|

시장보고서

상품코드

1846329

커스텀 시술 팩 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Custom Procedure Packs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

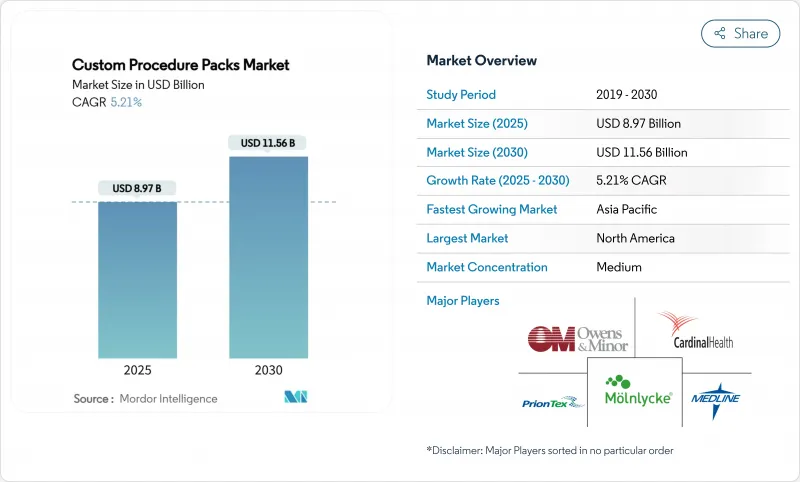

세계의 커스텀 시술 팩 시장 규모는 2025년에 89억 7,000만 달러로 추정되고, 2030년에는 115억 6,000만 달러로 확대될 것으로 예측되며, 예측 기간 중 CAGR 5.21%로 성장할 전망입니다.

수술 건수 증가, 외래 채용 확대, 소모품 표준화에 대한 병원 수준의 압력이 수요를 촉진하는 한편, 스마트 팩의 혁신과 증강현실 교육은 제품 차별화를 촉진합니다. 미국의 양호한 상환 전환 및 아시아태평양의 헬스케어 제공 모델에 대한 민간 자본 투자 증가는 성장을 더욱 향상시킵니다. 한편, 의료용 폴리머의 지속가능성에 대한 규제 및 공급망의 취약성으로 인해 비용과 컴플라이언스가 복잡해지고 있으며, 제조업체는 이를 능숙하게 극복해야 합니다. 틈새 이노베이터가 고성장 뇌신경 수술 및 심장병학의 하위 부문을 목표로 하고 있는 반면, 경쟁의 심각성은 여전히 완만하며, 소수의 규모를 가진 기업이 핵심 지역을 지배하고 있습니다.

세계의 커스텀 시술 팩 시장 동향 및 인사이트

외과 수술 건수 증가

외래수술센터(ASC)는 2034년까지 4,400만 건의 수술을 처리했으며, 2024년 수준에서 21% 증가할 것으로 예측됩니다. 노화로 인해 정형외과, 심장 병학 및 신경 외과 수술에 대한 수요가 증가하고 있으며, 이들은 모두 회전 시간을 단축하기 위해 기성품 무균 키트에 의존합니다. 메디케어 및 메디케이드 서비스센터(CMS)는 2026년 ASC 대상 수술 리스트에 276 수술을 새롭게 추가해 전문 팩의 대응 가능 베이스를 직접 확대했습니다. ASC의 경로를 이용한 외래에서의 견관절 전치환술은 입원에 비해 증례당 3,614-5,594달러의 절약이 되어, 경제적 인센티브가 강화되기 때문에 의료 제공업체는 점점 표준화된 키트를 선호하게 되고 있습니다. 이와 병행하여 외과의사가 당일치기 수술 프로토콜에 익숙해지면 더욱 복잡한 사례가 ASC로 이동하여 중기 수술 건수 증가가 예상됩니다.

혁신적인 도구 개발 및 출시 증가

기술 혁신의 파도가 키트의 구성을 검토하고 있습니다. 존슨 엔드 존슨은 1,480억 7,000만 달러의 의료 기술 전력 중 313억 5,000만 달러를 특수한 일회용이 필요한 심장병용 기기에 충당해, 커스텀 시술 팩의 보급을 가속화하고 있습니다. 뇌신경 수술은 주목할만한 프론티어입니다. 로봇 플랫폼은 수술 시간을 단축하고 부속 소모품을 묶은 기구 적합 멸균 팩 시장을 엽니다. 증강현실 훈련 및 원격 지도는 수술실 워크플로우를 재구성하여 몰입형 장비에 적합한 케이블, 센서 마운트, 보호 드레이프를 포함한 팩에 대한 수요를 창출하고 있습니다. 끊임없는 혁신으로 팩 제조업체는 재고 단위를 신속하게 새로 고쳐야 하기 때문에 구성 가능한 조립 라인과 민첩한 공급 네트워크의 전략적 가치가 높아지고 있습니다.

팩에 결함 및 중복 장치 존재

품질 결함은 신뢰를 손상시킵니다. 캐뉼라에 결함이 있었기 때문에 FDA가 알콘 커스텀 시술 팩 5만 7,352개를 클래스 II에서 회수한 것은 키트가 수술 중에 고장을 일으켰을 경우에 발생하는 오퍼레이션의 혼란을 돋보이게 하고 있습니다. 중복성은 또 다른 발판입니다. 병원은 연간 추정 200만 파운드의 미사용품을 폐기하고 있지만, 이는 주로 외과의사의 선호와 어긋난 제네릭 팩의 제조 결과입니다. 비용 분석에 따르면 공급 비용은 총 사례 수의 절반 이상을 차지하기 때문에 장비 중복은 이익률을 크게 줄입니다. 변동에 관한 연구에서는 외과의사 간 비용 변동의 최대 38.2%는 소모품의 사용법의 차이에 의한 것이며, 보다 엄격한 커스터마이즈가 필요하다고 하는 주장이 강해지고 있습니다. 자동 설정 엔진이 성숙할 때까지 회의적인 구매자는 채용을 억제할 수 있으며 단기적인 사용자 지정 프로시저 팩 시장의 확대가 억제됩니다.

부문 분석

2024년 커스텀 시술 팩 시장의 71.51%는 단일 사용 키트이며, 감염 관리 프로토콜의 보급과 OR의 효율화를 반영하고 있습니다. 의료 제공업체는 재처리의 번거로움을 최소화하고 잔류 바이오바덴 위험을 제거하는 무균으로 즉시 폐기할 수 있는 세트를 높이 평가합니다. 재사용 가능한 대체품의 맞춤 프로시저 팩 시장 규모는 대규모 시스템이 사이클 카운트를 확인하기 위한 디지털 추적과 결합한 멸균 허브를 시험적으로 도입했기 때문에 CAGR 예측 8.25%에 의해 지원되고 급성장하고 있습니다. 효과적인 재처리 패스웨이에 대한 최근의 FDA 지침은 컴플라이언스 장애물을 낮추고 예산에 제약이 있는 시설에 관심을 불러일으켰습니다. 환경 스튜어드십 프로그램을 통해 유럽의 일부 구매자는 재사용 가능한 직물과 내구성있는 트레이에 더 기울고 있지만 중앙 무균 업그레이드 비용은 여전히 장벽이 되고 있습니다. 향후 예측에서는 병원은 이중 경로를 채택하고, 고도급성기 의료나 시간적 제약이 있는 전문 의료에는 일회용을 예약하고, 증례 수가 집중되어 자본 레이아웃이 정당화되는 경우에는 재이용 가능한 팩을 도입할 것으로 예측됩니다.

리유저블의 채용은 사이클 프루프 소재나 오토클레이브에 대한 노출을 기록하고 무균 보증 레벨이 충족되었는지 확인하면서 분석 대시보드에 반영하는 RFID 칩을 포함한 기술 혁신과 일치하고 있습니다. 이 축에서 경쟁하는 공급업체는 종종 하이브리드 팩 포트폴리오를 제공하며 조달 팀에게 임상적, 경제적, 지속가능성의 성과를 균형있게 만드는 레버를 제공합니다. 신흥 클라우드 플랫폼은 세척 소독기의 성능 데이터를 OR 스케줄링과 통합하여 기구 세트의 저스트 인 타임 배송을 가능하게 하고 재고 부동을 줄입니다. 이러한 개발로 커스텀 프로 시저 팩 시장에서 재사용 가능한 팩은 단일 사용 우위를 전반적으로 대체하는 것이 아니라 오히려 보완하는 것으로 신뢰할 수 있습니다.

지역 분석

2024년 커스텀 시술 팩 시장 점유율은 40.32%로 북미가 선도하고 있으며, 이는 고급 상환 구조와 밀집한 외래 네트워크에 지지되고 있습니다. 2025년 CMS에 의한 2.9%의 외래 환자 지불 인상은 ASC의 치료 등록의 확대와 맛물려 직접적으로 유닛 수요를 확대합니다. 그래도 공급망의 비틀림은 계속됩니다. 의료기관 간부의 93%는 병행 조달 및 안전 재고의 쌓기에 박차를 가하고 있는 거듭되는 공급 부족을 들고 있습니다. 2026년에 다가온 FDA 품질경영시스템 규정은 컴플라이언스 비용을 상승시키지만, ISO-13485의 세계 표준에 맞추어 수출 전망을 강화할 것입니다. 중기적으로는 주요 IDN의 디지털 추적성 테스트 운영이 표준 관행으로 전환되어 기술 지원 팩 공급업체의 선행자 이익을 확고히 할 것으로 예측됩니다.

아시아태평양은 가장 성장 현저한 지역으로 병원 건설 붐과 인구대국에서의 수술 보급률의 상승을 배경으로 2030년까지 CAGR 9.71%로 성장할 전망입니다. 의료보험 적용을 확대하는 정부 프로그램과 적극적인 프라이빗 에퀴티 활동에 의해 복잡한 처치에 대응할 수 있는 고도 급성기 수술센터에 자본이 유입되고 있습니다. 이 지역은 병원 공급망의 Industry 4.0의 조기 도입 지역이기도 하며, IoT와 분석 도구를 통합한 후의 연계 지표로 61.3%의 향상을 기록하고 있습니다. 중국, 인도, 동남아시아의 CDMO는 비용 효율적인 조립 능력을 제공하며, 구미 OEM은 고분자의 이중 조달 및 희소성 위험을 줄일 수 있습니다.

유럽에서는 규제의 조화가 진행되고 안정된 수요가 유지되고 있습니다. 포장 및 포장 폐기물 규정 2025/40은 재료 혁신과 재활용 루프를 추진하고 생산자에게 2030년까지 접촉에 민감하면서도 재활용 가능한 솔루션을 제공합니다. EU 의료기기 규정의 개정은 조기 중단 경고를 의무화하고 병원에 대한 조달 가시성을 향상시키고 토단장에서의 팩 대체를 줄였습니다. 독일과 네덜란드의 산업 클러스터는 폐쇄형 루프 회수 시스템을 시험적으로 도입하여 재생 폴리프로필렌을 비멸균 부품으로 되돌리고 단일 사용 안전과 순환 경제의 의무화를 양립시키는 방법을 보여줍니다. 이러한 역학을 종합하면 유럽은 지속가능한 제품 설계 실험실로 강화되어 나중에 다른 성숙 시장으로 전환될 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 수술 건수 증가

- 혁신적 툴의 개발 및 발매 증가

- 의료 관련 감염 억제를 향한 멸균 용품의 일회용으로의 시프트

- 병원에 의한 절차의 표준화 추진에 의한 비용 절감

- 실시간 추적성을 위한 RFID 및 Iot 대응 스마트 팩

- 외래수술센터(ASC)의 특수 팩에 CAPEX 급증

- 시장 성장 억제요인

- 팩에 결함 및 중복 장치의 존재

- 규제 준수 및 리콜 리스크 증가

- 일회용 플라스틱에 대한 지속가능성에 대한 압력

- 의료 등급 폴리머 공급망 취약성

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 용도별

- 일회용

- 재사용

- 제품별

- 심장혈관 수술용 팩

- 미용 수술용 팩

- 일반 외과용 팩

- 정형외과용 팩

- 뇌신경 외과 팩

- 안과 수술 팩

- 기타 전문 팩

- 최종 사용자별

- 병원

- 클리닉

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medline Industries Inc.

- Owens & Minor Inc.

- Cardinal Health Inc.

- Molnlycke Health Care AB

- Solventum Corporation

- B. Braun SE

- PrionTex

- Unisurge International Ltd.

- Pennine Healthcare

- Kimal Group

- Med-Italia Biomedica Srl

- Hogy Medical Co., Ltd.

- Smiths Medical(ICU Medical)

- Lohmann & Rauscher

- Hartmann Group

- DeRoyal Industries

- Steris plc

- Defries Industries

- Merit Medical Systems

- Teleflex Medical

제7장 시장 기회 및 전망

AJY 25.11.10The global Custom procedure packs market size stands at USD 8.97 billion in 2025 and is forecast to expand to USD 11.56 billion by 2030, translating into a 5.21% CAGR over the period.

Accelerating surgical volumes, wider ambulatory adoption, and hospital-level pressure to standardize supplies propel demand, while smart-pack innovations and extended reality training amplify product differentiation. Growth is further underwritten by favorable reimbursement shifts in the United States and rising private-equity investment in Asia-Pacific healthcare delivery models. At the same time, sustainability mandates and supply-chain fragility for medical-grade polymers introduce cost and compliance complexities that producers must navigate deftly. Competitive intensity remains moderate, with a handful of scale players dominating core geographies even as niche innovators target high-growth neurosurgery and cardiology sub-segments.

Global Custom Procedure Packs Market Trends and Insights

Increasing Volume Of Surgical Procedures

Sustained growth in global surgical interventions underpins the Custom procedure packs market, with ambulatory surgical centers (ASCs) forecast to handle 44 million procedures by 2034, up 21% from 2024 levels. Ageing populations intensify demand for orthopedic, cardiology, and neurosurgery interventions, all of which rely on ready-made sterile kits to compress turnover times. Policy momentum is equally supportive: the Centers for Medicare & Medicaid Services (CMS) has added 276 new procedures to the ASC Covered Procedures List for 2026, directly enlarging the addressable base for specialty packs. Providers increasingly prefer standardized kits because outpatient total shoulder arthroplasty on an ASC pathway saves USD 3,614-5,594 per case versus inpatient settings, reinforcing economic incentives. In parallel, rising surgeon comfort with day-surgery protocols is likely to push more complex cases into the ASC space, sustaining mid-term volume growth.

Rising Development & Launch Of Innovative Tools

A wave of innovation is recalibrating kit composition. Johnson & Johnson has earmarked USD 31.35 billion of its USD 148.07 billion medtech war-chest for cardiology devices that require specialized disposables, amplifying pull-through for custom packs. Neurosurgery is a notable frontier; robotic platforms reduce operative time and open a market for instrument-compatible sterile packs that bundle accessory disposables. Extended reality training and tele-proctoring are reshaping operating theatre workflows, creating demand for packs that include cables, sensor mounts, and protective drapes suited to immersive equipment. Continuous innovation obliges pack manufacturers to refresh stock-keeping units rapidly, thereby raising the strategic value of configurable assembly lines and agile supply networks.

Presence Of Faulty Or Redundant Devices In Packs

Quality lapses erode confidence. The FDA's Class II recall of 57,352 Alcon Custom Pak units for cannula defects highlights the operational chaos caused when kits fail intraoperatively. Redundancy is another drag: hospitals discard an estimated 2 million lb of unused items annually, largely the result of generic pack builds misaligned with surgeon preference. Cost analyses show supply expense accounts for over half of total case spend, so device duplication materially dents margins. Variation studies attribute up to 38.2% of cost dispersion across surgeons to differing consumable use, strengthening the argument for tighter customization. Until automated configuration engines mature, skeptical purchasers may curtail adoption, tempering near-term Custom procedure packs market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Single-Use Sterile Supplies To Curb HAIs

- Hospital Push For Procedure-Standardization Cost Savings

- Heightened Regulatory Compliance & Recall Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-use kits held 71.51% of the Custom procedure packs market in 2024, reflecting widespread infection-control protocols and OR efficiency imperatives. Providers value sterile, ready-to-discard sets that minimize reprocessing labor and eliminate residual bio-burden risk. The Custom procedure packs market size for reusable alternatives is nonetheless growing quickly, underpinned by 8.25% CAGR projections as large systems pilot sterilization hubs paired with digital tracking to verify cycle counts. Recent FDA guidance on validated reprocessing pathways has lowered compliance hurdles, catalyzing interest among budget-constrained facilities. Environmental stewardship programs further tilt some European buyers toward reusable textiles and durable trays, though the cost of central sterile upgrades remains a gating variable. Over the forecast, hospitals are expected to operate dual pathways, reserving disposables for high-acuity or time-constrained specialties and deploying reusable packs where case volume concentration justifies capital layout.

Reusable adoption is matched by innovation in cycle-proof materials and embedded RFID chips that log autoclave exposure, ensuring sterility assurance levels are met while feeding analytics dashboards. Vendors competing on this axis often offer hybrid pack portfolios, giving procurement teams levers to balance clinical, economic, and sustainability outcomes. Emerging cloud platforms integrate washer-disinfector performance data with OR scheduling, enabling just-in-time dispatch of instrument sets and reducing inventory float. Such developments solidify reusable packs as a credible complement rather than a wholesale replacement of single-use dominance within the Custom procedure packs market.

The Custom Procedure Packs Market Report is Segmented by Use (Single-Use and Reusable), Product (Cardiovascular Surgery Packs, Cosmetic Surgery Packs, General Surgery Packs, Orthopedic Surgery Packs, and More), End-User (Hospitals, Clinics, and Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads with a 40.32% Custom procedure packs market share in 2024, anchored by advanced reimbursement structures and a dense ambulatory network. The CMS 2.9% outpatient payment uplift for 2025, coupled with an expanded ASC procedure roster, directly enlarges unit demand. Still, supply-chain kinks endure; 93% of provider executives cite recurring shortages that spur parallel sourcing and larger safety stock positions. The imminent 2026 FDA Quality Management System Regulation raises compliance costs yet should strengthen export prospects by aligning with global ISO-13485 norms. Over the medium term, digital traceability pilots in major IDNs are expected to transition into standard practice, cementing first-mover advantages for tech-enabled pack suppliers.

Asia-Pacific is the fastest-growing region, charting a 9.71% CAGR through 2030 on the back of hospital construction booms and rising surgical penetration rates in populous nations. Government programs to expand health-insurance coverage and aggressive private-equity activity are funneling capital into high-acuity surgical centers equipped for complex procedures. The region is also an early adopter of Industry 4.0 in hospital supply chains, posting 61.3% gains in collaboration metrics after integrating IoT and analytics tools, a development that favors agile pack vendors capable of electronic data interchange. CDMOs in China, India, and Southeast Asia offer cost-efficient assembly capacity, allowing Western OEMs to dual-source and mitigate polymer scarcity risks.

Europe sustains steady demand as regulatory harmonization progresses. The Packaging and Packaging Waste Regulation 2025/40 drives material innovation and recycling loops, challenging producers to deliver contact-sensitive yet recyclable solutions by 2030. Amendments to the EU Medical Device Regulation now obligate early disruption alerts, improving procurement visibility for hospitals and reducing last-minute pack substitutions. Industry clusters in Germany and the Netherlands are piloting closed-loop recovery systems, feeding reclaimed polypropylene back into non-sterile components, and illustrating a pathway to reconcile single-use safety with circular-economy mandates. Collectively, these dynamics reinforce Europe as a laboratory for sustainable product design that could later migrate to other mature markets.

- Medline Industries

- Owens & Minor Inc.

- Cardinal Health

- Molnlycke Health Care

- Solventum Corporation

- B. Braun

- PrionTex

- Unisurge International Ltd.

- Pennine Healthcare

- Kimal Group

- Med-Italia Biomedica Srl

- Hogy Medical Co., Ltd.

- Smiths Group

- Lohmann & Rauscher

- Hartmann Group

- DeRoyal Industries

- Steris plc

- Defries Industries

- Merit Medical Systems

- Teleflex Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Volume Of Surgical Procedures

- 4.2.2 Rising Development & Launch Of Innovative Tools

- 4.2.3 Shift Toward Single-Use Sterile Supplies To Curb Hais

- 4.2.4 Hospital Push For Procedure-Standardization Cost Savings

- 4.2.5 RFID- & Iot-Enabled Smart Packs For Real-Time Traceability

- 4.2.6 Ambulatory Surgical-Center CAPEX Surge For Specialty Packs

- 4.3 Market Restraints

- 4.3.1 Presence Of Faulty Or Redundant Devices In Packs

- 4.3.2 Heightened Regulatory Compliance & Recall Risk

- 4.3.3 Sustainability Pressure On Single-Use Plastics

- 4.3.4 Supply-Chain Fragility Of Medical-Grade Polymers

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Use

- 5.1.1 Single-Use

- 5.1.2 Reusable

- 5.2 By Product

- 5.2.1 Cardiovascular Surgery Packs

- 5.2.2 Cosmetic Surgery Packs

- 5.2.3 General Surgery Packs

- 5.2.4 Orthopedic Surgery Packs

- 5.2.5 Neurosurgery Packs

- 5.2.6 Ophthalmic Surgery Packs

- 5.2.7 Other Specialized Packs

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Clinics

- 5.3.3 Ambulatory Surgical Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medline Industries Inc.

- 6.3.2 Owens & Minor Inc.

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Molnlycke Health Care AB

- 6.3.5 Solventum Corporation

- 6.3.6 B. Braun SE

- 6.3.7 PrionTex

- 6.3.8 Unisurge International Ltd.

- 6.3.9 Pennine Healthcare

- 6.3.10 Kimal Group

- 6.3.11 Med-Italia Biomedica Srl

- 6.3.12 Hogy Medical Co., Ltd.

- 6.3.13 Smiths Medical (ICU Medical)

- 6.3.14 Lohmann & Rauscher

- 6.3.15 Hartmann Group

- 6.3.16 DeRoyal Industries

- 6.3.17 Steris plc

- 6.3.18 Defries Industries

- 6.3.19 Merit Medical Systems

- 6.3.20 Teleflex Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment