|

시장보고서

상품코드

1846320

안저 카메라 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Fundus Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

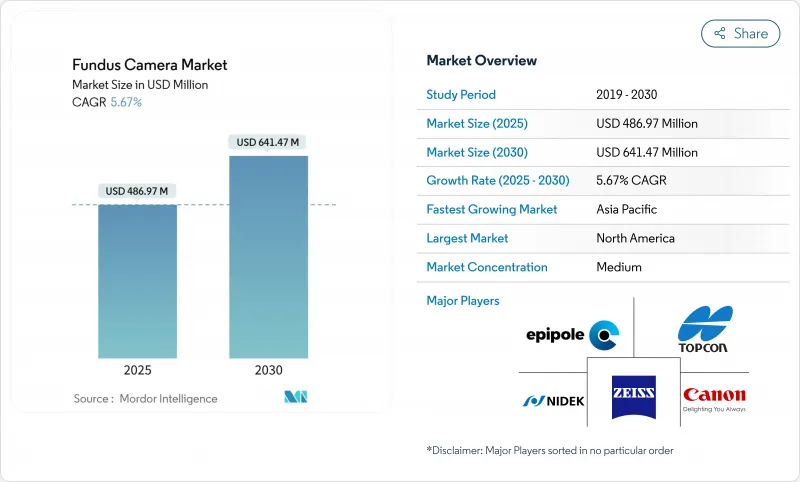

안저 카메라 시장 규모는 2025년에 4억 8,697만 달러로 추정되고, 2030년에는 6억 4,147만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 5.67%를 나타낼 전망입니다.

IDx-DR 및 EyeArt와 같은 FDA 승인 플랫폼이 당뇨병 망막증 검출에서 96% 이상의 감도를 보이는 등 인공지능 알고리즘이 시험적 사용에서 일상적인 사용으로 전환함에 따라 수요가 강화됩니다. 스크리닝 프로그램의 의무화, 원격 안과 진료에 대한 상환 개선, AI에 의한 안저 사진 촬영을 의료상 필요하다고 인정하는 CMS 가이던스 등이 채용을 확대하고 있습니다. 제품의 선호도로는 전자 차트와 원활하게 통합할 수 있는 무산동 시스템이 계속 지원되고 있지만, 하이브리드 및 초광시야 장치가 가장 빠르게 성장하고 있습니다. 휴대형 핸드헬드 카메라가 모달리티 수요를 독점하는 반면, OCT와 안저 사진을 융합시킨 콤비네이션 플랫폼이 종합적인 망막 평가를 위해 기세를 늘리고 있습니다. 지역별로는 북미가 시장 점유율로 선도하고 있지만 당뇨병 유병률의 상승과 각국 정부의 지역안과의료 투자로 아시아태평양이 가장 높은 성장을 보이고 있습니다.

세계의 안저 카메라 시장 동향과 인사이트

가속화되는 당뇨병 망막증 검진의 의무화

현재 많은 나라에서 당뇨병 환자에 대한 연 1회의 망막검사가 의무화되고 있으며, 미국의 메디케어 정책에서는 AI로 해석된 안저 이미지가 의료상 필요로 간주되고 있습니다. 이러한 규칙은 AI 인식 이미지를 생성하고 원격 의료 워크플로우를 지원하는 카메라의 대량 구매에 박차를 가하고 있습니다. 미국에서는 410만 명 이상의 성인이 당뇨병성 망막증을 앓고 있으며, 안저 카메라를 사용한 체계적인 스크리닝으로 회피 가능한 시력 저하를 막는 동시에 장기 요양비를 절감할 수 있습니다.

AI 임베디드 이미지 워크플로우의 급속한 보급

IDx-DR과 같은 FDA 인증 AI 플랫폼은 감도 96% 이상, 특이도 93% 이상을 실현하여 촬영 후 3분 이내에 결과를 냅니다. Optos, Nikon 및 Google은 망막증과 함께 황반 부종을 감지하는 초광시야 AI 도구를 공동 개발했습니다. 임상의는 속도, 일관성 및 전문 독자의 의존도 감소를 평가하고 있으며, AI 대응 카메라는 스크리닝 프로그램의 확대에 필수적인 요소가 되고 있습니다.

높은 설비 투자와 OCT 콤보 시스템의 비교

콤비네이션 이미징 플랫폼은 정교한 기술 통합을 통해 프리미엄 가격을 요구하고 단독 안저 카메라 가격이 5만 달러 이하인 것에 비해 시스템은 종종 10만 달러를 초과합니다. 이 비용 차이는 종합적인 진단 기능을 제공하려고 하지만 엄격한 예산 제약 하에서 운영되는 전문 안과 클리닉 및 외래 수술 센터(ASC)에 특히 어려움이 있습니다. 복잡한 이미지 시스템과 관련된 지속적인 유지 보수 비용, 소프트웨어 라이선스 비용 및 직원 교육의 필요성을 고려하면 경제적인 압력이 더욱 커집니다.

부문 분석

무산동 시스템은 고통 없이 적하가 필요 없는 촬영으로 환자의 처리량을 가속화하여 2024년 안저 카메라 시장에서 48.17%의 점유율을 확보했습니다. EHR과의 완벽한 통합을 통해 AI 리뷰에 즉시 업로드할 수 있어 대규모 스크리닝 프로그램을 지원합니다. Zeis의 CIRRUS 6000은 네트워크 등급 사이버 보안과 미국 최대 OCT 참조 데이터베이스를 추가합니다. 하이브리드 및 광시야 디바이스는 CAGR 6.50%로 확대되어, 1회 촬영으로 최대 200도의 망막을 촬영해, 병변 검출율을 2배로 할 예정입니다.

초광 시야 카메라 수요는 당뇨병과 말초 망막 질환 관리로 확대됩니다. 눈동자 카메라는 최대한의 선명한 이미지나 연구 수준의 색심도가 필요한 경우에 필수적인 것으로 변함이 없습니다. 소아용 카메라는 맞춤형 광학 시스템으로 틈새 요구를 충족합니다. 이러한 제품군을 통해 공급자는 자본 예산과 균형을 유지하면서 임상 복잡성에 따라 이미지 심도를 얻을 수 있습니다.

2024년 안저 카메라 시장 점유율의 53.84%는 핸드헬드 장비였습니다. 스마트폰 연동형은 취득 비용을 억제하면서 동등한 정밀도를 달성했습니다. OCT와 안저 이미징을 융합한 콤비네이션 플랫폼은 1회로 종합적인 데이터를 요구하는 클리닉에 대응해, CAGR 7.25%를 나타낼 전망입니다.

거치형 탁상용 카메라는 이동성보다 이미지 일관성을 선호하는 대량 처리 센터에서 여전히 일반적입니다. SightSync와 같은 휴대용 OCT 장치는 POC(Point of Care) 진단을 지역 프로그램으로 확장합니다. 사용자 친화적인 디자인은 기술자 교육의 필요성을 줄이고 일반 클리닉에 광범위한 배포를 지원합니다.

지역 분석

북미는 견고한 의료 인프라, 유리한 상환 정책, AI 대응 진단 시스템의 조기 도입에 힘입어 2024년 시장 점유율 41.74%로 선두를 유지했습니다. 이 지역은 종합적인 당뇨병 망막증 스크리닝 프로그램과 다양한 임상 현장에서 안저 카메라 통합을 촉진하는 원격 의료 틀이 확립되어 있다는 장점이 있습니다. 주요 의료 시스템은 멀티모달 이미징 기능을 제공하는 첨단 조합 플랫폼에 투자하고 있으며, 지역에서는 지리적 접근 장벽을 해결하기 위해 휴대용 솔루션의 채택이 증가하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.86%로 가장 높은 성장 궤도를 보였습니다. 이는 의료 접근 구상 확대, 당뇨병 유병률 상승, 중국, 인도, 동남아시아 국가의 정부 지원 스크리닝 프로그램 등이 배경에 있습니다. 이 지역의 성장은 의료 인프라에 대한 많은 투자와 예방 안과 의료의 경제적 이익에 대한 인식 증가를 반영합니다. 지방의 지역 밀착형 안과 의료 모델은 기존 전문의에 대한 액세스를 제한하고 있던 지리적·경제적 장벽을 극복하기 위해 휴대용 안저 카메라와 스마트폰 기반의 이미지 솔루션에 중점을 둡니다. 유럽은 에너지 효율적인 핸드헬드 장비를 권장하는 ESG가 주도하는 조달 정책과 장비의 품질과 안전 기준을 보장하는 종합적인 규제 프레임워크를 지원하여 안정적인 성장을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당뇨병 망막증의 스크리닝 의무화의 가속

- Ai 임베디드 이미지 워크플로우의 급속한 보급

- 노화황반변성(AMD)의 급증

- 원격 안과 진료 보수의 평준화

- 스마트폰 기반 신생아 ROP 스크리닝 롤아웃

- 저에너지 핸드헬드를 선호하는 ESG 연동 조달

- 시장 성장 억제요인

- OCT-콤보 시스템에 비해 고액의 설비투자

- LMICs에서 안과 기술자의 부족

- 클라우드 기반 망막 아카이브의 데이터 프라이버시 장애물

- 광학 부품의 수입 관세 변동

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(단위 : 달러)

- 제품 유형별

- 동공확대 안저 카메라

- 비동공확대 안저 카메라

- 하이브리드/광시야 안저 카메라

- 기타 제품 유형

- 모달리티별

- 휴대용 기기

- 탁상형/고정식 시스템

- 복합 영상 플랫폼

- 용도별

- 당뇨병 망막병증

- 녹내장

- 노인성 황반변성

- 미숙아망막병증

- 기타 적응증

- 최종 사용자별

- 병원

- 전문 및 안과 클리닉

- 외래 수술 센터(ASC)

- 검진 및 원격 안과 프로그램

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Canon Inc.

- Carl Zeiss Meditec AG

- Topcon Healthcare

- NIDEK Co., Ltd.

- Kowa Company Ltd.

- Optos plc

- Revenio Group(iCare)

- Heidelberg Engineering GmbH

- Optomed Oy Ltd.

- Visionix

- Epipole Ltd.

- Phelcom Technologies

- Forus Health Pvt Ltd.

- Visunex Medical Systems

- Clarity Medical Systems

- Phoenix Technology Group

- HEINE Optotechnik

- Nikon Corp.

- Beye LLC

- Essilor Instruments USA

제7장 시장 기회와 전망

KTH 25.10.31The Fundus Camera Market size is estimated at USD 486.97 million in 2025, and is expected to reach USD 641.47 million by 2030, at a CAGR of 5.67% during the forecast period (2025-2030).

Demand strengthens as artificial-intelligence algorithms move from pilot to routine use, with FDA-cleared platforms such as IDx-DR and EyeArt showing more than 96% sensitivity for diabetic-retinopathy detection. Mandatory screening programs, improved reimbursement for tele-ophthalmology, and CMS guidance that recognizes AI-interpreted fundus photography as medically necessary are expanding adoption. Product preferences continue to favor non-mydriatic systems that integrate smoothly with electronic health records, yet hybrid and ultra-widefield devices are growing fastest because they capture up to 200 degrees of retinal surface. Portable hand-held cameras dominate modality demand, while combination platforms that fuse OCT and fundus photography gain momentum for comprehensive retinal assessment. Regionally, North America leads on market share, but Asia-Pacific posts the highest growth as diabetes prevalence rises and governments invest in community eye-care delivery.

Global Fundus Camera Market Trends and Insights

Accelerating Diabetic-Retinopathy Screening Mandates

Many countries now require annual retinal exams for people with diabetes, and U.S. Medicare policies deem AI-interpreted fundus images medically necessary. These rules spur bulk purchases of cameras that produce AI-ready images and support telemedicine workflows. More than 4.1 million U.S. adults live with diabetic retinopathy, and systematic screening using fundus cameras prevents avoidable vision loss while lowering long-term care costs.

Rapid Adoption of AI-Embedded Imaging Workflows

FDA-cleared AI platforms such as IDx-DR deliver >= 96% sensitivity and >= 93% specificity, producing results within three minutes of capture. Optos, Nikon and Google have co-developed ultra-widefield AI tools that detect macular edema alongside retinopathy. Clinicians value the speed, consistency and reduced dependence on specialist readers, making AI-enabled cameras an essential element of expanded screening programs.

High Capex Versus OCT-Combo Systems

Combination imaging platforms command premium pricing due to their sophisticated technology integration, with systems often exceeding USD 100,000 compared to standalone fundus cameras priced below USD 50,000. This cost differential becomes particularly challenging for specialty eye clinics and ambulatory surgical centers operating under tight budget constraints while seeking to offer comprehensive diagnostic capabilities. The economic pressure intensifies when considering ongoing maintenance costs, software licensing fees, and staff training requirements associated with complex imaging systems.

Other drivers and restraints analyzed in the detailed report include:

- Prevalence Spike of Age-Related Macular Degeneration

- Tele-Ophthalmology Reimbursement Parity

- Shortage of Trained Ophthalmic Technicians in LMICs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-mydriatic systems secured 48.17% share of the fundus camera market in 2024 thanks to painless, drop-free imaging that accelerates patient throughput. Their seamless EHR integration enables instant upload for AI review, supporting large screening programs. Zeiss's CIRRUS 6000 adds network-grade cybersecurity and the largest OCT reference database in the United States. Hybrid and wide-field devices are slated to expand at a 6.50% CAGR, capturing up to 200 degrees of retina in a single shot and doubling lesion detection rates.

Demand for ultra-widefield cameras grows in diabetic and peripheral-retinal disease management. Mydriatic cameras remain essential when maximum image clarity or research-grade color depth is required. Pediatric-specific cameras fill niche needs with tailored optics. The product palette thus enables providers to match imaging depth with clinical complexity while balancing capital budgets.

Hand-held devices held 53.84% of the fundus camera market share in 2024 as portability opened doors to rural clinics, emergency rooms and drive-through screenings. Smartphone-coupled models achieve comparable accuracy with lower acquisition cost. Combination platforms that merge OCT and fundus imaging will grow at a 7.25% CAGR, responding to clinics that want comprehensive data in one sitting.

Stationary table-top cameras remain common in high-volume centers that prioritize image consistency over mobility. Portable OCT units such as SightSync extend point-of-care diagnostics to community programs. User-friendly designs reduce technician training needs, supporting wider deployment across general-practice offices.

The Fundus Camera Market is Segmented by Product Type (Mydriatic Fundus Cameras, Non-Mydriatic Fundus Cameras, Hybrid Fundus Cameras, and More), Modality (Hand-Held Devices, and More), Application (Diabetic Retinopathy, Glaucoma, and More), End-User (Hospitals, Specialty & Eye Clinics, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintains market leadership with 41.74% share in 2024, supported by robust healthcare infrastructure, favorable reimbursement policies, and early adoption of AI-enabled diagnostic systems. The region benefits from comprehensive diabetic retinopathy screening programs and established telemedicine frameworks that facilitate fundus camera integration across diverse clinical settings. Major healthcare systems invest in advanced combination platforms that provide multimodal imaging capabilities, while rural areas increasingly adopt portable solutions to address geographic access barriers.

Asia-Pacific demonstrates the highest growth trajectory at 6.86% CAGR through 2030, driven by expanding healthcare access initiatives, rising diabetes prevalence, and government-backed screening programs across China, India, and Southeast Asian countries. The region's growth reflects substantial investments in healthcare infrastructure and increasing recognition of preventive eye care's economic benefits. Rural community-based eye care models emphasize portable fundus cameras and smartphone-based imaging solutions to overcome geographic and economic barriers that traditionally limited specialist access. Europe maintains steady growth supported by ESG-driven procurement policies that favor energy-efficient handheld devices and comprehensive regulatory frameworks that ensure device quality and safety standards.

- Canon

- Carl Zeiss

- Topcon Healthcare

- Nidek

- Kowa

- Optos

- Revenio Group

- Heidelberg Engineering

- Optomed Oy

- Visionix

- Epipole

- Phelcom Technologies

- Forus Health Pvt Ltd.

- Visunex Medical Systems

- Clarity Medical Systems

- Phoenix Technology Group

- HEINE Optotechnik

- Nikon Corp.

- Beye

- EssilorLuxottica

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Diabetic-Retinopathy Screening Mandates

- 4.2.2 Rapid Adoption of Ai-Embedded Imaging Workflows

- 4.2.3 Prevalence Spike of Age-Related Macular Degeneration (AMD)

- 4.2.4 Tele-Ophthalmology Reimbursement Parity

- 4.2.5 Smartphone-Based Neonatal ROP Screening Roll-Outs

- 4.2.6 ESG-Linked Procurement Favouring Low-Energy Handhelds

- 4.3 Market Restraints

- 4.3.1 High Capex Versus OCT-Combo Systems

- 4.3.2 Shortage of Trained Ophthalmic Technicians in LMICs

- 4.3.3 Data-Privacy Hurdles for Cloud-Based Retinal Archives

- 4.3.4 Import-Tariff Volatility on Optical Components

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Mydriatic Fundus Cameras

- 5.1.2 Non-mydriatic Fundus Cameras

- 5.1.3 Hybrid / Wide-field Fundus Cameras

- 5.1.4 Other Product Types

- 5.2 By Modality

- 5.2.1 Hand-held Devices

- 5.2.2 Table-top / Stationary Systems

- 5.2.3 Combination Imaging Platforms

- 5.3 By Application

- 5.3.1 Diabetic Retinopathy

- 5.3.2 Glaucoma

- 5.3.3 Age-related Macular Degeneration

- 5.3.4 Retinopathy of Prematurity

- 5.3.5 Other Indications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specialty & Eye Clinics

- 5.4.3 Ambulatory Surgical Centres

- 5.4.4 Screening & Tele-ophthalmology Programs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Canon Inc.

- 6.3.2 Carl Zeiss Meditec AG

- 6.3.3 Topcon Healthcare

- 6.3.4 NIDEK Co., Ltd.

- 6.3.5 Kowa Company Ltd.

- 6.3.6 Optos plc

- 6.3.7 Revenio Group (iCare)

- 6.3.8 Heidelberg Engineering GmbH

- 6.3.9 Optomed Oy Ltd.

- 6.3.10 Visionix

- 6.3.11 Epipole Ltd.

- 6.3.12 Phelcom Technologies

- 6.3.13 Forus Health Pvt Ltd.

- 6.3.14 Visunex Medical Systems

- 6.3.15 Clarity Medical Systems

- 6.3.16 Phoenix Technology Group

- 6.3.17 HEINE Optotechnik

- 6.3.18 Nikon Corp.

- 6.3.19 Beye LLC

- 6.3.20 Essilor Instruments USA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment