|

시장보고서

상품코드

1848070

3D 세포 배양 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)3D Cell Culture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

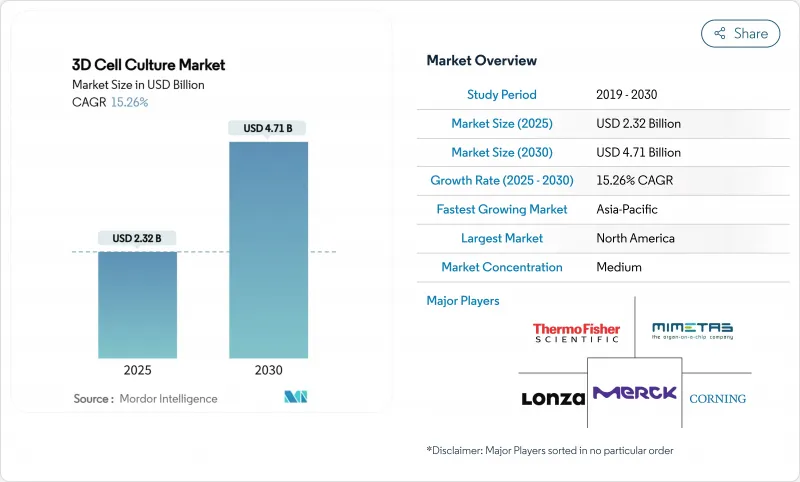

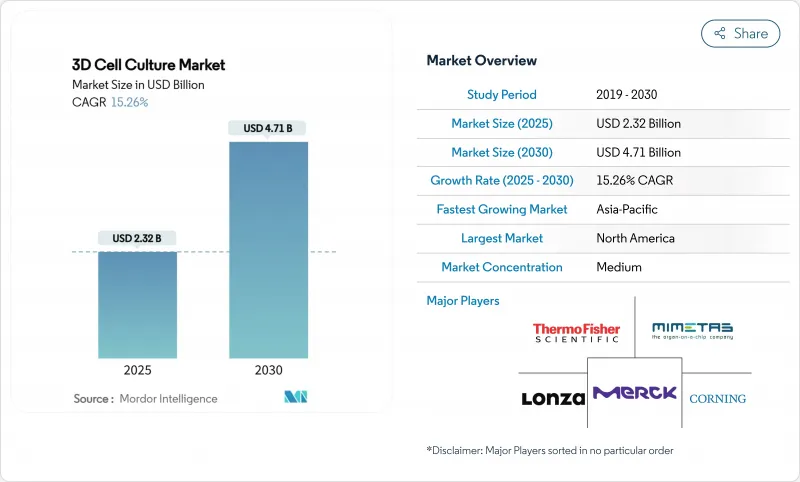

3D 세포 배양 시장 규모는 2025년에 23억 2,000만 달러로 평가되었고, 2030년에 47억 1,000만 달러에 이를 것으로 예측되며, 2025-2030년의 CAGR은 15.26%를 나타낼 전망입니다.

북미는 풍부한 제약 파이프라인, 풍부한 벤처 자금, FDA의 비동물 실험 장려로 리더십을 유지하고 있습니다. 아시아태평양 지역은 정부가 생명공학을 국가 산업 정책에 포함시키고 전환의학 클러스터를 확장함에 따라 가장 가파른 성장세를 보이고 있습니다. 턴키 프로토콜 덕분에 스캐폴드 기반 형식이 여전히 주류를 이루고 있지만, 신뢰할 수 있는 독성 스크리닝에 필수적인 조직 간 교신과 유동 기반 전단력을 재현하는 마이크로플루이딕 장기-온-칩 장치가 가장 빠르게 확장 중입니다. 이미지 분석과 다중 오믹스 판독을 자동화하는 인공지능 부가 기능은 3D 배양 시스템을 고함량 발견 엔진으로 전환하며, 실험실과 임상 사이의 역사적 데이터 격차를 해소하고 있습니다.

세계의 3D 세포 배양 시장 동향 및 인사이트

후기 단계 약물 실패를 줄이기 위한 생리학적 관련성 높은 전임상 모델 수요 확대

2상 및 3상에서 약물 후보의 90%가 탈락함에 따라 예측 정확도는 R&D의 필수 요소가 되었습니다. 세포외 기질 강성, 산소 농도 구배 및 다세포 상호작용을 재현하는 3차원 조직은 2차원 배지에서 종종 놓치는 독성 지표를 제공합니다. FDA 현대화법 3.0은 이제 비동물 데이터 기반 신약 임상시험 신청을 허용하여 기업 검증 주기를 가속화합니다. 바이오프린팅된 환자 유래 오가노이드는 반응자와 비반응자의 실시간 계층화를 가능케 하여 비용이 많이 드는 임상시험 재설계를 줄입니다. 간-온-칩 배열을 도입한 제약사들은 2024년 제출된 후보물질 중 간독성 관련 철회 사례가 30% 감소했다고 보고했습니다. 이러한 개선들은 임상 위험을 축소하고 첨단 배양 플랫폼에 대한 초기 투자 확대를 정당화합니다.

재생의학 및 맞춤형 의학에 대한 글로벌 투자 확대, 3D 배양 기술 도입 가속화

재생 치료제에 투입된 민간 및 공공 자본은 2025년 전 세계적으로 300억 달러를 초과했으며, 이 중 35%가 조직공학 툴킷에 배정되었습니다. 자가 이식편은 환자 맞춤형 미세환경을 요구하기 때문에 기업들은 면역 호환성 이식편 제작을 위해 3D 바이오 프린팅과 유도 만능 줄기세포를 통합하고 있습니다. 중국 국가자연과학기금회는 하이드로겔 기반 장기 패치 연구 지원금을 두 배로 증액하며 국내 바이오잉크 공급업체를 촉진하고 있습니다. CRISPR 편집 장기유사체에 대한 병행 투자는 한때 치료 불가능하다고 여겨졌던 단일 유전자 질환에 대한 전임상 설계도를 창출 중입니다. 이러한 전환적 워크플로는 맞춤형 스캐폴드 화학 및 관류형 바이오리액터에 의존하며, 3D 배양 하드웨어를 정밀의학 가치 사슬의 핵심에 내재화하고 있습니다.

고급 3D 문화 플랫폼과 기존 2D 시스템의 높은 자본 비용과 운영 비용

상용 유동 제어형 장기-온-칩 장비는 8만-15만 달러로, 1만5천 달러의 스택형 2D 인큐베이터 진입 가격을 압도합니다. 마이크로플루이딕 펌프, 인라인 센서, 다중 이미지 캡처 기능이 추가되면 운영 비용은 더욱 증가합니다. 소규모 연구소는 업그레이드를 미루는 경향이 있어 남미와 아프리카 지역의 보급률이 제한됩니다. 제조사들은 데스크탑 스테레오리소그래피 프린터로 제작된 모듈형 칩으로 대응하며, 실행당 비용을 35% 절감하고 있습니다. 광경화성 수지 대량 공급 계약과 오픈소스 제어 소프트웨어는 소유 비용을 절감하며, 많은 실험실에서 두 번의 예산 주기 내에 제약 요인을 상쇄할 수 있습니다.

부문 분석

스캐폴드 플랫폼은 2024년 3D 세포 배양 시장 점유율의 48.9%를 차지했으며, 세포외 기질 모방이 필요한 장기 배양에 여전히 필수적입니다. 이 기존 카테고리는 수십 년간 발표된 프로토콜의 혜택을 받아 규제된 품질 시스템 내에서 검증이 용이했습니다. 그러나 마이크로플루이딕 장기-온-칩 하위 부문은 층류 흐름, 실시간 이미징 창, 다중 장기 네트워킹을 통한 전환적 약동학 구현 능력으로 18.9%의 연평균 성장률(CAGR)을 기록하며 모든 경쟁사를 앞지르고 있습니다. 공급업체들은 연동 펌프가 필요 없는 중력 유동 및 자기 결합 밸브를 통합하여 유지보수 중단 시간을 단축하고 실험 재현성을 높이고 있습니다. 클라우드 연결 센서가 대사 유동을 머신러닝 모델로 스트리밍하여 원시 이미지를 며칠이 아닌 몇 분 만에 용량-반응 곡선으로 변환하는 기술이 추가 동력을 제공합니다. 이 효율성은 공격적인 마일스톤 일정에 압박받는 연구팀의 공감을 얻으며, 정적 하이드로겔 삽입체 대체를 촉진하고 있습니다. 비용이 하락함에 따라 마이크로플루이딕스 기반 3D 세포 배양 시장 규모는 2029년까지 2024년 기준 대비 두 배로 성장할 전망이며, 이는 모든 스캐폴드 수요를 잠식하지 않을 것입니다. 하이브리드 프로토콜이 칩 내부에 하이드로겔 액적들을 혼합하여 기질 구획을 모방하기 때문입니다.

비스캐폴드 구상체 생성기는 음향 또는 자기력을 활용해 세포 집합체를 조립하며, 384웰 처리량이 필요한 고처리량 스크리닝 그룹에 매력적입니다. 한때 엔지니어링 부서에 국한되었던 3D 바이오프린팅 워크스테이션은 이제 GMP 등급 인클로저와 함께 출고되어 상업적 자가 조직 제조를 위한 기술로 자리매김하고 있습니다. 관류 센서와 결합된 바이오리액터는 세포 치료제 제조를 목표로 하는 밀리리터 규모 조직 구조물에 필요한 균일한 영양분 농도 구배를 제공합니다. 풀스택 모델 설계, 검증 및 데이터 해석 서비스를 제공하는 업체들은 처리 속도와 분자 주석의 깊이로 경쟁하며, 이는 내부 역량이 부족한 소규모 바이오테크 기업들에게 공감을 얻는 차별화 요소입니다. 이러한 기술적 진보는 종합적으로 접근 가능한 사용자 기반을 확대하고 3D 배양을 탐색적 부가 기능이 아닌 필수 요소로 확고히 자리매김하게 합니다.

지역 분석

북미는 2024년 전 세계 매출의 42%를 차지했으며, 이는 NIH(미국 국립보건원)의 전환 연구 지원금, 벤처 캐피털의 풍부한 자금, 비동물 데이터에 대한 FDA(미국 식품의약국)의 신속 승인 절차에 힘입은 결과입니다. 미국 실험실은 지역 매출의 85%를 차지했으며, 특히 장기 칩 혁신 기업과 시퀀싱 서비스 제공업체가 집중된 매사추세츠 및 캘리포니아 클러스터에서 두드러졌습니다. 캐나다와 멕시코는 바이오테크 인큐베이터 자금 풀을 확대하여 사용자 접근성을 넓히고 소모품 수입 흐름을 보완했습니다.

유럽은 엄격한 동물 실험 금지 조치와 대체 방법 전용 호라이즌 유럽(Horizon Europe) 보조금을 통해 성장을 공고히 하며 2위를 차지했습니다. 독일의 프라운호퍼 연구소(Fraunhofer institutes)와 영국의 캐터펄트 센터(Catapult centers)는 중소기업과 협력하여 근골격계 장애 파이프라인을 해결하는 혈관화 뼈 모델을 상용화하고 있습니다. 규제 기관들은 표준 개발 기관과 협력하여 검증 프레임워크를 조화시켜 국경을 초월한 연구 비교를 용이하게 하고 수요 신뢰도를 강화하고 있습니다.

아시아태평양 지역은 중국, 일본, 한국이 3D 배양 기술을 국가 정밀의학 로드맵에 통합함에 따라 16.8%라는 가장 빠른 연평균 복합 성장률(CAGR)을 기록하고 있습니다. 중국 과학기술부는 국가 핵심 연구소에서 장기-온-칩 시범 사업을 지원하며, 일본 컨소시엄은 신경퇴행성 질환을 위한 뇌-온-칩 솔루션을 목표로 합니다. 인도 과학산업연구위원회는 수입 의존도를 낮추기 위해 자국 하이드로겔 스타트업에 자금을 지원합니다. 한편 중동, 아프리카, 남미 지역에서는 대학병원 주변에 학계-산업 클러스터가 형성되며 초기 단계이지만 주문량이 증가하고 있습니다. 브라질은 새로운 화장품 규제에 부합하기 위해 피부 독성 시험에 중점을 둔 3D 바이오 프린팅 센터에 자금을 지원합니다. 확대되는 글로벌 영향력은 지역별 시장 규모를 증대시키고 해당 기술을 주류 채택 주기로 진입시키는 역할을 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 후기 단계 약물 실패를 줄이기 위한 생리학적 관련성 높은 전임상 모델 수요 확대

- 재생의학 및 맞춤형 의학에 대한 글로벌 투자 증가로 가속화되는 3D 배양 기술 도입

- 화장품 및 제약 분야에서 동물 실험 대체를 위한 규제 및 윤리적 압박 강화

- 상업적 규모의 3D 생산을 가능케 하는 스캐폴드 재료 및 바이오잉크의 급속한 발전

- 임상 적용 기간 단축을 위한 턴키 방식 3D 모델을 위한 제약-CRO 협력

- 시장 성장 억제요인

- 기존 2D 시스템 대비 고급 3D 배양 플랫폼의 높은 자본 및 운영 비용

- 밸리데이션과 재현성을 위한 통일된 세계의 표준 부족

- 신흥 지역의 전문 기술 인력 부족

- 규제 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기술별

- 스캐폴드 기반 플랫폼

- 마이크로 패턴 표면 마이크로플레이트

- 하이드로겔(천연, 합성, 하이브리드)

- ECM 유래 스캐폴드

- 다공성 마이크로캐리어

- 비스캐폴드 플랫폼

- 행잉 드롭 플레이트

- 자기 부상 스페로이드

- 마이크로플루이딕 장기-온-칩

- 3D 바이오리액터(스피너, 관류, 회전벽)

- 3D 바이오 프린팅 시스템과 시약

- 서비스(맞춤형 분석법 개발, 아웃소싱 모델)

- 스캐폴드 기반 플랫폼

- 용도별

- 암 연구 및 항암제 스크리닝

- 줄기세포 연구 및 조직 공학

- 신약 개발 및 독성학 스크리닝

- 재생 의학 및 맞춤형 치료제

- 기타 용도(바이러스학, 화장품 안전성)

- 최종 사용자별

- 생명공학 및 제약회사

- 학술기관 및 연구기관

- 계약연구기관 및 CDMO

- 병원 및 진단센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Corning Incorporated

- Merck KGaA

- Lonza Group AG

- Sartorius AG

- Becton Dickinson & Co.

- InSphero AG

- MIMETAS BV

- CN Bio Innovations Ltd.

- BiomimX SRL

- Hurel Corporation

- Nortis Inc.

- PromoCell GmbH

- Kirkstall Ltd.

- TissUse GmbH

- Synthecon Inc.

- QGel SA

- Prellis Biologics Inc.

- Advanced Solutions Life Sciences

- CELLINK AB

제7장 시장 기회와 전망

HBR 25.11.10The 3D cell culture market size is valued at USD 2.32 billion in 2025 and is forecast to reach USD 4.71 billion by 2030, progressing at a 15.26% CAGR during 2025-2030.

North America sustains leadership because of deep pharmaceutical pipelines, abundant venture funding and FDA encouragement of non-animal assays. Asia-Pacific shows the steepest trajectory as governments embed biotechnology in national industrial policies and expand translational medicine clusters. Scaffold-based formats still dominate because of turnkey protocols, yet microfluidic organ-on-chip devices are scaling fastest as they reproduce tissue-tissue crosstalk and flow-driven shear essential for reliable toxicity screening. Artificial-intelligence add-ons that automate image analytics and multi-omics readouts are turning 3D culture systems into high-content discovery engines, closing historic data gaps between bench and clinic.

Global 3D Cell Culture Market Trends and Insights

Expanding Demand for Physiologically Relevant Pre-clinical Models to Cut Late-Stage Drug Failures

The 90% attrition of drug candidates at phase II and phase III has made predictive fidelity an R&D imperative. Three-dimensional tissues that recapitulate extracellular matrix stiffness, oxygen gradients and multicellular interactions yield toxicity signatures frequently missed in 2D plates. FDA Modernization Act 3.0 now permits investigational new drug submissions anchored on non-animal data, accelerating corporate validation cycles. Bioprinted patient-derived organoids allow real-time stratification of responders and non-responders, reducing costly trial redesigns. Pharmaceutical teams that deployed liver-on-chip arrays reported a 30% drop in candidate withdrawal related to hepatotoxicity in 2024 filings. Together these improvements shrink clinical risk and justify higher up-front spending on advanced culture platforms.

Escalating Global Investment in Regenerative & Personalized Medicine Accelerating 3D Culture Uptake

Private and public capital directed to regenerative therapeutics exceeded USD 30 billion globally in 2025, with 35% earmarked for tissue-engineering toolkits. Because autologous implants demand patient-specific microenvironments, companies integrate 3D bioprinting with induced pluripotent stem cells to fabricate immune-compatible grafts. China's National Natural Science Foundation doubled grants for hydrogel-based organ patches, spurring domestic suppliers of bioinks. Parallel investments in CRISPR-edited organoids are creating pre-clinical blueprints for single-gene disorders once deemed untreatable. These translational workflows rely on customizable scaffold chemistries and perfusion bioreactors, embedding 3D culture hardware into the core of precision-medicine value chains.

High Capital & Operating Costs of Advanced 3D Culture Platforms vs. Conventional 2D Systems

Commercial flow-controlled organ-on-chip rigs list between USD 80,000 and USD 150,000, dwarfing the USD 15,000 entry point for stackable 2D incubators. Operating outlays rise further once microfluidic pumps, inline sensors and multiplex image capture are included. Smaller institutes postpone upgrades, limiting regional penetration in South America and Africa. Manufacturers are responding with modulable chips produced on desktop stereolithography printers, slicing per-run costs by 35%. Bulk supply agreements for photo-curable resins and open-source control software reduce ownership expenses and could neutralize the restraint within two budget cycles for many labs.

Other drivers and restraints analyzed in the detailed report include:

- Intensifying Regulatory & Ethical Pressure to Replace Animal Testing in Cosmetics and Pharma

- Rapid Advances in Scaffold Materials & Bioinks Enabling Commercial-Scale 3D Production

- Lack of Harmonized Global Standards for Validation & Reproducibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Scaffold platforms held a 48.9% slice of the 3D cell culture market share in 2024 and remained indispensable for long-term cultures that require extracellular-matrix mimicry. This legacy category benefited from decades of published protocols, which made validation straightforward inside regulated quality systems. Yet the microfluidic organ-on-chip sub-segment is outpacing all rivals with an 18.9% CAGR tied to its capacity for laminar flow, real-time imaging windows and multi-organ networking that unlock translational pharmacokinetics. Vendors are integrating peristaltic-pump-free gravity flow and magnetically coupled valves, trimming maintenance downtime and increasing experiment reproducibility. Further momentum stems from cloud-connected sensors that stream metabolic flux to machine-learning models, turning raw images into dose-response curves in minutes rather than days. This efficiency resonates with discovery teams pressured by aggressive milestone timelines, encouraging substitution away from static hydrogel inserts. As costs fall, the 3D cell culture market size for microfluidics is projected to double its 2024 baseline before 2029 without cannibalizing all scaffold demand, because hybrid protocols mix hydrogel droplets within chips to simulate stromal compartments.

Scaffold-free spheroid generators leverage acoustic or magnetic forces to assemble cellular aggregates, appealing to high-throughput screening groups that need 384-well throughput. 3D bioprinting workstations, once confined to engineering departments, now ship with GMP-grade enclosures, positioning the technology for commercial autologous tissue fabrication. Bioreactors married to perfusion sensors deliver homogeneous nutrient gradients required for milliliter-scale tissue constructs aimed at cell-therapy manufacturing. Service providers offering full-stack model design, validation, and data interpretation compete on turnaround speed and depth of molecular annotation, a differentiation that resonates with small biotech firms with lean internal capacities. Collectively, these technological advances expand the addressable user base and cement 3D culture as a staple rather than an exploratory add-on.

The 3D Cell Culture Market Report is Segmented by Technology (Scaffold-Based Platforms, Scaffold-Free Platforms, Microfluidics-Based Organ-On-Chip Systems, and More), Application (Cancer Research & Oncology Drug Screening, and More), End User (Biotechnology & Pharmaceutical Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 42% of global revenue in 2024, supported by NIH translational grants, venture-capital depth and expedited FDA pathways for non-animal data. United States laboratories accumulated 85% of regional turnover, particularly within Massachusetts and California clusters that concentrate organ-chip innovators and sequencing providers. Canada and Mexico increased funding pools for biotech incubators, broadening user access and supplementing import flows of consumables.

Europe ranked second and fortified growth through stringent animal-testing bans and Horizon Europe grants earmarked for alternative methods. Germany's Fraunhofer institutes and the United Kingdom's Catapult centers collaborate with SMEs to commercialize vascularized bone models that tackle musculoskeletal-disorder pipelines. Regulators collaborate with standard-development bodies to harmonize validation frameworks, smoothing cross-border study comparisons and reinforcing demand confidence.

Asia-Pacific logs the fastest CAGR at 16.8% as China, Japan and South Korea integrate 3D culture into national precision-medicine roadmaps. China's Ministry of Science and Technology subsidizes organ-on-chip pilots in state key laboratories, while Japanese consortia target brain-on-chip solutions for neurodegeneration. India's Council of Scientific and Industrial Research sponsors indigenous hydrogel startups to cut import dependency. Elsewhere, the Middle East, Africa and South America register nascent but rising orders as academic-industry clusters form around university hospitals. Brazil funds 3D bioprinting centers focused on dermal toxicity tests to align with new cosmetic regulations. The growing global footprint magnifies the 3D cell culture market size in regional breakouts and propels the technology into mainstream adoption cycles.

- Thermo Fisher Scientific

- Corning

- Merck

- Lonza Group

- Sartorius

- Becton Dickinson & Co.

- InSphero

- Mimetas

- CN Bio Innovations Ltd.

- BiomimX

- Hurel

- Nortis

- PromoCell

- Kirkstall Ltd.

- TissUse

- Synthecon Inc.

- QGel SA

- Prellis Biologics Inc.

- Advanced Solutions Life Sciences

- CELLINK AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Demand for Physiologically Relevant Pre-clinical Models to Cut Late-Stage Drug Failures

- 4.2.2 Escalating Global Investment in Regenerative & Personalized Medicine Accelerating 3D Culture Uptake

- 4.2.3 Intensifying Regulatory & Ethical Pressure to Replace Animal Testing in Cosmetics and Pharma

- 4.2.4 Rapid Advances in Scaffold Materials & Bioinks Enabling Commercial-Scale 3D Production

- 4.2.5 Pharma-CRO Partnerships for Turn-Key 3D Models Shortening Time-to-Clinic

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs of Advanced 3D Culture Platforms vs. Conventional 2D Systems

- 4.3.2 Lack of Harmonized Global Standards for Validation & Reproducibility

- 4.3.3 Scarcity of Specialized Technical Talent in Emerging Regions

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Scaffold-based Platforms

- 5.1.1.1 Micropatterned Surface Microplates

- 5.1.1.2 Hydrogels (Natural, Synthetic, Hybrid)

- 5.1.1.3 ECM-Derived Scaffolds

- 5.1.1.4 Porous Microcarriers

- 5.1.2 Scaffold-free Platforms

- 5.1.2.1 Hanging Drop Plates

- 5.1.2.2 Magnetic Levitated Spheroids

- 5.1.3 Microfluidics-based Organ-on-Chip Systems

- 5.1.4 3D Bioreactors (Spinner, Perfusion, Rotating-Wall)

- 5.1.5 3D Bioprinting Systems & Reagents

- 5.1.6 Services (Custom Assay Development, Outsourced Models)

- 5.1.1 Scaffold-based Platforms

- 5.2 By Application

- 5.2.1 Cancer Research & Oncology Drug Screening

- 5.2.2 Stem Cell Research & Tissue Engineering

- 5.2.3 Drug Discovery & Toxicology Screening

- 5.2.4 Regenerative Medicine / Personalized Therapeutics

- 5.2.5 Other Applications (Virology, Cosmetics Safety)

- 5.3 By End User

- 5.3.1 Biotechnology & Pharmaceutical Companies

- 5.3.2 Academic & Research Institutes

- 5.3.3 Contract Research Organizations & CDMOs

- 5.3.4 Hospitals & Diagnostic Centers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Corning Incorporated

- 6.3.3 Merck KGaA

- 6.3.4 Lonza Group AG

- 6.3.5 Sartorius AG

- 6.3.6 Becton Dickinson & Co.

- 6.3.7 InSphero AG

- 6.3.8 MIMETAS BV

- 6.3.9 CN Bio Innovations Ltd.

- 6.3.10 BiomimX SRL

- 6.3.11 Hurel Corporation

- 6.3.12 Nortis Inc.

- 6.3.13 PromoCell GmbH

- 6.3.14 Kirkstall Ltd.

- 6.3.15 TissUse GmbH

- 6.3.16 Synthecon Inc.

- 6.3.17 QGel SA

- 6.3.18 Prellis Biologics Inc.

- 6.3.19 Advanced Solutions Life Sciences

- 6.3.20 CELLINK AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment