화를 추진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- COPD 및 천식 환자 급증

- 고령자에서 입원 환자 증가

- 재택 NIV 요법으로의 시프트

- 재택 NIV에 대한 상환 확대

- AI를 활용한 클로즈드 루프 NIV의 보급

- Lmics용 저가격 음압 NIV 디바이스의 상승

- 시장 성장 억제요인

- 인공호흡기 관련 폐렴(Vap)의 위험

- 높은 장치 및 유지 보수 비용

- 고급 NIV 모드의 취급에서 스킬 갭

- 중요 부품 공급망의 취약성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 비침습적 양압 호흡기(PPV)

- 바이레벨 기도 양압(BiPAP)

- 일정 양압 호흡기(CPAP)

- 자동 적정 양압 호흡기(APAP)

- 비침습적 음압호흡기(NPV)

- 비침습적 양압 호흡기(PPV)

- 용도별

- COPD 및 천식

- 호흡 곤란 증후군

- 기타

- 최종 사용자별

- 병원 및 클리닉

- 외래수술센터(ASC)

- 재택치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- ResMed Inc.

- Koninklijke Philips NV

- Fisher & Paykel Healthcare

- Hamilton Medical AG

- Teleflex Incorporated

- Medtronic plc

- GE Healthcare

- Draegerwerk AG & Co. KGaA

- Vyaire Medical

- Nihon Kohden Corp.

- Smiths Medical

- Getinge AB

- Airon Corporation

- Air Liquide Medical Systems

- Ventec Life Systems

- Phoenix Medical Systems

- Heyer Medical AG

- Zoll Medical Corp.

제7장 시장 기회 및 전망

AJY 25.11.10The non-invasive ventilator market stood at USD 3.18 billion in 2025 and is forecast to reach USD 4.30 billion by 2030, advancing at a 6.22% CAGR.

Demand is shifting from pandemic-driven surges to secular growth anchored in chronic respiratory disease management, geriatric care requirements and rising home-based therapy adoption. Artificial-intelligence algorithms that fine-tune pressure delivery, together with simplified negative-pressure concepts for resource-limited settings, are broadening the clinical footprint of the non-invasive ventilator market. Device makers focus on comfort-oriented interfaces, noise reduction and cloud connectivity to keep patients on therapy, while payers in the United States and selected European Union countries expand reimbursement to ease budget constraints. Asia-Pacific healthcare build-outs, semiconductor supply-chain stabilization and FDA fast-track clearances for portable platforms support a resilient outlook for the non-invasive ventilator market beyond traditional hospital walls.

Global Non-invasive Ventilators Market Trends and Insights

Surging Prevalence of COPD & Asthma Cases

More than 390 million people live with COPD and 262 million with asthma worldwide, generating steady demand for advanced ventilation support. Meta-analyses show that long-term non-invasive ventilation reduces mortality in obstructive sleep apnea and hypercapnic COPD cohorts. The 2025 GOLD report adds cardiovascular risk control and climate-related exacerbation management to treatment pathways, favoring intelligent ventilation that adapts to fluctuating physiology. Average Volume Assured Pressure Support paired with transcutaneous CO2 monitoring lowers 48-hour reintubation risk and shortens stays for acute-on-chronic COPD cases. Real-time analytics platforms further personalize therapy and cut unplanned admissions by predicting decompensation events.

Increasing ICU Admissions Among Geriatrics

Adults over 65 account for a growing portion of intensive-care occupancy, often presenting with respiratory failure and multiple comorbidities. Non-invasive ventilation reduces inspiratory effort and improves tidal volumes in elderly patients compared with high-flow nasal oxygen. Device protocols now incorporate lower trigger thresholds and synchrony features to match diminished muscle strength, lowering extubation failure odds. Health systems expand ICU beds yet prefer NIV to avoid invasive airway complications and to shorten length of stay, protecting budgets while raising quality scores.

Ventilator-Associated Pneumonia Risk

VAP incidence ranges from 9.2% to 30% in mechanically ventilated cohorts, adding roughly USD 544,467 per case to hospital bills versus non-VAP patients. Diagnostic variability complicates prevention, prompting global infection societies to standardize bundles that combine head-of-bed elevation, circuit hygiene and early mobilization. While NIV avoids intubation, mask leaks and secretion buildup can still seed infection, requiring design tweaks such as automatic secretion drainage and antimicrobial surfaces. Education campaigns in low- and middle-income countries show that bundle adherence cuts VAP rates by up to 35%, protecting fragile budgets.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Home-Based NIV Therapy

- Reimbursement Expansion for Home NIV

- High Device & Maintenance Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The non-invasive ventilator market size for positive-pressure devices stood at USD 1.98 billion in 2025, corresponding to a 62.36% revenue share that reflects their entrenched role in acute and chronic care settings. Continuous Positive Airway Pressure and Bilevel PAP remain gold standards for obstructive sleep apnea and COPD exacerbations, benefiting from auto-adjusting algorithms that calibrate pressure in five-millisecond cycles. Manufacturers add humidification controls and noise-attenuation chambers to lift adherence above 80% during the first 90 days of therapy. Cloud-native dashboards push ventilatory parameters to clinicians, allowing remote titration that reduces follow-up visits. Patient-facing mobile apps gamify nightly use and flag mask-fit issues in real time.

Negative-pressure ventilators are experiencing a technical renaissance, recording the fastest 7.15% CAGR through 2030. Modern shells use lightweight composites and compact vacuum pumps, enabling patients to sit upright, converse and ingest food without therapy interruption. Clinical studies in acute respiratory distress syndrome report 15% higher PaO2/FiO2 ratios compared with positive-pressure modes, suggesting lung-protective advantages. Philanthropic consortia fund open-source designs aimed at district hospitals in low-resource geographies, and regulatory agencies have published fast-track guidelines to validate essential safety features.

The Non-Invasive Ventilator Market Report is Segmented by Product (Non-Invasive Positive-Pressure Ventilator, Non-Invasive Negative-Pressure Ventilator), Application (COPD & Asthma, and More), End User (Hospitals & Clinics, Ambulatory Surgical Centers, Homecare Settings), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 43.45% of non-invasive ventilator market revenue in 2024 on the back of high disease prevalence, sophisticated reimbursement and rapid device approvals. The FDA granted 510(k) clearance to the Servo-air portable ventilator in June 2024, adding choice for outpatient programs. CMS's national coverage analysis for home NIV therapy is expected to widen beneficiary access in late 2025, stimulating supplier investment in cloud ecosystems. Data-integration mandates encourage interoperability between ventilators, electronic health records and payer portals, creating a virtuous cycle of evidence generation and reimbursement reinforcement.

Asia-Pacific records the fastest 8.14% CAGR through 2030. Healthcare expenditure in China surpassed CNY 8.5 trillion in 2022 and is projected to hit CNY 20.5 trillion by 2030, enabling tertiary-care network upgrades . Governments introduce pilot schemes for negative-pressure ventilation kits in rural clinics to address acute pneumonia outbreaks without relying on scarce intensive-care beds. Local assembly lines shorten lead times and insulate procurement from currency volatility. Regional academic partnerships generate data on NIV efficacy in tuberculosis-coexistent COPD, guiding tailored protocols.

Europe stabilizes growth at mid-single digits, supported by universal health systems and stringent safety standards. The European Respiratory Society's latest guideline endorses early application of NIV in postoperative respiratory failure, feeding procurement pipelines for high-flow capable machines. ESG initiatives push suppliers to design recyclable circuits and to measure carbon footprints across the ventilator life cycle.

Middle East & Africa and South America contribute modest base-effect expansion. Oil-exporting economies channel surplus revenue into critical-care capacity, while public-private partnerships in Brazil fund tele-ventilation projects that connect secondary hospitals with urban pulmonology hubs. Development banks back equipment-leasing pools to sidestep high import tariffs, further democratizing access.

- Resmed

- Koninklijke Philips

- Fisher & Paykel Healthcare

- Hamilton Medical

- Teleflex

- Medtronic

- GE Healthcare

- Dragerwerk

- Vyaire Medical

- Nihon Kohden Corp.

- Smiths Group

- Getinge

- Airon

- Air Liquide

- Ventec Life Systems

- Phoenix Medical Systems

- Heyer Medical

- Zoll Medical Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Prevalence Of COPD & Asthma Cases

- 4.2.2 Increasing Icu Admissions Among Geriatrics

- 4.2.3 Shift Toward Home-Based NIV Therapy

- 4.2.4 Reimbursement Expansion For Home NIV

- 4.2.5 AI-Driven Closed-Loop Niv Modes Gain Traction

- 4.2.6 Rise Of Low-Cost Negative-Pressure NIV Devices For Lmics

- 4.3 Market Restraints

- 4.3.1 Ventilator-Associated Pneumonia (Vap) Risk

- 4.3.2 High Device & Maintenance Cost

- 4.3.3 Skill Gap In Handling Advanced NIV Modes

- 4.3.4 Supply-Chain Fragility For Critical Components

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Non-invasive Positive-pressure Ventilator (PPV)

- 5.1.1.1 Bi-level Positive Airway Pressure (BiPAP)

- 5.1.1.2 Constant Positive Airway Pressure (CPAP)

- 5.1.1.3 Autotitrating Positive Airway Pressure (APAP)

- 5.1.2 Non-invasive Negative-pressure Ventilator (NPV)

- 5.1.1 Non-invasive Positive-pressure Ventilator (PPV)

- 5.2 By Application

- 5.2.1 COPD & Asthma

- 5.2.2 Respiratory Distress Syndrome

- 5.2.3 Others

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Homecare Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.3.1 ResMed Inc.

- 6.3.2 Koninklijke Philips N.V.

- 6.3.3 Fisher & Paykel Healthcare

- 6.3.4 Hamilton Medical AG

- 6.3.5 Teleflex Incorporated

- 6.3.6 Medtronic plc

- 6.3.7 GE Healthcare

- 6.3.8 Draegerwerk AG & Co. KGaA

- 6.3.9 Vyaire Medical

- 6.3.10 Nihon Kohden Corp.

- 6.3.11 Smiths Medical

- 6.3.12 Getinge AB

- 6.3.13 Airon Corporation

- 6.3.14 Air Liquide Medical Systems

- 6.3.15 Ventec Life Systems

- 6.3.16 Phoenix Medical Systems

- 6.3.17 Heyer Medical AG

- 6.3.18 Zoll Medical Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment