|

시장보고서

상품코드

1848155

협골 및 익골 임플란트 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Zygomatic And Pterygoid Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

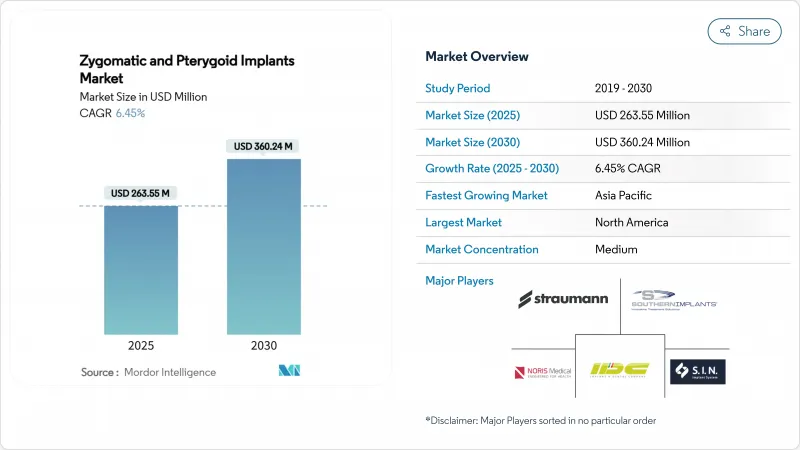

협골 및 익골 임플란트 시장 규모는 2025년 2억 6,355만 달러로 추정됩니다.

2030년에는 3억 6,024만 달러에 달할 것으로 예측되며, 예측 기간 중 CAGR 6.45%로 특수 임플란트 카테고리의 기세를 나타냅니다.

외과의사 사이에서 지속적으로 받아들여지고 있는 것, 환자의 재활이 빠른 것, 뼈 이식을 회피할 수 있는 것 등으로부터, 협골 및 익골 임플란트 시장은 복잡한 상악의 재건에 적합한 선택지로서 자리매김되고 있습니다. 즉각적인 부하가 수요의 대부분을 차지하고 디지털 워크플로우가 임베디드 정밀도를 향상시키며, 2024년 10월 FDA 지침에 의한 규제의 명확화가 신제품의 인가를 가속화하고 있습니다. 경쟁 역학은 장기적인 임상 증거와 AI 대응 네비게이션 툴과 견고한 교육 네트워크를 결합한 공급업체가 유리합니다. 새로운 재생 요법과 지속적인 비용 장벽은 확대를 억제하고 있지만, 협골 및 익골 임플란트 시장의 양호한 장기적 궤도를 상쇄하는 것은 아닙니다.

세계의 협골 및 익골 임플란트 시장 동향 및 인사이트

무치악증 및 위축성 상악골 발생률 증가

심한 상악골 결손은 전통적인 이식에 의존하는 프로토콜에서 많은 노인 증례로 충분하지 않은 것으로 밝혀졌기 때문에 특수 임플란트 수요를 계속 자극하고 있습니다. 임상경과 관찰에 의하면 위축된 상악 후부의 익상골 고정구의 성공률은 90.7%로 사이너스 리프트의 이환율을 없애고 의자 시간을 단축하고 있습니다. 인구의 고령화는 무치악증의 유병률을 높이고 있으며, 옥수수 빔을 이용한 연구에서는 120개의 위축된 아치 중 116개가 가상 익골의 임베디드에 대응할 수 있는 것으로 나타났으며, 해부학적으로 폭넓은 적용이 가능하다는 것이 검증되었습니다. 디지털 플래닝은 각도와 깊이를 매핑하여 해부학적 실현 가능성을 보완하고 수술 중 추측을 줄이며 협골 및 익골 임플란트 시장의 1차적 안정성을 높입니다. 외과의사는 치유 중단을 최소화하기 위해 그래프트리스 접근법을 강조하고 환자는 치료 주기의 단축을 평가하고 이러한 복잡한 조명기의 지속적인 흡수를 강화하고 있습니다.

확대하는 세계 노인 인구 통계

65세 이상의 인구 비율이 증가하고 있으며, 그들의 보철에 대한 기대는 저침습 치료로 진화하고 있습니다. 초 고령자를 위해 설계된 임플란트 치료는 기증자 부위의 이식 채취를 피할 수 있기 때문에 전신 위험을 줄일 수 있음이 입증되었습니다. 협골 구조는 부비동 증대술과 관련된 이환율을 피할 수 있기 때문에 치유가 위험한 노인 코호트에게 임상적으로 매력적인 치료법입니다. 디지털 워크플로우는 24시간 이내의 수복물 장착을 가능하게 함으로써 예지성을 더욱 향상시키고 있습니다. 이러한 인구 동태의 변화에 의해 협골 및 익골 임플란트 시장은 확대하는 노인 의료 경로에 따른 것으로 되어 있습니다.

높은 치료비 및 제한된 보험 적용

풀 아치 재활 비용은 60,000달러에서 90,000달러로 많은 후보자가 치료를 받는 것을 망설이는 장벽이 되고 있습니다. 미국 연방 보험 제도는 임플란트 혜택을 배제하고 있으며 메디케어 어드밴티지 플랜의 일부만 연간 1,500달러의 저액으로 부분 환불을 제공합니다. 민간 보험 회사는 '결핍 치아' 제외를 부과하고 환자는 지불 계획 및 회원제 할인 네트워크를 통해 자기 자금을 조달해야 합니다. 국민 1인당 평균 소득이 낮은 신흥국에서는 자기부담액이 크기 때문에 임상상의 이점이 있음에도 불구하고 협골 및 익골 임플란트 시장의 세계적인 성장이 억제되고 있습니다.

부문 분석

협골 픽스처는 NobelZygoma와 같은 시스템의 96.1%의 10년 생존율을 확인하는 수십년에 걸친 종단적 근거에 이어 2024년의 협골 및 익골 임플란트 시장 규모의 72.34%를 차지합니다. 이 이점은 외과 의사의 숙련도와 수술 시간을 단축하는 종합적인 장비 세트로 강화되었습니다. 그럼에도 불구하고, 날개 모양의 편성 기구는 2030년까지 8.54%의 연평균 복합 성장률(CAGR)을 기록했으며, 이는 동해부학적 구조를 우회하고 익상 돌기의 피질골을 확보하는 능력을 반영합니다. 3개의 전치부 임플란트와 2개의 익상 돌기 임플란트를 결합한 'VIV' 컨셉은 캔틸레버 힘을 줄이고 응력 분포를 넓히기 때문에 극도의 위축을 치료하는 임상의에게 매력적입니다.

디지털 기획 도구는 임플란트의 궤적과 길이를 시뮬레이션하고, 안전 마진을 향상시키며, 시술자가 해부학적 제약을 시각화하는 데 도움이 됩니다. 이 매개변수는 우수한 1차 안정성을 예측합니다. 이러한 특성은 협골 및 익골 임플란트 시장을 강화하고 두 가지 유형의 임플란트가 서로 보완하여 치료 가능한 환자층을 확대합니다.

30-50mm의 임플란트는 일반적인 상악 위축 시나리오에 적합하며 시판되는 드릴 키트에 들어가기 때문에 2024년의 협골 및 익골 임플란트 시장 점유율의 46.54%를 차지했습니다. 길이가 50mm를 초과하는 장치는 조밀한 광골 피질 또는 날개 돌기판에 고정되므로 토크 값이 증가하고 극단적인 경우에는 즉시 프로비저널화가 가능하므로 CAGR 8.67%로 가속화됩니다. 길이를 연장하면 원위 보철 장치에 가해지는 캔틸레버 응력이 더욱 감소하여 장기 안정성이 향상됩니다.

산 에칭 및 UV 활성화와 같은 표면 개질은 골아세포의 활성을 자극하여 즉각적인 하중에 필수적인 오세오 통합 속도를 향상시킵니다. 반대로, 30mm보다 짧은 임플란트는 경도에서 중등도 위축에 중점을 두고 있지만, 임상의가 보다 다목적인 중간 길이에 매료되기 때문에 채용은 여전히 완만합니다. 그 결과, 협골 및 익골 임플란트 시장에서는 다양한 해부학적 특징에 대응하는 균형 잡힌 포트폴리오가 형성됩니다.

지역 분석

북미는 2024년 42.34% 시장 점유율을 유지했습니다. 프리미엄 처치 및 훈련의 강도가 예측 가능한 결과를 요구하는 환자 수요에 부합했기 때문입니다. AI 네비게이션의 채택과 2024년 10월 FDA 지침의 엄격한 준수가 임상가의 신뢰를 뒷받침하고 있지만, Straumann은 보급 수준이 성숙에 가까워짐에 따라 임플란트 치료의 매출이 연화되고 있다고 보고했습니다. 현재는 평균 판매 가격이 높은 복잡한 재건술이 성장의 중심이 되고 있으며, 협골 및 익골 임플란트 시장은 이 지역 내에서 가치 주도권을 유지하고 있습니다.

아시아태평양은 적극적인 의료 투자, 의료 관광 인센티브, 기술 보급에 힘입어 CAGR 7.54%에서 최고의 궤도를 묘사하고 있습니다. 중국 수요가 회복되어 동남아 클리닉이 비용 효율적이면서도 정교한 의료 경로를 추진했기 때문에 스트라우먼의 2024년 1분기 기존 사업 매출은 82% 증가했습니다. 수입 승인을 가속화하는 규제 개혁은 협골 및 익골 시스템의 APAC 배치를 선호하는 제조업체를 더욱 강화합니다.

유럽은 ITI의 유럽 캠퍼스와 시장 진입을 합리화하는 CE 마킹의 조화 등 견고한 트레이닝의 틀에 힘입어 한 자리대 중반의 꾸준한 성장을 이루고 있습니다. 임상의는 잘 정비된 보험 제도를 활용하고 있지만, 일부 국가에서는 비용 억제책을 취하고 있기 때문에 일부 환자는 보다 저비용 인근 국가로 흐르고 있습니다. 라틴아메리카와 중동, 아프리카는 아직 개발 도상 시장이지만 인지도 향상과 인프라 정비가 진행되고 있으며, 협골 및 익골 임플란트 시장에 점차 기회가 확산되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 무치증 및 상악 위축증의 발생률 상승

- 확대하는 세계의 고령자 인구

- 즉각 하중 임플란트 솔루션에 대한 관심 증가

- 디지털 치과 및 수술 네비게이션의 진보

- 비용 경쟁력 있는 시장에 대한 치과 관광의 확대

- 임상 연수 및 인정 프로그램의 확충

- 시장 성장 억제요인

- 고액의 수술 비용 및 한정된 보험 적용

- 수술 후 부비동염 및 감염 위험

- 복잡한 임플란트 기술에 관한 한정된 외과의 전문 지식

- 새로운 대체 골 재생 요법

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 임플란트 유형별

- 협골 임플란트

- 익골 임플란트

- 제품 길이별

- 최대 30mm

- 30-50밀리미터

- 50mm 이상

- 처치 유형별

- 즉시 로드

- 지연 로드

- 최종 사용자별

- 병원

- 치과 진료소 및 외래수술센터(ASC)

- 용도별

- 상악동 재건술

- 심한 상악골 위축

- 기타 용도

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Straumann Holding AG

- Danaher Corp(Nobel Biocare)

- Dentsply Sirona

- Zimmer Biomet

- Southern Implants

- Noris Medical

- SIN Implant System

- Titaniumfix

- Osstem Implant

- Megagen Implant

- Neodent

- Implance

- IDC Implant & Dental Co.

- Bioline Dental Implants

- B&B Dental Implant Co.

- BioHorizons

- Zygotek Medical

- Cortex Dental Implants

- Anthogyr(Straumann)

- KeyStone Dental

제7장 시장 기회 및 향후 전망

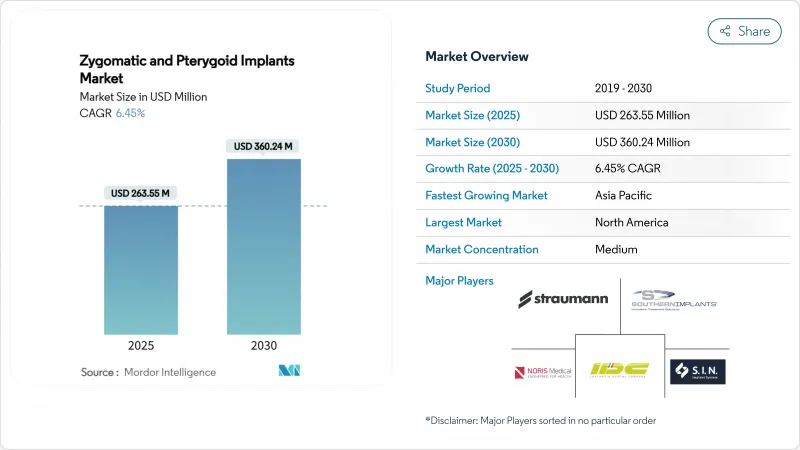

AJY 25.11.03The zygomatic & pterygoid implants market size stands at USD 263.55 million in 2025. It is forecast to reach USD 360.24 million by 2030, reflecting a 6.45% CAGR during the period and underscoring strong momentum in the specialty implant category.

Sustained acceptance among surgeons, faster patient rehabilitation, and the ability to avoid bone-grafting procedures position the Zygomatic & Pterygoid Implants market as the preferred option for complex maxillary reconstruction. Immediate loading dominates demand, digital workflows improve placement accuracy, and regulatory clarity from the October 2024 FDA guidance accelerates new product clearances. Competitive dynamics favor suppliers that combine long-term clinical evidence with AI-enabled navigation tools and robust training networks. Emerging regenerative therapies and persistent cost barriers moderate expansion yet do not offset the favorable long-term trajectory of the Zygomatic & Pterygoid Implants market.

Global Zygomatic And Pterygoid Implants Market Trends and Insights

Rising Incidence of Edentulism and Atrophic Maxilla

Severe maxillary bone loss continues to stimulate demand for specialized implants because conventional graft-dependent protocols prove inadequate in many elderly cases. Clinical follow-ups indicate 90.7% success for pterygoid fixtures in atrophic posterior maxillae, which eliminates sinus-lift morbidity and shortens chair time. Population aging intensifies the prevalence of edentulism, and cone-beam studies show that 116 of 120 examined atrophic arches can accommodate virtual pterygoid placement, validating broad anatomical applicability. Digital planning complements anatomical feasibility by mapping angulation and depth, thereby reducing intraoperative guesswork and enhancing primary stability for the Zygomatic & Pterygoid Implants market. Surgeons emphasize graftless approaches to minimize healing disruptions, and patients appreciate shorter treatment cycles, reinforcing sustained uptake of these complex fixtures.

Expanding Global Geriatric Demographics

The share of individuals above 65 years is rising, and their prosthetic expectations evolve toward minimally invasive therapy. Evidence shows implant therapies designed for ultra-aged profiles reduce systemic risk because they avoid donor-site graft harvesting. Zygomatic constructs sidestep the morbidity linked with sinus augmentation, making them clinically attractive for elderly cohorts with compromised healing. Digital workflows further enhance predictability by enabling restorative loading within 24 hours, as validated by immediate protocols that restore mastication and speech on the same day. These demographic shifts ensure that the Zygomatic & Pterygoid Implants market remains aligned with expanding geriatric care pathways.

High Procedure Cost and Limited Insurance Coverage

Full-arch rehabilitation costs range from USD 60,000 to USD 90,000, a barrier that deters many candidates from seeking care. U.S. federal insurance programs exclude implant benefits, and only a subset of Medicare Advantage plans provide partial reimbursement with annual caps as low as USD 1,500. Private carriers impose "missing-tooth" exclusions, obligating patients to self-finance via payment plans or membership-based discount networks. Out-of-pocket liabilities slow uptake in emerging economies where average per-capita income is lower, thereby restraining global growth for the Zygomatic & Pterygoid Implants market despite clinical advantages.

Other drivers and restraints analyzed in the detailed report include:

- Growing Preference for Immediate-Loading Implant Solutions

- Advances in Digital Dentistry and Surgical Navigation

- Postoperative Sinusitis and Infection Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zygomatic fixtures delivered 72.34% of the 2024 Zygomatic & Pterygoid Implants market size following decades of longitudinal evidence that confirms 96.1% ten-year survival for systems such as NobelZygoma. This dominance is reinforced by surgeon familiarity and comprehensive instrumentation sets that shorten operating time. Nonetheless, pterygoid devices post an 8.54% CAGR to 2030, reflecting their ability to bypass sinus anatomy and secure cortical bone in the pterygoid process. The "VIV" concept, which combines three anterior with two pterygoid implants, reduces cantilever forces and widens stress distribution, thus appealing to clinicians treating extreme atrophy.

Digital planning tools simulate implant trajectory and length, improving safety margins and helping practitioners visualize anatomical constraints. Studies reveal 7.1 mm average bone engagement beyond the pterygoid junction, a parameter that predicts superior primary stability. Together, these attributes strengthen the Zygomatic & Pterygoid Implants market, where both implant types complement each other to broaden the treatable patient population.

Implants measuring 30-50 mm held 46.54% Zygomatic & Pterygoid Implants market share during 2024 because they suit common maxillary atrophy scenarios and fit within commercially available drill kits. Devices exceeding 50 mm length accelerate at an 8.67% CAGR because they anchor into dense zygomatic cortex or pterygoid plates, increasing torque values and allowing immediate provisionalization in extreme cases. Extended lengths further decrease cantilever stress on distal prosthetic units, thereby boosting long-term stability.

Surface modifications, including acid etching and UV activation, stimulate osteoblast activity and improve osseointegration speed, which is critical for immediate loading. Conversely, implants shorter than 30 mm focus on mild to moderate atrophy, but their adoption remains slower as clinicians gravitate toward more versatile intermediate lengths. The result is a balanced portfolio within the Zygomatic & Pterygoid Implants market that caters to varying anatomical presentations.

The Zygomatic & Pterygoid Implants Market Report is Segmented by Implant Type (Zygomatic Implants, and More), Product Length (Up To 30 Mm, and More), Procedure Type (Immediate Loading, and More), End User (Hospitals, and More), Application (Maxillary Sinus Reconstruction, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.34% market share in 2024 as premium procedures and training intensity aligned to patient demand for predictable outcomes. Adoption of AI navigation and strict adherence to the October 2024 FDA guidance sustain clinician confidence, although Straumann reported soft implantology sales as penetration levels approach maturity. Growth now centers on complex reconstructions that carry higher average selling prices, ensuring the Zygomatic & Pterygoid Implants market maintains value leadership within the region.

Asia-Pacific posts the highest trajectory at a 7.54% CAGR, buoyed by aggressive health-care investments, medical-tourism incentives, and technological diffusion. Straumann logged 82% organic sales growth in Q1 2024 as Chinese demand recovered and Southeast Asian clinics promoted cost-effective yet sophisticated care pathways. Regulatory reforms that expedite import approvals further encourage manufacturers to prioritize APAC rollouts of zygomatic and pterygoid systems.

Europe delivers steady mid-single-digit growth supported by robust training frameworks such as ITI's European Campus and harmonized CE marking that streamlines market entry. Clinicians leverage well-developed insurance schemes, although cost containment measures in certain countries nudge some patients toward neighboring lower-cost destinations. Latin America and the Middle East & Africa remain nascent markets but display increasing awareness and incremental infrastructure upgrades that unlock gradual opportunities for the Zygomatic & Pterygoid Implants market.

- Straumann Group

- Danaher Corp (Nobel Biocare)

- Dentsply Sirona

- Zimmer Biomet

- Southern Implants

- Noris Medical

- S.I.N. Implant System

- Titaniumfix

- Osstem Implant

- Megagen Implant

- Neodent

- Implance

- IDC Implant & Dental Co.

- Bioline Dental Implants

- B&B Dental Implant Co.

- BioHorizons

- Zygotek Medical

- Cortex Dental Implants

- Anthogyr (Straumann)

- KeyStone Dental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Edentulism And Atrophic Maxilla

- 4.2.2 Expanding Global Geriatric Demographics

- 4.2.3 Growing Preference for Immediate-Loading Implant Solutions

- 4.2.4 Advances in Digital Dentistry and Surgical Navigation

- 4.2.5 Increasing Dental Tourism to Cost-Competitive Markets

- 4.2.6 Expanded Clinical Training and Certification Programs

- 4.3 Market Restraints

- 4.3.1 High Procedure Cost and Limited Insurance Coverage

- 4.3.2 Postoperative Sinusitis and Infection Risks

- 4.3.3 Limited Surgeon Expertise in Complex Implant Techniques

- 4.3.4 Emerging Alternative Bone Regeneration Therapies

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitute Products

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Implant Type

- 5.1.1 Zygomatic Implants

- 5.1.2 Pterygoid Implants

- 5.2 By Product Length

- 5.2.1 Up To 30 mm

- 5.2.2 30 - 50 mm

- 5.2.3 Above 50 mm

- 5.3 By Procedure Type

- 5.3.1 Immediate Loading

- 5.3.2 Delayed Loading

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Dental Clinics & Ambulatory Surgical Centers

- 5.5 By Application

- 5.5.1 Maxillary Sinus Reconstruction

- 5.5.2 Severe Maxillary Bone Atrophy

- 5.5.3 Other Applications

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Straumann Holding AG

- 6.3.2 Danaher Corp (Nobel Biocare)

- 6.3.3 Dentsply Sirona

- 6.3.4 Zimmer Biomet

- 6.3.5 Southern Implants

- 6.3.6 Noris Medical

- 6.3.7 S.I.N. Implant System

- 6.3.8 Titaniumfix

- 6.3.9 Osstem Implant

- 6.3.10 Megagen Implant

- 6.3.11 Neodent

- 6.3.12 Implance

- 6.3.13 IDC Implant & Dental Co.

- 6.3.14 Bioline Dental Implants

- 6.3.15 B&B Dental Implant Co.

- 6.3.16 BioHorizons

- 6.3.17 Zygotek Medical

- 6.3.18 Cortex Dental Implants

- 6.3.19 Anthogyr (Straumann)

- 6.3.20 KeyStone Dental

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment