|

시장보고서

상품코드

1848145

디지털 정량 흡입기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Digital Dose Inhaler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

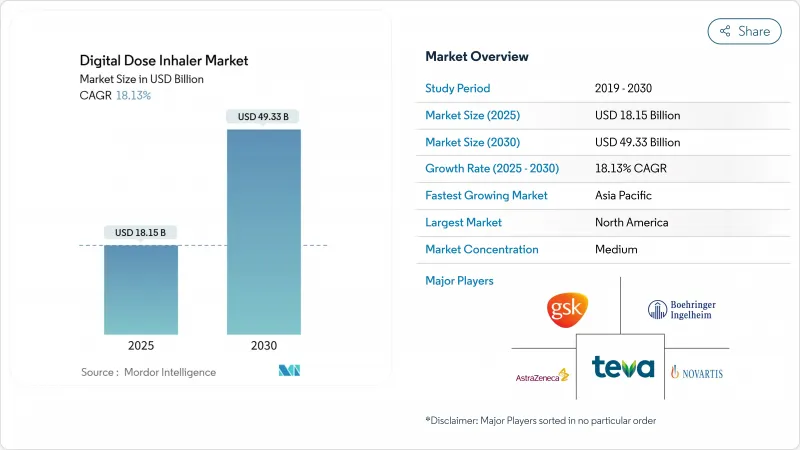

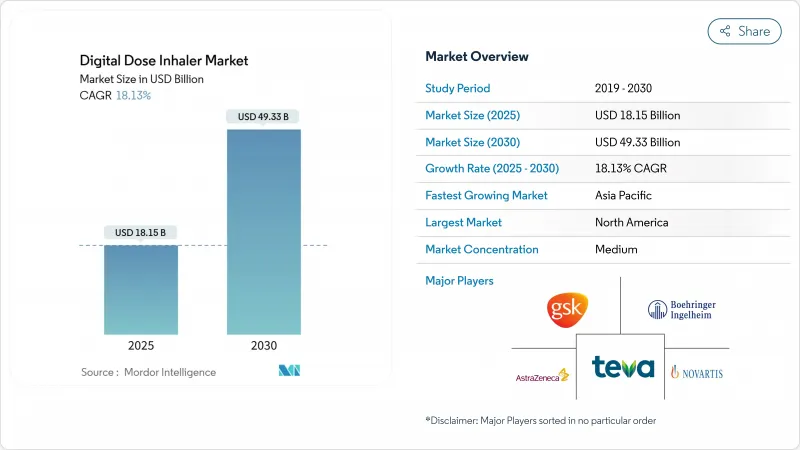

디지털 정량 흡입기 시장 규모는 2025년 181억 5,000만 달러로 추정되고, CAGR 18.13%로 성장할 전망이며, 2030년에는 493억 3,000만 달러에 이를 것으로 예측됩니다.

강력한 성장은 호흡기 질환의 유병률 증가, 연결 치료제의 급속한 보급, 추진제 기술 혁신을 강요하는 엄격한 환경 규제와 관련이 있습니다. 사물인터넷에 대응하는 흡입기로부터 실시간 데이터 획득은 의사에게 객관적인 어드히어런스의 증거를 부여하고, 인공지능은 악화를 미리 예측하기 시작했습니다. 디지털 호흡 케어 신흥 기업으로의 자본 유입은 증가의 일환으로, 경쟁 구도를 강화하고, 센서 탑재 기기에 대한 환자 액세스를 확대하고 있습니다. 유럽의 환경법은 낮은 GWP 추진제로의 전환을 가속화하고 있으며, 주요 공급업체는 2030년 컴플라이언스 마감일을 크게 앞당겨 정량 흡입기 포트폴리오의 오버홀을 촉진하고 있습니다.

세계의 디지털 정량 흡입기 시장 동향 및 인사이트

심각화하는 세계의 호흡기 질환 부담

2021년에는 2억 1,339만 명이 만성호흡기 질환을 앓아, 어드히어런스를 객관적으로 기록하는 커넥티드 흡입기에 대한 수요가 높아졌습니다. 스마트 디바이스와 연동한 행동 변형 프로그램에 의해 COPD 환자의 복약 준수가 44% 개선되었다는 연구 결과도 있습니다. 인공지능의 통합은 조기 악화 경고를 가능하게 하고, 디지털 장비는 수동적인 추적기에서 적극적인 질병 관리 도구로 전환하고 있습니다.

노년 환자 집단 확대

노년층은 2030년까지 연평균 복합 성장률(CAGR)이 18.67%로 가장 빠르게 성장하고 있는 사용자 그룹입니다. 이는 노화와 관련된 손가락 민첩성의 제한으로 인해 직관적인 호흡 작동 장치가 매력적이기 때문입니다. 간소화된 인터페이스와 대형 디스플레이는 사용 편의성을 향상시키고 Medicare는 센서 상환을 시험적으로 도입했지만 전국적인 적용 범위는 여전히 불균일합니다.

커넥티드 흡입기 장치의 고가격

스마트 흡입기는 기존 흡입기보다 훨씬 비쌉니다. 총소유 비용에는 데이터 플랜과 소프트웨어 구독이 포함됩니다. 경제적 평가에서 임상적 이점은 인정되지만, 약국의 금리가 좁은 경우 비용 효과에 의문이 남습니다. 단계적 가격 설정과 지불자와의 파트너십은 진화하고 있지만, 일관된 상환, 특히 공적 제도가 없기 때문에 개발 도상 지역에서의 보급은 한정적입니다.

부문 분석

정량 흡입기는 2024년에 디지털 정량 흡입기 시장 점유율의 48.54%를 유지해 사용자에게 친숙함과 성숙한 제조 경제성을 뒷받침하고 있습니다. 이 부문의 디지털 정량 흡입기 시장 규모는 기업이 초저 GWP 추진제로 전환함에 따라 CAGR 14.2%로 상승할 것으로 예측됩니다. AstraZeneca사의 HFO-1234ze(E)의 전개에 의해 폭넓은 환경 부하가 99.9% 삭감되고 있습니다.

소프트 미스트 흡입기는 폐에 도달률이 높고, 추진제를 필요로 하지 않기 때문에 CAGR 20.34%로 성장이 전망되며, 보다 광범위한 디지털 정량 흡입기 시장을 상회하고 있습니다. 장치의 소형화 및 내장 센서를 통해 실시간 유량 측정이 가능해 정확한 복용량 검증을 요구하는 의료 제공업체에게 매력적입니다. 건조 분말 흡입기는 기후가 시원하고 성인 유저의 흡입 유량이 많은 지역에서는 계속 유효하지만 열대 지역에서는 습도가 높기 때문에 흡입량이 제한됩니다.

천식은 2024년 매출의 41.48%를 차지했으며, 대규모 소아 및 청소년 성인 코호트와 연결 어드히어런스 솔루션을 지원하는 풍부한 임상 증거에 의해 지원됩니다. COPD의 디지털 정량 흡입기 시장 규모는 고령화로 이병 기간이 장기화되고 지불자가 입원 횟수 감소에 따른 비용 절감을 요구하고 있기 때문에 CAGR 18.9%로 급속히 확대하고 있습니다. HealthPrize의 RespiPoints는 티오트로피움 사용자의 어드히어런스가 44% 향상되어 실질적인 비용 절감으로 이어졌다고 보고되었습니다.

CAGR 19.45%라는 낭포성 섬유증의 성장은 고가치의 투약 요법을 최적화하기 위한 프리미엄 모니터링에 대한 간병인의 투자 의욕을 보여줍니다. AI 알고리즘은 현재 질병 특유의 흡입 패턴을 구별하고 각 적응증에 대한 코칭을 개인화하며 연결 플랫폼의 임상적 타당성을 높입니다.

지역 분석

북미는 정교한 지불자 시스템, 높은 COPD 유병률, 디지털 치료제의 조기 FDA 승인 등을 배경으로 2024년 매출의 43.45%를 창출했습니다. GSK와 Propeller Health는 센서가 장착된 Ellipta 흡입기를 전국에 출하하기 위해 협력을 확대하여 통합 처방 기술 번들의 상업적 실행 가능성을 입증했습니다. 캐나다에서는 단일 보험자에 의한 구매의 이점이 있는 반면, 각 국가의 처방전에서는 어드히어런스 보고서에 연동된 결과 기반 조달이 시험적으로 실시되고 있습니다. 멕시코에서는 중산 계급이 증가하고 디지털 헬스 인센티브가 중가격대 의료기기에 문을 열고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 19.45%로 가장 빠르게 성장이 전망되고 있는 지역입니다. 중국에서는 인구 수준의 부담이 정책 입안자에게 예방 도구의 도입을 강요하고 있으며, 공립 병원에서는 흡입기 데이터를 전자 의료 기록과 통합하는 클라우드 대시보드의 시행이 이루어지고 있습니다. 인도에서는 4G의 보급이 진행되고 원격 의료 가이드라인이 개정됨에 따라 온라인 약국에서의 센서 키트 전개가 지원되고 있습니다. 일본은 급속한 고령화 및 성숙한 기술 문화를 겸비하고 AI 코칭을 번들한 고급 소프트 미스트 흡입기의 비옥한 시장이 되고 있습니다.

유럽은 성숙하면서도 혁신적인 시장이며, 환경 규제가 세계적인 선례가 되고 있습니다. F-Gas 규칙 2024/573은 2025년부터 할당 이외의 신규 HFC 충전 흡입기를 금지하고 저GWP 채용 스케줄을 가속시킵니다. 독일의 DiGA 프레임워크는 인증된 디지털 건강 앱을 환불하고 흡입기 컴패니언 소프트웨어를 급속한 보급을 위해 자리잡고 있습니다. 영국은 현실적인 스탠스를 유지해 입원 회피를 실증한 기기에 상환을 실시합니다. 중동 및 아프리카와 남미는 인프라, 임상의의 훈련, 소비자의 구매력에 의해 제한되지만, 이제 막 시작되었으며 유망합니다. 기부 프로그램과 단계적 가격 모델은 이러한 격차를 메우기 위한 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계 호흡기 질환의 부담 증대

- 고령자 환자층 확대

- 스마트 흡입기 플랫폼의 기술적 진보

- 디지털 치료 및 원격 모니터링으로의 전환

- 데이터 분석 및 가치에 근거한 케어 모델의 통합

- 환경 컴플라이언스 및 저 GWP 추진제의 채용

- 시장 성장 억제요인

- 커넥티드 흡입기의 프리미엄 가격

- 복잡한 규제 및 상환 경로

- 엄격한 데이터 프라이버시 및 사이버 보안 요건

- 반도체 공급망의 제약

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 드라이 파우더 흡입기

- 정량 분무식 흡입기

- 소프트 미스트 흡입기

- 적응증별

- COPD

- 천식

- 낭포성 섬유증

- 기타 호흡기 질환

- 유형별

- 브랜드

- 제네릭

- 환자의 연령층별

- 소아

- 성인용

- 고령자

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Teva Pharmaceutical Industries

- GlaxoSmithKline plc

- AstraZeneca plc

- Boehringer Ingelheim

- Novartis AG

- Glenmark Pharmaceuticals

- Koninklijke Philips NV

- Propeller Health

- AptarGroup Inc.

- H&T Presspart Manufacturing Ltd.

- Trudell Medical Group

- Adherium Ltd.

- ResMed Inc.

- Vectura Group plc

- Mundipharma International

- 3M Drug Delivery Systems

- Cipla Ltd.

- Opko Health Inc.

- Amiko Digital Health

- Pneuma Respiratory

- FindAir

- Cohero Health

- BreatheSuite Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.03The digital dose inhaler market size is valued at USD 18.15 billion in 2025 and is projected to reach USD 49.33 billion by 2030, reflecting an 18.13% CAGR.

Robust growth is linked to rising respiratory disease prevalence, rapid uptake of connected therapeutics, and stringent environmental regulations that are forcing propellant innovation. Real-time data capture from Internet of Things-enabled inhalers is giving physicians objective adherence evidence, while artificial intelligence is beginning to predict exacerbations before they occur. Capital inflows into digital respiratory care start-ups continue to climb, strengthening the competitive landscape and expanding patient access to sensor-equipped devices. Environmental legislation in Europe is accelerating the switch to low-GWP propellants, prompting major suppliers to overhaul meter-dose inhaler portfolios well ahead of 2030 compliance deadlines.

Global Digital Dose Inhaler Market Trends and Insights

Escalating Global Respiratory Disease Burden

Chronic respiratory diseases affected 213.39 million people in 2021, sustaining demand for connected inhalers that objectively record adherence. Studies show 44% adherence improvement among COPD patients using behavior-change programs linked to smart devices. Integration of artificial intelligence is enabling early exacerbation alerts, moving digital devices from passive trackers to proactive disease-management tools.

Expanding Geriatric Patient Pool

The geriatric cohort is the fastest-growing user group at an 18.67% CAGR through 2030 as age-related dexterity limitations make intuitive breath-activated devices attractive. Simplified interfaces and larger displays improve usability, while Medicare payment pilots are experimenting with sensor reimbursement, although national coverage remains uneven.

Premium Pricing of Connected Inhaler Devices

Smart inhalers cost substantially more than conventional units, and total ownership expenses include data plans and software subscriptions. Economic evaluations find clinical benefits but question cost-effectiveness when pharmacy margins are narrow. Tiered pricing and payer partnerships are evolving, yet the lack of consistent reimbursement, especially in public systems, limits penetration in developing regions.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Smart Inhaler Platforms

- Transition Toward Digital Therapeutics and Remote Monitoring

- Complex Regulatory and Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metered dose inhalers retained 48.54% of digital dose inhaler market share in 2024, underscoring user familiarity and mature manufacturing economics. The digital dose inhaler market size for this segment is projected to rise at a 14.2% CAGR as companies transition to ultra-low-GWP propellants. Environmental mandates are accelerating formulation re-engineering, with AstraZeneca's HFO-1234ze(E) rollout reducing broad environmental impact by 99.9%.

Soft-mist inhalers provide higher lung deposition and need no propellant, fueling a 20.34% CAGR that outpaces the broader digital dose inhaler market. Device miniaturization and embedded sensors allow real-time flow measurement, appealing to providers seeking precise dose verification. Dry-powder inhalers remain relevant in regions with cooler climates and robust inspiratory flow among adult users, yet high humidity limits uptake in tropical geographies.

Asthma accounted for 41.48% of revenue in 2024, buoyed by large pediatric and young-adult cohorts and plentiful clinical evidence supporting connected adherence solutions. The digital dose inhaler market size for COPD is expanding faster at 18.9% CAGR as aging populations lengthen disease duration and payers seek cost offsets through fewer hospitalizations. HealthPrize RespiPoints documented a 44% adherence increase among tiotropium users, translating to material cost savings.

Cystic fibrosis growth at 19.45% CAGR demonstrates willingness of caregivers to invest in premium monitoring to optimize high-value medication regimens. AI algorithms now differentiate disease-specific inhalation patterns, personalizing coaching for each indication and raising the clinical relevance of connected platforms.

The Digital Dose Inhaler Market Report is Segmented by Product (Dry Powder Inhalers, and More), Indication (COPD, and More), Type (Branded and Generic), Patient Age Group (Pediatric, and More), Distribution Channel (Hospital Pharmacies, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.45% of revenue in 2024 on the back of sophisticated payer systems, high COPD prevalence, and early FDA approvals of digital therapeutics. GSK and Propeller Health broadened their collaboration to ship sensor-enabled Ellipta inhalers nationwide, demonstrating the commercial viability of integrated prescription-tech bundles. Canada benefits from single-payer purchasing leverage, while Provincial formularies are piloting outcome-based procurement tied to adherence reports. Mexico's growing middle class and digital-health incentives open gateways for mid-priced devices.

Asia-Pacific is the fastest-growing region at 19.45% CAGR through 2030 as urban air pollution and smoking contribute to rising COPD cases. China's population-level burden pressures policymakers to adopt preventive tools; public hospitals are trialling cloud dashboards that integrate inhaler data with electronic medical records. India's expanding 4G coverage and revised telemedicine guidelines underpin online pharmacy distribution of sensor kits, yet affordability gaps persist. Japan couples rapidly aging demographics with a mature technology culture, making it a fertile market for premium soft-mist inhalers bundled with AI coaching.

Europe remains a mature but innovative market where environmental regulation sets global precedents. The F-Gas Regulation 2024/573 bans new HFC-filled inhalers outside of quota allocations from 2025, accelerating low-GWP adoption schedules. Germany's DiGA framework reimburses certified digital health apps, positioning inhaler companion software for rapid uptake. The United Kingdom maintains a pragmatic stance, reimbursing devices that demonstrate hospital-admission avoidance. Middle East & Africa and South America are nascent yet promising, limited by infrastructure, clinician training, and consumer purchasing power. Donation programs and tiered pricing models aim to bridge these gaps.

- Teva Pharmaceutical Industries

- GlaxoSmithKline

- AstraZeneca

- Boehringer Ingelheim

- Novartis

- Glenmark Pharmaceuticals

- Koninklijke Philips

- Propeller Health

- AptarGroup Inc.

- H&T Presspart Manufacturing Ltd.

- Trudell Medical Group

- Adherium Ltd.

- Resmed

- Vectura Group plc

- Mundipharma International

- 3M Drug Delivery Systems

- Cipla

- Opko Health Inc.

- Amiko Digital Health

- Pneuma Respiratory

- Findair

- Cohero Health

- BreatheSuite

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Respiratory Disease Burden

- 4.2.2 Expanding Geriatric Patient Pool

- 4.2.3 Technological Advancements in Smart Inhaler Platforms

- 4.2.4 Transition Toward Digital Therapeutics and Remote Monitoring

- 4.2.5 Integration of Data Analytics And Value-Based Care Models

- 4.2.6 Environmental Compliance and Low-Gwp Propellant Adoption

- 4.3 Market Restraints

- 4.3.1 Premium Pricing of Connected Inhaler Devices

- 4.3.2 Complex Regulatory and Reimbursement Pathways

- 4.3.3 Stringent Data Privacy and Cybersecurity Requirements

- 4.3.4 Semiconductor Supply Chain Constraints

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Dry Powder Inhalers

- 5.1.2 Metered Dose Inhalers

- 5.1.3 Soft-Mist Inhalers

- 5.2 By Indication

- 5.2.1 COPD

- 5.2.2 Asthma

- 5.2.3 Cystic Fibrosis

- 5.2.4 Other Respiratory Disorders

- 5.3 By Type

- 5.3.1 Branded

- 5.3.2 Generic

- 5.4 By Patient Age Group

- 5.4.1 Pediatric

- 5.4.2 Adult

- 5.4.3 Geriatric

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Teva Pharmaceutical Industries

- 6.3.2 GlaxoSmithKline plc

- 6.3.3 AstraZeneca plc

- 6.3.4 Boehringer Ingelheim

- 6.3.5 Novartis AG

- 6.3.6 Glenmark Pharmaceuticals

- 6.3.7 Koninklijke Philips N.V.

- 6.3.8 Propeller Health

- 6.3.9 AptarGroup Inc.

- 6.3.10 H&T Presspart Manufacturing Ltd.

- 6.3.11 Trudell Medical Group

- 6.3.12 Adherium Ltd.

- 6.3.13 ResMed Inc.

- 6.3.14 Vectura Group plc

- 6.3.15 Mundipharma International

- 6.3.16 3M Drug Delivery Systems

- 6.3.17 Cipla Ltd.

- 6.3.18 Opko Health Inc.

- 6.3.19 Amiko Digital Health

- 6.3.20 Pneuma Respiratory

- 6.3.21 FindAir

- 6.3.22 Cohero Health

- 6.3.23 BreatheSuite Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment