|

시장보고서

상품코드

1846346

스코폴라민(Scopolamine) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Scopolamine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

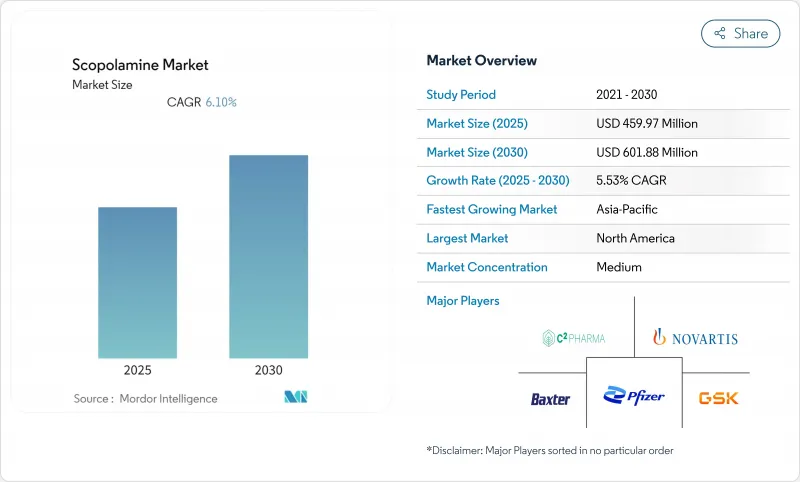

세계의 스코폴라민 시장 규모는 2025년에 4,599억 7,000만 달러로 추정되고, 2030년에는 6,018억 8,000만 달러에 이를 전망이며, CAGR 5.53%로 성장할 것으로 예측됩니다.

성장은 여행 회복, 선택적 수술 증가, 경피 투여에서 기술 업그레이드의 수렴을 반영합니다. 의료 제공자는 지속적인 제토약으로서 경피흡수형 패치를 계속 유력시하고 있지만, 신속한 효능이 필요한 경우에는 주사제가 발판을 굳게 하고 있습니다. 호주에서는 듀보이시아 속의 관목이 상업 규모로 재배되고 있으며, 신뢰성이 높은 원약 공급이 확보되고 있지만, 기후와 관련된 작물 리스크에 의해 제조업체는 환경 제어형 농업을 지향하고 있습니다. 경쟁의 심각성은 중간이지만, 이는 원료의 추출과 패치의 조립에 엄격하게 규제된 제조 능력이 필요하기 때문에 신규 진입을 막고 있습니다.

세계의 스코폴라민 시장 동향 및 인사이트

여행자의 멀미 유행

레저나 비즈니스로의 이동이 급증하며, 약리학적 대책에 대한 수요가 높아집니다. 크루즈 이용자 수, 민간 항공기 탑승률, 도시 간 철도 이용자 수는 모두 팬데믹 이전 수준으로 회복되었으며, 이에 따라 전정 증상에 대한 불만이 끊이지 않습니다. 여행 빈도가 높고 eVTOL 에어 택시와 같은 새로운 유형의 차량을 채용하는 젊은 층은 메스꺼움을 유발하는 감각적 갈등에 대한 민감성이 높다고 보고했습니다. 운송업체는 출발 전 건강 권고에서 스코폴라민 패치를 권장하고 있으며, 승객층 전체에서 브랜드에 대한 친근감을 강화하고 있습니다. 스코폴라민 패치는 3일 동안 안정적인 혈장 농도를 유지하기 때문에 전형적인 주말 여행 및 단거리 항해 기간과 일치하여 복약 준수 및 반복 구매 행동을 촉진합니다.

수술 건수 증가 및 PONV 예방약 수요

세계 병원은 수술을 입원 수술실에서 외래 센터로 계속 전환하고 있으며 당일치기 수술 건수는 사상 최고를 갱신하고 있습니다. PONV는 수술 환자의 35.4%, 고위험군의 최대 80%가 앓고, 관리하지 않으면 고액의 재입원으로 이어집니다. 경피 흡수형 스코폴라민은 72시간의 예방 효과를 가지고 있으며, 복용량을 조정하지 않고 조기 및 후기 구토 창을 커버합니다. 비교 연구는 수술 후 구토의 상대 위험이 위약에 비해 37% 감소하고 온단세트론 요법보다 비용면에서 우수함을 보여줍니다. 지불자가 환자 보고 결과 및 상환을 연결함에 따라, 시설은 점차 회복 촉진 프로토콜에 패치를 통합하게 되어, 주술기 약국 전체의 안정된 주문 패턴을 자극하고 있습니다.

항콜린성 부작용의 안전성에 관한 경고

FDA는 2025년 6월 열 관련 합병증을 보고한 후 Transderm Scop의 표시를 업데이트하여 체온 조절 위험에 대한 보다 긴밀한 환자 모니터링 및 교육을 의무화했습니다. 레트로 스펙티브 코호트 분석은 수술 기간 동안 스코폴라민과 노인의 섬망 및 요폐 증가를 연관시켰습니다. 병원은 위험 경감을 위한 추가 데이터가 나올 때까지 노인 코호트의 패치량을 억제할 수 있기 때문에 통합 기준을 엄격하게 함으로써 대응하고 있습니다.

부문 분석

2024년 스코폴라민 시장 점유율의 49.50%는 경피 흡수형 패치이며, 며칠간의 여행이나 수술 후 회복 시 컴플라이언스를 확보할 수 있는 72시간 전달에 대한 임상의의 강한 기호를 반영하고 있습니다. 이 부문의 CAGR은 6.24%로 정제와 주사제보다 높습니다. 이는 병원이 외래 수술의 처리 능력을 확대하고 장기간의 예방 투여가 콜백을 줄이는 환경이기 때문입니다. 2024년 제네릭 의약품 출시로 단가가 인하되고 가격에 민감한 구매자의 가격 감이 개선되며 고객 기반이 확대됩니다. 정제는 피부 반응으로 인해 접착제를 사용할 수 없을 때 틈새 수요에 부응하고 있지만, 위장에 대한 부작용과 흡수의 변동이 처방자의 신뢰를 제한하기 때문에 점유율은 하강하는 경향이 있습니다. 주사제는 즉각적인 효능이 지속시간보다 중시되는 구급 부문에서 중요성을 유지하며, 스코폴라민 시장의 성장률이 낮은 반면, 안정된 지위를 구축하고 있습니다.

2세대 패치 디자인은 땀을 흘린 피부에서도 점착성을 유지하는 바이오폴리머 점착제를 채용하고 있어, 고성장을 이루고 있는 여행 루트인 습도가 높은 열대 기후에는 필수적입니다. 제조업체는 또한 약동학 시험에서 피크와 스루의 편차를 20% 줄이기 위해 플럭스를 균등화하는 마이크로 저장소 형태를 통합하고 있습니다. 이러한 개선은 경피 흡수형 제제의 가치 제안을 강화하고 스코폴라민 시장에서의 리더십을 강화합니다.

지역 분석

북미는 2024년 매출의 37.32%를 차지하며 선두를 유지했습니다. 이것은 선택적 수술 건수와 성숙한 크루즈 및 항공 부문에 밀려 있습니다. 2024년 FDA가 제네릭 의약품을 신속하게 승인함으로써 가격에 대한 민감도가 높아지면서 액세스는 확대되었습니다. 동시에 이 지역의 상업 우주 부문은 지상에서의 효능을 창출할 수 있는 약리학적 연구에 자금을 제공하고 있으며, 허약한 집단들 사이에서 안전성 권고가 성장을 억제하더라도 장기적인 수요를 뒷받침하고 있습니다.

유럽에서는 멀미 및 PONV 예방을 위한 보험 상환이 유럽 전역에서 실시되어 꾸준히 확대되고 있습니다. 규제 기준의 조화와 페리, 철도, 크루즈의 호조로운 운송이 폭넓은 소비자층을 유지하고 있습니다. 독일, 프랑스, 영국에서는 디지털 약국의 보급으로 액세스가 가속화되고 있으며, eID 처방전 흐름에 의해 패치의 리필이 간소화되고 있습니다. 단거리 비행보다 철도를 장려하는 기후 정책은 부주의하게 여행 시간을 연장하고, 멀미의 에피소드를 증가시키며, 의약품 수요를 강화할 수 있습니다.

아시아태평양은 CAGR 7.19%로 가장 빠른 성장을 보이고 있습니다. 중산계급 관광 확대, 국내 항공 여객 수 급증, 수입 제네릭 의약품에 대한 규제 개방이 함께 의약품 수요가 크게 증가하고 있습니다. 중국의 의약품등록제도 개혁 및 인도의 항공 사업 확대로 대응 가능한 여행자수는 10년 이내에 두배가 될 전망입니다. 패치 제조업체는 지역 유통업체와 제휴하여 리드 타임을 단축하고 호주 원료 수출업체는 가뭄 위험을 줄이기 위해 환경 제어 듀보이시아를 증산합니다. 아시아태평양에서는 전자 약국 솔루션의 조기 도입으로 공급망의 합리화가 진행되고 아시아태평양이 스코폴라민 시장의 주요 증수 엔진으로 자리매김하고 있습니다.

남미와 중동, 아프리카의 공헌은 작지만 점유율은 상승하고 있습니다. 사우디아라비아에서는 정부에 의한 현지화가 추진되고, 이집트에서는 의약품 부문의 개혁이 진행되고 있습니다. 또한 인도주의 기관은 사막에서 수송하는 동안 더위가 탈취를 악화시키기 위해 건강 키트에 패치를 넣습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 여행자의 멀미 유행

- 수술 건수 증가 및 PONV 예방 수요 증가

- 경피 투여 기술의 진보

- 상업 우주 비행 대책의 연구 개발

- VR 및 방위 시뮬레이터에 의한 메스꺼움 수요

- 듀보이시아의 수경 재배에 의한 원약 비용 저하

- 시장 성장 억제요인

- 항콜린 작용에 의한 부작용의 안전성 경고

- 특허 만료 및 가격 하락

- 기후에 따른 듀보이시아 공급 변동

- 대체제토약(NK-1 길항제)의 보급

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제형별

- 주사제

- 태블릿

- 경피 패치

- 기타

- 용도별

- 멀미

- 수술 후 메스꺼움 및 구토(PONV)

- 파킨슨병 및 소화기질환

- 기타

- 유통 채널별(금액 : 백만 달러)

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Baxter International Inc.

- GlaxoSmithKline plc

- Teva Pharmaceutical Industries Ltd.

- Mylan Pharmaceuticals Inc.

- Zydus Lifesciences Ltd.

- Padagis Israel Pharmaceuticals Ltd.

- Ingenus Pharmaceuticals LLC

- Boehringer Ingelheim International GmbH

- Rhodes Pharmaceuticals LP

- RiconPharma LLC

- Alchem International Pvt Ltd.

- Alkaloids Corporation

- Aspen Pharmacare Holdings Ltd.

- Alps Pharmaceutical Industries Co., Ltd.

- DKSH Holding Ltd.

- Phytex Australia Pty Ltd.

제7장 시장 기회 및 전망

AJY 25.11.10The global scopolamine market size stands at USD 459.97 billion in 2025 and is projected to reach USD 601.88 billion by 2030, advancing at a 5.53% CAGR.

Growth reflects a convergence of travel recovery, rising elective surgery volumes and technology upgrades in transdermal delivery. Healthcare providers continue to view transdermal patches as the workhorse for sustained antiemetic coverage, while injectable products retain a foothold where rapid onset is essential. Commercial-scale cultivation of Duboisia shrubs in Australia ensures reliable active-ingredient supply, yet climate-related crop risks push manufacturers toward controlled-environment agriculture. Competitive intensity is moderate because API extraction and patch assembly require tightly regulated manufacturing capabilities that deter new entrants.

Global Scopolamine Market Trends and Insights

Prevalence of Motion Sickness among Travellers

Sharp rebounds in leisure and business mobility lift demand for pharmacological countermeasures. Cruise traffic, civil aviation load factors and inter-city rail ridership have all returned to pre-pandemic ranges, bringing with them a steady stream of vestibular complaints. Younger cohorts, who travel more frequently and adopt emerging vehicle types such as eVTOL air taxis, report higher susceptibility to sensory conflicts that induce nausea. Transport operators increasingly recommend scopolamine patches in pre-departure health advisories, reinforcing brand familiarity across passenger segments. Because the patch delivers consistent plasma levels over three days, it matches the duration of typical weekend trips and short-haul voyages, enhancing adherence and repeat purchase behaviour.

Rising Surgical Volumes & Demand for PONV Prophylaxis

Hospitals worldwide continue to shift procedures out of inpatient theatres and into ambulatory centres, driving day-surgery numbers to new highs. PONV affects 35.4% of surgical patients and up to 80% of high-risk groups, translating to costly readmissions if unmanaged. Transdermal scopolamine offers 72-hour prophylaxis, covering both early and late emetic windows without dosing adjustments. Comparative studies show a 37% relative risk reduction in postoperative vomiting versus placebo and cost superiority over ondansetron regimens. As payers link reimbursement to patient-reported outcomes, facilities increasingly embed the patch into enhanced-recovery protocols, stimulating steady ordering patterns across perioperative pharmacies.

Anticholinergic Adverse-Effect Safety Warnings

The FDA updated Transderm Scop labelling in June 2025 after reports of heat-related complications, mandating closer patient monitoring and education on thermoregulation risks. Retrospective cohort analysis linked perioperative scopolamine to increased delirium and urinary retention in older adults. Hospitals respond by tightening inclusion criteria, potentially curbing patch volumes in geriatric cohorts until additional risk-mitigation data emerge.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Transdermal Delivery Technologies

- Commercial Space-Flight Counter-Measure R&D

- Uptake of Alternative Antiemetics (NK-1 Antagonists)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transdermal patches hold 49.50% of the scopolamine market share in 2024, reflecting strong clinician preference for 72-hour delivery that secures compliance during multi-day travel and postoperative recovery. The segment's 6.24% CAGR outpaces tablets and injectables as hospitals expand ambulatory surgery throughput, a setting where extended prophylaxis reduces callbacks. Generic launches in 2024 compressed unit costs, improving affordability for price-sensitive buyers and broadening the customer base. Tablets continue to meet niche demand when dermal reactions preclude patch use, yet their share edges downward as gastrointestinal side effects and variable absorption limit prescriber confidence. Injectables retain relevance in emergency departments where immediate onset overrides duration considerations, anchoring a stable though slower-growth slice of the scopolamine market.

Second-generation patch designs employ bio-polymer adhesives that maintain adherence on perspiring skin, crucial for humid tropical climates that dominate high-growth travel corridors. Manufacturers also integrate micro-reservoir geometries that equalise flux, cutting peak-trough variance by 20% in pharmacokinetic studies. These refinements strengthen the transdermal segment's value proposition and reinforce its leadership across the scopolamine market.

The Scopolamine Market Report is Segmented by Dosage Form (Injectables, Tablets, Transdermal Patches, Others), Application (Motion Sickness, Post-Operative Nausea & Vomiting, Parkinsonian & GI Disorders, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains leadership with 37.32% of 2024 sales, buoyed by high elective surgery throughput and mature cruise and aviation sectors. The FDA's swift generic approvals in 2024 broadened access while sharpening price sensitivity, yet entrenched clinical protocols continued to endorse prophylactic patch use following cost-benefit reviews. Concurrently, the region's commercial space sector funds pharmacological research that could spin off terrestrial indications, underpinning long-term demand even as safety advisories temper growth among frail cohorts.

Europe posts steady expansion supported by continent-wide reimbursement for motion-sickness and PONV prophylaxis. Harmonised regulatory standards and strong ferry, rail and cruise traffic sustain a broad consumer base. Digital pharmacy uptake accelerates access in Germany, France and the UK, where eID prescription flows simplify patch refills. Climate policies encouraging rail over short-haul flights inadvertently extend travel times, potentially increasing motion sickness episodes and reinforcing pharmaceutical demand.

Asia-Pacific shows the fastest trajectory at 7.19% CAGR. Expanding middle-class tourism, rapid domestic air-passenger multiplication and regulatory opening for imported generics combine to drive outsized volumes. China's drug-registration reforms and India's aviation expansion double the addressable traveller pool within the decade. Patch manufacturers partner with regional distributors to shorten lead times, while Australian API exporters ramp controlled-environment Duboisia to mitigate drought risk. The region's early adoption of e-pharmacy solutions further streamlines supply chains, positioning Asia-Pacific as the primary incremental revenue engine for the scopolamine market.

South America and the Middle East & Africa contribute smaller but rising shares. Currency swings and uneven reimbursement temper uptake, yet government localisation drives in Saudi Arabia and pharmaceutical-sector reforms in Egypt unlock medium-term opportunity. Humanitarian aid agencies also include patches in health kits for desert deployments where heat exacerbates motion sickness during road convoys.

- Baxter

- GlaxoSmithKline

- Teva Pharmaceutical Industries

- Mylan

- Zydus Lifesciences Ltd.

- Padagis Israel Pharmaceuticals Ltd.

- Ingenus Pharmaceuticals LLC

- Boehringer Ingelheim

- Rhodes Pharmaceuticals L.P.

- RiconPharma LLC

- Alchem International Pvt Ltd.

- Alkaloids Corporation

- Aspen Pharmacare Holdings Ltd.

- Alps Pharmaceutical Industries Co., Ltd.

- DKSH Holding Ltd.

- Phytex Australia Pty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prevalence of motion sickness among global travellers

- 4.2.2 Rising surgical volumes & demand for PONV prophylaxis

- 4.2.3 Advancements in transdermal delivery technologies

- 4.2.4 Commercial space-flight counter-measure R&D

- 4.2.5 VR & defence-simulator-induced nausea demand

- 4.2.6 Hydroponic Duboisia cultivation lowering API costs

- 4.3 Market Restraints

- 4.3.1 Anticholinergic adverse-effect safety warnings

- 4.3.2 Patent expiries & price erosion

- 4.3.3 Climate-driven Duboisia supply volatility

- 4.3.4 Uptake of alternative antiemetics (NK-1 antagonists)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Dosage Form (Value, USD million)

- 5.1.1 Injectables

- 5.1.2 Tablets

- 5.1.3 Transdermal Patches

- 5.1.4 Others

- 5.2 By Application (Value, USD million)

- 5.2.1 Motion Sickness

- 5.2.2 Post-operative Nausea & Vomiting (PONV)

- 5.2.3 Parkinsonian & GI Disorders

- 5.2.4 Others

- 5.3 By Distribution Channel (Value, USD million)

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography (Value, USD million)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Baxter International Inc.

- 6.3.2 GlaxoSmithKline plc

- 6.3.3 Teva Pharmaceutical Industries Ltd.

- 6.3.4 Mylan Pharmaceuticals Inc.

- 6.3.5 Zydus Lifesciences Ltd.

- 6.3.6 Padagis Israel Pharmaceuticals Ltd.

- 6.3.7 Ingenus Pharmaceuticals LLC

- 6.3.8 Boehringer Ingelheim International GmbH

- 6.3.9 Rhodes Pharmaceuticals L.P.

- 6.3.10 RiconPharma LLC

- 6.3.11 Alchem International Pvt Ltd.

- 6.3.12 Alkaloids Corporation

- 6.3.13 Aspen Pharmacare Holdings Ltd.

- 6.3.14 Alps Pharmaceutical Industries Co., Ltd.

- 6.3.15 DKSH Holding Ltd.

- 6.3.16 Phytex Australia Pty Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment