|

시장보고서

상품코드

1848108

광견병 백신 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Rabies Vaccine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

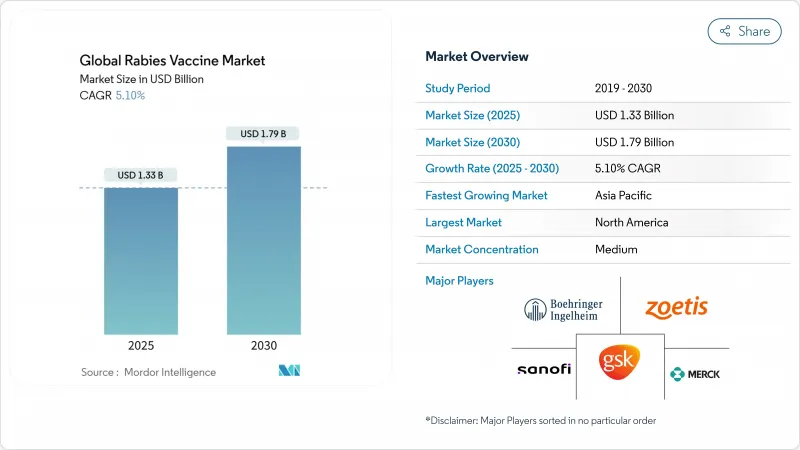

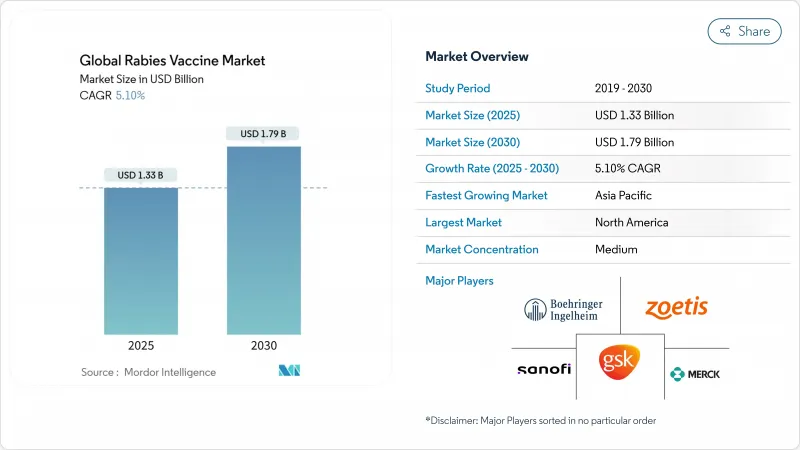

광견병 백신 시장 규모는 2025년 13억 3,000만 달러로 평가되었고, 2030년 17억 9,000만 달러에 이를 것으로 예측되며, CAGR은 5.1%를 나타낼 전망입니다.

성장은 WHO 주도의 ‘30년까지 제로(Zero by 30)’ 캠페인을 통해 확보된 다자간 자금과 신경조직에서 첨단 세포 배양 및 mRNA 플랫폼으로의 기술 전환에 기반하며, 이 두 요소가 결합되어 생산 효율성을 높이고 안전성 프로파일을 개선합니다. 가비(Gavi)가 2024년 50개 이상의 적격 국가에서 인간 노출 후 예방(PEP)을 지원하기로 결정하면서, 가장 부담이 큰 지역의 접근성 장벽을 낮춤으로써 수요가 급격히 확대될 전망입니다. 한편 아시아와 아프리카에서 증가하는 유기견 밀도는 대응적 백신 수요를 지속시키는 반면, 북미와 유럽의 반려동물 소유 증가로 예방적 접종이 확대되고 있습니다. 충진 및 완제 생산 능력 부족과 취약한 콜드체인 네트워크로 공급 부족이 지속되면서 비용 효율적인 아시아 신규 진입업체의 기회가 열리고 있습니다. 사노피의 후기 mRNA 후보물질 SP0087은 2025년 하반기 미국 및 EU 허가 신청을 목표로 하며, 프리미엄 시장 가속화와 경쟁사 대응을 촉진할 수 있습니다.

세계의 광견병 백신 시장 동향 및 인사이트

세계의 ‘30년까지 제로(Zero by 30)’ 광견병 퇴치 이니셔티브, 다자간 자금 지원 확대

2030년까지 개 매개 인간 광견병 사망을 종식시키려는 WHO 주도 목표는 장기적 백신 수요를 보장하는 전례 없는 다자간 자금 흐름을 창출했습니다. 가비(Gavi)는 현재 50개 이상의 대상국에서 노출 후 예방접종을 지원하며 저소득 환경의 최대 접근성 장벽을 제거하고 있습니다. 이 프레임워크 하에 마련된 대량 입찰은 제조사에게 미래 물량에 대한 가시성을 제공하여 생산 능력 확장을 촉진합니다. 프로그램과 함께 도입된 통합 물림 사례 관리 도구는 감시 체계를 개선하여 수요 예측을 정밀화하고 낭비를 줄입니다. 이러한 요소들이 결합되어 이전에는 예측 불가능했던 인도적 구매를 안정적인 상업적 공급망으로 전환합니다.

신경 조직에서 첨단 세포 배양 및 mRNA 플랫폼으로의 이동 안전성 및 보급률 향상

제조사들은 신경조직 기반 백신을 단계적으로 폐지하고, 더 높은 효능과 우수한 안전성 기록을 제공하는 베로 세포(Vero), BHK 세포, mRNA 기술로 전환하고 있습니다. mRNA 후보 백신은 동물 모델에서 단 두 차례 접종만으로 완전한 보호 효과를 보여주어 환자 순응도를 높이고 프로그램 비용을 절감합니다. 중국에서 검토 중인 무혈청 생산 방식은 동물 혈청 관련 위험을 제거하고 품질에 민감한 시장에서 프리미엄 가격 책정을 가능하게 합니다. 현탁 배양을 통한 높은 수율은 1회 투여당 비용을 절감하여 공공 입찰에서도 첨단 플랫폼의 경쟁력을 높입니다. 이러한 변화들은 종합적으로 공급 확대, 신뢰 증진, 투여량 절감 일정의 가능성을 열어줍니다.

한정된 콜드체인 및 의료 인프라로 인한 풍토병 지역 농촌 지역 배급 제약

안정적인 전력 공급 부재로 인해 여러 아프리카 및 남아시아 국가에서 원격 진료소에 도달하기 전에 최대 30%의 백신이 손상되어 부족한 공중보건 예산을 낭비하고 있습니다. WHO의 백신 혁신 우선순위 전략은 현재 내열성 광견병 제형을 최우선 필요 기술로 지정하여, 향후 입찰에서 최소 3일간 40°C 온도 변동을 견딜 수 있는 제품에 대한 선호도를 시사합니다. 2024년 도입된 초저온 보로실리케이트 바이알을 활용한 현장 시범 연구는 비포장 도로에서 오토바이로 진행되는 최종 배송 단계에서 파손률을 70% 감소시켰습니다. 저장 시설이 있더라도 진료소에는 보정된 온도 모니터링 장비가 부족한 경우가 많아 배치별 품질 불확실성이 발생합니다. 이는 의료진의 신뢰를 약화시키고 수요를 위축시킵니다. 현재 후기 개발 단계에 있는 내열성 인간 광견병 면역글로불린(HRIG)은 엄격한 2-8°C 취급 요건을 없애 물류 부담을 추가로 완화할 수 있으나, 상업적 출시 시점은 2027년 이전으로 예상되지 않습니다.

부문 분석

베로 세포 부문은 2024년 광견병 백신 시장 점유율의 55.0%를 차지합니다. 강력한 항원 회수율과 99.99%의 숙주 DNA 제거율은 신뢰할 수 있는 안전성 기준을 제공하며, 무혈청 현탁 배양은 수율을 5.2 X 10^7 FFU/mL까지 끌어올립니다. 신흥 mRNA 및 BHK 제품이 연평균 10% 성장함에 따라 제조사들은 포트폴리오를 다각화하여 경쟁력을 유지하고 있습니다. 지속적인 공정 고도화로 베로 세포 공장은 틈새 프리미엄 부문이 가속화되는 상황에서도 생산량을 방위할 수 있습니다.

기타 제품 유형이 가장 빠르게 성장하는 클러스터를 형성합니다. mRNA 후보물질은 2회 접종 일정, 소규모 배치, 부족 시 신속한 확장성을 약속하며 향후 입찰 기준과 부합합니다. AIM Vaccine은 2025년 규제 당국에 최초의 무혈청 인간 광견병 백신을 제출하여 중상위 소득 시장에서의 경쟁 확대를 예고했습니다. 이러한 혁신으로 2030년까지 비베로(Vero) 기반이 아닌 광견병 백신 시장 규모가 4억 달러를 넘어설 전망입니다.

2024년 광견병 백신 시장의 78.0%를 PEP(사후노출 예방접종)가 차지합니다. WHO의 1주 간 피내접종 프로토콜은 준수율을 높여: 접종자의 87%가 1년 후에도 보호 항체 역가를 유지합니다. 현재 임상 적용 단계에 진입한 단일클론 항체 조합은 부작용을 줄이고 효능을 표준화하여 PEP의 임상적 우위를 강화합니다.

여행 수요 회복과 직업별 지침 변경으로 PrEP 시장은 연평균 6.8% 성장률을 기록 중입니다. CDC는 이제 2회 접종 PrEP 시리즈를 권장하여 비용과 진료 방문 횟수를 줄였습니다. 부스터 접종 간격이 길어짐에 따라 광견병 백신 업계는 수의사, 실험실 직원, 모험 여행객을 대상으로 한 고용주 지원 프로그램에서 새로운 기회를 모색하고 있습니다.

지역 분석

북미는 엄격한 규제 감독과 광범위한 보험 적용으로 2024년 광견병 백신 시장의 41% 점유율을 유지할 전망입니다. 캐나다 예방접종 지침은 수의사 및 실험실 종사자에게 위험 기반 접종 요법을 의무화하여 꾸준한 기본 접종률을 촉진합니다. 브라운스빌의 무료 2025 클리닉과 같은 지역사회 프로그램은 공평한 접근성을 강화합니다.

아시아태평양 지역은 6.5%의 가장 빠른 지역 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 인도 및 중국은 현재 연간 10억 회분 이상의 백신을 공급하며 지역 수요의 85% 이상을 자체 조달합니다. 중국의 광견병 백신 시장 규모는 도시 반려동물 소유 증가와 현지 혁신 파이프라인을 바탕으로 2030년까지 148억 위안(20억 6,000만 달러)을 넘어설 전망입니다. 무혈청 및 복합 제형이 이 환경에서 초기 채택자가 될 것으로 예상됩니다.

유럽, 중동 및 아프리카, 남미는 다양한 기회를 형성합니다. 유럽에서는 바바리안 노르딕의 라비푸르/라바버트가 2024년 판매 기대치를 초과하며 프리미엄 수요의 탄력성을 입증했습니다. 아프리카 연합의 PAVM 같은 이니셔티브는 금융 및 기술 이전을 통한 현지 생산 확대를 목표로 하여 장기적인 공급 측면 변화를 예고합니다. 남미는 지속적인 진전을 보여줍니다. 개를 매개로 한 인간 감염 사례는 1983년 이후 98% 감소했으나, 정부들은 여전히 80% 이상의 접종률을 유지하기 위해 개 대상 캠페인을 최우선으로 삼고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 「Zero by 30」이니셔티브로 다자간 자금 지원 확대

- 신경 조직에서 첨단 세포 배양 및 mRNA 플랫폼으로의 전환으로 안전성 및 도입률 향상

- 신흥 경제국에서의 동물 물림 사고 증가 및 유기견 밀집도 상승으로 수요 지속

- 전 세계 반려동물 소유율 및 예방적 수의 의료비 지출 증가

- 확대된 정부 조달 및 기부자 지원 메커니즘으로 백신 접근성 개선

- 신기술(mRNA, 단일클론 항체) 분야의 강력한 R&D 파이프라인으로 대상 시장 확대

- 시장 성장 억제요인

- 한정된 콜드체인과 헬스 케어 인프라가 유행 지역의 지방 유통을 제한

- 전체 PEP 요법의 높은 총비용으로 인한 경제성 장벽

- 간헐적 공급 부족 및 생산 능력 제약으로 인한 글로벌 가용성 영향

- 복잡하고 가격 민감한 입찰 및 규제 절차로 인한 신종 백신 시장 진입 지연

- 가치/공급망 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 아기 햄스터 신장(BHK) 백신

- 정제 닭 배아 세포 광견병 백신

- 베로 세포 광견병 백신

- 기타 제품 유형

- 백신 접종 유형별

- 사전 노출 백신(PrEP/PEV)

- 사후 노출 예방(PEP)

- 최종 사용자별

- 인간

- 동물

- 유통 채널별

- 공중위생조달 및 집단 예방접종 프로그램

- 병원 및 여행 클리닉

- 동물병원

- 소매 및 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Sanofi SA

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Zoetis Inc.

- Boehringer Ingelheim International GmbH

- Pfizer Inc.

- Elanco Animal Health

- Virbac SA

- Bharat Biotech

- AIM Vaccine Co., Ltd.

- Chengdu Institute of Biological Products

- Indian Immunologicals Ltd.

- Kamada Ltd.

- Kedrion Biopharma Inc.

- CSL Behring

- Grifols SA

- Liaoning Cheng Da Co., Ltd.

- Shuanglin Bio-Pharmaceutical Co., Ltd.

제7장 시장 기회와 전망

HBR 25.11.10The rabies vaccine market size is valued at USD1.33 billion in 2025 and is forecast to reach USD1.79 billion by 2030, registering a 5.1% CAGR.

Growth rests on multilateral funding unlocked by the WHO-led "Zero by 30" campaign and on technology shifts from nerve-tissue to advanced cell-culture and mRNA platforms, which together lift production efficiency and improve safety profiles. Gavi's 2024 decision to finance human post-exposure prophylaxis (PEP) across more than 50 eligible countries sharply widens demand by lowering affordability barriers in the highest-burden regions[1]. Meanwhile, rising stray-dog density in Asia and Africa sustains reactive vaccination needs, even as companion-animal ownership in North America and Europe drives preventive uptake. Supply shortages persist because of limited fill-finish capacity and fragile cold-chain networks, creating space for cost-efficient Asian entrants. Sanofi's late-stage mRNA candidate SP0087, slated for US and EU filings in 2H 2025, could accelerate the premium segment and stimulate competitive responses.

Global Rabies Vaccine Market Trends and Insights

Global "Zero by 30" Rabies Elimination Initiative Boosting Multilateral Funding

The WHO-led goal of ending dog-mediated human rabies deaths by 2030 has unlocked unprecedented multilateral funding streams that guarantee long-term vaccine demand. Gavi now finances post-exposure prophylaxis in more than 50 eligible countries, removing the biggest affordability hurdle in low-income settings. Bulk tenders created under this framework give manufacturers better visibility into future volumes, encouraging capacity expansions. Integrated Bite Case Management tools rolled out with the program improve surveillance, which sharpens demand forecasts and cuts wastage. Together, these elements convert previously unpredictable humanitarian purchases into a stable commercial pipeline.

Shift from Nerve-Tissue to Advanced Cell-Culture & mRNA Platforms Enhancing Safety and Uptake

Manufacturers are phasing out nerve-tissue vaccines in favor of Vero, BHK, and mRNA technologies that deliver higher efficacy and better safety records. mRNA candidates show full protection in animal models with just two doses, which improves patient compliance and lowers program costs. Serum-free production under review in China eliminates animal serum risks and supports premium pricing in quality-sensitive markets. Higher yields from suspension cultures reduce per-dose cost, making advanced platforms attractive even for public tenders. These shifts collectively expand supply, enhance trust, and open doors to dose-sparing schedules.

Limited Cold-Chain & Healthcare Infrastructure Restricting Rural Distribution in Endemic Regions

The absence of reliable electricity means that up to 30% of vaccines spoil before reaching remote clinics in several African and South Asian countries, wiping out scarce public-health budgets. WHO's Vaccine Innovation Prioritisation Strategy now places thermostable rabies formulations in its top tier of needed technologies, signalling future tender preference for products that tolerate 40 °C excursions for at least three days. Pilot field studies with deep-cold borosilicate vials introduced in 2024 cut breakage rates by 70% during last-mile transport on motorcycles over unpaved roads. Even where storage exists, clinics often lack calibrated temperature monitoring, leading to batch-by-batch quality uncertainty that erodes clinician confidence and depresses demand. Thermostable human rabies immune globulin (HRIG) now in late-stage development could further ease logistics by eliminating strict 2-8 °C handling requirements, but commercial launch is not expected before 2027.

Other drivers and restraints analyzed in the detailed report include:

- Expanded Government Procurement & Donor Support Mechanisms Improving Vaccine Accessibility

- Robust R&D Pipeline in Novel Modalities (mRNA, Monoclonal Antibodies) Broadening Addressable Market

- High Total Cost of Full PEP Regimen Creating Affordability Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Vero Cell segment holds 55.0% of the rabies vaccine market share in 2024. Robust antigen recovery and 99.99% host-DNA removal deliver reliable safety benchmarks, while serum-free suspension culture pushes yields to 5.2 X 10^7 FFU/mL. As emerging mRNA and BHK products grow at 10% CAGR, manufacturers hedge portfolios to retain relevance. Continuous process intensification positions Vero Cell plants to defend volumes even as niche premium segments accelerate.

Other product types form the quickest-growing cluster. mRNA candidates promise two-dose schedules, smaller batch sizes, and rapid scalability during shortages, aligning with future tender criteria. AIM Vaccine filed the first serum-free human rabies vaccine with regulators in 2025, signalling wider competition in upper-middle-income markets. These innovations are likely to lift the rabies vaccine market size for non-Vero formats above USD400 million by 2030.

PEP accounts for 78.0% of the rabies vaccine market in 2024. WHO's 1-week intradermal protocol lifts compliance: 87% of recipients maintain protective antibody titres after 1 year. Monoclonal antibody combinations now entering practice cut adverse reactions and standardize potency, strengthening PEP's clinical edge.

PrEP grows at 6.8% CAGR as travel rebounds and occupational guidelines shift. CDC now endorses a 2-dose PrEP series, lowering cost and clinic visits. With longer booster intervals, the rabies vaccine industry sees new opportunities in employer-funded schemes for veterinarians, laboratory staff, and adventure tourists.

The Rabies Vaccine Market Report is Segmented by Product Type (Baby Hamster Kidney (BHK) Vaccine, and More), Vaccination Type (Pre-Exposure Vaccination (PrEP/PEV) and Post-Exposure Prophylaxis (PEP)), End-User (Humans and Animals), Distribution Channel (Public Health Procurement & Mass Immunization Programs, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 41% share of the rabies vaccine market in 2024, propelled by airtight regulatory oversight and widespread insurance coverage. Canada's Immunization Guide mandates risk-based regimens for veterinarians and laboratory workers, promoting steady baseline uptake. Community programs such as Brownsville's free 2025 clinic reinforce equitable access.

Asia Pacific records the fastest regional CAGR at 6.5%. India and China now deliver more than 1 billion vaccine doses annually and self-supply over 85% of regional demand. China's rabies vaccine market size is forecast to surpass RMB14.8 billion (USD 2.06 billion) by 2030 on the back of rising urban pet ownership and local innovation pipelines. Serum-free and combination formulations are expected to be early adopters in this environment.

Europe, Middle East & Africa, and South America form a diversified opportunity set. In Europe, Bavarian Nordic's Rabipur/RabAvert exceeded sales expectations in 2024, highlighting resilient premium demand. African Union initiatives such as PAVM aim to grow local manufacturing through finance and technology transfer, signalling long-run supply-side changes. South America showcases sustained progress: dog-transmitted human cases dropped 98% since 1983, yet governments still prioritize canine campaigns to maintain >=80% coverage.

- Sanofi

- GlaxoSmithKline

- Merck

- Zoetis

- Boehringer Ingelheim

- Pfizer

- Elanco

- Virbac

- Bharat Biotech

- AIM Vaccine Co., Ltd.

- Chengdu Institute of Biological Products

- Indian Immunologicals

- Kamada Ltd.

- Kedrion Biopharma

- CSL Behring

- Grifols

- Liaoning Cheng Da Co., Ltd.

- Shuanglin Bio-Pharmaceutical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global 'Zero by 30' Rabies Elimination Initiative Boosting Multilateral Funding

- 4.2.2 Shift from Nerve-Tissue to Advanced Cell-Culture & mRNA Platforms Enhancing Safety and Uptake

- 4.2.3 Escalating Animal-Bite Incidence & Stray-Dog Density in Emerging Economies Sustaining Demand

- 4.2.4 Rising Companion-Animal Ownership and Preventive Vet-Care Expenditure Worldwide

- 4.2.5 Expanded Government Procurement & Donor Support Mechanisms Improving Vaccine Accessibility

- 4.2.6 Robust R&D Pipeline in Novel Modalities (mRNA, Monoclonal Antibodies) Broadening Addressable Market

- 4.3 Market Restraints

- 4.3.1 Limited Cold-Chain & Healthcare Infrastructure Restricting Rural Distribution in Endemic Regions

- 4.3.2 High Total Cost of Full PEP Regimen Creating Affordability Barriers

- 4.3.3 Intermittent Supply Shortages & Manufacturing Capacity Constraints Impacting Global Availability

- 4.3.4 Complex, Price-Sensitive Tender and Regulatory Processes Delaying New Vaccine Market Entry

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Baby Hamster Kidney (BHK) Vaccine

- 5.1.2 Purified Chick Embryo Cell Rabies Vaccine

- 5.1.3 Vero Cell Rabies Vaccine

- 5.1.4 Other Product Types

- 5.2 By Vaccination Type

- 5.2.1 Pre-Exposure Vaccination (PrEP/PEV)

- 5.2.2 Post-Exposure Prophylaxis (PEP)

- 5.3 By End-User

- 5.3.1 Humans

- 5.3.2 Animals

- 5.4 By Distribution Channel

- 5.4.1 Public Health Procurement & Mass Immunization Programs

- 5.4.2 Hospitals & Travel Clinics

- 5.4.3 Veterinary Clinics

- 5.4.4 Retail & Online Pharmacies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Sanofi SA

- 6.4.2 GlaxoSmithKline plc

- 6.4.3 Merck & Co., Inc.

- 6.4.4 Zoetis Inc.

- 6.4.5 Boehringer Ingelheim International GmbH

- 6.4.6 Pfizer Inc.

- 6.4.7 Elanco Animal Health

- 6.4.8 Virbac SA

- 6.4.9 Bharat Biotech

- 6.4.10 AIM Vaccine Co., Ltd.

- 6.4.11 Chengdu Institute of Biological Products

- 6.4.12 Indian Immunologicals Ltd.

- 6.4.13 Kamada Ltd.

- 6.4.14 Kedrion Biopharma Inc.

- 6.4.15 CSL Behring

- 6.4.16 Grifols SA

- 6.4.17 Liaoning Cheng Da Co., Ltd.

- 6.4.18 Shuanglin Bio-Pharmaceutical Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment