|

시장보고서

상품코드

1848037

호르몬 대체 요법 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hormone Replacement Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

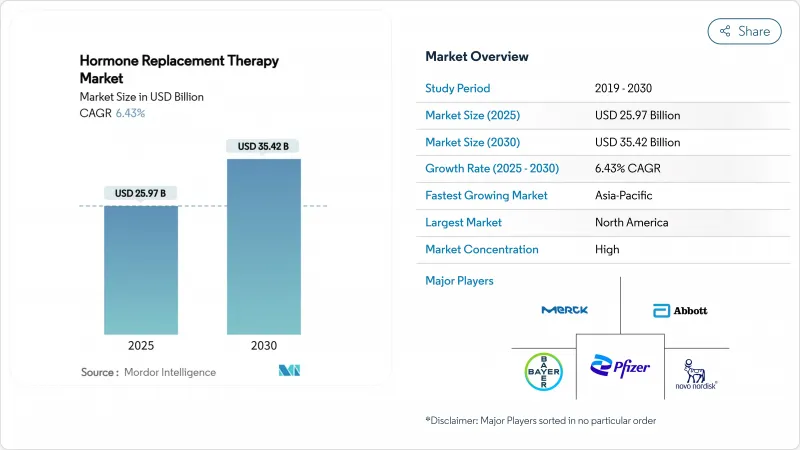

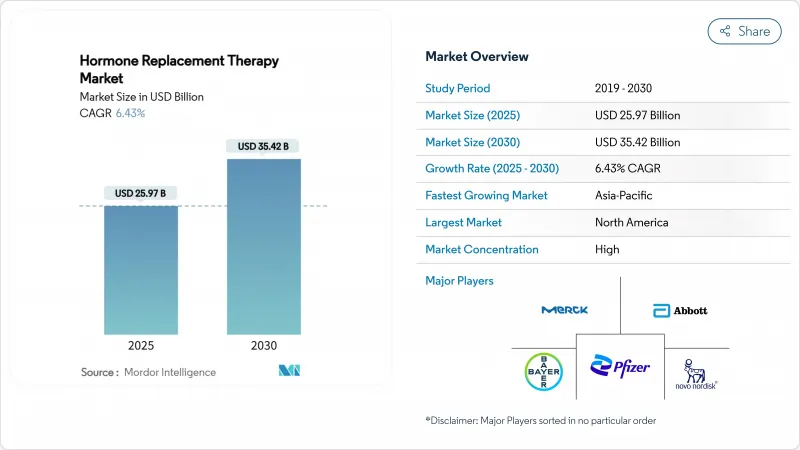

세계의 호르몬 대체 요법 시장 규모는 2025년에 259억 7,000만 달러로 평가되었고, 2030년에 354억 2,000만 달러로 확대될 것으로 예측되며, CAGR은 6.43%를 나타낼 전망입니다.

인구 고령화에 따라 수요가 증가하고 있으며, 50세 이상 여성 인구는 2030년까지 12억 명을 넘어설 것으로 전망됩니다. 여성 건강 이니셔티브(Women's Health Initiative)의 후속 연구 결과는 개별 제형별 위험도를 구분하여 의사의 신뢰를 회복시키고 치료 대상자 풀을 확대했습니다. 원격의료의 급속한 도입으로 지리적 장벽이 제거되었으며, 소비자 직접 플랫폼은 최대 90%의 비용 절감을 실현하고 신규 사용자 유입을 가속화하고 있습니다. 의료비 보상 체계는 지속적으로 확대되고 있으며, 의학적으로 필요한 트랜스젠더 치료 요법에 대한 메디케어 적용이 그 예시로, 이는 더 광범위한 호르몬 치료 보상 모델의 선례를 마련하고 있습니다. 혁신의 초점은 비호르몬성 뉴로키닌 길항제와 조직 선택적 조절제로 이동하면서, 주기적인 안전성 논쟁과 다가오는 특허 만료에도 불구하고 호르몬 대체 요법 시장이 중간 단일자리 수의 지속적인 성장을 유지할 수 있도록 하고 있습니다.

세계의 호르몬 대체 요법 시장 동향 및 인사이트

폐경 후 인구 급증과 평균 수명 증가

여성의 약 1/3 생애가 폐경 후로 이어지면서 인구학적 추세가 잠재적 치료 대상 집단을 확대하고 있습니다. 일본의 경우 관리되지 않은 폐경 증상으로 인한 연간 120억 달러의 부담과 같은 노동력 생산성 손실이 의료비 지불자와 고용주를 선제적 호르몬 치료 프로그램으로 이끌고 있습니다. 공공 보건 전략 내 통합 장수 이니셔티브는 증상 완화를 넘어 장기적 예방 요법으로 이어지는 지속적 수요를 창출하고 있습니다.

생체동일 호르몬 제제의 급속한 채택

임상 증거에 따르면 미분화된 프로게스테론과 에스트라디올 복합제는 기존 말 유래 에스트로겐 복합제보다 심혈관 대사 및 종양학적 위험이 낮아, 건강을 중시하는 중년 여성들 사이에서 20-30%의 프리미엄 가격 책정과 빠른 시장 진입이 가능해졌습니다. TherapeuticsMD의 BIJUVA 승인은 규제 기준을 설정했으며, 2032년까지의 특허 보호로 혁신 기업들에게 방위 가능한 틈새 시장을 제공합니다. Biote의 503B 복합제조 시설 인수를 대표하는 인수합병을 통한 생산 능력 확장은 품질을 표준화하면서 공급을 확보합니다.

WHI 및 후속 연구 이후 암 위험 인식

21년간의 추적 관찰 데이터는 에스트로겐 단독 요법이 유방암 발생률을 23%, 사망률을 40% 감소시킨다는 점을 보여주지만, 2002년 WHI 연구의 초기 헤드라인은 여전히 대중의 인식을 형성하고 있습니다. 비호르몬제인 페졸리네탄(fezolinetant)에 적용된 최근 FDA의 박스 경고문과 같은 조치들은 안전성 논쟁을 지속시키고 의사의 메시지 전달을 복잡하게 만듭니다. 전문 학회들은 개별화된 상담을 통해 65세 이상 치료를 허용하는 입장을 업데이트했으나, 광범위한 채택은 지속적인 교육 확산에 달려 있습니다.

부문 분석

에스트로겐 제품은 2024년 매출의 42.56%를 차지하며 호르몬 대체 요법 시장에서의 핵심적 위치를 재확인했습니다. 그러나 부갑상선 부문은 새로운 적응증이 등장함에 따라 2030년까지 8.51%의 연평균 복합 성장률(CAGR)을 기록하며 호르몬 대체 요법 시장 규모를 다각화된 성장 경로로 이끌고 있습니다. 만성 부갑상선 기능 저하증 치료제인 YORVIPATH와 같은 전문 제품은 프리미엄 가격을 형성하며 광범위한 증상 관리에서 표적 장기 지원으로의 전환을 강조합니다.

정밀 지향적 파이프라인은 미세 투여 에스트로겐과 조직 선택적 조절제를 결합해 세분화된 환자 프로필에 대응합니다. 다중 호르몬 포트폴리오를 보유한 기업들은 유리한 입장에 있는 반면, 단일 제품 업체들은 시장 점유율 감소 위험에 직면합니다. 테스토스테론 수요는 심혈관 관련 경고문 강화로 위축된 반면, 성장 호르몬은 장수 지향 소비자층 사이에서 꾸준한 수요 증가세를 이어가고 있습니다.

경구 요법은 2024년 40.34% 점유율을 유지하며 편의성으로 인해 여전히 광범위하게 처방됩니다. 경피 패치 및 젤은 7.92%의 예상 연평균 성장률(CAGR)에 힘입어 초회 통과 대사 없이 일관된 혈장 농도를 제공하여 호르몬 대체 요법 시장이 맞춤형 투여 방식으로 전환하는 데 기여합니다. 노바티스의 에스트라닷(Estradot) 마이크로 패치는 소형화된 시스템이 어떻게 순응도를 높이는지 보여줍니다.

MIT의 SLIM 미세결정 기술과 같은 장기작용 주사제는 분기별 또는 반기별 투여 가능성을 시사합니다. 질 및 자궁 내 장치는 전신 노출을 최소화하면서 국소 비뇨생식기 증상을 지속적으로 해결하여 투여 선택의 폭을 넓힌다.

지역 분석

북미는 강력한 보험급여 체계, FDA 지침의 명확성, 원격의료 신속 확장을 지원하는 생태계 덕분에 2024년 38.63%의 점유율을 유지했습니다. 성별 확인 치료에 대한 메디케어의 선례는 정책이 어떻게 새로운 시장을 개척할 수 있는지 보여줍니다. 에스트라디올 젤 제네릭 승인 확대는 접근성을 높였으나, 다가오는 특허 만료로 기존 브랜드에 압박이 가해질 수 있습니다.

아시아태평양 지역은 2030년까지 연평균 7.41% 성장률(CAGR)을 기록할 것으로 전망됩니다. 도시 소득 증가, 인구 고령화, 여성 건강에 대한 문화적 인식 변화가 시장 확대를 뒷받침하는 가운데, 일본 기업들은 폐경 관련 결근 비용을 연간 120억 달러로 추산하며 고용주 지원 웰니스 프로그램을 촉진하고 있습니다. 성정체성 확인 치료에 대한 중국의 규제 시범 운영과 인도 중산층의 구매력 증가는 이 지역 전체에 걸쳐 호르몬 대체 요법 시장의 영향력을 확대하고 있습니다.

유럽은 지침에 기반한 꾸준한 수요를 보이지만, 보건기술평가기관(HTA)의 비용 효율성 심사를 받고 있습니다. 내분비계에 영향을 미치는 배출물에 대한 엄격한 환경 규정이 생산 비용에 영향을 미치며, 유럽의약품청(EMA)은 전 지역 모니터링을 의무화하고 있습니다. 중동, 아프리카, 남미 등 신흥 지역은 성장 가능성이 있지만, 다양한 문화적·규제적 환경에 부합하는 현지화 전략이 필요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 폐경 후 인구의 급증과 평균 수명의 성장

- 생체 동일 호르몬 제제의 빠른 채택

- 확장되는 원격 의료 기반 BHRT 구독 모델

- 트랜스젠더 호르몬 대체 요법(HRT)에 대한 보험 적용 확대

- 미량 투여 및 조직 선택적 제제의 파이프라인

- 웨어러블 경피 패치 혁신 및 지속형 주사제

- 시장 성장 억제요인

- WHI 및 후속 연구 이후 암 위험 인식

- 높은 평생 치료 비용 및 제네릭 생체동일성 제품 부재

- 기존 에스트로겐 브랜드의 특허 만료 및 가격 압박

- 내분비계 활성 배출물에 대한 강화된 환경 규제

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 요법별

- 에스트로겐

- 성장 호르몬

- 갑상선 호르몬

- 남성 호르몬

- 부갑상선

- 투여 경로별

- 경구

- 비경구

- 경피

- 질/자궁내

- 이식형 펠릿

- 적응증별

- 갱년기 장애

- 갑상선 기능 저하증

- 성장 호르몬 결핍증

- 기타 적응증

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인/직접 판매 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Bayer AG

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Merck KGaA

- Mylan Viatris

- Novartis AG

- Novo Nordisk A/S

- Pfizer Inc.

- Amgen Inc.

- AbbVie Inc.

- Hisamitsu Pharma

- Endo International

- TherapeuticsMD

- BioTE Medical

- Viatris Inc.

- Ascend Therapeutics

- Acerus Pharma

- Johnson & Johnson(Janssen)

- Teva Pharmaceuticals

제7장 시장 기회와 전망

HBR 25.11.10The global hormone replacement therapy market size reached USD 25.97 billion in 2025 and is forecast to rise to USD 35.42 billion by 2030, translating to a 6.43% CAGR.

Demand grows in line with an aging demographic-women over 50 are projected to exceed 1.2 billion by 2030. Follow-up findings from the Women's Health Initiative now distinguish risks across individual formulations, restoring physician confidence and widening candidate pools for treatment. Rapid telehealth adoption removes geographic barriers, while direct-to-consumer platforms deliver up to 90% cost savings and accelerate first-time user adoption. Reimbursement pathways keep expanding, as seen in Medicare coverage for medically necessary transgender regimens, which establishes precedents for broader hormonal care reimbursement models. Innovation attention has shifted toward non-hormonal neurokinin antagonists and tissue-selective modulators, positioning the hormone replacement therapy market for sustained mid-single-digit growth despite periodic safety debates and upcoming patent cliffs.

Global Hormone Replacement Therapy Market Trends and Insights

Surging Post-Menopausal Population & Life-Expectancy Gains

Demographic momentum is enlarging the potential treatment pool as women now spend roughly one-third of their lives post-menopause. Workforce productivity losses, such as Japan's USD 12 billion annual burden tied to unmanaged menopausal symptoms, nudge healthcare payers and employers toward proactive hormone care programs. Integrated longevity initiatives in public health strategies are creating sustained demand that moves beyond symptom relief toward long-term preventive regimens.

Rapid Adoption of Bio-Identical Hormone Formulations

Clinical evidence shows micronized progesterone and estradiol combinations exhibit lower cardiometabolic and oncologic risk than earlier conjugated equine estrogens, enabling 20-30% premium pricing and faster uptake among health-conscious mid-life women. TherapeuticsMD's BIJUVA approval set a regulatory benchmark and, with patent protection to 2032, provides a defensible niche for innovators. Capacity expansion through acquisitions, exemplified by Biote's purchase of 503B compounding facilities, secures supply while standardizing quality.

Cancer-Risk Perception After WHI & Follow-Up Studies

Though 21-year follow-up data indicate estrogen-only regimens reduce breast cancer incidence by 23% and mortality by 40%, the original 2002 WHI headlines still shape public opinion. Recent FDA boxed warnings, such as that applied to non-hormonal fezolinetant, keep safety debates visible and complicate physician messaging. Professional societies have updated positions to allow therapy beyond age 65 with individualized counseling, yet broad adoption hinges on continuous educational outreach.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Tele-Health BHRT Subscription Models

- Pipeline of Micro-Dosed & Tissue-Selective SERMs/SARMs

- High Lifetime Therapy Cost & Lack of Generic Bio-Identicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Estrogen products retained 42.56% of 2024 revenue, underlining their central position in the hormone replacement therapy market. The parathyroid segment, however, is charting an 8.51% CAGR through 2030 as newer indications surface, pushing the hormone replacement therapy market size toward diversified growth corridors. Specialized products such as YORVIPATH for chronic hypoparathyroidism command premium pricing and underscore the shift from broad symptom control to targeted organ support.

Precision-oriented pipelines pair micro-dosed estrogens with tissue-selective modulators to serve nuanced patient profiles. Companies with multi-hormone portfolios are well positioned, whereas single-product players risk share attrition. Testosterone demand is dampened by heightened cardiovascular labeling while growth hormone continues steady uptake among longevity-focused consumers.

Oral regimens held 40.34% share in 2024 and remain widely prescribed owing to convenience. Transdermal patches and gels, buoyed by a 7.92% forecast CAGR, offer consistent plasma levels without first-pass metabolism, helping the hormone replacement therapy market transition toward personalized dosing. Novartis's Estradot micro-patch illustrates how miniaturized systems elevate compliance.

Long-acting injectables such as MIT's SLIM microcrystal technology hint at quarterly or semi-annual dosing horizons. Vaginal and intrauterine devices continue to address local genitourinary symptoms with minimal systemic exposure, adding breadth to delivery choices.

The Hormone Replacement Therapy Market Report is Segmented by Therapy (Estrogen, Growth Hormone, Thyroid, and More), Route of Administration (Oral, Parenteral, Transdermal, Vaginal/Intra-uterine, and More), Indication (Menopause, Hypothyroidism, and More), Distribution Channel (Hospital Pharmacy, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America sustained 38.63% share in 2024 owing to strong reimbursement frameworks, FDA guidance clarity, and an ecosystem that supports rapid telehealth scaling. Medicare's precedent on gender-affirming coverage signals how policy can unlock new segments. Generic estradiol gel approvals improve affordability, though upcoming patent expiries may pressure established brands.

Asia-Pacific is projected to grow at 7.41% CAGR through 2030. Rising urban incomes, aging populations, and shifting cultural perceptions on women's health underpin uptake, while corporate Japan quantifies menopause-related absenteeism at USD 12 billion annually, spurring employer-financed wellness offerings. Regulatory pilots in China for gender-affirming therapies and increasing Indian middle-class purchasing power collectively expand the hormone replacement therapy market footprint across the region.

Europe shows steady, guideline-driven demand yet faces cost-effectiveness scrutiny by health technology assessment bodies. Tough environmental rules on endocrine-active emissions influence production costs, with the European Medicines Agency mandating statewide monitoring ema. Emerging regions across the Middle East, Africa, and South America present growth runways but require localization strategies that align with diverse cultural and regulatory landscapes.

- Abbott Laboratories

- Bayer

- Eli Lilly and Company

- Roche

- Merck

- Mylan Viatris

- Novartis

- Novo Nordisk

- Pfizer

- Amgen

- Abbvie

- Hisamitsu Pharma

- Endo International

- TherapeuticsMD

- BioTE Medical

- Viatris

- Ascend Therapeutics

- Acerus Pharma

- Johnson & Johnson

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Post-Menopausal Population & Life-Expectancy Gains

- 4.2.2 Rapid Adoption of Bio-Identical Hormone Formulations

- 4.2.3 Expanding Tele-Health BHRT Subscription Models

- 4.2.4 Insurance Reimbursement Expansion for Transgender HRT

- 4.2.5 Pipeline Of Micro-Dosed & Tissue-Selective Serms / Sarms

- 4.2.6 Wearable Transdermal Patch Innovations & Long-Acting Injectables

- 4.3 Market Restraints

- 4.3.1 Cancer-Risk Perception After WHI & Follow-Up Studies

- 4.3.2 High Lifetime Therapy Cost & Lack of Generic Bio-Identicals

- 4.3.3 Patent-Cliff & Pricing Pressure on Legacy Estrogen Brands

- 4.3.4 Tightening Environmental Rules on Endocrine-Active Emissions

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy

- 5.1.1 Estrogen

- 5.1.2 Growth Hormone

- 5.1.3 Thyroid

- 5.1.4 Testosterone

- 5.1.5 Parathyroid

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Parenteral

- 5.2.3 Transdermal

- 5.2.4 Vaginal/Intra-uterine

- 5.2.5 Implantable Pellets

- 5.3 By Indication

- 5.3.1 Menopause

- 5.3.2 Hypothyroidism

- 5.3.3 Growth Hormone Deficiency

- 5.3.4 Other Indications

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacy

- 5.4.2 Retail Pharmacy

- 5.4.3 Online/Direct-to-Consumer Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Bayer AG

- 6.3.3 Eli Lilly and Company

- 6.3.4 F. Hoffmann-La Roche

- 6.3.5 Merck KGaA

- 6.3.6 Mylan Viatris

- 6.3.7 Novartis AG

- 6.3.8 Novo Nordisk A/S

- 6.3.9 Pfizer Inc.

- 6.3.10 Amgen Inc.

- 6.3.11 AbbVie Inc.

- 6.3.12 Hisamitsu Pharma

- 6.3.13 Endo International

- 6.3.14 TherapeuticsMD

- 6.3.15 BioTE Medical

- 6.3.16 Viatris Inc.

- 6.3.17 Ascend Therapeutics

- 6.3.18 Acerus Pharma

- 6.3.19 Johnson & Johnson (Janssen)

- 6.3.20 Teva Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment