|

시장보고서

상품코드

1848034

홈 헬스케어 소프트웨어 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Home Healthcare Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

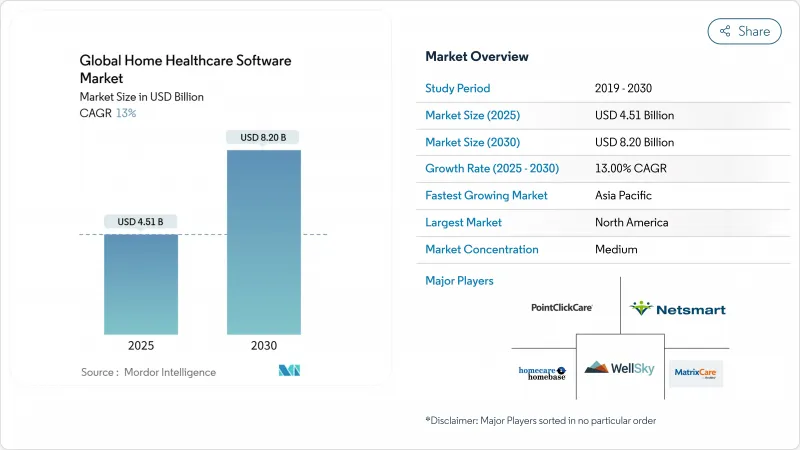

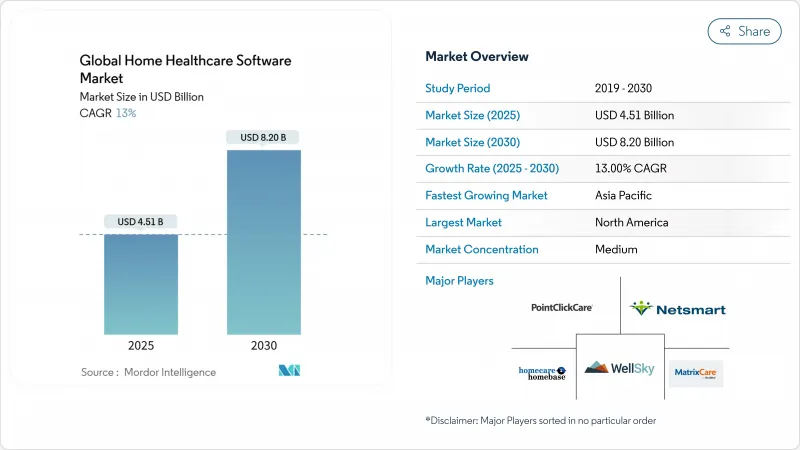

홈 헬스케어 소프트웨어 시장 규모는 2025년에 45억 1,000만 달러로 평가되었고, 2030년에 82억 달러에 이를 것으로 예측되며, CAGR은 13.00%를 나타낼 전망입니다.

가치 기반 의료에 대한 보험사의 보상, 의료 시스템의 복잡한 치료 가정 이송 확대, 그리고 보상 규칙이 점점 더 문서화된 결과와 지급을 연계함에 따라 수요가 증가하고 있습니다. 특히 메디케이드 자금과 연계된 전자 방문 확인(EVV) 의무화는 디지털 문서화를 지급 조건으로 삼아 소프트웨어 도입을 더욱 촉진합니다. 클라우드 배포는 온프레미스 대안에 비해 총 소유 비용을 약 77% 절감하여 모든 규모의 기관에 매력적인 제공 모델을 제공합니다. 강력한 벤처 자금과 기존 벤더들의 전략적 인수는 분석, 원격 모니터링, AI 기반 수익 주기 도구 분야의 혁신을 가속화합니다. 마지막으로, 지불자와 제공자는 주거 환경에서 급성 치료를 조정할 수 있는 상호 운용 가능한 플랫폼에 의존하는 ‘병원형 가정 간호(hospital-at-home)’ 프로그램을 실험 중입니다.

세계의 홈 헬스케어 소프트웨어 시장 동향 및 인사이트

가치 기반 의료로의 전환이 소프트웨어 요구사항을 변화시키고 있습니다

지불자들은 계속해서 행위별 요금제(fee-for-service)에서 측정 가능한 결과를 보상하는 모델로 전환하고 있습니다. 유나이티드헬스 그룹은 조정된 재택 간호가 만성 질환 환자의 병원 입원률을 최대 25%까지 낮출 수 있다고 보고합니다. 의료 제공자들은 이제 품질 지표, 위험 점수, 임상 경로를 추적하는 내장형 분석 기능을 갖춘 플랫폼을 구매합니다. 홈 헬스케어 가치 기반 구매(Home Health Value-Based Purchasing) 프레임워크를 시범 운영하는 주에서는 소프트웨어가 시기적절하고 정확한 결과 보고서를 제공할 때 기관들이 보상 보너스를 받습니다. 공급업체들은 환자가 재입원 임계치에 접근할 때 직원을 경고하는 예측 알고리즘을 통합하여 정액제 계약의 마진을 보호합니다. 성과 기반 지불이 확대됨에 따라 홈 헬스케어 소프트웨어 시장은 선택적 도구가 아닌 핵심 인프라로 자리매김하고 있습니다.

전자 방문 확인 의무화로 가속화되는 디지털 도입

21세기 치료법(21st Century Cures Act)은 EVV를 메디케이드(Medicaid) 환급에 필수로 규정합니다. 펜실베이니아주와 뉴욕주 등은 2025년까지 각각 85%, 90%의 EVV 준수율을 요구하며, 미준수 시 지급을 거부합니다. EVV 플랫폼은 서비스 유형, 수혜자, 날짜, 위치, 제공자, 시간 등 6가지 데이터 포인트를 GPS 지원 모바일 앱이나 고정 장치를 통해 검증해야 합니다. 종이 프로세스에 의존하던 소규모 기관들도 이제 면허 유지를 위해 디지털 방문 기록을 도입하고 있습니다. 공급업체들은 EVV 모듈을 광범위한 제품군에 통합하여 스케줄링, 청구, 임상 문서화 등 추가 판매의 관문을 마련하고 있습니다. 이러한 의무화는 도입 일정을 압축하여 홈 헬스케어 소프트웨어 시장의 잠재 수요에 급격한 변화를 초래하고 있습니다.

데이터 보안 우려가 도입 장벽으로 작용

의료 분야는 여전히 주요 사이버 범죄 표적입니다. 2024년 랜섬웨어 공격 급증으로 기관들은 위험 허용 수준을 재평가해야 했으며, 특히 HIPAA 위반 시 건당 100-50,000달러의 벌금이 부과되기 때문입니다. 소규모 공급업체들은 전담 보안 인력이 부족해 신규 플랫폼 도입 결정이 지연됩니다. 벤더들은 종단 간 암호화, 세분화된 역할 기반 권한, 감사 추적 기능을 추가하지만, 고객사는 여전히 반복적인 침투 테스트 및 규정 준수 감사 비용에 직면합니다. 유럽에서는 GDPR이 엄격한 침해 통보 기간을 규정하여 잠재적 벌금과 평판 손상을 가중시킵니다. 이러한 요인들은 디지털 도구에 대한 운영적 필요성이 계속 증가함에도 불구하고 홈 헬스케어 소프트웨어 시장의 판매 주기를 연장시킵니다.

부문 분석

2024년 전체 매출의 35%를 차지한 기관 관리 솔루션은 대부분의 공급업체 운영 핵심 역할을 반영합니다. 이러한 플랫폼은 일정 관리, 급여 처리, 규정 준수 보고를 통합하여 소규모 기관조차도 분산된 인력을 효율적으로 조정할 수 있게 합니다. Homecare Homebase 및 MatrixCare와 같은 선도적인 제품군은 안정적인 가동 시간과 분기별 심층적인 규제 업데이트를 결합하여 장기 계약을 확보하고 있습니다. 홈 헬스케어 소프트웨어 시장은 보다 광범위한 디지털 전환의 진입점으로 이러한 핵심 시스템에 의존하고 있습니다.

성장세는 원격의료, 원격 모니터링, AI 지원 임상 의사 결정 지원을 결합한 기타 소프트웨어 부문으로 이동하고 있습니다. 해당 부문은 2030년까지 연평균 15.2% 성장률을 기록하며 전체 홈 헬스케어 소프트웨어 시장을 앞지르고 있습니다. 가상 진료 플랫폼은 팬데믹 이전 수준을 훨씬 상회하는 사용률을 유지하고 있으며, AI 기록 보조 시스템은 이제 영상 통화에서 직접 진료 기록을 작성합니다. 공급업체들은 이러한 전문 모듈을 핵심 기관 시스템에 긴밀히 통합하여 원활한 데이터 흐름과 풍부한 분석 기능을 창출합니다. 보험사들이 원격 서비스를 대면 진료와 동등하게 보상함에 따라, 전문 솔루션들은 제공자 전반에 걸쳐 점유율을 확대하고 있습니다.

전문 간호 부문은 2024년 매출의 42%를 차지하며 가정 기반 급성기 후 치료에서의 우위를 입증했습니다. 병원들은 복잡한 사례를 조기에 퇴원시키고, 품질 점수에 영향을 미치는 30일 재입원 기간 동안 재입원을 방지하기 위해 기관들과 협력합니다. 전문 간호 소프트웨어는 상처 관리 템플릿, 약물 조정, 다학제적 치료 계획 조정을 우선시합니다. 간호 방문은 방대한 문서 작업량을 발생시키므로, 자연어 처리 유틸리티가 임상진의 기록 작성 속도를 높여 홈 헬스케어 소프트웨어 시장에서 방문 수용 능력을 유지합니다.

현재 규모는 작지만, 주입 요법은 14%의 연평균 성장률(CAGR)로 발전하며 가장 빠르게 성장하는 서비스 라인입니다. 고가의 생물학적 제제 및 특수 의약품은 과거 입원 환경에 국한되었으나, 이제는 가정으로 이동하며 투여 비용이 급격히 감소합니다. 플랫폼은 백 로트 번호 추적 및 자동 재주문 기능을 갖춘 재고 관리 시스템을 내장하여 낭비를 최소화합니다. 원격 약국 연결을 통해 의료진은 환자의 생체 신호에 기반하여 실시간으로 용량을 조정할 수 있어 안전성이 향상됩니다. 이 부문의 역동성은 치료별 워크플로우를 목표로 하는 공급업체들에게 서비스 다각화가 홈 헬스케어 소프트웨어 시장 규모를 어떻게 확대하는지 보여줍니다.

지역 분석

북미는 2024년 글로벌 매출의 42.0%를 유지하며, 선진화된 보상 모델과 메디케이드 방문마다 소프트웨어 사용을 의무화하는 엄격한 EVV 시행이 이를 견인합니다. 미국 단독으로 지역 지출의 5분의 4 이상을 차지하는 반면, 캐나다의 단일 지불자 구조는 주 전체 플랫폼 조달을 지원합니다. 국경을 초월한 상호운용성은 여전히 주요 의제로 남아 있습니다. 겨울철 남부 지역으로 이동하는 인구(스노우버드)를 지원하는 기관들은 여러 주의 메디케이드 시스템과 데이터 교환이 필요하기 때문입니다.

아시아태평양 지역은 14.0%의 연평균 성장률(CAGR)로 가장 빠른 확장세를 기록하고 있습니다. 인도, 중국, 인도네시아 정부는 클라우드 시범 사업 및 원격의료 네트워크를 지원하는 디지털 헬스 미션을 후원하고 있습니다. 대형 민간 병원 체인들은 퇴원 후 수익을 확보하고 입원 환자 혼잡을 줄이기 위해 가정 건강 관리 부서를 개설하고 있습니다. 스마트폰 보급률 급증으로 중장비 투자 없이도 모바일 진료 워크플로우가 가능해져 신규 진입업체들이 기존 시스템을 뛰어넘을 수 있게 되었습니다. 이러한 추세는 현지 언어 지원 및 데이터 거주 규정 준수가 가능한 국제 벤더들의 홈 헬스케어 소프트웨어 시장 규모를 확대합니다.

유럽은 매출 기준 2위를 차지하며, 수요는 독일, 영국, 프랑스에 집중됩니다. 규제 당국은 '상호운용 가능한 유럽 법(Interoperable Europe Act)'과 같은 법률을 통해 국경 간 데이터 이동성을 촉진하여 표준 기반 플랫폼 투자 유인을 창출합니다. 기관들은 GDPR(일반 데이터 보호 규정) 준수 의무를 이행해야 하므로 암호화 및 동의 관리에 대한 관심이 더욱 강화되고 있습니다. 해당 지역의 민간 보험사들은 미국식 가치 기반 지불 체계와 유사한 성과 기반 계약을 시범 운영하며, 홈헬스케어 소프트웨어 시장 내 고급 분석 기술 도입 필요성을 부각시키고 있습니다. 중동, 아프리카, 남미 등 신흥 지역은 기반이 작지만 기존 인프라가 취약하여 클라우드 솔루션을 빠르게 도입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 가치 기반 및 가정 중심 치료 모델로의 전환

- 전자 방문 확인 및 결과 보고에 대한 정부 의무화

- 의료 제공자의 클라우드 및 모바일 우선 건강 정보 기술(Health-IT)의 급속한 도입

- 고령화와 만성 질환에 의한 홈 헬스케어 수요의 확대

- 급성기, 급성기 후 치료 및 보험자 시스템 전반에 걸친 상호운용성 추진

- 벤처 기업에 의한 자금 조달과 M&A가 디지털 홈 헬스케어의 혁신을 가속

- 시장 성장 억제요인

- 데이터 보안 및 HIPAA/GDPR 준수 문제

- 지불자 간 분산된 보상 및 청구 규정

- 소규모 기관의 제한된 IT 예산 및 변화 관리 장벽

- 기존 EHR 및 의료 기기와의 통합 복잡성

- 가치/공급망 분석

- 규제의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 소프트웨어 유형별

- 기관 관리 솔루션

- 임상 관리 시스템

- 호스피스 및 완화 의료 소프트웨어

- 기타 소프트웨어

- 서비스별

- 재활

- 주입 요법

- 호흡 요법

- 임신 및 산후 케어

- 전문 간호

- 기타 서비스

- 제공 형태별

- 클라우드 기반

- 온프레미스

- 하이브리드

- 최종 사용자별

- 홈 헬스케어 기관

- 호스피스

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- WellSky Corp.

- NetSmart Technologies

- MatrixCare(Brightree & ResMed)

- Homecare Homebase LLC

- PointClickCare Technologies

- Axxess Technology Solutions

- AlayaCare Inc.

- Delta Health Technologies

- Allscripts Healthcare Solutions Inc.

- MEDITECH

- Oracle Health(Cerner)

- McKesson Corporation

- CARECENTA, INC.

- AxisCare LLC

- Thornberry Ltd.

- Kinnser Software Inc.

- ClearCare(WellSky Personal Care)

- HealthCare Provider Solutions Inc.

- Epic Systems(Home Health module)

- GE Healthcare Digital

- Teladoc Health

제7장 시장 기회와 전망

HBR 25.11.10The home healthcare software market size is valued at USD 4.51 billion in 2025 and is forecast to reach USD 8.20 billion by 2030, expanding at a 13.00% CAGR.

Demand is rising as payers reward value-based care, health systems push more complex treatments into the home, and reimbursement rules increasingly link payment to documented outcomes. Electronic visit verification (EVV) mandates, especially those tied to Medicaid funding, further increase software adoption by making digital documentation a condition for payment. Cloud deployment lowers total cost of ownership by about 77% versus on-premises alternatives, making the delivery model attractive for agencies of all sizes. Strong venture funding and strategic acquisitions by established vendors accelerate innovation in analytics, remote monitoring, and AI-driven revenue cycle tools. Finally, payers and providers are experimenting with hospital-at-home programs, which depend on interoperable platforms capable of orchestrating acute care in residential settings.

Global Home Healthcare Software Market Trends and Insights

Shift to Value-Based Care Transforming Software Requirements

Payers continue to pivot away from fee-for-service toward models that reward measurable outcomes. UnitedHealth Group reports that coordinated home care can lower hospital admissions by as much as 25% for chronically ill patients. Providers now purchase platforms with embedded analytics that track quality metrics, risk scores, and clinical pathways. In states piloting the Home Health Value-Based Purchasing framework, agencies see reimbursement bonuses when software supplies timely, accurate outcome reports. Vendors integrate predictive algorithms to alert staff when patients approach thresholds for readmission, thereby protecting margins in capitated contracts. As pay-for-performance expands, the home healthcare software market becomes mission-critical infrastructure rather than an optional tool.

Electronic Visit Verification Mandates Accelerating Digital Adoption

The 21st Century Cures Act locks EVV into Medicaid reimbursement. States such as Pennsylvania and New York require 85% and 90% EVV compliance respectively by 2025, with payment denials for failures. EVV platforms must verify six data points-service type, recipient, date, location, provider, and time-often through GPS-enabled mobile apps or fixed devices. Smaller agencies that once relied on paper processes are now adopting digital visit capture to stay licensed. Vendors bundle EVV modules into broader suites, creating a gateway to upsell scheduling, billing, and clinical documentation. These mandates compress adoption timelines, producing a step-change in addressable demand for the home healthcare software market.

Data Security Concerns Creating Implementation Barriers

Healthcare remains a prime cyber-crime target. A surge in ransomware hits during 2024 forced agencies to reassess risk tolerance, especially when HIPAA fines span USD 100 to USD 50,000 per incident. Smaller providers lack dedicated security staff, slowing decisions on new platforms. Vendors add end-to-end encryption, granular role-based permissions, and audit trails, yet clients still face recurring penetration-testing and compliance audit costs. In Europe, GDPR stipulates strict breach notification windows, raising potential penalties and reputational damage. These factors lengthen sales cycles in the home healthcare software market even as the operational need for digital tools grows unchecked.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Based Solutions Dominating Market Growth

- Chronic Disease Management Driving Specialized Software Demand

- Reimbursement Complexity Hampering Software ROI

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agency Management Solutions accounted for 35% of total revenue in 2024, reflecting their role as the operational backbone for most providers. These platforms consolidate scheduling, payroll, and compliance reporting, enabling even small agencies to coordinate distributed workforces efficiently. Leading suites such as Homecare Homebase and MatrixCare secure long-term contracts by pairing reliable uptime with deep regulatory updates every quarter. The home healthcare software market relies on these core systems as entry points for broader digital transformation.

Growth momentum is shifting toward the Other Software segment, which combines telehealth, remote monitoring, and AI-assisted clinical decision support. That segment is posting a 15.2% CAGR through 2030, outpacing the overall home healthcare software market. Virtual visit platforms maintain usage levels far above pre-pandemic norms, and AI scribes now draft encounter notes directly from video calls. Vendors tightly integrate these niche modules into core agency systems, creating seamless data flows and richer analytics. As payers reimburse remote services at parity with in-person care, specialized solutions carve out growing wallet share across providers.

Skilled Nursing commands 42% of 2024 revenues, confirming its primacy in home-based post-acute care. Hospitals discharge complex cases earlier, and they partner with agencies to prevent readmissions during the 30-day window that affects quality scores. Software for Skilled Nursing prioritizes wound care templates, medication reconciliation, and interdisciplinary care plan coordination. Because nursing visits generate high documentation volume, natural-language processing utilities help clinicians complete notes faster, preserving visit capacity in the home healthcare software market.

Infusion Therapy, though smaller today, advances at a 14% CAGR and is the fastest-growing service line. Expensive biologics and specialty drugs once confined to inpatient settings now move to the home, where administration costs drop sharply. Platforms embed inventory management to track bag lot numbers and auto-reorder supplies, minimizing waste. Telepharmacy links let clinicians adjust doses in real-time based on patient vitals, improving safety. The segment's dynamism illustrates how service diversification broadens the home healthcare software market size for vendors targeting therapy-specific workflows.

The Home Healthcare Software Market Report is Segmented by Software Type (Air Agency Management Solutions, Clinical Management Systems, and More), Service (Rehabilitation, Infusion Therapy, and More), Mode of Delivery (Cloud-Based, and More), End-User (Home Health Agencies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 42.0% of global revenue in 2024, propelled by advanced reimbursement models and stringent EVV enforcement that mandates software for every Medicaid visit. The United States alone contributes more than four-fifths of regional spending, while Canada's single-payer structure supports province-wide platform procurements. Cross-border interoperability remains an agenda item, as agencies serving snowbird populations require data exchange with multiple state Medicaid systems.

Asia-Pacific records the briskest expansion at 14.0% CAGR. Governments in India, China, and Indonesia sponsor digital health missions that fund cloud pilots and telehealth networks. Large private hospital chains open home health divisions to capture post-discharge revenue and reduce inpatient congestion. Rapid smartphone penetration enables mobile clinician workflows without heavy hardware investment, allowing new entrants to leapfrog legacy deployments. These trends enlarge the home healthcare software market size for international vendors capable of local language support and data residency compliance.

Europe ranks second by revenue, with demand concentrated in Germany, the United Kingdom, and France. Regulators promote cross-border data portability through laws such as the Interoperable Europe Act, creating incentives to invest in standards-based platforms. Agencies must also align with GDPR, reinforcing focus on encryption and consent management. Private insurers in the region pilot outcome-based contracts that mirror U.S. value-based payment schemes, strengthening the case for advanced analytics within the home healthcare software market. Emerging regions in the Middle East, Africa, and South America grow from a smaller base but adopt cloud solutions quickly due to scarce legacy infrastructure.

- WellSky Corp.

- Netsmart Technologies

- MatrixCare (Brightree & ResMed)

- Homecare Homebase LLC

- PointClickCare Technologies

- Axxess Technology Solutions

- AlayaCare Inc.

- Delta Health Technologies

- Allscripts

- Meditech

- Oracle Health (Cerner)

- Mckesson

- CARECENTA

- AxisCare LLC

- Thornberry Ltd.

- Kinnser Software

- ClearCare (WellSky Personal Care)

- HealthCare Provider Solutions Inc.

- Epic Systems (Home Health module)

- GE Healthcare Digital

- Teladoc Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Value-Based & Home-Centric Care Models

- 4.2.2 Government Mandates for Electronic Visit Verification & Outcome Reporting

- 4.2.3 Rapid Cloud- and Mobile-First Health-IT Adoption by Care Providers

- 4.2.4 Aging Population & Chronic?Disease Burden Expanding Home-Care Demand

- 4.2.5 Interoperability Push Across Acute, Post-Acute, and Payer Systems

- 4.2.6 Venture Funding & M&A Accelerating Digital Home-Care Innovation

- 4.3 Market Restraints

- 4.3.1 Data-Security & HIPAA / GDPR Compliance Concerns

- 4.3.2 Fragmented Reimbursement & Billing Regulations Across Payers

- 4.3.3 Limited IT Budgets & Change-Management Barriers in Small Agencies

- 4.3.4 Integration Complexity with Legacy EHRs and Medical Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Software Type

- 5.1.1 Agency Management Solutions

- 5.1.2 Clinical Management Systems

- 5.1.3 Hospice & Palliative Care Software

- 5.1.4 Other Software

- 5.2 By Service

- 5.2.1 Rehabilitation

- 5.2.2 Infusion Therapy

- 5.2.3 Respiratory Therapy

- 5.2.4 Pregnancy & Post-partum Care

- 5.2.5 Skilled Nursing

- 5.2.6 Other Services

- 5.3 By Mode of Delivery

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End-User

- 5.4.1 Home Health Agencies

- 5.4.2 Hospice Agencies

- 5.4.3 Other End-Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 WellSky Corp.

- 6.4.2 NetSmart Technologies

- 6.4.3 MatrixCare (Brightree & ResMed)

- 6.4.4 Homecare Homebase LLC

- 6.4.5 PointClickCare Technologies

- 6.4.6 Axxess Technology Solutions

- 6.4.7 AlayaCare Inc.

- 6.4.8 Delta Health Technologies

- 6.4.9 Allscripts Healthcare Solutions Inc.

- 6.4.10 MEDITECH

- 6.4.11 Oracle Health (Cerner)

- 6.4.12 McKesson Corporation

- 6.4.13 CARECENTA, INC.

- 6.4.14 AxisCare LLC

- 6.4.15 Thornberry Ltd.

- 6.4.16 Kinnser Software Inc.

- 6.4.17 ClearCare (WellSky Personal Care)

- 6.4.18 HealthCare Provider Solutions Inc.

- 6.4.19 Epic Systems (Home Health module)

- 6.4.20 GE Healthcare Digital

- 6.4.21 Teladoc Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment