|

시장보고서

상품코드

1846342

바이오메디컬 텍스타일 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biomedical Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

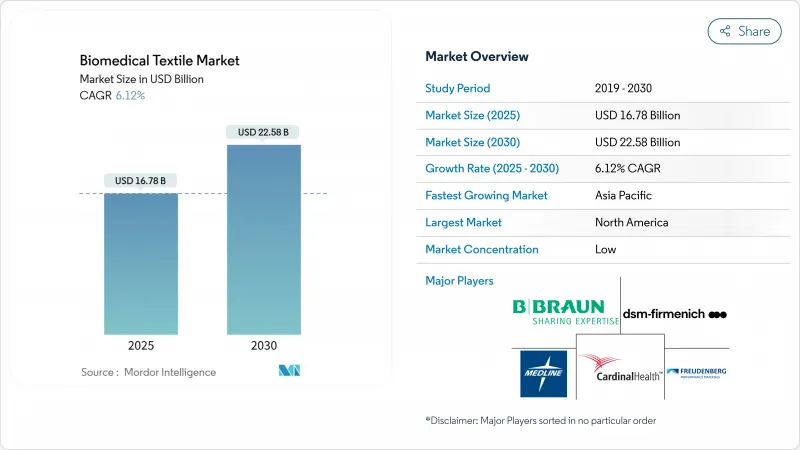

바이오메디컬 텍스타일 시장 규모는 2025년에 167억 8,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 6.12%로 성장할 전망이며, 2030년에는 225억 8,000만 달러에 달할 것으로 예측됩니다.

이 성장은 고령화로 인한 외과 수술의 작업량 확대, 저침습성 이식형 섬유의 상업화, 국방 섬유 연구를 민간의료로 전환시키는 안정적인 공적 자금 기여로 이루어져 있습니다. 또한 휴대 가능한 센서 부착 드레싱재에 의존하는 재택 치료 및 외래 진료로 간병 환경이 시프트함에 따라 수요도 높아집니다. FDA에 의한 생체적합성 시험에 관한 규제의 지속적인 명확화는 승인 사이클을 단축하고, 유럽의 일회용 플라스틱 규제는 퇴비화 가능한 섬유 및 생체 흡수성 스캐폴드로의 전환을 가속시킵니다. 플로이덴베르크에 의한 헤이텍스 인수와 같은 합병은 부직포 노하우를 집중시켜 공급의 탄력성을 강화하고 기술 혁신 일정을 단축시킵니다. 동시에, 소매 채널은 전기 방사 나노섬유 드레싱을 취급하게 되어, 선진적인 상처 제품이 주류에 받아들여져, 임상용 제품의 소비자를 위한 바리에이션에 경상적인 수입원이 생겼음을 나타내고 있습니다.

세계의 바이오메디컬 텍스타일 시장 동향 및 인사이트

수술 건수 증가

연령 중앙값이 상승하고 선택적 수술이 더 가까워짐에 따라 세계 수술 수는 늘어나고 있습니다. 미국 국방부의 나노 패브릭스 프로그램은 원래 전장에서의 치료를 목적으로 하고 있었지만, 항균사나 경량의 인공 혈관을 만들어 민간의 수술실에도 도입되고 있습니다. 병원에서는 절개 부위의 온도와 pH를 기록하는 프로그램 가능한 섬유를 통합하여 외과 의사가 드레싱을 벗기지 않고 감염 위험을 감지할 수 있습니다. 아시아태평양의 병원이 채용을 가속하고 있는 이유는 보험 적용률 향상으로 중간소득층이 수술실로 늘어나 1증례당 섬유 소비량이 증가하고 있기 때문입니다.

고품질 상처 케어용 섬유에 대한 요구 증가

고급 드레싱 소재는 회복을 가속화하고 재입원을 줄이며 간호 시간을 단축합니다. 스핀케어(Spincare)와 같은 전기방사 나노 섬유 제품은 임상시험에서 기존 거즈에 비해 재입원 없이 46.6%의 상피화율을 달성했습니다. 중국 공장은 박테리아의 성장을 억제하는 다기능 은이온 매트의 국내 수요를 충족하는 동시에 수출을 위한 생산량을 증가시켰습니다. 웨어러블 바이오센서는 현재 스펀본드 기판에 그래핀의 흔적을 매립해 방문 간호사가 모바일 대시보드로 상처의 수분을 원격으로 읽을 수 있도록 하고 있습니다. 이러한 기능은 만성 상처의 치료를 입원 병동에서 외래 및 재택 환경으로 이동시키려는 지불 측의 압력과 일치합니다.

인공 혈관 및 인공 피부의 높은 비용

조직 공학적 이식편은 무균 클린 룸, 몇 주간 세포 파종, 정밀한 뜨개질이 필요하기 때문에 많은 의료 시스템에서 상환 한도를 초과하는 가격이 되었습니다. 미국의 보험 가이드라인은 아직도 많은 생체공학적 드레싱재를 임상시험약으로 분류하고 있으며, 보험 적용이 제한되어 스케일 이코노미의 방해가 되고 있습니다. 수량이 수반되지 않으면 단가는 고정되어 라틴아메리카와 동남아시아의 일부에서는 병원에 의한 조달의 방해가 되고 있습니다.

부문 분석

생분해성 실은 2024년 매출의 40.48%를 차지했는데, 2030년까지 CAGR 8.12%로 바이오메디컬 텍스타일 시장을 선도할 전망입니다. 폴리유산과 폴리카프로락톤의 재흡수 프로파일이 FDA에서 인정되었으며 규제의 문이 열렸습니다. 신흥 기업은 현재 폴리유산 마이크로 화이버에 벌꿀 유래의 항균제를 코팅하고 항생제를 전신 투여하지 않고 감염 제어의 목표를 달성하고 있습니다.

폴리에틸렌 테레프탈레이트와 같은 비생분해성 섬유는 인대 수리 및 탈장용 메쉬와 같은 지속적인 내하중성이 필수적인 분야에서 우위를 유지하고 있습니다. 폴리에틸렌 테레프탈레이트는 수십년에 걸친 임상 데이터에 의해 지원되며 바이오메디컬 텍스타일 시장 점유율의 59.52%를 차지합니다. 생산자는 장시간 임플란트 시 입자의 방출을 억제하는 저탈락사 치료에 투자하고 있습니다. 이 2개의 섬유 유형이 통합되어 공급업체의 포트폴리오가 확대되고, 조달 팀은 재료를 절차의 복잡성에 맞출 수 있게 되어 바이오메디컬 텍스타일 시장의 회복력을 강화합니다.

부직포 라인은 2024년 매출의 62.43%를 차지했으며, 멜트블로우의 다용도성과 수분 밸런스를 위해 하이드로겔층을 매립하는 인라인 라미네이션에 의해 이 분야에서 최고의 CAGR 8.65%를 달성합니다. 플로이덴베르크는 ISO 13432의 퇴비화 가능 기준값을 충족하는 단일 사용 드레이프로 매일 700만 개의 플라스틱 병을 재활용합니다. 이 드레이프는 보풀이 적고 장벽 배치가 빠르기 때문에 병원에서 지원합니다.

직물과 니트의 형태는 정확한 인장 강도와 통제된 공극률이 요구되는 틈새 이식 도구에 유용합니다. 기술자들은 현재 자연의 혈관 분기를 모방하는 3D 분기 튜브를 짜고 섬유 기반 혈관 내 이식편의 적응을 확대하고 있습니다. 멜트블로운 항균 코어를 경편의 커버 사이에 라미네이트한 하이브리드 구조는 양자의 이점을 융합시킨 것으로, 이 동향은 바이오메디컬 텍스타일 시장의 광범위한 성장을 유지하는 데 도움이 되고 있습니다.

지역 분석

북미는 2024년 매출의 38.09%를 차지했으며, 이는 광범위한 보험 적용 및 연방 정부가 자금을 제공한 섬유 연구의 상업적 공급망으로의 신속한 전개가 원동력이 되고 있습니다. 국방부의 7,500만 달러의 스마트 패브릭 프로그램은 센서 원사를 제공하며 현재는 소비자용 음압 상처 피복재에 사용되고 있습니다. 2025년에 발표된 FDA의 생체적합성 지침을 통해 승인이 효율화되어 현지 기업이 조기에 계약을 획득할 수 있게 되었습니다. 스미스 앤 네퓨와 같은 주요 의료기기 제조업체의 자본 투자는 매사추세츠와 미네소타의 지역 제조 클러스터를 형성합니다.

아시아태평양은 각국 정부가 국민 모두 보험 제도를 확대하고 국내 의료기술 생산을 자극함으로써 2030년까지 CAGR 7.42%로 성장할 전망입니다. 중국은 수출 주문과 국내 수요를 모두 충족하기 위해 나노섬유 제조 라인을 적극적으로 확장하고, 일본은 센서 내장 거즈에 의존하는 노인 원격 간병 조종사 사업에 자금을 제공합니다. ASEAN 의료기기 지령에 의한 규제의 조화는 진입 장벽을 서서히 낮추어 다국적 벤더와 지역 벤더를 똑같이 지원합니다.

유럽에서는 첨단 규제와 지속가능성 요청이 융합되어 있습니다. EU의 단일 사용 플라스틱 지침은 특정 화석 유래 디스포저블을 금지하기 때문에 병원은 렌칭 셀룰로오스 스텐트 커버와 바이오 부직포 패드를 시험하고 있습니다. 플로이덴베르크는 헤이텍스의 인수를 활용하여 음압 치료기용 폴리우레탄 코팅 기재를 공급하고 있습니다. 그럼에도 불구하고 폐기물 감축 규칙은 컴플라이언스 비용을 증가시켰습니다. 공급업체는 퇴비화 가능성 증명과 폐쇄 루프 재활용 감사를 통해 성공했습니다.

남미와 중동 및 아프리카는 금액면에서 뒷쳐져 있지만, 3차 병원의 개설과 정부에 의한 외상 네트워크에의 보조금에 의해 대수의 성장은 가속하고 있습니다. 현지에서 재활용된 PET로 만든 비용 최적화된 스펀본드 상처 패드는 가격과 충분한 장벽 기능의 균형을 이룹니다. 국제 NGO는 조달 교육을 지원하고 임상의가 증거를 뒷받침하는 섬유 솔루션을 선택할 수 있도록 하여 바이오메디컬 텍스타일 시장의 저변을 넓히고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 수술 건수 증가

- 고품질의 상처 케어용 텍스타일에 대한 요구 고조

- 주요국에서의 급속한 고령화

- 저침습성 임플란트용 섬유의 진보

- 소매 채널에 진입하는 생체 흡수성 전기 방사 나노 화이버 드레싱

- 의료용 스마트 섬유의 크로스 오버를 가속하는 국방부 출자의 센서 섬유

- 시장 성장 억제요인

- 인공 혈관 및 인공 피부의 고비용

- 전자섬유 및 텍스타일의 통합의 복잡성

- 항균 바이오텍스타일의 보존 가능 기간 기준의 부재

- 의료용 부직포의 일회용 폐기물에 대한 규제의 반발

- 밸류체인 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 섬유 유형별

- 비생분해성 섬유

- 생분해성 섬유

- 원단 형태별

- 부직포

- 직포

- 기타 원단 유형(니트, 블레이드)

- 용도별

- 비 이식형

- 이식 가능

- 기타 이식형(체외식 등)

- 최종 사용자별

- 병원 및 외과 센터

- 외래의료센터

- 재택 헬스케어

- 스포츠 의학 및 정형외과 클리닉

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%) 및 랭킹 분석

- 기업 프로파일

- Ahlstrom

- ATEX TECHNOLOGIES INC.

- B. Braun SE

- Bally Ribbon Mills

- Cardinal Health

- CORTLAND BIOMEDICAL

- dsm-firmenich

- Freudenberg Performance Materials

- Lenzing AG

- Medline Industries LP

- Meister & Cie AG

- Milliken & Company

- Secant Group, LLC

- Smith Nephew

제7장 시장 기회 및 전망

AJY 25.11.10The Biomedical Textile Market size is estimated at USD 16.78 billion in 2025, and is expected to reach USD 22.58 billion by 2030, at a CAGR of 6.12% during the forecast period (2025-2030).

This growth rests on the expanding surgical workload created by older populations, the commercialization of minimally-invasive implantable fabrics, and steady public-sector funding that migrates defense textile research into civilian care. Demand also rises as care settings shift toward home health and ambulatory clinics that rely on portable, sensor-ready dressings. Sustained regulatory clarity from the FDA on biocompatibility testing shortens approval cycles, while Europe's single-use plastics rules accelerate the switch to compostable fibers and bioresorbable scaffolds. Mergers such as Freudenberg's acquisition of Heytex concentrate know-how in nonwovens, strengthening supply resilience and shortening innovation timelines. Simultaneously, retail channels now stock electro-spun nanofiber dressings, signaling mainstream acceptance of advanced wound products and opening recurring revenue streams for consumer-facing variants of clinical lines.

Global Biomedical Textile Market Trends and Insights

Rising Number of Surgeries

Global surgical procedures continue to climb as median ages rise and elective interventions become more accessible. The U.S. Department of Defense's nanofabric programs, originally aimed at battlefield care, generate antimicrobial yarns and lightweight vascular grafts that transfer into civilian operating rooms. Hospitals integrate programmable fibers that record temperature and pH at incision sites, letting surgeons detect infection risk without removing dressings. Asia-Pacific hospitals accelerate adoption because improved insurance coverage brings larger middle-class cohorts into surgical theaters, amplifying textile consumption per case.

Growing Need for High-Quality Wound Care Textiles

Advanced dressings shorten recovery, lower readmissions, and reduce nursing time. Electro-spun nanofiber products, such as Spincare, achieved 46.6% epithelialization without rehospitalization versus conventional gauze in clinical trials. Chinese factories boost output for export while also meeting domestic demand for multifunctional silver-ion mats that limit bacterial growth. Wearable biosensors now embed graphene traces into spun-bond substrates, allowing home-care nurses to remotely read wound moisture on mobile dashboards. These capabilities align with payer pressure to shift chronic-wound treatment from inpatient wards to outpatient and home settings.

High Cost of Vascular Grafts & Artificial Skin

Tissue-engineered grafts require sterile cleanrooms, multi-week cell seeding, and precision weaving, driving prices beyond reimbursement caps in many health systems. Insurance guidelines in the United States still classify numerous bioengineered dressings as investigational, limiting coverage and slowing scale economies. Without volume, unit costs remain high, deterring procurement by hospitals in Latin America and parts of Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Aging Population

- Advances in Minimally-Invasive Implantable Textiles

- Electronic-Textile Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biodegradable threads account for 40.48% of 2024 revenue, yet are pacing the biomedical textile market at an 8.12% CAGR through 2030. FDA recognition of poly-lactic acid and poly-caprolactone resorption profiles opens regulatory doors, and surgeons value scaffolds that dissolve, eliminating follow-up retrieval. Start-ups now coat polylactic acid microfibers with honey-derived antimicrobials to meet infection control goals without systemic antibiotics.

Non-biodegradable fibers such as polyethylene terephthalate retain dominance where permanent load-bearing is vital, including ligament repairs and hernia meshes. They hold 59.52% of the biomedical textile market share, supported by decades of clinical data. Producers invest in low-shedding yarn treatments that reduce particle release during long implants. Together, these dual fiber classes widen supplier portfolios and let procurement teams match materials to procedure complexity, reinforcing the resilience of the biomedical textile market.

Non-woven lines posted 62.43% 2024 revenue and deliver the sector's highest 8.65% CAGR due to melt-blown versatility and inline lamination that embeds hydrogel layers for moisture balance. Production scale allows Freudenberg to recycle 7 million PET bottles daily into single-use drapes that meet ISO 13432 compostability thresholds. Hospitals favor these drapes for reduced lint and rapid barrier deployment.

Woven and knitted formats serve niche implantables that demand precise tensile strength and controlled porosity. Engineers now weave 3D bifurcated tubes that mimic natural blood-vessel branches, expanding indications for textile-based endovascular grafts. Hybrid constructions that laminate a melt-blown antimicrobial core between warp-knit covers converge benefits of both worlds, a trend that helps sustain broad-based growth in the biomedical textile market.

The Biomedical Textile Market Report is Segmented by Fiber Type (Non-Biodegradable Fibers, Biodegradable Fibers), Fabric Form (Non-Woven, Woven, Other Fabric Types), Application (Non-Implantable, Implantable, Other Implantable), End-User (Hospitals & Surgical Centers, Ambulatory Care Centers, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands 38.09% 2024 revenue, driven by broad insurance coverage and rapid translation of federally funded textile research into commercial supply chains. The Department of Defense's USD 75 million smart-fabric program delivered sensor yarns now appearing in civilian negative-pressure wound dressings. FDA biocompatibility guidance released in 2025 streamlines approvals, letting local firms secure early-mover contracts. Capital investment from device majors such as Smith & Nephew anchors regional manufacturing clusters in Massachusetts and Minnesota.

Asia-Pacific posts a 7.42% CAGR to 2030 as governments expand universal health insurance and stimulate domestic medtech output. China aggressively scales nanofiber lines to meet both export orders and home demand, while Japan funds geriatric remote-care pilots that rely on sensor-integrated gauze. Regulatory harmonization through ASEAN Medical Device Directives gradually lowers entry barriers, supporting multinational and regional vendors alike.

Europe blends advanced regulation with sustainability imperatives. The EU Single-Use Plastics Directive bans certain fossil-based disposables, prompting hospitals to trial Lenzing's cellulosic stent covers and bio-based nonwoven pads. Freudenberg leverages the Heytex acquisition to supply polyurethane-coated substrates for negative-pressure therapy devices. Nonetheless, waste-reduction rules raise compliance costs; suppliers succeed by certifying compostability and closed-loop recycling audits.

South America and the Middle East & Africa trail on value but show accelerating unit growth as tertiary hospitals open and governments subsidize trauma networks. Cost-optimized spun-bond wound pads made from locally recycled PET balance price sensitives with adequate barrier function. International NGOs aid procurement training, helping clinicians choose evidence-backed textile solutions and broadening the biomedical textile market footprint.

- Ahlstrom

- ATEX TECHNOLOGIES INC.

- B. Braun SE

- Bally Ribbon Mills

- Cardinal Health

- CORTLAND BIOMEDICAL

- dsm-firmenich

- Freudenberg Performance Materials

- Lenzing AG

- Medline Industries LP

- Meister & Cie AG

- Milliken & Company

- Secant Group, LLC

- Smith+Nephew

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising number of surgeries

- 4.2.2 Growing need for high-quality wound-care textiles

- 4.2.3 Rapid ageing population in key economies

- 4.2.4 Advances in minimally-invasive implantable textiles

- 4.2.5 Bioresorbable electro-spun nanofiber dressings entering retail channels

- 4.2.6 Defense-funded sensor fabrics accelerating med-smart textile crossover

- 4.3 Market Restraints

- 4.3.1 High cost of vascular grafts and artificial skin

- 4.3.2 Electronic-textile integration complexity

- 4.3.3 Absent shelf-life standards for antimicrobial biotextiles

- 4.3.4 Regulatory backlash on single-use medical nonwovens waste

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fiber Type

- 5.1.1 Non-biodegradable Fibers

- 5.1.2 Biodegradable Fibers

- 5.2 By Fabric Form

- 5.2.1 Non-woven

- 5.2.2 Woven

- 5.2.3 Other Fabric Types (Knitted, Braided)

- 5.3 By Application

- 5.3.1 Non-implantable

- 5.3.2 Implantable

- 5.3.3 Other Implantable (Extracorporeal, etc.)

- 5.4 By End-user

- 5.4.1 Hospitals and Surgical Centers

- 5.4.2 Ambulatory Care Centers

- 5.4.3 Home Healthcare

- 5.4.4 Sports Medicine and Orthopedic Clinics

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ahlstrom

- 6.4.2 ATEX TECHNOLOGIES INC.

- 6.4.3 B. Braun SE

- 6.4.4 Bally Ribbon Mills

- 6.4.5 Cardinal Health

- 6.4.6 CORTLAND BIOMEDICAL

- 6.4.7 dsm-firmenich

- 6.4.8 Freudenberg Performance Materials

- 6.4.9 Lenzing AG

- 6.4.10 Medline Industries LP

- 6.4.11 Meister & Cie AG

- 6.4.12 Milliken & Company

- 6.4.13 Secant Group, LLC

- 6.4.14 Smith+Nephew

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment