|

시장보고서

상품코드

1846335

내시경 협착 관리 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Endoscopic Stricture Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

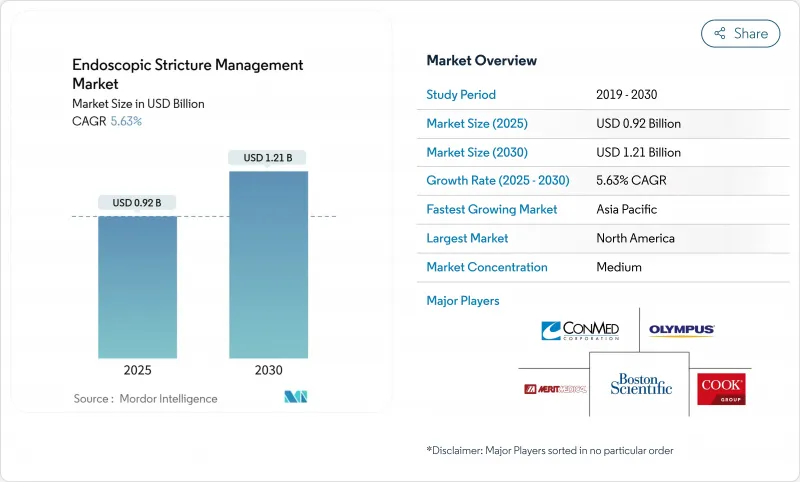

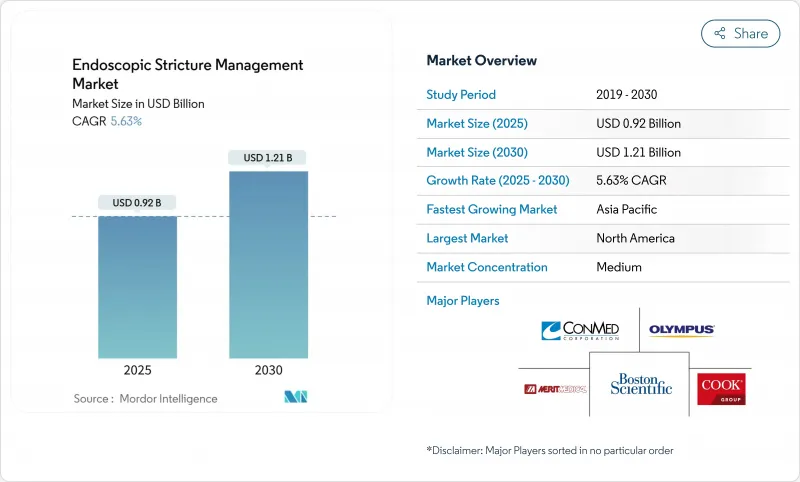

내시경 협착 관리 시장 규모는 2025년 9억 2,000만 달러로 추정되고, 2030년 12억 1,000만 달러에 이를 것으로 예상되며, CAGR 5.63%로 성장이 전망됩니다.

외래 환자의 수용 태세 확대, 장비의 급속한 기술 혁신, 저침습 치료에 대한 지불 측의 지원으로 병원과 의사는 개복 수술에서 내시경 솔루션으로 방향타를 끊고 있습니다. 풍선 확장기, 약물 코팅 플랫폼, 생분해성 스텐트, 내강 접착형 금속 스텐트는 회복 시간을 단축하고 합병증 위험을 감소시킵니다. 노인의 소화관 협착의 꾸준한 증가로 수술 건수는 증가의 길을 따라갔고, 외래수술센터(ASC)는 예전에는 입원 병동에 한정되어 있던 사례의 점유율을 확대하고 있습니다. 주요 공급업체가 포트폴리오를 확대하고 수직 통합이 기세를 높이고 신흥 기업이 차세대 기술에 대한 투자를 확보함에 따라 경쟁의 치열성이 커지고 있습니다.

세계의 내시경 협착 관리 시장 동향 및 인사이트

노인 인구 증가 및 소화관 협착 부담 증가

식도 협착의 유병률은 상업 보험 가입자의 경우 100,000명당 203.1명, 메디케어 수급자의 경우 10만 명당 1,123.5명에 이르며 연간 비용은 13억 9,000만 달러에 달할 전망입니다. 노인 환자의 경우 역류로 인한 협착과 문합 부위의 흉터가 자주 발생하며 확장술과 스텐트 유치술이 반복적으로 필요합니다. 치료되지 않은 협착은 영양 불량 및 오연을 일으켜 시스템 비용을 더욱 증가시킵니다. 신흥경제 국가에서 장수화가 진행됨에 따라 헬스케어 플래너는 외과적 재건술보다 비용이 낮고 내구성 있는 결과를 제공하는 내시경 치료 경로에 대한 의존도가 높아질 것으로 예상하고 있습니다.

저침습 내시경 확장술에 대한 선호

내시경 풍선 확장술은 요도 협착에 대해 67.1%의 성공률을 달성하여 최대 요 유량을 개선합니다. 또, 약제 코팅 풍선에서는 2년 후, 재개입의 자유도가 77.8%인 반면, 표준 치료에서는 23.6%입니다. 조기 회복과 통증 완화를 요구하는 환자의 요구는 입원 기간 제한을 요구하는 지불 측의 압력과 일치합니다. 병원과 ASC는 첨단 범위와 확장 플랫폼에 투자하고 치료 내시경 검사에 익숙한 젊은 소화기내과 의사가 일상 진료에서 채용을 가속화하고 있습니다.

고가의 장비 및 절차 비용

프리미엄 가격의 LAMS 및 약물 코팅 풍선은 많은 신흥 국가에서 자본 예산을 초과하고 있으며, 지불자는 장기적인 절약 효과가 입증되지 않은 경우 신속한 보험 적용을 망설이는 경우가 많습니다. 병원은 심장병학, 종양학, 외과학에 걸친 요구를 다루기 때문에 고급 내시경 시스템의 구입을 지연시키는 경우가 많습니다. 이용 관리는 접근을 제한하고 비용에 민감한 지역의 내시경 협착 관리 시장을 감속시킬 수 있습니다.

부문 분석

스텐트는 협착이 복잡하거나 악성일 경우 루멘의 개존성을 유지하는 역할을 확립하고 있기 때문에 2024년 내시경 협착 관리 시장의 45.41%를 지배했습니다. 풍선 확장기는 약물 코팅 표면과 제어 가능한 팽창 프로파일로 CAGR 6.45%에서 성장을 이끌고 있습니다. 내시경 협착 관리 시장 규모는 스텐트가 견조하게 확대될 것으로 예상되지만, 천공 위험이 낮아 평가되고 풍선에 의한 재수술이 증가하고 있습니다. 보스턴 사이언티픽의 CRE 풍선 플랫폼은 투시 시야를 향상시키고 메리트 메디컬의 랩소디 스텐트는 투석 접근에도 사용되고 전문 분야 횡단적인 기회를 시사하고 있습니다. 부지 확장기는 일회용 경제성과 풍선 확장을 통제하여 계속 감소하고 있습니다. 파클리탁셀이 포함된 약물 코팅 풍선은 ROBUST III 시험에서 77.8%의 재수술의 자유도를 나타내며 의사가 재발성 양성 협착에 채택하도록 권장합니다. 생분해성 스텐트는 제거 절차를 필요로 하지 않으며 LAMS는 더 넓은 플랜지로 이동에 대응합니다.

신흥 '기타' 카테고리-절개 장치, 흉터 방지 주사제, AI 가이드 기반 확장 플랫폼-은 여전히 작은 조각이지만 벤처 기업의 관심을 끌고 있습니다. 공급업체는 병원과 ASC 워크플로우 모두에 맞는 장비를 설계하고 재사용성과 사례당 비용 절감에 중점을 두어 소득환경 전반에 퍼져 나가고 있습니다. 초기 세대의 금속 스텐트에 특허의 절벽이 다가오는 가운데, 각사는 코팅, 전달의 인체공학, 실세계에서의 절약을 증명하는 근거 번들에 의해 차별화를 도모하고 있습니다.

2024년 식도 사례의 점유율은 51.45%로 역류 유행 및 수술 후 문합부의 흉터를 반영합니다. 식도 질환의 내시경 협착 관리 시장 점유율은 양성 협착에서 평생 동안 여러 번 확장술이 필요하기 때문에 높은 수준을 유지하고 있습니다. 한편, 십이지장의 치료는 영상 진단의 향상과 기기 지원에 의한 장 내시경 검사에 의해 소장 병변의 발견이 증가하기 때문에 2030년까지 CAGR 6.44%로 성장할 전망입니다. 올림푸스는 피사계 심도 확대 광학계를 탑재한 EZ1500 시리즈 스코프의 FDA 인가를 취득하여 십이지장 병변의 시인성을 향상시켰습니다. 담도 협착은 주로 스텐트 유치에 의한 치료로 안정적입니다.

비뇨기과, 간과, 대장 항문 외과의 각 전문과의 틀을 넘은 도입이 '기타'의 버킷을 지지하고 있어 요도나 췌장의 용도에서는 소화기 수술의 풍선이나 스텐트의 노하우가 채용되고 있습니다. 양성 식도 협착은 먼저 풍선을 선호하지만 악성 폐색은 직접 금속 스텐트로 이동합니다. 아시아태평양에서는 담도와 십이지장의 협착의 유병률이 높기 때문에 연구 개발에서는 이 지역에서 일반적인 좁은 루멘에 해당하는 크기의 스텐트가 선택되었습니다.

지역 분석

북미는 2024년 내시경 협착 관리 시장 매출액의 41.34%를 차지했으며, 여전히 기술의 견인 역할을 하고 있습니다. 메디케어 부위 중립 규칙과 광범위한 민간 지급기관의 연계는 외래환자로의 이행을 촉진하고 강력한 휄로우십 파이프라인이 인터벤셔널 내시경의사 층의 두께를 보장하고 있습니다. 장비 제조업체는 매우 중요한 데이터를 생성하는 이른 어댑터 클리닉을 활용하기 때문에 미국에서 처음 출시하는 경우가 많습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 6.66%로 성장을 이끌 것으로 예측됩니다. 중국의 연간 초음파 내시경 수술 건수는 2012년 20만 7,166건에서 2019년에는 46만 4,182건으로 증가하고 있으며, 국민 1인당 사용률이 선진국을 밑돌고 있음에도 불구하고 고급 도구의 신속한 도입이 밝혀졌습니다. 인도에서는 AI를 활용한 검출 소프트웨어가 시험적으로 도입되어 선종의 검출률이 상승했습니다. 일본은 국민 모두 보험제도와 협착을 조기에 발견하는 국민 의식 향상 캠페인에 도움을 받고 이 지역의 수술 건수 리더로 계속되고 있습니다. 호주와 한국은 고화질 시스템과 의료 관광에 투자하여 지역 환자를 유치하고 있습니다.

유럽은 성숙하지만 성장은 둔합니다. 엄격한 트레이닝 기준(자격 인정에는 EUS 지도 증례 250례)이 질을 높이고 있지만, 예산의 상한이 프리미엄 DCB 및 LAMS로의 전환을 억제하고 있습니다. 독일과 영국은 병원 기반의 왕성한 검사 건수를 유지하고 있으며, 북유럽 국가들은 번들 결제로 외래 환자의 성장을 뒷받침하고 있습니다.

남미와 중동 및 아프리카는 새로운 비즈니스 기회 영역입니다. 브라질의 공립 병원을 위한 통일 조달은 가격 협상에 도움이 되며 스텐트에 대한 접근을 촉진합니다. 남아프리카공화국은 민간 공적 병원 클러스터를 통해 사하라 이남에서 채용을 이끌고 있지만 농촌 지역에서는 여전히 격차가 남아 있습니다. 원격지도 및 모듈식 내시경 검사실은 이러한 지역에서 노동력 부족을 해소하기 위해 노력하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령자 인구 증가 및 GI 협착 부담 증가

- 저침습의 내시경적 확장술에 대한 기호

- 지속적인 제품 혁신 : 다단 풍선 및 생분해성 스텐트

- 외래 협착 치료에 대한 상환 확대

- 루멘 부착형 금속 스텐트의 조기 임상 성공

- 환자 관리의 자기 확장 프로토콜의 출현

- 시장 성장 억제요인

- 높은 디바이스 및 기술 비용

- 훈련을 받은 인터벤셔널 내시경의의 부족

- 양성 협착에 있어서 LAMS의 적응 외 사용에 대한 안전성의 우려

- 약물 코팅 풍선 승인을 위한 제한된 장기 데이터

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 풍선 다이레이터

- 부지 다이레이터

- 스텐트

- 기타

- 협착 부위별

- 식도

- 담도

- 십이지장

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 기타

- 수술 설정별

- 입원환자

- 외래환자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Boston Scientific Corporation

- Olympus Corporation

- Becton, Dickinson and Company

- Cook Medical LLC

- CONMED Corporation

- STERIS

- Medi-Globe Corporation

- Hobbs Medical Inc.

- PanMed US

- Merit Medical Systems

- Micro-Tech Endoscopy

- Laborie

- Medtronic plc

- Karl Storz SE & Co. KG

- Taewoong Medical Co., Ltd.

- Endo-Flex GmbH

- PENTAX Medical(HOYA)

- ELLA-CS sro

- MI Tech Co., Ltd.

- Stryker Corporation

- Changzhou Health MicroPort Medical Device Co., Ltd.

제7장 시장 기회 및 전망

AJY 25.11.10The Endoscopic stricture management market size stands at USD 0.92 billion in 2025 and is forecast to reach USD 1.21 billion by 2030, translating into a 5.63% CAGR.

Expanding outpatient capacity, rapid device innovation, and payer support for minimally invasive treatments are steering hospitals and physicians away from open surgery toward endoscopic solutions. Balloon dilators, drug-coated platforms, biodegradable stents, and lumen-apposing metal stents shorten recovery times and lower complication risks, which aligns with payer incentives to cut inpatient costs. A steady rise in gastrointestinal strictures among older adults keeps procedure volumes growing, while ambulatory surgical centers (ASCs) capture a rising share of cases once restricted to inpatient wards. Competitive intensity is building as major suppliers broaden portfolios, vertical integration gains momentum, and emerging companies secure investment for next-generation technologies .

Global Endoscopic Stricture Management Market Trends and Insights

Growing Geriatric Population & Rising GI-Stricture Burden

Esophageal stricture prevalence reached 203.1 cases per 100,000 among commercially insured adults and 1,123.5 cases per 100,000 in Medicare beneficiaries, driving USD 1.39 billion in annual costs . Older patients often present with reflux-induced strictures or anastomotic scarring that require repeated dilations or stenting. Untreated strictures lead to malnutrition and aspiration, creating additional system costs. As longevity rises across developed economies, healthcare planners anticipate heavier reliance on endoscopic treatment pathways that cost less than surgical reconstruction yet deliver durable results.

Preference for Minimally Invasive Endoscopic Dilation

Endoscopic balloon dilation achieves 67.1% success in urethral strictures and improves maximum urinary flow, while drug-coated balloons show 77.8% freedom from re-intervention at two years versus 23.6% for standard therapy. Patient demand for fast recovery and lower pain dovetails with payer pressure to limit inpatient stays . Hospitals and ASCs invest in advanced scopes and dilation platforms, and younger gastroenterologists-trained heavily in therapeutic endoscopy-are driving faster adoption in daily practice.

High Device & Procedure Costs

Premium-priced LAMS and drug-coated balloons exceed capital budgets in many emerging economies, and payers often hesitate to grant quick coverage when long-term savings remain unproven. Hospitals juggle needs across cardiology, oncology, and surgery, often delaying purchases of advanced endoscopy systems. Utilization management controls can restrict access, slowing the Endoscopic stricture management market in cost-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Product Innovation: Multi-Stage Balloons & Biodegradable Stents

- Expanding Reimbursement for Outpatient Stricture Procedures

- Shortage of Trained Interventional Endoscopists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stents controlled 45.41% of the Endoscopic stricture management market in 2024 owing to their established role in maintaining luminal patency when strictures are complex or malignant. Balloon dilators lead growth at a 6.45% CAGR thanks to drug-coated surfaces and controllable inflation profiles. The Endoscopic stricture management market size for stents is projected to expand steadily, yet balloons increasingly capture repeat procedures as physicians value their lower perforation risk. Boston Scientific's CRE balloon platform improves fluoroscopic visibility, while Merit Medical's Wrapsody stent extends use into dialysis access, signaling cross-specialty opportunity. Bougie dilators continue to decline as single-use economics and controlled dilation favor balloons. Drug-coated balloons incorporating paclitaxel showed 77.8% freedom from repeat procedure in the ROBUST III trial, encouraging physicians to adopt them in recurrent benign strictures. Biodegradable stents eliminate removal procedures, and LAMS address migration with wider flanges.

The emerging "others" category-incision devices, anti-scarring injectables, and AI-guided dilation platforms-remains a small slice but attracts venture interest. Suppliers design devices that fit both hospital and ASC workflows, focusing on reusability and lower per-case cost to widen adoption across income settings. As patent cliffs approach for early-generation metal stents, companies differentiate through coatings, delivery ergonomics, and evidence bundles that document real-world savings.

Esophageal cases held 51.45% share in 2024, reflecting reflux prevalence and post-surgical anastomotic scarring. The Endoscopic stricture management market share for esophageal disease stays high because benign strictures often require multiple dilations over a lifetime. Duodenal procedures, however, grow at a 6.44% CAGR through 2030 as improved imaging and device-assisted enteroscopy increase detection of small-bowel lesions. Olympus earned FDA clearance for its EZ1500 series scopes with extended depth-of-field optics, improving duodenal lesion visibility. Biliary strictures remain steady, treated mainly with stent placement.

Cross-specialty uptake in urology, hepatology, and colorectal surgery supports the "others" bucket, where urethral and pancreatic applications adopt balloon and stent know-how from gastroenterology. Location drives therapy choice: benign esophageal strictures prefer balloons first, while malignant obstructions move directly to metal stents. In Asia-Pacific, higher prevalence of biliary and duodenal strictures nudges R&D toward devices sized for narrower lumens common in that population set.

The Endoscopic Stricture Management Market Report is Segmented by Product Type (Balloon Dilators, Bougie Dilators, Stents, Others), Stricture Location (Esophageal, Biliary, Duodenal, Others), End-User (Hospitals, Ambulatory Surgical Centers, Others), Procedure Setting (Inpatient, Outpatient), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 41.34% of Endoscopic stricture management market revenue in 2024 and remains the technology bellwether. Medicare site-neutral rules and broad private payor alignment nurture outpatient migration, while strong fellowship pipelines ensure a deep bench of interventional endoscopists. Device makers often launch first in the United States to leverage early adopter clinics that generate pivotal data.

Asia-Pacific is forecast to lead growth with a 6.66% CAGR through 2030. China's annual endoscopic ultrasound procedures rose from 207,166 in 2012 to 464,182 in 2019, revealing swift uptake of advanced tools even as per-capita usage trails developed nations. India rolled out AI-driven detection software that lifted adenoma detection rates in pilot sites, showing technology leapfrogging potential. Japan remains the region's procedure volume leader, aided by universal coverage and public awareness campaigns that catch strictures earlier. Australia and South Korea invest in high-definition systems and medical tourism, luring regional patients.

Europe holds a mature yet slower-growing position. Rigorous training standards-250 supervised EUS cases for credentialing-uphold quality, but budget caps temper switching to premium DCBs and LAMS. Germany and the United Kingdom maintain strong hospital-based volumes, while Nordic countries push outpatient growth via bundled payments.

South America and the Middle East & Africa are emerging opportunity zones. Brazil's unified procurement for public hospitals helps negotiate pricing, boosting stent access. South Africa leads sub-Saharan adoption through private-public hospital clusters, yet rural gaps remain. Tele-mentoring and modular endoscopy suites aim to solve workforce shortages in these regions.

- Boston Scientific

- Olympus

- Beckton Dickinson

- Cook Group

- Conmed

- STERIS

- Medi-Globe

- Hobbs Medical

- PanMed

- Merit Medical Systems

- Micro-tech

- Laborie

- Medtronic

- Karl Storz

- Taewoong Medical

- Endo-Flex

- PENTAX Medical (HOYA)

- ELLA-CS s.r.o.

- M.I. Tech Co., Ltd.

- Stryker

- Changzhou Health MicroPort Medical Device Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Geriatric Population & Rising GI?Stricture Burden

- 4.2.2 Preference For Minimally Invasive Endoscopic Dilation

- 4.2.3 Continuous Product Innovation: Multi-Stage Balloons & Biodegradable Stents

- 4.2.4 Expanding Reimbursement for Outpatient Stricture Procedures

- 4.2.5 Early Clinical Success of Lumen-Apposing Metal Stents

- 4.2.6 Emergence Of Patient-Managed Self-Dilation Protocols

- 4.3 Market Restraints

- 4.3.1 High Device & Procedure Costs

- 4.3.2 Shortage Of Trained Interventional Endoscopists

- 4.3.3 Safety Concerns Over Off-Label LAMS Use in Benign Strictures

- 4.3.4 Limited Long-Term Data for Drug-Coated Balloon Approvals

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Balloon Dilators

- 5.1.2 Bougie Dilators

- 5.1.3 Stents

- 5.1.4 Others

- 5.2 By Stricture Location

- 5.2.1 Esophageal

- 5.2.2 Biliary

- 5.2.3 Duodenal

- 5.2.4 Others

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 By Procedure Setting

- 5.4.1 Inpatient

- 5.4.2 Outpatient

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Boston Scientific Corporation

- 6.3.2 Olympus Corporation

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Cook Medical LLC

- 6.3.5 CONMED Corporation

- 6.3.6 STERIS

- 6.3.7 Medi-Globe Corporation

- 6.3.8 Hobbs Medical Inc.

- 6.3.9 PanMed US

- 6.3.10 Merit Medical Systems

- 6.3.11 Micro-Tech Endoscopy

- 6.3.12 Laborie

- 6.3.13 Medtronic plc

- 6.3.14 Karl Storz SE & Co. KG

- 6.3.15 Taewoong Medical Co., Ltd.

- 6.3.16 Endo-Flex GmbH

- 6.3.17 PENTAX Medical (HOYA)

- 6.3.18 ELLA-CS s.r.o.

- 6.3.19 M.I. Tech Co., Ltd.

- 6.3.20 Stryker Corporation

- 6.3.21 Changzhou Health MicroPort Medical Device Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment