|

시장보고서

상품코드

1846352

스트레처 체어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Stretcher Chairs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

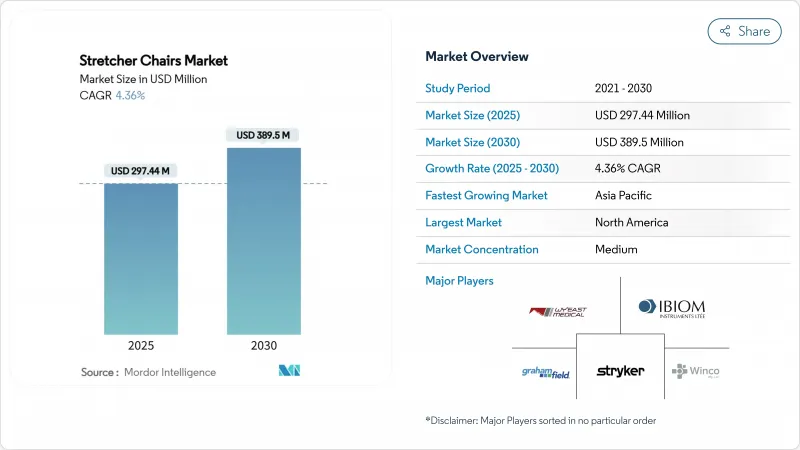

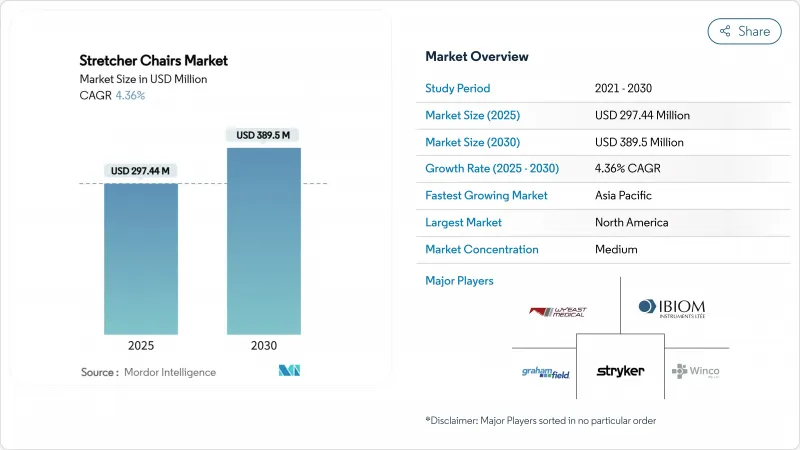

스트레처 체어 시장의 2025년 시장 규모는 2억 9,744만 달러로 평가되었고, 2030년에 3억 8,950만 달러에 이를 것으로 예측되며, CAGR은 4.36%를 나타낼 전망입니다.

이러한 꾸준한 성장은 환자 중심 이동성, 간병인 인체공학, 강화되는 규제 요건을 조화시킨 의료 시스템의 우선순위를 반영합니다. 외래 수술 센터(ASC) 성장 가속화, ‘무리프트’ 병원 정책의 광범위한 도입, 구동 시스템의 기술 업그레이드가 모두 수요를 뒷받침합니다. 시설들이 근골격계 손상 감소를 정량화함에 따라 전동식 모델의 인기가 높아지고 있으며, 비만 유병률 증가 속에서 비만 환자 대응 모델은 프리미엄 가격을 형성하고 있습니다. 동시에 제조사들은 2026년 시행 예정인 FDA 품질 시스템 개정안 강화와 구매 주기를 연장시킬 수 있는 변동성 있는 메디케어 환급 정책을 헤쳐 나가야 합니다. 이러한 전반적인 추세는 의료용 스트레처 체어 시장이 인구 구조 변화와 의료 시설 현대화 프로그램 모두로부터 혜택을 볼 수 있는 위치에 놓이게 합니다.

세계의 스트레처 체어 동향 및 인사이트

노인 인구 증가

65세 이상 인구의 비율이 급격히 상승하며, 병원, 외래 진료 센터, 장기 요양 시설 전반에 걸쳐 일상적 이동성 수요가 증가하는 인구학적 전환이 진행 중입니다. 시설들은 낮은 이송 높이, 통합 생체 신호 모니터링, 압박 손상 위험을 최소화하는 쿠션 기능을 갖춘 스트레처 체어를 지정함으로써 이에 대응하고 있습니다. 규제 준수 요구도 강화되고 있습니다. 미국 접근성 위원회(Access Board)의 개정된 장비 규정은 대부분의 휠체어 사용자가 스스로 이동할 수 있도록 17인치(약 43cm)의 이동 높이를 요구하며, 이는 높이 조절이 가능한 전동식 모델 채택을 가속화하는 기준입니다. 공급업체에게 고령화 추세는 다년간의 수요 가시성을 확보하고, 존엄성과 처리량을 개선하는 인체공학적 혁신을 향한 의료용 스트레처 체어 시장의 방향성을 강화합니다.

외래수술센터(ASC) 확대

ASC는 메디케어의 장소 중립적 지급과 완화된 필요 인증 규정 덕분에 2023년부터 2027년까지 16.2% 성장할 전망입니다. 환자 회전율이 높은 환경에서는 당일 수술 워크플로우에 부합하는 신속한 세척 표면과 모듈식 액세서리를 갖춘 스트레처 체어가 선호됩니다. 원활한 영상 통합 및 측면 틸팅이 가능한 장비는 수술실 주기 시간을 더욱 단축시킵니다. 이로 인한 구매 물결은 ASC를 의료용 스트레처 체어 시장에서 가장 빠르게 성장하는 고객 그룹으로 자리매김하게 하여, 제조업체들이 전문 외래 환자 요구 사항에 맞춰 서비스 패키지와 교육 모듈을 개발하도록 촉진하고 있습니다.

전동식 스트레처 체어의 높은 자본 비용

전동식 스트레처 체어의 자본 비용은 수동식 대비 약 3-5배 비싸며, 이는 신흥 경제권의 소규모 클리닉 및 시설 예산에 부담을 줍니다. 부상 관련 청구 감소로 구매 비용을 상쇄할 수 있지만, 많은 관리자들은 여전히 여러 회계 연도에 걸쳐 구매를 분할하거나 리스로 전환해야 합니다. 공급업체들은 예방 정비 계약과 수명 주기 내 서비스 요청을 줄여주는 장수명 배터리 번들로 구매 망설임을 해소하고 있습니다. 그러나 단기적으로는 자본 집약도가 전환 속도를 늦추고 광범위한 의료용 스트레처 체어 시장 내 가격 민감형 틈새 시장을 형성할 것입니다.

부문 분석

2024년 의료용 스트레처 체어 시장의 52.34%를 수동식 유닛이 차지했습니다. 그러나 시설들이 간병인 안전과 규정 준수 지표를 우선시함에 따라 전동식 모델은 5.26%의 연평균 성장률(CAGR)로 가속화되고 있습니다. 이러한 변화는 전동식 의료용 스트레처 체어 시장 규모에 반영되어, 2030년까지 다른 어떤 제품 카테고리보다 빠르게 성장할 것으로 전망됩니다. 초기 전환은 주로 응급실과 수술실에서 시작되지만, 교체 주기가 이제 영상의학과 및 외래 진료소로 확대되고 있습니다.

전동식 디자인은 조이스틱 조향, 배터리 상태 표시기, 병원 자산 관리 시스템에 직접 연동되는 사용 분석 기능을 통합합니다. 초기 구매 비용이 높지만 근로자 보상 청구 감소와 이송 시간 단축으로 상쇄되어 총비용 측면에서 경쟁력을 확보합니다. 제조사들은 배터리 소진 시 수동 조작으로 전환 가능한 하이브리드 시스템도 도입하며 구매팀의 위험 인식을 완화하고 있습니다. 이러한 동향들은 의료용 스트레처 체어 시장 내 제품 구성 변화를 재정의할 점진적이면서도 지속적인 전환을 뒷받침합니다.

2024년 의료용 스트레처 체어 시장에서 유압 플랫폼은 43.48%의 점유율을 차지했습니다. 그러나 정밀 위치 조정, 낮은 에너지 사용량, 디지털 인프라와의 원활한 통합으로 전기 모터 시스템은 5.12%의 연평균 성장률(CAGR)로 확장 중입니다. 데이터 기반 유지보수 프로그램을 추구하는 시설들은 탑재 센서가 실시간 진단 정보를 중앙 대시보드에 전송하는 전기 액추에이터를 선택합니다.

전기기계 연구에 따르면 유압식 대비 35-50%의 에너지 절감 효과가 확인되었으며, 이는 병원 지속가능성 목표와 부합하는 이점입니다. 배터리 기술 발전은 작동 주기 관련 기존 우려도 완화합니다. 안전 여유가 최우선인 비만 환자 치료 환경에서는 유압식 리프팅과 전기식 틸팅을 결합한 하이브리드 구성의 인기가 높아지고 있습니다. 결과적으로 전기식 솔루션의 의료용 스트레처 체어 시장 규모는 예측 기간 동안 유압식과의 격차를 좁힐 것으로 예상되나, 다양한 중증도와 예산 수준을 충족하기 위해 두 기술이 공존할 전망입니다.

스트레처 체어 시장은 제품 유형(전동식 스트레처 체어, 수동식 스트레처 체어, 기타), 구동 기술별(전기 모터, 유압식, 기타), 최종 사용자별(병원, 외래 수술 센터, 전문 클리닉 등), 유통 채널별(기관 직접 판매, 의료용품 유통업체, 온라인/기타)로 세분화됩니다. (전기 모터, 유압식 등), 최종 사용자(병원, 외래 수술 센터, 전문 클리닉 등), 유통 채널(기관 직접 판매, 의료용품 유통업체, 온라인/전자상거래), 지역(북미, 유럽, 아시아태평양 등)별로 세분화됩니다.

지역별 분석

2024년 의료용 스트레처 체어 시장은 북미 지역이 41.18%의 점유율로 선두를 차지했습니다. 이 같은 점유율 확대는 OSHA(미국 노동안전보건청)가 지원하는 안전 의무 규정, ASC(외래 수술 센터)에 유리한 메디케어 지급 인센티브, 이동성 프로토콜을 표준화하는 2024년 CDC(미국 질병통제예방센터) 안전 환자 취급 프레임워크에 의해 주도되고 있습니다. 병원들은 주 정부의 ‘무리거림 금지’ 법규를 충족하기 위해 전동식 솔루션에 대규모 투자를 진행하는 반면, 비만율이 40%를 초과하는 가운데 비만 환자용 모델의 중요성이 부각되고 있습니다. 강력한 애프터마켓 서비스 네트워크와 확립된 자본 예산 주기는 자본 심사가 강화되는 상황에서도 지속적인 수요를 유지합니다.

아시아태평양 지역은 중국, 인도, 동남아시아의 의료 인프라 프로젝트에 힘입어 2030년까지 6.28%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 정부 보험 확대는 장비 예산을 늘리는 반면, 민간 운영사는 첨단 이동성 솔루션을 요구하는 고난도 전문 센터를 추가합니다. 지역 제조 클러스터는 부품 비용을 절감하지만, 지역 구매자들은 여전히 프리미엄 액추에이터와 제어 모듈을 수입합니다. 아세안(ASEAN) 의료기기 규정의 조화는 다국적 공급업체의 진입 장벽을 낮추어 지역 의료용 스트레처 체어 시장 내 경쟁 심화를 가속화합니다.

유럽은 고령화 인구, 통합된 의료기기 규정(MDR) 준수, 장기 요양 시설의 인체공학적 업그레이드 지원 국가 정책에 힘입어 꾸준한 도입 추세를 유지하고 있습니다. 병원들은 EN 60601-2-52 침대 안전 기준 인증을 받은 스트레처 체어를 우선적으로 도입하며, 영국과 북유럽 국가들의 조달 체계는 수명 주기 탄소 발자국 평가를 점차 확대 적용하고 있습니다. 브렉시트 관련 통관 검사로 인해 영국 구매자들의 리드 타임이 길어지면서 일부는 지역 조달 전략으로 전환하고 있습니다. 지속가능성 지표와 엄격한 근로자 안전 규정이 결합되어 전체 의료용 스트레처 체어 시장 확장에 느리지만 꾸준한 기여를 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 사고 및 외상 발생 건수 증가

- 고령 인구 증가

- 외래수술센터(ASC)의 확대

- 병원에서「노리프트」안전 대처

- 영상 촬영대 시스템과의 통합

- 비만 환자용 의자 수요 증가

- 시장 성장 억제요인

- 전동식 의자의 높은 자본 비용

- 제한된 보험 적용 정책

- 영상 규정 준수 관련 규제 지연

- 고하중 액추에이터 공급망 공백

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 전동식 스트레처 의자

- 수동식 스트레처 체어

- 기타

- 작동 기술별

- 전동 모터

- 유압식

- 공압

- 기계식

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 재택치료

- 기타

- 판매 채널별

- 기관 직접 판매

- 의료용품 판매업자

- 온라인 및 전자상거래

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Stryker Corporation

- GF Health Products, Inc.

- Winco Mfg LLC(Champion Manufacturing Inc.)

- Wy'East Medical

- IBIOM Instruments Ltee

- Productos Metalicos del Bages(Promeba)

- NovyMed International

- UFSK-International OSYS

- LINET Group SE

- Drive DeVilbiss Healthcare(Medical Depot, Inc.)

- Invacare Corporation

- Ferno-Washington

- TransMotion Medical

- Midmark Corporation

제7장 시장 기회와 전망

HBR 25.11.10The medical stretcher chairs market is valued at USD 297.44 million in 2025 and is forecast to reach USD 389.50 million by 2030, expanding at a 4.36% CAGR.

This steady progression reflects health-system priorities that blend patient-centric mobility, caregiver ergonomics, and tightening regulatory mandates. Accelerating ambulatory surgical center (ASC) growth, wider adoption of "no-lift" hospital policies, and technology upgrades in actuation systems all reinforce demand. Powered variants gain traction as facilities quantify reductions in musculoskeletal injuries, while bariatric-capable models command premium pricing amid rising obesity prevalence. At the same time, manufacturers navigate stricter FDA quality system amendments taking effect in 2026 and variable Medicare reimbursement that can prolong purchase cycles. The overall momentum positions the medical stretcher chairs market to benefit from both demographic shifts and health-facility modernization programs.

Global Stretcher Chairs Market Trends and Insights

Rise in Geriatric Population

The proportion of individuals aged 65 and older is climbing sharply, a demographic transition that elevates day-to-day mobility demands across hospitals, outpatient centers, and long-term-care sites. Facilities respond by specifying stretcher chairs with low transfer heights, integrated vital-sign monitoring, and cushioning that minimizes pressure-injury risk. Compliance imperatives also intensify: updated U.S. Access Board equipment rules require 17-inch transfer heights so most wheelchair users can self-transfer, a standard that accelerates adoption of height-adjustable powered models. For vendors, the aging trend secures multi-year demand visibility and reinforces the medical stretcher chairs market's orientation toward ergonomic innovations that improve dignity and throughput.

Expansion of Ambulatory Surgical Centers

ASCs are expanding by 16.2% from 2023-2027, supported by Medicare site-neutral payments and relaxed certificate-of-need statutes. High patient-turnover environments favor stretcher chairs with rapid cleaning surfaces and modular accessories that align with same-day surgery workflows. Equipment capable of seamless imaging integration and lateral tilting further shortens room cycles. The resulting procurement wave positions ASCs as the fastest-growing customer group within the medical stretcher chairs market, prompting manufacturers to tailor service packages and training modules to specialized outpatient requirements.

High Capital Cost of Powered Chairs

Powered stretcher chairs cost roughly 3-5 times more than manual units, challenging budgets of small clinics and facilities in emerging economies. Although reductions in injury claims can offset purchase expense, many administrators must still stage acquisitions over multiple fiscal cycles or shift toward leasing. Vendors counter hesitation by bundling preventative-maintenance contracts and extended batteries that lower lifetime service calls. Over the near term, however, capital intensity will temper conversion speed and carve price-sensitive niches inside the broader medical stretcher chairs market.

Other drivers and restraints analyzed in the detailed report include:

- Hospital "No-Lift" Safety Initiatives

- Demand for Bariatric-Capable Chairs

- Limited Reimbursement Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual units accounted for 52.34% of the medical stretcher chairs market in 2024 thanks to cost advantages and minimal training needs. Powered models, however, are accelerating at a 5.26% CAGR as facilities prioritize caregiver safety and compliance metrics. This migration is reflected in the medical stretcher chairs market size for powered variants, which is projected to expand faster than any other product category through 2030. Early conversions often begin in emergency departments and surgical suites, but replacement cycles are now spreading to imaging wings and outpatient clinics.

Powered designs integrate joystick steering, battery health indicators, and usage analytics that feed directly into hospital asset-management systems. Their higher upfront price is counterbalanced by fewer worker compensation claims and shorter transfer times, reinforcing total-cost propositions. Manufacturers are also introducing hybrid systems that allow manual fallback during battery depletion, reducing risk perception among procurement teams. Collectively, these dynamics underpin a gradual yet durable shift that will redefine product-mix composition inside the medical stretcher chairs market.

Hydraulic platforms held 43.48% of the medical stretcher chairs market share in 2024 due to proven load-bearing reliability and smooth motion. Electric motor systems, though, are expanding at a 5.12% CAGR, propelled by precision positioning, lower energy usage, and seamless integration with digital infrastructures. Facilities seeking data-rich maintenance programs opt for electric actuators because onboard sensors feed real-time diagnostics to central dashboards.

Electromechanical research indicates 35-50% energy savings compared with hydraulics, a benefit aligned with hospital sustainability goals. Battery advances also mitigate prior concerns over duty cycles. Hybrid configurations, pairing hydraulic lifting with electric tilting, gain popularity in bariatric contexts where fail-safe margin remains paramount. As a result, the medical stretcher chairs market size for electric solutions is expected to close the gap on hydraulics during the forecast period, although both technologies will coexist to address varying acuity and budget tiers.

The Stretcher Chairs Market is Segmented by Product Type (Powered Stretcher Chairs, Manual Stretcher Chairs, Others), by Actuation Technology (Electric Motor, Hydraulic, and More), by End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and More), by Distribution Channel (Direct Institutional Sales, Medical Supply Distributors, Online / E-Commerce), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America led with 41.18% share of the medical stretcher chairs market in 2024. Uptake is driven by OSHA-backed safety mandates, Medicare payment incentives favoring ASCs, and the 2024 CDC Safe Patient Handling framework that standardizes mobility protocols. Hospitals invest heavily in powered solutions to meet state "no-lift" laws, whereas bariatric models gain prominence amid obesity rates exceeding 40%. Robust aftermarket service networks and established capital-budget cycles sustain recurring demand even as capital scrutiny intensifies.

Asia-Pacific is poised for the fastest 6.28% CAGR through 2030, buoyed by healthcare infrastructure projects in China, India, and Southeast Asia. Government insurance expansions broaden equipment budgets, while private operators add high-acuity specialty centers that specify advanced mobility solutions. Local manufacturing clusters reduce component costs, but regional buyers still import premium actuators and control modules. Harmonization of ASEAN medical device regulations lowers entry barriers for multinational suppliers, amplifying competitive depth within the regional medical stretcher chairs market.

Europe maintains steady adoption on the back of aging demographics, unified MDR compliance, and national initiatives that reward ergonomic upgrades in long-term care. Hospitals prioritize stretcher chairs certified to EN 60601-2-52 bed safety standards, while procurement frameworks in the United Kingdom and Nordic countries increasingly apply lifecycle carbon-footprint scoring. Brexit-related customs checks have elongated lead times for U.K. buyers, nudging some toward regional sourcing strategies. Sustainability metrics combined with stringent worker-safety regulations underpin a consistent, if slower, contribution to overall medical stretcher chairs market expansion.

- Stryker

- GF Health Products, Inc.

- Winco Mfg LLC (Champion Manufacturing Inc.)

- Wy'East Medical

- IBIOM Instruments Ltee

- Productos Metalicos del Bages (Promeba)

- NovyMed International

- UFSK-International OSYS

- LINET Group

- Drive DeVilbiss Healthcare (Medical Depot, Inc. )

- Invacare

- Ferno-Washington

- TransMotion Medical

- Midmark

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in number of accidents & trauma

- 4.2.2 Rise in geriatric population

- 4.2.3 Expansion of ambulatory surgical centers

- 4.2.4 Hospital "no-lift" safety initiatives

- 4.2.5 Integration with imaging-table systems

- 4.2.6 Demand for bariatric-capable chairs

- 4.3 Market Restraints

- 4.3.1 High capital cost of powered chairs

- 4.3.2 Limited reimbursement policies

- 4.3.3 Regulatory delays for imaging compliance

- 4.3.4 Supply-chain gaps in high-load actuators

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Powered Stretcher Chairs

- 5.1.2 Manual Stretcher Chairs

- 5.1.3 Others

- 5.2 By Actuation Technology

- 5.2.1 Electric Motor

- 5.2.2 Hydraulic

- 5.2.3 Pneumatic

- 5.2.4 Mechanical

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Home-Care Settings

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Direct Institutional Sales

- 5.4.2 Medical Supply Distributors

- 5.4.3 Online / E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Stryker Corporation

- 6.3.2 GF Health Products, Inc.

- 6.3.3 Winco Mfg LLC (Champion Manufacturing Inc.)

- 6.3.4 Wy'East Medical

- 6.3.5 IBIOM Instruments Ltee

- 6.3.6 Productos Metalicos del Bages (Promeba)

- 6.3.7 NovyMed International

- 6.3.8 UFSK-International OSYS

- 6.3.9 LINET Group SE

- 6.3.10 Drive DeVilbiss Healthcare (Medical Depot, Inc. )

- 6.3.11 Invacare Corporation

- 6.3.12 Ferno-Washington

- 6.3.13 TransMotion Medical

- 6.3.14 Midmark Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment