|

시장보고서

상품코드

1848137

환자 리프트 장비 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Patient Lifting Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

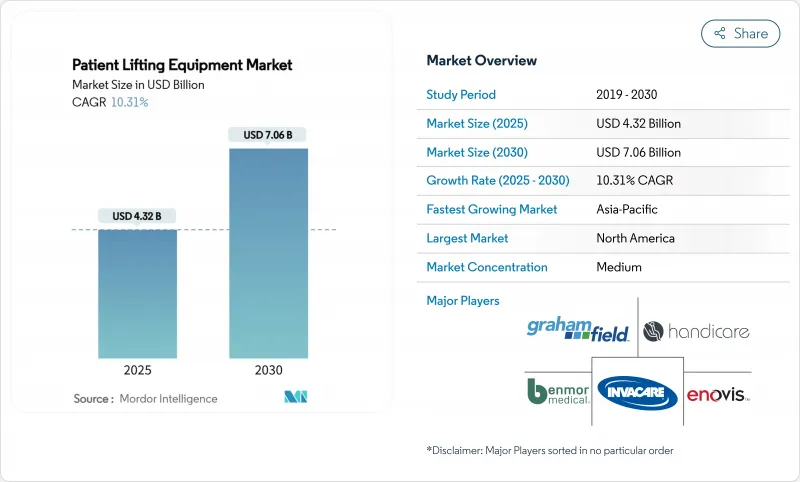

환자 리프트 장비 시장 규모는 2025년에 43억 2,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 10.31%로 성장할 전망이며, 2030년에는 70억 6,000만 달러에 달할 것으로 예측됩니다.

이 확장은 급성기 의료 및 장기 간호 제공을 총체적으로 재형성하는 광범위한 제로 리프트 의무화, 급속한 기술 업그레이드 및 인구 역학의 고령화를 반영합니다. 설비 투자는 간병인의 부상률을 낮추고 감염 제어 프로토콜을 준수하며 디지털 기록과 통합하는 전원 공급 장치로 IoT 지원 장비를 향해 이루어집니다. 아시아태평양은 병원 건설, 국내 제조업 인센티브, 비만 관리의 요구가 수렴함에 따라 가장 빠르게 가속화되고 있습니다. 동시에 임대 및 '서비스로서의 장비' 모델은 특히 가정 환경에서 비용에 민감한 구매자의 액세스를 개방합니다. 세계 기존 기업이 전문가를 흡수하고, 스마트 센서 플랫폼을 전개하며, 판매 후 서비스를 번들해 다년간 계약을 확보함에 따라, 경쟁의 격렬함이 증가합니다.

세계의 환자 리프트 장비 시장 동향 및 인사이트

노년 인구 및 비만 인구 증가

미국에서는 2050년까지 장기적인 도움을 필요로 하는 노인이 8,800만 명을 넘을 전망이며, 그 중에서도 85세 이상의 노인 증가가 가장 두드러집니다. 비만의 만연은 이동의 제한을 더욱 강화하기 위해 최대 454kg까지 대응 가능한 아르조의 시타델 플러스와 같은 비만 대응 기기에 대한 수요를 촉구하고 있습니다. 수동 취급은 현재 간병인 허리 통증의 52%를 유발하고 있기 때문에 병원은 리프팅 시스템을 재량 자본이 아니라 필수적인 안전 인프라로 취급하고 있습니다. 인구 동태의 압력은 장기간에 걸쳐, 예산 사이클 중에서도 지속적인 조달이 가능하고, 환자 리프트 장비 시장의 장기적인 성장 플로어를 지지하고 있습니다. 제품 로드맵은 이 층을 수용하기 때문에 더 높은 안전 작업 하중과 더 넓은 슬링 형상을 점점 더 선호합니다.

안전한 환자 취급 규제의 의무화

2024년에 갱신된 AORN 가이드라인은 수술실과 주술기 유닛에 개별 이동 계획에 맞는 천장 리프트 및 붐 리프트를 채택하도록 지시하고 있습니다. 캘리포니아의 AB1136 법은 종합적이고 안전한 환자 취급 틀을 요구하는 미국 법률의 예이며, 단위 수준의 규정 준수를 모니터링하는 UCLA Health의 리프트 챔피언 프로그램에 의해 지원됩니다. 노인 홈에 대한 OSHA 권고는 기계식 리프트를 더욱 권장하고 자발적인 규범을 강제력있는 노동 안전 명령으로 바꾸고 있습니다. 동등한 정책이 유럽에서 기세를 늘리고 APAC에서도 표면화하기 시작하여 환자 리프트 장비 시장의 대응 가능한 기반을 넓히고 있습니다. 환불이나 산재 청구에 얽힌 벌칙이 조달의 긴급성을 높여, 종래의 수동 호이스트의 교체가 가속합니다.

불충분한 간병인 교육 및 규정 준수 격차

기기를 도입한 후에도 많은 병원에서는 근골격계의 부상이 끊이지 않습니다. 전임 인체공학 교육자가 없는 소규모 시설에서는 기술 부족이 심각하여 설치된 시스템의 실현 가치를 저하시킵니다. 복잡한 전동 리프트를 안전하게 작동하려면 프로그래밍 가능한 설정, 배터리 점검, 슬링 선택에 익숙해야 합니다. 지속적인 감사가 없으면 과소 이용은 투자 수익률을 낮추고 환자 리프트 장비 시장 전체에 대한 도입을 지연시킵니다.

부문 분석

천장 주행형 리프트는 바닥 면적을 해제하고 이동 경로를 표준화하는 원활한 레일 마운트 통합을 통해 2024년 환자 리프트 장비 시장 점유율의 33.38%를 확보했습니다. 그 고정된 존재감은 감염 통제 구역화를 지원하고 넘어질 위험을 최소화하기 위해 병원의 신축에 대한 기본 옵션입니다. 바닥 주행형 및 이동식 리프트는 천장의 궤도의 개수가 불가능한 경우에 필수적이며, 자리에서 일어나는 보조 장치는 재활 병동에서 능동적인 이동의 서포트를 제공합니다. 급속히 진행되는 주택 노후화로 계단 승강기와 휠체어용 플랫폼 리프트의 2030년까지 CAGR은 14.92%로 성장이 전망됩니다. 제조업체 각 회사는 슬링 생태계를 다양화하고 있으며, Savaria의 Silvalea 라인은 비만, 절단 및 배설 용도에 적합한 직물 변형을 제공합니다.

진화하는 제품 로드맵은 모듈성을 강조하고 레일을 교체하지 않고 섀시를 업그레이드하거나 모터를 교체할 수 있습니다. 비만 환자를 위한 휴대용 무게 옵션은 최상급 모델 이외에도 퍼지고 있으며, 헤비 듀티 능력을 표준으로 하는 설계의 수렴을 보여줍니다. 터치 프리 펜던트 컨트롤을 갖춘 스마트 사용자 인터페이스는 감염 예방의 필요성을 해결하고 온보드 진단은 다운 타임을 줄입니다. 이러한 진보는 천장 주행 리프트의 프랜차이즈를 유지하며, 환자 리프트 장비 시장 전체의 안정적인 가치 획득을 지원합니다.

지역 분석

북미의 39.06% 매출 리더십은 견고한 안전 처리 규제, 상환 프레임워크 및 잘 조직된 공급망으로 인한 것입니다. Encompass Health는 161개의 재활 병원을 운영하며, 표준 리프트 프로토콜은 지역 조달의 벤치마크입니다. 미국의 헬스케어 고용은 2032년까지 210만 명 증가할 것으로 예상되며, 상해 완화 도구에 대한 수요가 증가하고 있습니다. 환자 리프트 장비 시장은 공공 병원과 민간 병원의 자본 계획 템플릿에 리프트를 통합하여 상환과 관련된 통합 노동자 안전 지표로부터 이익을 얻고 있습니다.

아시아태평양은 인구 동태 고령화, 보험 적용 범위 확대, 장비 생산 현지화를 추진하는 정부의 뒷받침을 받아 CAGR 예측 15.71%로 가장 급성장이 전망되고 있는 지역입니다. 중국에서는 2024년 7월에 의료기기 업그레이드에 관한 정책이 내세워져 현 수준의 병원에서의 고도 리프트 조달이 가속화되고 있습니다. 인구 고령화에 고민하는 일본은 혁신 보조금을 로봇 지원 이동 장치를 향해 하이 스펙 천장 주행 장치 수요를 강화합니다.

유럽은 노동안전 지령이 회원국 간 장비 기준을 조화시키기 때문에 규제 주도의 안정적인 성장을 유지하고 있습니다. 지속가능성 규칙은 재활용 가능한 재료와 에너지 효율적인 모터 플랫폼을 장려합니다. 중동 및 아프리카와 남미는 병원 건설 파이프라인과 임상 품질 인정이 초기 구매에 박차를 가하고 있는 것, 환율 변동과 조달 관료주의가 대규모 전개를 늦추고 있는 신흥 프론티어입니다. 이러한 지역 차이는 환자 리프트 장비 시장에서 적응성이 높은 시장 투입 모델의 전략적 필요성을 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 노인 및 비만 인구 증가

- 강제적인 '환자 안전 취급' 규제

- 재택 장기 간병 증가

- 전동 및 IoT 대응 리프트로의 기술 변화

- 병원의 '제로 리프트' 정책으로 스탭의 MSD 청구 억제

- 렌탈 및 서비스로서의 비즈니스 모델 상승

- 시장 성장 억제요인

- 간병인 연수의 부족 및 컴플라이언스의 갭

- 신흥 경제 국가에서 고액의 설비 투자 및 분산된 상환

- 의료기기 관련 환자 안전 리콜과 소송

- 짧은 제품 교환 사이클이 예산의 압박 초래

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 제품별

- 천장 리프트

- 바닥 및 이동식 리프트

- 상승 보조 및 이승 보조구

- 버스 및 풀 리프트

- 계단 및 휠체어용 플랫폼 리프트

- 리프팅용 슬링

- 액세서리

- 기구별

- 파워드

- 매뉴얼

- 최종 사용자별

- 병원

- 장기 및 간병 시설

- 재택 케어의 설정

- 재활센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Arjo AB

- Baxter(Hillrom)

- Invacare Corporation

- Savaria(HANDICARE)

- Enovis(DJO Global)

- Joerns Healthcare

- GF Health Products

- Benmor Medical

- V. Guldmann A/S

- Drive DeVilbiss Healthcare

- Prism Medical

- Medline Industries

- Getinge Group

- Stryker(MedSurg/Safe-patient-handling)

- Stiegelmeyer GmbH

- Vancare Inc.

- Etac AB(Molift)

- Handi-Move International

- HumanCare Group

- HoverTech International

- Sizewise

제7장 시장 기회 및 향후 전망

AJY 25.11.03The Patient Lifting Equipment Market size is estimated at USD 4.32 billion in 2025, and is expected to reach USD 7.06 billion by 2030, at a CAGR of 10.31% during the forecast period (2025-2030).

The expansion reflects widespread zero-lift mandates, rapid technology upgrades, and demographic aging that collectively reshape acute and long-term care delivery. Capital investments flow toward powered and IoT-ready devices that lower caregiver injury rates, align with infection-control protocols, and integrate with digital records. Asia-Pacific registers the fastest regional acceleration as hospital build-outs, domestic manufacturing incentives, and bariatric care needs converge. At the same time, rental and "equipment-as-a-service" models unlock access for cost-sensitive buyers, particularly in home settings. Competitive intensity rises as global incumbents absorb specialists, deploy smart-sensor platforms, and bundle post-sale services to secure multiyear contracts.

Global Patient Lifting Equipment Market Trends and Insights

Growing Geriatric & Bariatric Population

By 2050, the United States will support more than 88 million older adults who require long-term assistance, with the fastest growth among those aged 85 plus. Obesity prevalence compounds mobility limitations, prompting demand for bariatric-capable devices such as Arjo's Citadel Plus, which handles up to 454 kg. Manual handling currently causes 52% of caregiver back injuries, so hospitals treat lifting systems as essential safety infrastructure rather than discretionary capital. The longevity of demographic pressure underpins sustained procurement even through budgetary cycles, thereby anchoring a long-run growth floor for the patient lifting equipment market. Product roadmaps increasingly prioritize higher safe-working loads and wider sling geometries to serve this cohort.

Mandatory Safe-Patient-Handling Regulations

Updated 2024 AORN guidelines instruct surgical and perioperative units to adopt ceiling or boom lifts tailored to individualized transfer plans. California's AB 1136 law exemplifies U.S. legislation demanding comprehensive safe-patient-handling frameworks, supported by UCLA Health's Lift Champion program that monitors compliance at the unit level. OSHA advisories for nursing homes further recommend mechanical lifts, turning voluntary norms into enforceable occupational-safety commands. Equivalent policies gain momentum across Europe and start to surface in APAC, collectively widening the addressable base for the patient lifting equipment market. Penalties tied to reimbursement and worker-compensation claims reinforce procurement urgency, accelerating the replacement of legacy manual hoists.

Insufficient Caregiver Training & Compliance Gaps

Even after equipment rollout, many hospitals record persistent musculoskeletal injury rates because staff revert to manual lifting when pressed for time. The skill deficit is acute in smaller facilities lacking dedicated ergonomics educators, which curtails the realized value of installed systems. Complex powered lifts require familiarity with programmable settings, battery checks, and sling selection to operate safely. Without continuous audits, underutilization erodes return on investment and slows uptake across the patient lifting equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Home-Based Long-Term Care

- Technology Shift to Powered & IoT-Enabled Lifts

- High Capex and Fragmented Reimbursement in Developing Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling lifts secured 33.38% of the patient lifting equipment market share in 2024 owing to seamless rail-mount integration that frees floor space and standardizes transfer routes. Their anchored presence supports infection-control zoning and minimizes trip hazards, making them default choices in new hospital construction. Floor/mobile lifts remain indispensable where retrofitting ceiling tracks is infeasible, while sit-to-stand aids provide active-mobility support in rehabilitation wards. Rapidly aging residential stock propels stair and wheelchair platform lifts at a 14.92% CAGR to 2030, reflecting accessibility retrofits under building-code revisions. Manufacturers diversify sling ecosystems; Savaria's Silvalea line offers fabric variants for bariatric, amputee, and toileting applications.

The evolving product roadmap emphasizes modularity, enabling chassis upgrades or motor swaps without replacing rails. Bariatric payload options are spreading beyond top-tier models, signaling a design convergence that makes heavy-duty capability standard. Smart user interfaces with touch-free pendant controls address infection-prevention imperatives, while onboard diagnostics cut downtime. Collectively, these advances maintain the ceiling-lift franchise and support steady value capture across the patient lifting equipment market.

The Patient Lifting Equipment Market Report is Segmented by Product (Ceiling Lifts, Floor/Mobile Lifts, Sit-To-Stand & Transfer Aids, Bath & Pool Lifts, and More), Mechanism (Powered, Manual), End User (Hospitals, Long-Term & Nursing Homes, Home-Care Settings, Rehabilitation Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 39.06% revenue leadership rests on robust safe-handling regulations, reimbursement frameworks, and a well-organized supply chain. Encompass Health operates 161 rehabilitation hospitals whose standard lift protocols set benchmarks for regional procurement. U.S. healthcare employment is projected to add 2.1 million jobs by 2032, heightening demand for injury-mitigation tools. The patient lifting equipment market benefits from integrated worker-safety metrics tied to reimbursement, embedding lifts in capital-planning templates of both public and private hospitals.

Asia-Pacific represents the fastest-growing corridor, with a 15.71% CAGR forecast driven by aging demographics, expanded insurance coverage, and government pushes to localize device production. China's July 2024 policy on medical-equipment upgrades accelerates procurement of advanced lifts in county-level hospitals. Japan, grappling with population aging, directs innovation grants toward robotics-assisted mobility devices, reinforcing demand for high-specification ceiling tracks.

Europe maintains stable, regulation-driven growth as occupational-safety directives harmonize equipment standards across member states. Sustainability rules incentivize recyclable materials and energy-efficient motor platforms. Middle East & Africa and South America remain emerging frontiers where hospital-construction pipelines and clinical-quality accreditation spur initial purchases, yet currency swings and procurement bureaucracy slow large-scale rollouts. Collectively, regional variances amplify the strategic need for adaptable go-to-market models within the patient lifting equipment market.

- Arjo AB

- Baxter

- Invacare

- Savaria (HANDICARE)

- Enovis

- Joerns Healthcare

- GF Health Products

- Benmor Medical

- V. Guldmann A/S

- Drive DeVilbiss Healthcare

- Prism Medical

- Medline Industries

- Getinge

- Stryker (MedSurg / Safe-patient-handling)

- Stiegelmeyer GmbH

- Vancare Inc.

- Etac AB (Molift)

- Handi-Move International

- HumanCare Group

- HoverTech International

- Sizewise

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Geriatric & Bariatric Population

- 4.2.2 Mandatory "Safe-Patient-Handling" Regulations

- 4.2.3 Rise In Home-Based Long-Term Care

- 4.2.4 Technology Shift to Powered & IoT-Enabled Lifts

- 4.2.5 Hospital "Zero-Lift" Policies to Curb Staff MSD Claims

- 4.2.6 Emerging Rental & As-A-Service Business Models

- 4.3 Market Restraints

- 4.3.1 Insufficient Caregiver Training & Compliance Gaps

- 4.3.2 High Capex and Fragmented Reimbursement in Developing Economies

- 4.3.3 Device-Related Patient Safety Recalls & Litigation

- 4.3.4 Short Product-Replacement Cycles Causing Budget Strain

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Ceiling Lifts

- 5.1.2 Floor/Mobile Lifts

- 5.1.3 Sit-to-Stand & Transfer Aids

- 5.1.4 Bath & Pool Lifts

- 5.1.5 Stair & Wheelchair Platform Lifts

- 5.1.6 Lifting Slings

- 5.1.7 Accessories

- 5.2 By Mechanism

- 5.2.1 Powered

- 5.2.2 Manual

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Long-term & Nursing Homes

- 5.3.3 Home-care Settings

- 5.3.4 Rehabilitation Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Arjo AB

- 6.3.2 Baxter (Hillrom)

- 6.3.3 Invacare Corporation

- 6.3.4 Savaria (HANDICARE)

- 6.3.5 Enovis (DJO Global)

- 6.3.6 Joerns Healthcare

- 6.3.7 GF Health Products

- 6.3.8 Benmor Medical

- 6.3.9 V. Guldmann A/S

- 6.3.10 Drive DeVilbiss Healthcare

- 6.3.11 Prism Medical

- 6.3.12 Medline Industries

- 6.3.13 Getinge Group

- 6.3.14 Stryker (MedSurg / Safe-patient-handling)

- 6.3.15 Stiegelmeyer GmbH

- 6.3.16 Vancare Inc.

- 6.3.17 Etac AB (Molift)

- 6.3.18 Handi-Move International

- 6.3.19 HumanCare Group

- 6.3.20 HoverTech International

- 6.3.21 Sizewise

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment