|

시장보고서

상품코드

1848147

배양 배지 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Culture Media - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

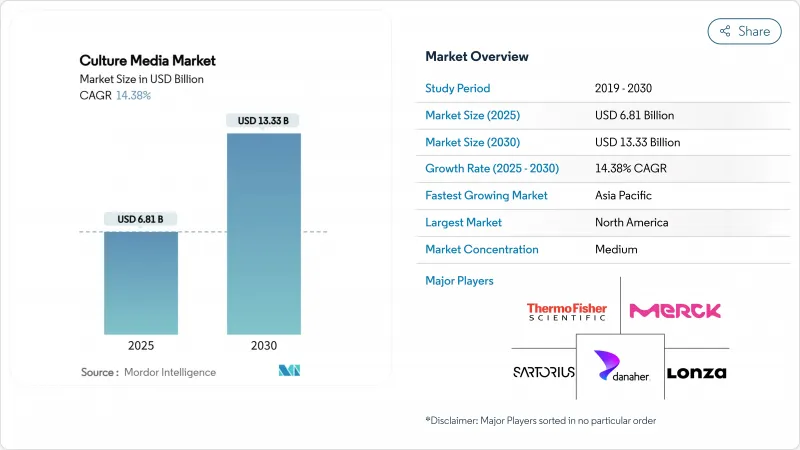

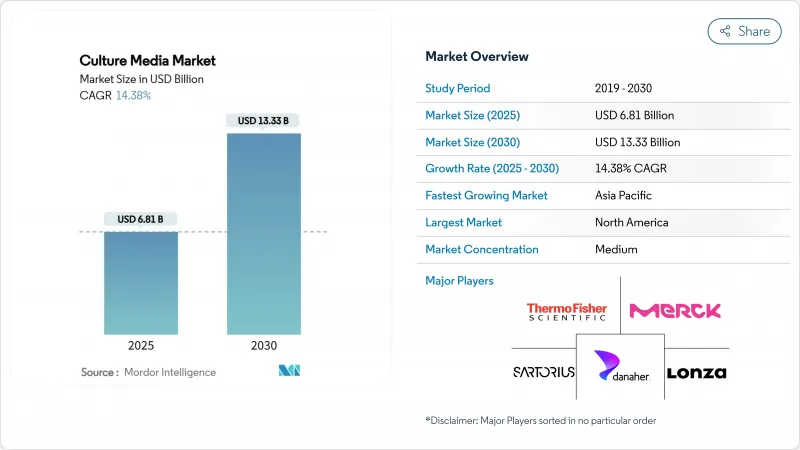

배양 배지 시장 규모는 2025년에 68억 1,000만 달러로 평가되었고, 2030년에는 133억 3,000만 달러에 달할 것으로 예측되고 있습니다.

차세대 바이오프로세싱 투입물에 대한 수요 증가, mRNA 백신 생산라인의 규모 확대, 바이오시밀러 상용화 가속화가 채택 확대의 주요 동력입니다. 공급망 경제성으로 인해 탈수 제형이 여전히 우위를 점하고 있으나, 발색성 제형의 인기는 실험실이 자동화 준비가 된 소모품으로 꾸준히 전환하고 있음을 시사합니다. 북미는 확립된 규제 환경과 벤처 자금 조달 파이프라인 덕분에 지역 수요가 집중되는 반면, 아시아태평양 지역은 정책 지원 시설 확장으로 가장 빠른 단위 확장세를 보일 전망입니다. 원료 조달, 일회용 하드웨어, 사내 분석을 통합하여 전 과정 워크플로우 지출을 포착하는 풀서비스 공급업체들의 경쟁 압력이 증가하고 있습니다. 국내 바이오프로세싱을 우대하는 재정적 인센티브와 자동화된 배지 준비 플랫폼이 결합되면서 원료 인플레이션과 물류 위험에 여전히 민감한 시장에서 새로운 기회가 열리고 있습니다.

세계의 배양 배지 시장 동향 및 인사이트

혈청 기반에서 동물 성분을 포함하지 않는 배지로의 이행

규제 당국이 동물성 성분이 없는 배지를 선호함에 따라 제조업체들은 혈청 투입을 중단하고 화학적으로 정의된 대체재에 대한 의존도를 높이고 있습니다. 혈청 무첨가 배지는 이미 36.32%의 점유율을 차지하고 있으며, FDA 지침이 우발적 병원체에 대한 감시를 강화함에 따라 점유율이 계속 증가하고 있습니다. 연평균 성장률(CAGR) 15.85%로 확장 중인 줄기세포 배지는 재생의학 생산자들이 정의된 화학 성분에 부여하는 프리미엄을 강조합니다. 메르크 KGaA의 항체 및 mRNA 개발을 위한 3억 유로 규모 연구 센터는 무성분 플랫폼으로의 자본 유입을 보여주는 사례입니다. 배치 간 일관성 향상, 다운스트림 정제 공정 간소화, 오염 위험 감소는 동물성분 무첨가 솔루션의 상업적 타당성을 뒷받침하며, 이러한 전환은 배지 시장의 핵심 구조적 성장 동력이 되고 있습니다.

신속하고 대규모 mRNA/바이러스 벡터 및 백신 생산 능력 확대

팬데믹 기간에 구축된 생산 설비는 암 백신, 유전자 치료제, 원숭이두 예방으로 전환되며 특수 바이러스 벡터 배지에 대한 지속적 수요를 확보했습니다. 바바리안 노르딕이 2025년 말까지 1천만 회분의 원숭이두 백신을 공급하겠다는 계획은 이러한 신규 시설의 지속적인 활용을 반영합니다. 고수율 mRNA 전사 및 바이러스 감염성을 위한 최적화된 배지는 동일한 시설에서 다중 프로그램을 운영하는 플랫폼 제조사에 핵심적입니다. 제품 간 표준화를 지원함으로써 배지 공급업체들은 공정 제어 분석 및 일회용 하드웨어 번들을 포함한 파트너십에 한 걸음 더 가까워지고 있습니다. 해당 분야의 시급성을 고려할 때 구매 계약은 종종 다년간에 걸쳐 체결되어, 배지 시장의 이 고성장 분야에서 활동하는 공급업체들의 매출 가시성을 높이고 있습니다.

의약품 원료 인플레이션 및 공급망 취약성

아미노산, 성장 인자, 고순도 물의 급등하는 가격에 운송 병목 현상이 더해져 마진이 계속 압박받고 있습니다. 코로나19 시대의 혼란은 긴 공급망의 취약성을 드러내며 기업들로 하여금 더 큰 안전 재고로 헤지하도록 유도했고, 이로 인해 운전 자본 수요가 증가했습니다. 이중 공급처 전략이 일부 노출을 완화하지만, 자격 인증 비용을 증가시키고 소규모 실험실에 불리하게 작용합니다. 결과적으로 정책 인센티브가 국내 생산을 장려하고 있음에도, 검증 및 자본 프로젝트를 위한 예산 유연성을 유지해야 하는 최종 사용자들의 비용 전가 피로감으로 인해 배지 시장의 단기 성장은 위축되고 있습니다.

부문 분석

2024년 배양 배지 시장 점유율은 탈수 제제가 51.25%를 차지하며 이는 긴 유통기한과 경제적인 운송 비용 덕분입니다. 그러나 자동화 배지 도포 시스템이 임상 및 식품 검사 환경에서 확산되면서 발색성 배지 대안은 15.65%의 연평균 성장률(CAGR)로 가속화되고 있습니다. 이러한 확장은 판독 시간을 단축하고 인적 오류를 줄이는 사전 분화형 색상 변화 배지를 실험실이 선호한다는 신호입니다. 예측 기간 동안 발색성 솔루션은 특히 고처리량 병원 실험실에서 탈수형 기존 제품의 점유율을 잠식할 것으로 전망됩니다. 그럼에도 신흥 경제권의 가격 민감도는 탈수 제품의 상당한 기반을 유지시켜 배지 시장의 핵심 요소로 남게 합니다.

자동화 친화적 특성 덕분에 발색성 배지는 바코드 플레이트 추적 및 로봇 배양이 균일한 물리적 특성을 요구하는 완전 실험실 자동화 시스템의 논리적 동반자가 됩니다. 이에 따라 미리 적층된 자동화 호환 형식을 공급할 수 있는 업체들이 불균형적인 시장 점유율을 확보하고 있습니다. 탈수 제형은 지역 혼합 센터로의 대량 운송에 여전히 선호되며, 구매자는 수화 중량 비용 없이 물량을 확장할 수 있습니다. 상반된 가치 제안은 선도 공급업체들이 기존 탈수 제품의 강점과 고마진 발색성 혁신을 균형 있게 조화시키는 혼합 포트폴리오 접근법을 유지하게 합니다.

무혈청 제품은 2024년 매출의 36.32%를 차지했으며, 이는 정의된 성분으로의 규제적 추진과 소 혈청 위험으로부터의 이탈을 반영합니다. 가장 빠르게 성장하는 하위 분야인 줄기세포 배지는 자가 및 동종 치료제로의 산업 전환에서 수혜를 입으며, 이는 피더 세포가 필요 없는 조건을 요구합니다. 재생의학 임상시험이 후기 단계로 진입함에 따라 줄기세포 배지 시장은 2030년까지 연평균 15.85% 성장할 것으로 전망됩니다.

대규모 항체 및 mRNA 제조에서 화학적으로 정의된 배지의 채택도 추적 가능성과 일관된 성능 덕분에 더욱 강화되고 있습니다. 공급업체와 세포주 개발 전문가 간의 협력을 통해 타이터 최적화를 가속화하는 맞춤형 레시피가 개발되며 고객 락인(lock-in)이 더욱 공고해지고 있습니다. 한편, CAR-T, 종양용해바이러스 또는 오가노이드 배양과 같은 특수한 대사 요구에 맞춰 설계된 특수 및 맞춤형 배지는 프리미엄 가격대를 형성하며 배지 시장 내 매출 구성비를 확대하고 있습니다.

지역 분석

북미는 2024년 배지 시장의 39.25% 점유율을 유지했으며, 2030년까지 연평균 13.8%의 성장률을 보일 것으로 예상됩니다. 미국은 팬데믹 자금으로 구축된 mRNA 인프라를 종양학 및 희귀질환 파이프라인에 재활용함으로써 지역 성장 동력을 주도하고 있으며, FDA의 배지 검증에 대한 명확한 지침은 업계 신뢰를 유지하고 있습니다. 메르크 KGaA의 메릴랜드 주 2억 9천만 달러 규모 생물안전 테스트 시설 및 BD의 주사기 생산 능력 확대와 같은 자본 투자는 공급업체 생태계를 더욱 공고히 합니다. 벤처 자금은 세포 치료 스타트업으로 집중되며, 고성능·동물성분 무첨가 제형에 대한 꾸준한 수요를 강화하고 있습니다.

아시아태평양 지역은 바이오기술을 전략적 분야로 삼는 국가 프로그램에 힘입어 연평균 16.45%의 가장 빠른 성장률을 기록할 전망입니다. 중국의 코로나19 이후 실험실 주문 패턴 정상화, 한국의 바이오시밀러 생산 인센티브, 인도의 바이오프로세싱 수입 관세 면제 등이 모두 지역 배지 수요를 증가시키고 있습니다. 밀리포어시그마의 3억 유로 규모 한국 시설은 다국적 기업의 현지화 공급 의지를 보여줍니다. 강력한 연구 기반과 조화된 GMP 프레임워크를 바탕으로 한 호주 및 일본 시장은 평균 이상의 운영률로 고사양 줄기세포 배지를 채택하고 있습니다.

유럽은 2024년 매출의 28.5%를 차지했으며, 2030년까지 연평균 12.9% 성장률을 목표로 합니다. 독일, 영국, 프랑스가 주요 3국을 구성합니다. 독일 다름슈타트의 첨단 연구 센터는 항체 및 mRNA 분야의 지역 R&D를 확대하는 반면, 영국은 백신 클러스터 유산과 MHRA 규제 역량의 혜택을 누립니다. 프랑스의 생물학적 제제 혁신 계획은 무혈청 및 화학적으로 정의된 배지 수요의 지속성을 유지합니다. 회원국 간 문서 및 품질 요건을 조화시키는 유럽의약품청(EMA) 지침은 공급업체의 허가 장벽을 낮추어 유럽을 안정적이면서도 경쟁력 있는 배지 수출 시장으로 자리매김합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 혈청 기반 배지로부터 동물 성분을 포함하지 않는 배지로의 이행

- 신속하고 대규모 mRNA/바이러스 벡터 백신의 생산 능력 확대

- 바이오시밀러 제조 붐으로 인한 대량 배지 수요 창출

- CDMO 및 대형 제약사의 완전 자동화 배지 제조 시스템 도입

- 국내 바이오프로세싱에 대한 재정적 인센티브

- 시장 성장 억제요인

- 의약품 원료 가격 상승과 공급망 취약점

- 배치 간 변동성으로 인한 복잡한 배지의 규제 승인 지연

- 숙련된 배지 최적화 과학자의 글로벌 부족

- 공급망 분석

- 기술의 전망

- Porter's Five Forces

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(달러 기준 가치)

- 배지 유형별

- 발색 배양 배지

- 탈수 증상 배양 배지

- 준비/즉시 사용 가능 배양 배지

- 처방별

- 혈청 기반 배지

- 무혈청 배지

- 화학적으로 정의된 배양 배지

- 줄기세포 배양 배지

- 특수 배지/맞춤형 배지

- 물리적 상태별

- 액체 배지

- 분말 배지

- 반고체/겔 배지

- 최종 사용자별

- 제약 및 생명공학 기업

- 위탁 개발 제조 조직(CDMO)

- 학술연구기관

- 임상 및 진단실험실

- 식품 및 음료 시험 연구소

- 준비 자동화

- 수동 배지 준비

- 자동 배지 준비 시스템

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 기업 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Merck KGaA(MilliporeSigma)

- Sartorius AG

- Danaher Corp.(Cytiva)

- Lonza Group Ltd.

- Becton, Dickinson and Company

- Corning Incorporated

- Bio-Rad Laboratories Inc.

- FUJIFILM Holdings(Irvine Scientific)

- Avantor Inc.

- HiMedia Laboratories Pvt. Ltd.

- GE HealthCare

- Ajinomoto Co. Inc.

- Caisson Laboratories Inc.

- PAN-Biotech GmbH

- MP Biomedicals LLC

- KOHJIN Bio Co. Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.12The culture media market size stood at USD 6.81 billion in 2025 and is projected to reach USD 13.33 billion by 2030, reflecting a sturdy 14.38% CAGR.

Intensifying demand for next-generation bioprocessing inputs, the scaling-up of mRNA vaccine lines, and accelerating biosimilar commercialization are the principal forces widening adoption. Dehydrated formulations preserve dominance because of supply-chain economy, yet the popularity of chromogenic formats signals laboratories' steady shift to automation-ready consumables. Regional demand tilts toward North America thanks to its established regulatory environment and venture funding pipeline, while Asia-Pacific's policy-backed facility build-out positions the region for the quickest unit expansion. Competitive pressure is rising as full-service suppliers integrate raw-material sourcing, single-use hardware, and in-house analytics to capture end-to-end workflow spending. Fiscal incentives that favor domestic bioprocessing, coupled with automated media-preparation platforms, are unlocking fresh opportunities in a market that remains sensitive to raw-material inflation and logistics risk.

Global Culture Media Market Trends and Insights

Shift from Serum-based to Animal-component-free Media

Regulators now favor media free from animal components, prompting manufacturers to retire serum inputs and increase reliance on chemically-defined alternatives. Serum-free variants already control 36.32% share and continue gaining as FDA guidance heightens scrutiny of adventitious agents. Stem-cell media, expanding at 15.85% CAGR, underscores the premium that regenerative-medicine producers place on defined chemistries. Merck KGaA's EUR 300 million research center for antibody and mRNA development exemplifies capital flowing into component-free platforms. Heightened lot-to-lot consistency, simpler downstream purification, and lower contamination risk anchor the commercial justification for animal-component-free solutions, making the transition a core structural tailwind for the culture media market.

Rapid, Large-scale mRNA / Viral-vector Vaccine Capacity Expansions

Production assets erected during the pandemic have pivoted toward cancer vaccines, gene therapies, and mpox prophylaxis, locking in recurrent demand for specialized viral-vector media. Bavarian Nordic's plan to deliver 10 million mpox doses by end-2025 reflects the sustained use of these green-field facilities. Media optimized for high-yield mRNA transcription and viral infectivity is pivotal for platform manufacturers that run multiple programs through the same suites. By supporting cross-product standardization, culture media suppliers are edging closer to partnerships that include process-control analytics and single-use hardware bundles. Given the sector's urgency, purchase commitments frequently span multi-year horizons, improving revenue visibility for media vendors operating in this high-growth corner of the culture media market.

Pharmaceutical-grade Raw-material Inflation & Supply-chain Fragility

Surging prices for amino acids, growth factors, and high-purity water, compounded by transportation bottlenecks, continue to squeeze margins. COVID-19-era disruptions exposed the vulnerability of lengthy supply chains, prompting companies to hedge with larger safety stocks, thereby increasing working-capital needs. While dual-sourcing strategies alleviate some exposure, they raise qualification costs and place smaller laboratories at a disadvantage. Consequently, although policy incentives are encouraging domestic production, near-term growth in the culture media market is dampened by cost pass-through fatigue among end users who must preserve budget flexibility for validation and capital projects.

Other drivers and restraints analyzed in the detailed report include:

- Biosimilar Manufacturing Boom Creating Bulk-Media Demand

- Adoption of Fully-Automated Media-Preparation Systems in CDMOs & Big Pharma

- Batch-to-batch Variability Hampers Regulatory Approvals for Complex Media

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dehydrated formulations accounted for 51.25% of culture media market share in 2024, anchored by long shelf life and economical freight profiles. Chromogenic alternatives, however, are accelerating at a 15.65% CAGR as automated plate-streaking systems proliferate in clinical and food-testing settings. This expansion signals laboratories' preference for pre-differentiated, color-changing substrates that shorten readout times and reduce human error. Over the forecast window, chromogenic solutions are projected to erode dehydrated incumbency, particularly in high-throughput hospital labs. Still, price sensitivity in emerging economies preserves a sizable base for dehydrated products, ensuring they remain a cornerstone of the culture media market.

Automation-friendly characteristics make chromogenic media the logical companion to total laboratory automation suites, where bar-coded plate tracking and robotic incubation demand uniform physical properties. Vendors able to supply ready-stacked, automation-compliant formats are accordingly capturing disproportionate share. Dehydrated formulations remain favored for bulk shipment into regional blending centers, allowing buyers to scale volumes without paying for hydrated weight. The contrasting value propositions sustain a mixed portfolio approach for leading suppliers that balance legacy dehydrated strengths with high-margin chromogenic innovations.

Serum-free products represented 36.32% of revenue in 2024, reflecting the regulatory push toward defined ingredients and away from bovine serum risks. Stem-cell media, the fastest-rising subset, benefits from the sector's pivot toward autologous and allogeneic therapies that require feeder-free conditions. Growth forecasts show stem-cell media climbing 15.85% CAGR through 2030 on the back of regenerative medicine trials entering late-phase studies.

The adoption of chemically defined blends in large-scale antibody and mRNA manufacturing is likewise intensifying, owing to their traceability and consistent performance. Vendor collaborations with cell-line development specialists are producing custom recipes that accelerate titer optimization, assuring deeper customer lock-in. Meanwhile, specialty and custom media tailored for unique metabolic needs of CAR-T, oncolytic viruses, or organoid cultures are commanding premium price points, widening the revenue mix inside the culture media market.

The Culture Media Market Report is Segmented by Media Type (Chromogenic Culture Media, and More), Formulation (Serum-Based Media, and More), Physical State (Liquid Media, and More), End User (Academic & Research Institutes, and More), Preparation Automation (Manual Media Preparation, and Automated Media-Preparation Systems), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.25% share of the culture media market in 2024 and is projected to expand at a 13.8% CAGR through 2030. The United States anchors regional momentum by repurposing pandemic-funded mRNA infrastructure for oncology and rare-disease pipelines, while the FDA's clear guidance on media validation sustains industry confidence. Capital deployment such as Merck KGaA's USD 290 million biosafety testing facility in Maryland and BD's syringe-capacity expansion further entrenches supplier ecosystems. Venture funding gravitates toward cell-therapy start-ups, reinforcing steady demand for high-performance, animal-component-free formulations.

Asia-Pacific is set to log the swiftest expansion at 16.45% CAGR, buoyed by national programs that treat biotechnology as a strategic sector. China's normalization of laboratory ordering patterns after COVID-19, South Korea's incentives for biosimilar production, and India's duty exemptions on bioprocessing imports all raise regional media volumes. MilliporeSigma's EUR 300 million Korean facility demonstrates multinationals' commitment to localized supply. Australian and Japanese markets, built on strong research bases and harmonized GMP frameworks, adopt high-spec stem-cell media at above-average run rates.

Europe captured 28.5% of 2024 revenue and aims for a 12.9% CAGR by 2030, with Germany, the United Kingdom, and France comprising the leading triad. Germany's Advanced Research Center in Darmstadt amplifies regional R&D in antibodies and mRNA, while the UK benefits from vaccine-cluster legacies and MHRA regulatory capacity. French initiatives for biologics innovation maintain demand continuity for serum-free and chemically defined inputs. EMA guidance that harmonizes documentation and quality requirements across member states lowers authorization hurdles for suppliers, positioning Europe as a stable yet competitive export market for culture media.

- Thermo Fisher Scientific

- Merck KGaA (MilliporeSigma)

- Sartorius

- Danaher Corp. (Cytiva)

- Lonza Group Ltd.

- Beckton Dickinson

- Corning

- Bio-Rad Laboratories

- FUJIFILM Holdings (Irvine Scientific)

- Avantor Inc.

- HiMedia Laboratories Pvt. Ltd.

- GE Healthcare

- Ajinomoto Co. Inc.

- Caisson Laboratories

- PAN-Biotech GmbH

- MP Biomedicals LLC

- KOHJIN Bio Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift from Serum-based to Animal-component-free Media

- 4.2.2 Rapid, Large-scale mRNA / Viral-vector Vaccine Capacity Expansions

- 4.2.3 Biosimilar Manufacturing Boom Creating Bulk-Media Demand

- 4.2.4 Adoption of Fully-Automated Media-Preparation Systems in CDMOs & Big Pharma

- 4.2.5 Fiscal Incentives for On-shore Bioprocessing

- 4.3 Market Restraints

- 4.3.1 Pharmaceutical-grade Raw-material Inflation & Supply-chain Fragility

- 4.3.2 Batch-to-batch Variability Hampers Regulatory Approvals for Complex Media

- 4.3.3 Global Shortage of Skilled Media-optimization Scientists

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Media Type

- 5.1.1 Chromogenic Culture Media

- 5.1.2 Dehydrated Culture Media

- 5.1.3 Prepared / Ready-to-use Culture Media

- 5.2 By Formulation

- 5.2.1 Serum-based Media

- 5.2.2 Serum-free Media

- 5.2.3 Chemically-defined Media

- 5.2.4 Stem-cell Culture Media

- 5.2.5 Specialty / Custom Media

- 5.3 By Physical State

- 5.3.1 Liquid Media

- 5.3.2 Powdered Media

- 5.3.3 Semi-solid / Gel Media

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Development & Manufacturing Organizations (CDMOs)

- 5.4.3 Academic & Research Institutes

- 5.4.4 Clinical & Diagnostic Laboratories

- 5.4.5 Food & Beverage Testing Laboratories

- 5.5 By Preparation Automation

- 5.5.1 Manual Media Preparation

- 5.5.2 Automated Media-Preparation Systems

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Company Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Merck KGaA (MilliporeSigma)

- 6.3.3 Sartorius AG

- 6.3.4 Danaher Corp. (Cytiva)

- 6.3.5 Lonza Group Ltd.

- 6.3.6 Becton, Dickinson and Company

- 6.3.7 Corning Incorporated

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 FUJIFILM Holdings (Irvine Scientific)

- 6.3.10 Avantor Inc.

- 6.3.11 HiMedia Laboratories Pvt. Ltd.

- 6.3.12 GE HealthCare

- 6.3.13 Ajinomoto Co. Inc.

- 6.3.14 Caisson Laboratories Inc.

- 6.3.15 PAN-Biotech GmbH

- 6.3.16 MP Biomedicals LLC

- 6.3.17 KOHJIN Bio Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment