|

시장보고서

상품코드

1846349

흉골 폐쇄 시스템 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Sternal Closure Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

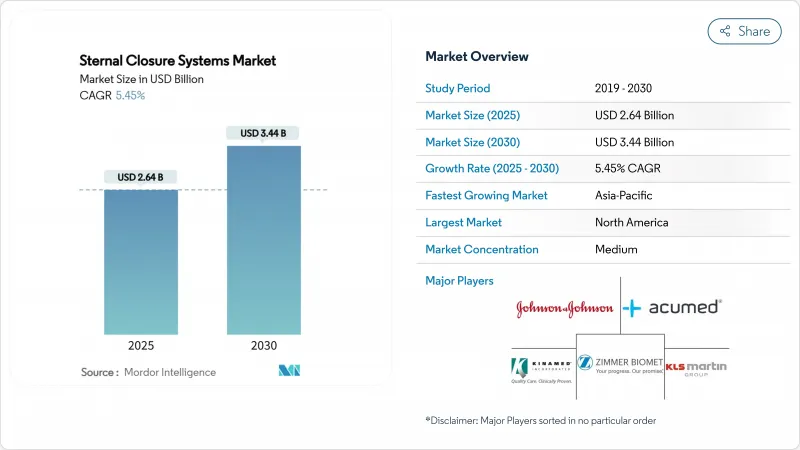

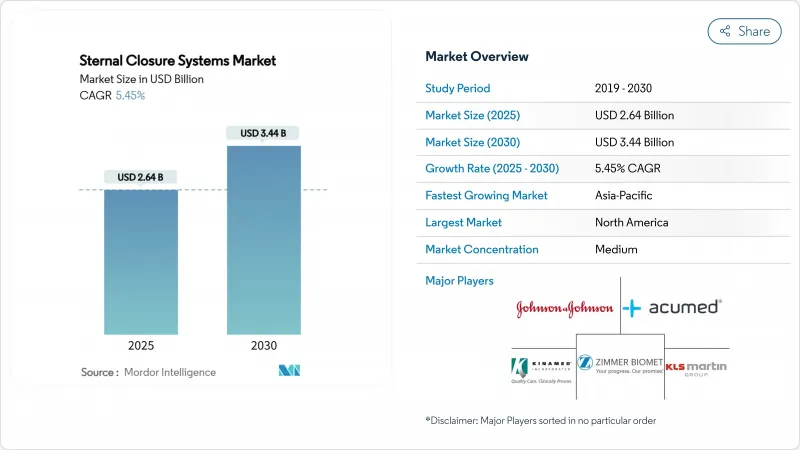

흉골 폐쇄 시스템 시장 규모는 2025년에 26억 4,000만 달러로 추정되고, 2030년에는 34억 4,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 5.45%로 성장할 전망입니다.

개발은 세계의 심장 수술 건수의 꾸준한 리듬을 반영하고 있으며, 선진 경제 국가는 대체 수요를 향해, 신흥 경제 국가는 새로운 수술 능력을 추가하고 있습니다. 레거시 와이어에서 경질 플레이트 및 스크류 구조로 눈에 보이는 시프트가 이 확장을 지원합니다. 80대 환자가 보다 복잡한 수술을 받고 흉골 안정성 요건이 높아짐에 따라 인구통계학적 압력이 더욱 기세를 늘리고 있습니다. 규제 당국, 특히 FDA는 품질 시스템 규칙을 지속적으로 강화하고, 충분한 증거를 가진 의료기기를 우대하며, 증거가 적은 의료기기의 진입을 늦추고 있습니다. 비용 억제는 여전히 중심이지만, 일괄 지불 모델은 합병증의 감소에 의해 에피소드 오브 케어 비용을 삭감하는 기술에 결정을 기울이고 있습니다.

세계 흉골 폐쇄 시스템 시장 동향 및 인사이트

개심술 증가 및 인구 동태 고령화

현재 세계의 심장병 치료실에서는 80세 이상의 환자를 많이 치료하고 있으며, 그 수술 증례 수는 2024년 이후 24배로 증가하고 있습니다. 평균 수명이 길어지고, 마취 프로토콜이 진보되며, 수술기 지원이 충실해짐에 따라, 외과의사는 보다 위험이 높은 복잡한 사례도 받아들일 수 있게 되었습니다. 고령자의 흉부는 골질이 부서지며 골화가 느리기 때문에 기존의 스테인레스 스틸 와이어에서는 충분히 완화할 수 없는 흉골 불안정성의 위험성이 높아지고 있습니다. 박리와 관련된 재입원 페널티는 비싼 기구 비용을 초과하는 경우가 많기 때문에 병원은 이 층에 경성 고정 키트를 할당하는 경우가 많습니다. 금액 기준으로 상처 합병증이 1회 회피될 때마다 90일간의 에피소드 전체에서 최대 4만 5,000달러가 절약되기 때문에 플레이트 시스템은 공적 자금으로 운영되고 있는 의료 기관에 대해서도 경제적으로 합리적입니다. 그러므로 이 인구역학 촉진요인은 구조적이며 흉골 폐쇄 시스템 시장에서 고급 시스템에 대한 장기적인 수요를 지원합니다.

복잡하고 치유되지 않는 흉골 절개의 발생률 증가

흉골 심부의 창 감염률은 0.5%에서 5%로 폭이 있지만, 박리가 일어나면 사망률은 25%를 초과합니다. 당뇨병, 비만, 면역 억제는 골절 가장자리의 혈관 신생을 악화시키고 호흡시 미세 운동을 허용하는 전선 만의 구조를 약화시킵니다. 단단한 플레이트는 6-8 주간의 치유 기간 동안 캘러스 형성을 촉진하기 위해 접촉을 유지하면서 두 피질 표를 따라 하중을 분산시킵니다. 병원은 현재 수술 전 HbA1c, BMI, 면역 상태를 기반으로 환자를 계층화하고 높은 위험의 5분위에 티타늄 플레이트를 보유하고 있습니다. 미국의 한 다시설 공동연구에서는 프로토콜 변경 후 심흉골창의 합병증이 43% 감소하고 평균 재원일수가 2.6일 단축된 것을 기록하고 있습니다. 상처 프로파일의 복잡성으로 인해 많은 지침에서 경성 고정이 옵션에서 권장되고 흉골 폐쇄 시스템 시장의 확대를 지원합니다.

높은 BMI 및 당뇨병 환자 집단에서 감염 및 박리 위험

비만 환자 및 당뇨병 환자는 필요와 위험의 역설을 나타냅니다. 연부 조직의 부피와 미세 순환 장애는 감염 감수성을 증가시키고 모든 이물질이 염증 캐스케이드를 악화시킵니다. 티타늄 표면조차도 때때로 나노 스케일 입자를 배출하고 장기적인 생체 반응성에 대한 우려를 부추깁니다. 따라서 임상의는 이러한 코호트의 안전성이 입증될 때까지 새로운 구조물의 승인을 망설이고 있습니다. 2024년 폴란드의 코호트 연구는 당뇨병의 임플란트 수령인에서 금속 이온 부하의 상승을 지적하고, 감시 프로토콜의 연장이 요구되고 있습니다. 의료 과오 소송을 두려워하여 보수적인 자세가 조장되어 흉골 폐쇄 시스템 시장에서의 신기술의 보급을 늦추고 있습니다.

부문 분석

2024년 흉골 폐쇄 시스템 시장 점유율의 45.51%를 기존의 스테인레스 스틸 와이어가 차지했습니다. 저위험의 관상동맥 우회 사례로 외과 의사가 익숙한 저렴한 절차를 선호하기 때문에 단위 수량의 이점이 계속되고 있습니다. 한편, 플레이트와 스크류는 CAGR 9.65%로 호조로 전단하중이 큰 노인 밸브 치환술이나 흉골절개의 재개술로 점유율을 획득했습니다. 전통적인 시멘트와 접착제 라인은 주로 골 결손과 관련된 복잡한 재건술을 위해 여전히 틈새 시장입니다. 폴리유산과 강화 PEEK 섬유로 만들어진 생체 흡수성 플레이트는 소아 수복에 매력적이지만, 미립자에 의한 조사를 위해 성인 흡수의 벽에 직면하고 있습니다. 경제 모델링에 따르면 경성 플레이트는 감염 발생률이 0.4% 떨어진 시점에서 비용 중립이 됩니다. 장비 제조업체는 외과의사의 워크숍과 수내 하중 계산기에서 전환을 지원하여 브랜드의 영향이 아니라 증거 기반 선택을 가능하게 합니다. 예측 기간 동안, 플레이트는 유닛 믹스의 35%에 도달할 것으로 예측되며, 와이어는 후퇴하는 반면, 저예산 시설에는 필수적이며, 흉골 폐쇄 시스템 시장에서 여러 기술이 공존하게 됩니다.

존슨 엔드 존슨의 MatrixSTERNUM과 같은 고급 플레이트 시스템은 최소한의 굽힘 조정으로 스팬, 스크류 벡터 및 하중 분담을 사용자 정의할 수 있는 모듈식 디자인을 도입하여 수술 중 추측을 줄입니다. 이러한 엔지니어링 유연성은 단일 트레이에서 체격 지수의 극단적인 차이를 다룰 수 있으므로 병원 재고 선호도와 일치합니다. 한편, 미니 스크류 기술은 프로파일의 높이를 잘라내어 연부 조직의 폐쇄를 용이하게 하고, 수술 후의 불쾌감을 줄여줍니다. 이러한 개선을 총칭하여 경성 고정은 일상 진료에 깊이 침투하며 프리미엄 ASP가 상승합니다. 와이어가 사라지지는 않지만 흉골 폐쇄 시스템 시장의 플레이트 중심 성장에 비해 상대적인 수익에 미치는 영향은 줄어들 것으로 보입니다.

흉골정중절개술은 계속 주력술식이며 2024년 흉골폐쇄시스템 시장 규모의 78.53%를 차지했습니다. 심장에 대한 완전한 노출은 다지 바이 패스와 복잡한 밸브 재건에 필수적입니다. 흉골 전체를 폐쇄하기 위해서는 호흡기의 비틀림에 대항할 수 있는 견고한 고정이 필요했고, 지금까지는 전체 길이의 와이어에 의한 셀 클러지가 주류였습니다. 양측 흉골절개술은 하이브리드 밸브 플러스 CABG의 프로토콜과 로봇에 의한 채취 기술이 측방으로부터의 접근을 선호하기 때문에 CAGR 9.85%를 올려 고성장 포켓을 형성했습니다. 양측 개흉술을 채용하는 외과의사는 내흉 페디클을 피하기 위해 오프셋 스크류 모양의 짧은 플레이트를 필요로 틈새 제품 라인에 박차를 가하고 있습니다.

격리된 대동맥 판막 치환술에 자주 사용되는 반 흉골 절개술은 노출과 조직 온존의 균형을 이루며 고정 복잡성에서 중간 위치를 제공합니다. 따라서 와이어나 스크류에 대응할 수 있어 해부학적 구조에 맞춘 폐쇄가 가능한 고정 스트립에 대한 수요가 높아지고 있습니다. 규제 기관은 현재 절차에 특화된 벤치 테스트를 요구하고 있습니다. 플레이트 벤더는 비대칭 호흡 사이클 하에서의 하중 분산을 증명하는 유한 요소 모델로 대응합니다. 접근 제한이 있는 수술로 전환함에 따라 절단 길이를 바꾸어도 부문의 안정성을 보장할 수 있는 다목적 폐쇄 키트가 가격 결정력을 갖게 되어 흉골 폐쇄 시스템 시장의 프리미엄층 성장이 강화될 것입니다.

지역 분석

북미는 심장 외과 인프라가 충실하고 경성 고정술의 상환 경로를 일찍부터 채용하고 있기 때문에 2024년 매출의 42.32%를 획득했습니다. 미국 병원은 이미 30일 Hospital Value-Based Purchasing에 따라 추적되는 재입원 지표에 폐쇄술의 선택을 통합했으며, 이는 캐나다와 멕시코의 기술적 기조가 되었습니다. FDA 모니터링은 문서화 장애물을 높이고 있지만 승인이 얻어지면 장기적으로 안정될 것임을 시사합니다. 폭발적인 성장보다 꾸준한 성장이 이어져, 수술의 확대보다 교체 수요나 기술의 갱신 사이클에 연결되고 있습니다.

유럽은 집중 구매 및 증거 주도의 장비 평가에 지원되는 균형 잡힌 성장을 이루고 있습니다. 의료기기 규제는 지속적인 시판 후 감시를 의무화하고 있으며, 제조업체는 실제 임상 등록에서 유용성을 입증하는 임상 데이터베이스를 유지하도록 촉구하고 있습니다. 독일과 영국은 학술 네트워크가 신속하게 결과 데이터를 발표하고 대륙 전체의 임상의의 감정을 흔들고 있기 때문에 플레이트 채용을 이끌고 있습니다. 남유럽과 동유럽은 비용 최적화된 티타늄 키트에 중점을 두고 MDR을 충족시키면서도 다국적 기업의 가격보다 낮은 지역의 제조업자로부터 수입하고 있습니다. 외환변화와 의료 예산 협상은 단위 흐름에 영향을 미치지 만 노화 사회는 흉골 폐쇄 시스템 시장의 유럽 슬라이스에서 수요의 회복력을 약속합니다.

아시아태평양의 CAGR은 가장 빠른 11.61% 중국의 관민병원 현대화 프로그램은 개심술의 용량을 전년 대비 14% 증가시켰고, 인도의 사립 3차 병원 체인은 의료 투어리즘을 유치하는 고도급성 심장병 플로어에 투자하고 있습니다. 일본은 엄격한 의료기기 승인제도(Shonin)를 유지해 시장 투입까지의 시간을 연장하고 있지만, 한 번 취득한 내구성이 있는 안전성 기록에는 보답하고 있습니다. 저소득 ASEAN 국가들은 하이브리드 조달을 선호하며, 종종 국가 병원에 티타늄 플레이트를 장비하는 반면 지역 센터는 여전히 와이어에 의존하고 있습니다. 흉터를 최소화하는 것을 중시하는 문화가, 저침습 수술의 보급에 박차를 가해, 간접적으로 플레이트의 채용을 뒷받침하고 있습니다. 이 지역에서 성공을 거두고 있는 벤더는 Tier1 도시용으로는 수입 티타늄을, 가격에 민감한 지향적으로는 현지에서 조립한 스테인리스의 2개의 포트폴리오를 전개해, 흉골 폐쇄 시스템 시장에서 폭을 넓히고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 개심술 증가 및 고령화

- 치유되지 않는 복잡한 흉골절개창의 발생률 상승

- 경질 플레이트 및 스크류 고정 시스템의 급속한 보급

- 저재진률 디바이스를 지지하는 병원 일괄 지불 프로그램

- 생체 흡수성 폴리머 및 PEEK제 흉골 임플란트의 출현

- AI에 의한 수술 중 영상 진단에 의한 폐쇄 정밀도 향상

- 시장 성장 억제요인

- 고BMI 및 당뇨병 코호트에 있어서 감염 및 박리의 위험

- 기존의 와이어와 비교하여 높은 디바이스 및 수술실의 시간 비용

- 경성 고정 시스템의 훈련을 받은 외과의의 부족

- 임플란트 미립자(마이크로플라스틱)에 대한 규제 강화

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 와이어

- 플레이트 및 스크류

- 뼈 시멘트 및 접착제

- 생체 흡수성 시스템

- 기타

- 수기별

- 중앙부 흉골절개술

- 혈측 흉골절개술

- 양측 흉골절개술

- 재료별

- 스테인레스 스틸

- 티타늄

- 폴리에테르에테르케톤(PEEK)

- 복합재료 및 생체 흡수성 폴리머

- 최종 사용자별

- 3차 의료 병원

- 심장 및 흉부 전문 클리닉

- 외래수술센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson(DePuy Synthes & Ethicon)

- Zimmer Biomet Holdings

- Stryker Corporation

- KLS Martin Group

- B Braun SE

- Acumed LLC

- Medtronic plc

- Orthofix Holdings Inc

- Abyrx Inc

- Kinamed Inc

- Jace Medical

- Praesidia SRL

- IDEAR SRL

- RTI Surgical

- Arthrex Inc

- Jeil Medical Corp

- Neos Surgery SL

- MedXpert GmbH

제7장 시장 기회 및 전망

AJY 25.11.10The sternal closure systems market size reached USD 2.64 billion in 2025 and is forecast to touch USD 3.44 billion by 2030, advancing at a 5.45% CAGR during the period.

Growth reflects the steady rhythm of global cardiac surgery volumes, with developed regions moving toward replacement demand and emerging economies adding new procedure capacity. A visible shift from legacy wires to rigid plate-and-screw constructs anchors this expansion because hospitals now link closure performance to lower readmission penalties under value-based reimbursement. Demographic pressure adds momentum as octogenarian patients undergo more complex surgeries that raise sternal stability requirements. Regulatory agencies, especially the FDA, continue to tighten quality-system rules, favoring well-documented devices and slowing low-evidence entrants. Cost containment remains central, but bundled-payment models tilt decisions toward technologies that cut episode-of-care expenses through fewer complications.

Global Sternal Closure Systems Market Trends and Insights

Growing Volume of Open-Heart Procedures & Ageing Demographics

Cardiac units worldwide now treat a much larger cohort of patients aged 80 years and above, whose numbers within surgical case mix have multiplied twenty-fourfold since 2024. Longer life expectancy, advanced anesthesia protocols, and better peri-operative support enable surgeons to accept higher-risk, complex candidates. Elderly chests exhibit brittle bone quality and slower ossification, raising sternal instability hazards that conventional stainless-steel wires cannot fully mitigate. Hospitals increasingly allocate rigid fixation kits to this segment because readmission penalties tied to dehiscence often exceed the premium device cost. In value terms, every avoided wound complication saves up to USD 45,000 across the 90-day episode, making plate systems economically rational even for publicly funded institutions. The demographic driver is therefore structural and sustains long-horizon demand for advanced systems within the sternal closure systems market.

Rising Incidence of Complex, Non-Healing Sternotomy Wounds

Deep sternal wound infection rates vary from 0.5% to 5%, but mortality still climbs above 25% when dehiscence occurs. Diabetes, obesity, and immunosuppression foster poor vascularization at the osteotomy margin, undermining wire-only constructs that permit micro-motion during respiration. Rigid plates distribute load along both cortical tables, maintaining contact to encourage callus formation throughout the 6-to-8-week healing window. Hospitals now stratify patients based on pre-operative HbA1c, BMI, and immune status, reserving titanium plates for the upper-risk quintile. This selective deployment yields demonstrable quality gains: one US multi-center study recorded a 43% drop in deep sternal wound complications after protocol change, trimming average length of stay by 2.6 days. Rising complexity of wound profiles thus elevates rigid fixation from optional to recommended in many guidelines, sustaining expansion of the sternal closure systems market.

Infection & Dehiscence Risks in High-BMI/Diabetic Cohorts

Obese and diabetic patients represent the paradox of need versus risk. Their soft-tissue bulk and impaired microcirculation heighten infection susceptibility, and any foreign body can aggravate inflammatory cascades. Even titanium surfaces occasionally shed nano-scale particles, fueling concern about long-term bioreactivity. Clinicians therefore hesitate to approve novel constructs until safety in these cohorts is documented. A 2024 Polish cohort study flagged elevated metallic ion loads in diabetic implant recipients, prompting calls for extended surveillance protocols. Fear of malpractice litigation fosters a conservative stance and slows new-technology spread within the sternal closure systems market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Rigid Plate-and-Screw Fixation Systems

- Hospital Bundled-Payment Programs Favouring Low-Readmission Devices

- High Device & OR Time Costs vs. Conventional Wires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional stainless-steel wires controlled 45.51% of the sternal closure systems market share in 2024. Unit volume dominance persists because surgeons in low-risk coronary bypass cases prefer a familiar, inexpensive technique. Plates and screws, however, recorded a vigorous 9.65% CAGR, capturing share in geriatric valve replacements and redo sternotomies where shear loads are higher. Legacy cement and adhesive lines remain niche, primarily for complex reconstructions involving bone loss. Bio-absorbable plates, fabricated from polylactide and reinforced PEEK fibers, appeal in pediatric repairs but face adult uptake barriers due to particulate scrutiny. Economic modeling shows that rigid plates become cost-neutral when infection incidence drops by 0.4 percentage points; tertiary centers already exceed that threshold, explaining their early conversion. Device manufacturers support the transition with surgeon workshops and intramedullary load calculators, enabling evidence-based selection rather than brand influence. Over the forecast horizon, plates are projected to reach 35% unit mix, leaving wires to retreat yet remain essential for low-budget facilities, ensuring plural technology coexistence within the sternal closure systems market.

Advanced plate systems like Johnson & Johnson's MatrixSTERNUM introduced modular designs that help customize span, screw vector, and load sharing with minimal bend adjustments, reducing intra-operative guesswork. This engineering flexibility dovetails with hospital inventory preferences because a single tray can cover body mass index extremes. Meanwhile, mini-screw technology trims profile height, allowing easier soft-tissue closure and lowering postoperative discomfort. Collectively, these refinements push rigid fixation deeper into everyday practice and lift premium ASPs, which in turn uplifts total revenue even if overall case volumes plateau. Although wires will not vanish, their relative revenue impact will shrink compared with plate-centric growth inside the sternal closure systems market.

Median sternotomy continued as the workhorse, securing 78.53% of the sternal closure systems market size in 2024. Complete exposure to the heart is indispensable for multivessel bypasses and complex valve reconstructions. Closure across the entire sternum demands robust fixation that counters respiratory torsion, historically the domain of full-length wire cerclage. Bilateral thoracosternotomy created a high-growth pocket, adding a 9.85% CAGR because hybrid valve-plus-CABG protocols and robotic harvesting techniques favor lateral access. Surgeons adopting bilateral windows need shorter plates with offset screw geometry to avoid internal mammary pedicles, spurring niche product lines.

Hemi-sternotomy, often used for isolated aortic valve replacement, balances exposure and tissue preservation, providing a middle ground on fixation complexity. It fosters demand for contourable fixation strips that accept either wires or screws, letting teams tailor closure to anatomy. Regulatory bodies now require procedure-specific bench testing. Plate vendors respond with finite-element models that prove load dispersion under asymmetric breathing cycles. As the mix migrates toward limited-access surgery, versatile closure kits capable of segmental stability across variable cut lengths will command pricing power, reinforcing growth of premium tiers in the sternal closure systems market.

The Sternal Closure Systems Market Report is Segmented by Product (Wires, Plates and Screws, Bone Cement, and More), Procedure (Median Sternotomy, Hemi-Sternotomy, and Bilateral Thoracosternotomy), Material (Stainless Steel, Titanium, and More), End User (Tertiary Care Hospitals, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 42.32% of 2024 revenue due to extensive cardiac surgery infrastructure and early embrace of rigid fixation reimbursement pathways. Hospitals in the United States already integrate closure choices into 30-day readmission metrics tracked under Hospital Value-Based Purchasing, a practice that sets the technological tone for Canada and Mexico. FDA oversight raises documentation hurdles but also signals long-term stability once approvals are secured. Growth remains steady rather than explosive, tied more to replacement demand and technology refresh cycles than to procedure expansion.

Europe contributes a balanced growth profile underpinned by centralized purchasing but evidence-driven device evaluation. The Medical Device Regulation compels continuous post-market surveillance, pushing manufacturers to maintain clinical databases that prove benefit in real-world registries. Germany and the United Kingdom lead plate adoption because academic networks publish outcome data rapidly, swaying clinician sentiment continent-wide. Southern and Eastern Europe focus on cost-optimized titanium kits, importing from regional producers that meet MDR yet undercut multinational prices. Currency volatility and healthcare budget negotiations influence unit flow, but ageing populations promise demand resilience inside the European slice of the sternal closure systems market.

Asia-Pacific posts the fastest 11.61% CAGR. China's public-private hospital modernization programs increased open-heart capacity by 14% year on year, while India's private tertiary chains invest in high-acuity cardiac floors that attract medical tourism. Japan retains strict Shonin device clearance, extending time to market but rewarding durable safety records once obtained. Lower-income ASEAN members favor hybrid procurement, often equipping flagship state hospitals with titanium plates while community centers still rely on wires. Cultural emphasis on scar minimization spurs minimally invasive procedure uptake, indirectly supporting plate adoption. Vendors successful in this region run dual portfolios: imported titanium for tier-1 cities and stainless assembled locally for price-sensitive provinces, achieving breadth in the sternal closure systems market.

- Johnson & Johnson (DePuy Synthes & Ethicon)

- Zimmer Biomet

- Stryker

- KLS Martin Group

- B. Braun

- Acumed

- Medtronic

- Orthofix

- Abyrx

- Kinamed Inc

- Jace Medical

- Praesidia

- IDEAR SRL

- RTI Surgical

- Arthrex

- Jeil Medical Corp

- Neos Surgery SL

- MedXpert GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Volume of Open-Heart Procedures & Ageing Demographics

- 4.2.2 Rising Incidence of Complex, Non-Healing Sternotomy Wounds

- 4.2.3 Rapid Adoption of Rigid Plate-And-Screw Fixation Systems

- 4.2.4 Hospital Bundled-Payment Programs Favouring Low-Readmission Devices

- 4.2.5 Emergence of Bio-Absorbable Polymer/PEEK Sternum Implants

- 4.2.6 AI-Guided Intra-Operative Imaging Improving Closure Accuracy

- 4.3 Market Restraints

- 4.3.1 Infection & Dehiscence Risks In High-BMI/Diabetic Cohorts

- 4.3.2 High Device & OR Time Costs Vs. Conventional Wires

- 4.3.3 Shortage Of Surgeons Trained On Rigid Fixation Systems

- 4.3.4 Heightened Regulatory Scrutiny On Implant Particulates (Micro-Plastics)

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Wires

- 5.1.2 Plates & Screws

- 5.1.3 Bone Cement & Adhesives

- 5.1.4 Bio-absorbable Systems

- 5.1.5 Others

- 5.2 By Procedure

- 5.2.1 Median Sternotomy

- 5.2.2 Hemi-sternotomy

- 5.2.3 Bilateral Thoracosternotomy

- 5.3 By Material

- 5.3.1 Stainless Steel

- 5.3.2 Titanium

- 5.3.3 Polyether-ether-ketone (PEEK)

- 5.3.4 Composite/Bio-absorbable Polymers

- 5.4 By End User

- 5.4.1 Tertiary Care Hospitals

- 5.4.2 Cardio-Thoracic Specialty Clinics

- 5.4.3 Ambulatory Surgery Centers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Johnson & Johnson (DePuy Synthes & Ethicon)

- 6.3.2 Zimmer Biomet Holdings

- 6.3.3 Stryker Corporation

- 6.3.4 KLS Martin Group

- 6.3.5 B Braun SE

- 6.3.6 Acumed LLC

- 6.3.7 Medtronic plc

- 6.3.8 Orthofix Holdings Inc

- 6.3.9 Abyrx Inc

- 6.3.10 Kinamed Inc

- 6.3.11 Jace Medical

- 6.3.12 Praesidia SRL

- 6.3.13 IDEAR SRL

- 6.3.14 RTI Surgical

- 6.3.15 Arthrex Inc

- 6.3.16 Jeil Medical Corp

- 6.3.17 Neos Surgery SL

- 6.3.18 MedXpert GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment