|

시장보고서

상품코드

1848149

영안실 설비 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Mortuary Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

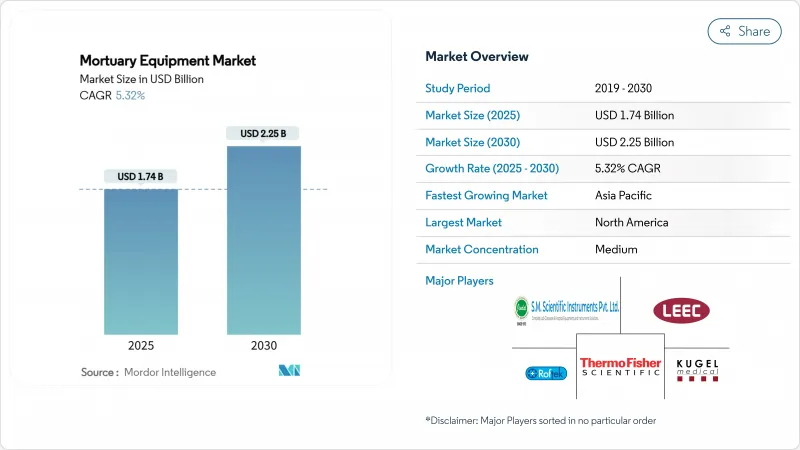

영안실 설비 시장 규모는 2025년에 17억 4,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.32%로 성장할 전망이며, 2030년에는 22억 5,000만 달러에 달할 것으로 예측됩니다.

냉동 장치에 대한 수요가 가장 강한 이유는 모든 시설이 최신 냉매 규정을 준수하는 신뢰할 수 있는 보냉고를 필요로 하기 때문입니다. 병원, 감찰의, 병리 검사실에서는 수작업을 IoT 연동 리프트 및 컨베이어 시스템으로 대체하여 처리 능력을 향상시키고 직원의 안전성을 높이기 위해 자동화의 기운이 높아지고 있습니다. 부검 인프라를 현대화하는 정부 보조금과 틈새 의료기기를 대상으로 한 미공개 주식 투자도 설비 투자를 뒷받침하고 있습니다. 스테인레스 스틸 및 냉매 공급망 변동은 제조업체가 엄격한 환경 규제를 충족하면서 비용 효율성을 높이기 위해 제품을 재설계하도록 촉구합니다. 영안실 설비 시장은 지역적인 문화적 감성에 의해 채용의 속도가 좌우되는 것, 이러한 힘을 종합하여 예측 가능한 상승궤도를 유지하고 있습니다.

세계의 영안실 설비 시장 동향 및 인사이트

고령화 및 사망률 상승

평균 수명이 연장되고 노인이 증가함에 따라 기존 시체 안치소의 인프라가 급박합니다. 아이오와 주 감찰 의국과 같은 시설은 원래 800건의 처리를 위해 건설되었지만, 2,000건을 처리하게 되었고, 새로운 부검 스테이션을 위해 3,630만 달러를 확보했습니다. 보다 광범위한 인구 통계 데이터에 따르면 미국과 유럽 국가에서도 유사한 불균형을 볼 수 있으며 관리자는 대용량 냉각 장치, 보다 견고한 리프트, 개조된 지하실에 맞는 컴팩트한 랙 등을 찾고 있습니다. 따라서 영안실 설비 시장은 재량적 자본 예산이 아니라 노후화 동향을 추적하는 예측 가능한 교환 및 확장 사이클로부터 이익을 얻고 있습니다.

시체 안치 시설의 확장 및 자동화의 필요성

병원 업그레이드 및 신설 법의학 센터에서는 IoT 모니터링을 통한 반자동 또는 완전 자동 워크플로를 지정하는 경우가 늘고 있습니다. 병리 검사실의 디지털 트윈 파일럿은 라벨링 오류를 90% 줄이고 슬라이드 품질을 최대 30% 향상시키며 센서 및 분석의 운영 가치를 증명합니다. 새로운 장비는 온도 프로브, RFID 태그가 있는 시체 트레이, 클라우드 대시 보드를 결합하여 감독자가 원격으로 상태를 모니터링 할 수 있도록 합니다. 자동화는 또한 병원 관리자가 혁신적인 리프트 및 컨베이어에 대한 설비 투자를 승인할 때 언급하는 불일치인 경험이 풍부한 영안실 기사가 후임자의 도착보다 빨리 퇴직함으로써 노동력 제약을 완화합니다. 그 결과, 영안실 설비 시장에서는 네트워크 대응 기기에 비싼 가격 설정이 이루어지고 있습니다.

고급 시스템의 높은 자본 비용 및 유지 보수 비용

몰리브덴이 2023년 1kg당 90달러에 이르자 의료용 스테인레스 스틸 가격이 급등했고 섀시와 래킹 비용이 두 자리 상승했습니다. 제조업체는 또한 2026년 2월부터 ISO 13485:2016과 일치하는 미국 FDA 품질 관리 시스템 규정의 마감일에 직면하여 감사 및 문서화 비용이 증가합니다. 이러한 배경이 정가를 밀어 올려 연간 설비 예산이 20만 달러를 넘는 일이 적은 많은 지자체의 감찰의에게 자동 영안실 카트는 손이 닿지 않는 것이 되고 있습니다. 센서가 장착된 시스템의 유지보수 계약도 수동 테이블보다 비용이 많이 들고 투자 회수 기간이 장기화됩니다. 그 결과, 일부 시설에서는 업그레이드 시기를 늦춰, 영안실 설비 시장의 단기적인 성장을 억제하고 있습니다.

부문 분석

냉동 시스템은 2024년에 영안실 설비 시장 점유율의 39.38%를 차지했는데, 이는 보편적인 보존 요구와 HFC 프리 모델에 대한 구매자를 뒷받침하는 타이트 가스 규제의 반영입니다. 냉장고와 모듈식 쿨러는 모든 자본 프로젝트의 핵심이며 이 분야는 영안실 시설 시장 규모에 가장 기여합니다. 시설의 단계적 축소 스케줄에 대한 대응, 재해 시의 서지 용량 확보를 위한 고내 증설에 수반하는 개수에 의해 성장이 계속되고 있습니다. 벤더는 보다 엄격한 온도 균일성, 탄화수소계 냉매, 컴플라이언스 대시보드에 데이터 로거 내장 등으로 차별화를 도모하고 있습니다.

시체 반송 리프트와 반송 대차는 CAGR이 가장 빠른 7.03%이지만, 이는 비만 환자가 보다 일반적이 되고, 노동자 상해 규칙이 기계적 보조를 요구하고 있기 때문입니다. OEM은 현재 정격 하중 1,000 파운드의 비만 환자용 리프트를 판매하고 있으며, 종종 혼잡한 복도에서도 안정성을 유지하는 이중 기둥 시저 설계가 되고 있습니다. 천장에 설치된 트럭 시스템과의 통합은 더욱 수작업을 줄이고, 이는 노동조합에 가입하고 있는 병원 직원에게 평가되고 있는 특징입니다. 이러한 리프트는 현재 영안실 설비 시장 규모에 차지하는 비율은 작지만, 그 급속한 보급에 의해 예측 기간 중 냉동기의 우위성은 축소될 것으로 보입니다. 쉘 빈그랙, 해부대, 엠버밍 펌프, 특수 소모품 등이 제품 믹스를 구성하고 있으며, 각각은 보다 광범위한 시설의 오버홀과 관련된 단계적인 업그레이드의 혜택을 받고 있습니다.

지역 분석

북미는 2024년 매출의 37.26%를 차지했으며, 영안실 설비 시장의 명확한 리더입니다. 강력한 공적 자금, 성숙한 민간부검 서비스 제공업체, 엄격한 OSHA 기준은 냉장실, 전동 리프트 및 스테인리스 워크스테이션에 대한 높은 기본 수요를 지원합니다. 최근 승인된 아이오와 주 3,630만 달러의 확장 공사는 주 예산이 상당한 역량 증대에 자금을 제공하고 즉각적으로 장비 주문에 연결된다는 것을 보여줍니다. 사법지원국(Bureau of Justice Assistance)을 통한 연방 보조금은 이미지 처리 시스템과 핸들링 시스템의 조달을 더욱 가속시킵니다. 그 결과, 이 지역은 높은 설치 기반에도 불구하고 5% 이상의 성장이 지속될 것으로 예측됩니다.

아시아태평양은 CAGR 7.41%로 세계 최고 속도로 확대될 것으로 예측됩니다. 중국, 인도 및 동남아시아 경제권의 의료 현대화 프로그램에는 병원의 마스터 플랜에 시체 안치소 업그레이드가 포함되어 있습니다. 일본은 윤리적 관행 및 컴플라이언스를 중시하고 시체 안치 서비스 전문화를 추진하고 있으며, 디지털 부검과 IoT 대응 쿨러를 장려하고 부문 수익을 직접 끌어올리고 있습니다. 급속한 도시화는 매장보다 화장을 추진하고, 재처리 장치를 포함한 대응 가능한 제품 범위를 확대하고 있습니다. 문화적 저항이 특정 하위 분야에 영향을 미치는 반면, 병원 건설의 대규모화와 인구 동태의 고령화로 인하여 영안실 설비 시장은 아시아태평양 전역에서 번영하고 있습니다.

유럽은 표준화된 규정을 배경으로 한 자릿수 중반의 성장을 보여줍니다. 2024/573년 F-Gas 규정은 2030년까지 구형 HFC 기반 냉동기의 교체를 강제하여 첨단 냉각기에 대한 규제적 인계를 초래했습니다. 비만이 증가함에 따라 국가의 의료 서비스도 비만 치료 리프트에 투자하고 있습니다. 공급망의 과제, 특히 스테인리스 코일의 부족이 비용 압력이 되고 있지만, 확대 계획은 좌절하지 않습니다. 라틴아메리카, 중동 및 아프리카는 기부금으로 병원 프로젝트가 현대적인 영안실을 도입하는 초기 단계의 비즈니스 기회입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인구의 고령화 및 사망률 상승

- 시체 안치 시설의 확장 및 자동화의 요구

- 법의학 및 병리학 조사 자금 증가

- 디지털 부검 워크플로우 도입

- 대용량 리프트를 필요로 하는 비만 시체 증가

- 재해 대응에 있어서 휴대용 모듈러 쿨러 수요

- 시장 성장 억제요인

- 고급 시스템의 높은 자본 비용 및 유지 비용

- 사후 처치에 관한 문화적 및 종교적 감수성

- 의료 등급 스테인레스 스틸의 불안정한 공급망

- 새로운 냉매 규격(F가스 단계적 삭감)에 의한 규제 압력

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 제품 유형별

- 냉동 유닛

- 부검대 및 워크스테이션

- 시체 리프트 및 수송 시스템

- 방부 및 보존용 기기

- 선반 및 수납 랙

- 바디백 및 소모품

- 화장 및 조직 처리 기기

- 기타 액세서리

- 기술별

- 매뉴얼

- 반자동

- 완전 자동화 및 IoT 대응

- 최종 사용자별

- 병원 및 클리닉

- 법의학 및 병리학 연구실

- 학술연구기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific Inc.

- Mopec

- LEEC Ltd

- Ferno-Washington Inc.

- KUGEL medical GmbH & Co. KG

- Mortech Manufacturing Company Inc.

- SM Scientific Instruments Pvt Ltd

- Roftek Ltd

- HYGECO

- Mortuary Lift Company

- Flexmort

- WJ Kenyon Ltd

- Frima Funeraire

- UFSK International GmbH

- Fiocchetti Scientific

- Mobi Medical Supply

- Intarcon

- Naugra Export

- Tekequipment(Aus)

- Mixta Medical

- Desco Medical India

제7장 시장 기회 및 향후 전망

AJY 25.11.03The Mortuary Equipment Market size is estimated at USD 1.74 billion in 2025, and is expected to reach USD 2.25 billion by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

Demand is strongest for refrigeration units because every facility requires reliable cold storage that complies with updated refrigerant rules. Automation momentum is visible as hospitals, medical examiners, and pathology labs replace manual handling with IoT-linked lifts and conveyor systems that raise throughput and improve staff safety. Capital spending is also encouraged by government grants that modernize autopsy infrastructure and by private-equity investment targeting niche medical devices. Supply chain volatility in stainless steel and refrigerants is pushing manufacturers to redesign products for cost efficiency while meeting stricter environmental mandates. Collectively these forces keep the mortuary equipment market on a predictable upward path, albeit one punctuated by regional cultural sensitivities that shape adoption speed.

Global Mortuary Equipment Market Trends and Insights

Aging Population and Rising Mortality Rates

Longer life expectancy coupled with larger cohorts of seniors, is straining existing morgue infrastructure. Facilities such as the Iowa Office of the State Medical Examiner-originally built for 800 cases but processing 2,000 have secured USD 36.3 million for new autopsy stations, illustrating how caseload pressure turns directly into equipment orders. Wider demographic data show a similar imbalance across U.S. and European countries, prompting administrators to seek high-capacity refrigeration, heavier-duty lifts, and compact racking that fits into retrofitted basements. The mortuary equipment market, therefore, benefits from predictable replacement and expansion cycles that track aging trends rather than discretionary capital budgets.

Expansion of Morgue Facilities and Need for Automation

Hospital upgrades and green-field forensic centers increasingly specify semi-automatic or fully automated workflows with IoT monitoring. Digital twin pilots in pathology labs cut labeling errors by 90% and improve slide quality by up to 30%, proving the operational value of sensors and analytics. New installations combine temperature probes, RFID-tagged cadaver trays, and cloud dashboards so supervisors can monitor conditions remotely. Automation also mitigates labor constraints as experienced mortuary technicians retire faster than replacements arrive, a mismatch that hospital administrators cite when approving cap-ex for innovative lifts and conveyors. Consequently, the mortuary equipment market is witnessing premium pricing for network-ready devices.

High Capital and Maintenance Costs of Advanced Systems

Medical-grade stainless steel prices spiked when molybdenum reached USD 90 per kg in 2023, lifting chassis and racking costs by double-digit percentages. Manufacturers also face the U.S. FDA Quality Management System Regulation deadline that harmonizes with ISO 13485:2016 from February 2026, adding audit and documentation expenses. These inputs push list prices upward, putting automated mortuary carts beyond the reach of many municipal coroners whose annual equipment budgets rarely exceed USD 200,000. Maintenance contracts for sensor-laden systems also cost more than manual tables, prolonging payback periods. As a result, some facilities stagger upgrades, tempering near-term growth in the mortuary equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Forensic and Pathology Research Funding Growth

- Adoption of Digital Autopsy Workflows

- Cultural and Religious Sensitivities Around Post-Mortem Practices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigeration systems retained 39.38% of mortuary equipment market share in 2024, a reflection of universal preservation needs and tighter F-Gas regulations that push buyers toward HFC-free models. Refrigerators and modular coolers anchor every capital project, making this segment the largest contributor to mortuary equipment market size. Growth continues as facilities retrofit to meet phase-down schedules and to add extra chambers for surge capacity during disasters. Vendors differentiate through tighter temperature uniformity, hydrocarbon refrigerants, and embedded data loggers that feed compliance dashboards.

Cadaver lifts and transport trolleys exhibit the fastest 7.03% CAGR because bariatric decedents are more common and worker-injury rules demand mechanical assistance. OEMs now market bariatric lifts rated to 1,000 lb, often with dual-column scissor designs that maintain stability in crowded corridors. Integration with ceiling-mounted track systems further reduces manual handling, a feature valued by unionized hospital staff. Although these lifts occupy a smaller slice of mortuary equipment market size today, their rapid adoption will trim refrigeration dominance over the forecast period. Shelving racks, autopsy tables, embalming pumps, and specialty consumables round out the product mix, each benefitting from incremental upgrades tied to broader facility overhauls.

The Mortuary Equipment Market Report is Segmented by Product Type (Refrigeration Units, Autopsy Tables & Workstations, Cadaver Lifts & Transport Systems, Embalming & Preservation Equipment, and More), Technology (Manual, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.26% of 2024 sales, making it the clear leader in the mortuary equipment market. Stronger public funding, mature private autopsy service providers, and rigorous OSHA standards underpin high baseline demand for refrigeration suites, powered lifts, and stainless workstations. The recently approved USD 36.3 million Iowa expansion illustrates how state budgets fund significant capacity additions that immediately translate into equipment orders. Federal grants through the Bureau of Justice Assistance further accelerate procurement of imaging and handling systems. As a result the region expects continued 5%-plus growth even against a high installed base.

Asia Pacific is forecast to expand at 7.41% CAGR, the fastest worldwide. Healthcare modernization programs in China, India, and Southeast Asian economies include morgue upgrades within hospital masterplans. Japan's concerted push to professionalize death-care services, emphasizing ethical practices and compliance, encourages digital autopsy and IoT-ready coolers, directly lifting segment revenues. Rapid urbanization drives cremation over burial, widening the addressable product scope to include ash-processing equipment. Although cultural resistance influences certain subsegments, the sheer scale of hospital construction and demographic aging allows the mortuary equipment market to flourish across Asia Pacific.

Europe shows mid-single-digit gains anchored by standardized regulations. The 2024/573 F-Gas rule forces the replacement of older HFC-based refrigeration by 2030, creating a regulatory pull for advanced coolers. National health services also invest in bariatric lifts as obesity prevalence rises. Supply chain challenges, especially stainless coil shortages, add cost pressures yet have not derailed expansion plans. Latin America, the Middle East, and Africa present early-stage opportunities where donor-funded hospital projects introduce modern mortuary suites; however, economic volatility and cultural factors limit the conversion of potential into immediate sales.

- Thermo Fisher Scientific

- Mopec

- LEEC Ltd

- Ferno-Washington

- KUGEL medical

- Mortech Manufacturing Company

- SM Scientific Instruments Pvt Ltd

- Roftek

- HYGECO

- Mortuary Lift Company

- Flexmort

- WJ Kenyon Ltd

- Frima Funeraire

- UFSK International GmbH

- Fiocchetti Scientific

- Mobi Medical Supply

- Intarcon

- Naugra Export

- Tekequipment (Aus)

- Mixta Medical

- Desco Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Rising Mortality Rates

- 4.2.2 Expansion of Morgue Facilities & Automation Needs

- 4.2.3 Growth in Forensic & Pathology Research Funding

- 4.2.4 Adoption of Digital Autopsy Workflows

- 4.2.5 Increase in Bariatric Cadavers Necessitating High-Capacity Lifts

- 4.2.6 Disaster-Response Demand for Portable Modular Coolers

- 4.3 Market Restraints

- 4.3.1 High Capital & Maintenance Costs of Advanced Systems

- 4.3.2 Cultural and Religious Sensitivities Around Post-Mortem Practices

- 4.3.3 Volatile Supply Chain for Medical-Grade Stainless Steel

- 4.3.4 Regulatory Pressure from New Refrigerant Standards (F-Gas Phase-Down)

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Refrigeration Units

- 5.1.2 Autopsy Tables & Workstations

- 5.1.3 Cadaver Lifts & Transport Systems

- 5.1.4 Embalming & Preservation Equipment

- 5.1.5 Shelving & Storage Racks

- 5.1.6 Body Bags & Consumables

- 5.1.7 Cremation & Tissue-Disposal Equipment

- 5.1.8 Other Accessories

- 5.2 By Technology

- 5.2.1 Manual

- 5.2.2 Semi-automatic

- 5.2.3 Fully-Automated / IoT-enabled

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Forensic & Pathology Labs

- 5.3.3 Academic & Research Institutes

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Mopec

- 6.3.3 LEEC Ltd

- 6.3.4 Ferno-Washington Inc.

- 6.3.5 KUGEL medical GmbH & Co. KG

- 6.3.6 Mortech Manufacturing Company Inc.

- 6.3.7 SM Scientific Instruments Pvt Ltd

- 6.3.8 Roftek Ltd

- 6.3.9 HYGECO

- 6.3.10 Mortuary Lift Company

- 6.3.11 Flexmort

- 6.3.12 WJ Kenyon Ltd

- 6.3.13 Frima Funeraire

- 6.3.14 UFSK International GmbH

- 6.3.15 Fiocchetti Scientific

- 6.3.16 Mobi Medical Supply

- 6.3.17 Intarcon

- 6.3.18 Naugra Export

- 6.3.19 Tekequipment (Aus)

- 6.3.20 Mixta Medical

- 6.3.21 Desco Medical India

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment