|

시장보고서

상품코드

1910660

소아 헬스케어 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pediatric Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

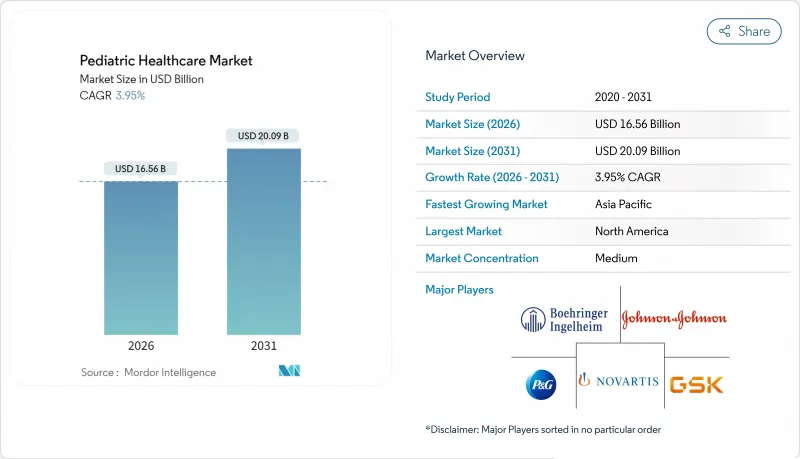

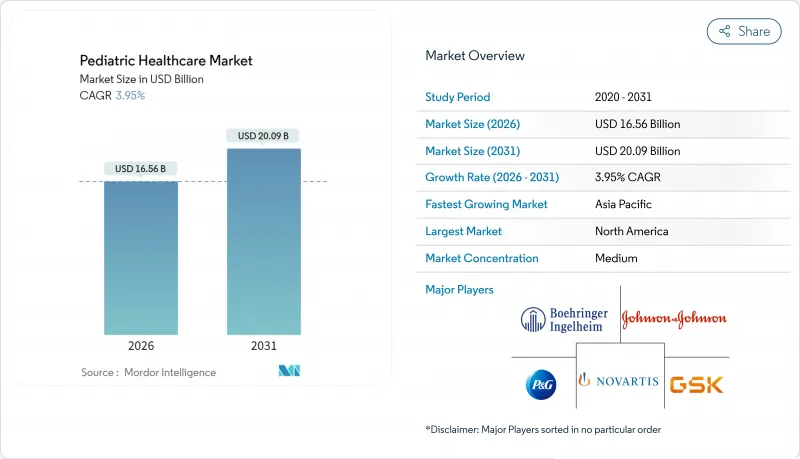

세계의 소아 헬스케어 시장 규모는 2026년 165억 6,000만 달러로 추정되며, 2025년 159억 3,000만 달러에서 성장을 이어갑니다. 2031년에는 200억 9,000만 달러에 달할 전망으로, 2026년부터 2031년까지 CAGR 3.95%로 확대될 것으로 예측되고 있습니다.

정기 예방 접종에 대한 강한 수요, 유전자 치료의 신속한 승인, 진단 이미지에서 인공지능의 활용 확대가 소아 헬스케어 시장의 현재 성장 궤도를 지원합니다. 시장 진출기업은 디지털 툴을 포트폴리오에 추가하고, 병원 통합을 추진하고, 원격 의료 확대를 위해 학교와 제휴하는 등 경쟁 전략을 형성하고 있습니다. 수입품에 비해 최대 70% 저가의 신생아 집중치료기기는 개발 도상 지역에서의 접근성 향상과 현지 생산 촉진에 기여하고 있습니다. 동시에 연간 250억 달러의 부담이 되는 호흡기 세포 융합 바이러스(RSV)의 유행 재발은 백신과 항바이러스제 수요를 뒷받침하고 있습니다.

세계의 소아 헬스케어 시장 동향과 통찰

정기 소아 예방접종 예산 급증

공중 보건 예산의 확대로, 특히 소아 사망률이 높은 아시아태평양에서 새로운 백신 라인이 추가되고 공급망이 강화되고 있습니다. 현재 국가 프로그램은 접종 횟수를 추적하고 비접종 스케줄을 통지하는 디지털 등록 시스템을 통합하여 접종률 향상에 기여하고 있습니다. 제약기업은 조달량 증가에 의해 제조 예측이 안정되고 진입 장벽이 높아지는 혜택을 받고 있습니다. 콜드체인 전문업체, 데이터 분석 벤더, 물류 제공업체도 가치를 얻고 있습니다. 훈련, 보관, 이동 클리닉의 전개에 이르는 시너지 효과로 소아 의료 시장은 탄력적인 성장 기반으로 강화되고 있습니다.

희귀질환 유전자 치료 승인 확대

미국과 유럽의 규제 당국은 이염성 백질이용양증, 뒤센형 근이영양증, 방향족 L-아미노산 탈탄산 효소 결핍에 대한 근치적 치료를 승인하고 새로운 임상 기준을 수립했습니다. Casgevy와 Lyfgenia는 겸상 적혈구증에 대한 최초의 CRISPR 기반 치료법이었고, 대부분의 사춘기 환자에서 발작이 없는 치료 결과를 가져왔습니다. 가격이 200만 달러를 넘지만, 지불 기관은 예산에 미치는 영향을 상쇄하기 위해 마일스톤 기반 계약을 시도하고 있습니다. 소아 독점권 프로그램에 따른 특허 기간 연장은 바이오 의약품 투자를 더욱 유인합니다. 예측 기간 동안 아시아태평양의 신규 신청은 접근을 확대하고 소아 헬스케어 시장을 밀어 올릴 것입니다.

소아의 항균제 내성 증가

다제 내성 패혈증은 미국에서 연간 380억 달러의 추가 비용을 발생시키고 소아 입원 기간을 연장하고 있습니다. 소아는 더 많은 항생제를 소비하므로 내성 사이클이 가속화됩니다. 스튜어드십 프로그램은 3차 의료기관에서의 처방 개선에 기여하고 있지만, 지방 진료소에서는 여전히 불충분한 상황입니다. 소아 전용 항생제의 파이프라인 부족은 임상 위험을 증가시키고 있습니다. 정책 인센티브나 공동 조달 없이는 내성균의 확대가 소아 의료 시장에서 항감염제 포트폴리오 전체의 수익 확대를 억제할 것입니다.

부문 분석

의약품 부문은 필수 백신과 만성 질환 치료제를 배경으로 2025년 의료 시장 점유율의 46.21%를 차지했습니다. 브랜드 의약품은 특허 연장의 혜택을 받는 반면 제네릭 의약품은 공공 프로그램의 수량 수요를 지원합니다. 디지털 헬스 솔루션은 4.17%의 연평균 복합 성장률(CAGR)로 다른 카테고리를 뛰어넘는 성장이 예상됩니다. 원격 모니터링 앱, 증상 검사기, 복약 관리 봇은 파일럿 코호트에서 응급 진찰을 42% 줄였습니다.

증가하는 벤처 자금은 행동 건강 모듈, 영양 지도, 예방 접종 알림을 통합한 소아 의료 특화 플랫폼을 지원하여 가족의 정착률 향상에 기여하고 있습니다. 상환 코드가 확대됨에 따라 디지털 도구의 소아 의료 시장 규모는 더욱 확대될 것으로 예측됩니다. 의료기기는 의약품에 이어 수익 규모이면서 소아 적응 표시의 제한에 의해 고전하고 있으며 임상 의사가 성인용 기기를 전용하는 사례가 증가했습니다. 이 관행은 규제 당국의 감시 대상입니다. 업계 관계자는 장비 승인 가속으로 인해 조화된 기준을 수립하고 있습니다.

2025년 시점의 소아 헬스케어 시장에서 감염증 분야는 27.94%의 최대 수익원을 유지해 RSV, 인플루엔자, 소화기 질환의 지속적인 부담을 부조하고 있습니다. 종합적인 백신 접종 일정과 항균제 병용 요법이 기초 수요를 지원합니다. 종양학 분야는 표적 요법과 유전자 편집 기술의 진전에 의해 4.45%라는 가장 빠른 CAGR을 나타내고 있습니다.

정밀의료 시험에서는 종양 유전학과 저분자 억제제를 조합하여 생존율 향상과 고가격 설정을 지원하고 있습니다. 신경질환 분야에서는 병변 매핑을 정밀화하는 AI 구동형 이미징 툴이 주목되고, 순환기 분야에서는 소아 혈관 구조에 맞춘 용해성 스텐트가 시험 중입니다. 다양화된 개발 파이프라인은 소아 헬스케어 시장을 강화하고 단일 치료 분야에 대한 의존도를 줄이고 있습니다.

이 보고서는 세계 소아 헬스케어 시장 점유율과 분석을 다룹니다. 시장은 유형별(만성질환, 급성질환), 치료법별(백신, 의약품, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)으로 분류되어 있습니다. 보고서는 위 부문 시장 규모(단위 : 백만 달러)를 제공합니다.

지역별 분석

북미는 2025년 세계 수익의 33.88%를 차지했습니다. 이는 고급 보험 적용 범위, 전문의 밀도, 조기 기술 도입이 지출을 지원하기 때문입니다. 그러나 200만명의 어린이가 중요한 전문의로부터 80마일 이상 떨어진 지역에 거주하고 있으며, 원격 의료 보조금이나 이동 진료 프로그램의 도입을 촉구하고 있습니다. 유전자 치료의 진전과 병원 합병이 전략적 재편을 추진하는 한편, 방사선 의학 분야에서의 AI 도입은 학술 기관에서 지역 화상 진단 시설로 확대되고 있습니다. 민간 협력에 의한 지방 광대역 네트워크와 진단 거점에 대한 투자는 소아 헬스케어 시장의 확대에 기여하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 6.05%를 보일 것으로 예측됩니다. 급속한 도시화로 소득과 보험 가입률이 상승하는 한편, 각국 정부는 2027년까지 병원 건설과 설비 갱신에 1,380억 달러를 예산화하고 있습니다. 중국은 소아용 의약품의 임상시험 건수로 세계를 선도하고 지역 수요에 부응하기 위해 제조 규모를 확대 중입니다. 인도의 신생 기업은 공립 병원에서 채용되는 비용 효율적인 신생아 장비를 개발하고 있습니다. 규제심사기간의 지역적인 조화에 의해 상시사이클이 단축되고, 소아헬스케어 시장에서의 수익 획득이 가속하고 있습니다.

유럽에서는 전국민 보험 제도와 희귀질환 대책의 제휴 체제를 배경으로, 안정된 5% 전후의 성장을 유지하고 있습니다. 공동조달로 백신가격은 하락하고 있지만 출생률 저하로 수량 성장은 완만합니다. 남미 및 중동 및 아프리카에서는 소규모 기반에서 두 자릿수 성장을 기록하는 신흥 생태계가 형성됩니다. 현지 정부는 NGO와 협력하여 이동 진료소와 모자 보건 캠페인을 전개함으로써 소아 의료 시장에 대한 접근을 확대하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정기 소아 예방접종 자금의 급격한 증가

- 희귀질환 유전자 치료 승인 확대

- AI 지원 소아 방사선 진단의 도입 상황

- RSV 및 기타 호흡기 감염의 재유행

- 학교 기반 원격 의료 도입(주목도 낮음)

- 소아 대상 마이크로호스피탈 형태(주목도 낮음)

- 시장 성장 억제요인

- 소아의 항균제 내성 증가

- 소아 전용 의료기기의 상환 제도에 존재하는 격차

- mRNA 백신의 장기 안전성 데이터 부족(주목도 낮음)

- 저소득 지역에서의 소아 전문의 부족(주목도 낮음)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 의약품

- 의료기기

- 디지털 건강 솔루션

- 소아 의료 서비스

- 치혀 영역별

- 감염증

- 호흡기 질환

- 신경질환

- 심혈관 질환

- 종양학

- 기타

- 연령층별

- 신생아(0-28일)

- 유아(1-23개월)

- 소아(2-11세)

- 사춘기(12-18세)

- 케어 환경별

- 병원

- 진료소

- 재택치료

- 원격 의료

- 최종 사용자별

- 공공 의료기관

- 민간 의료 제공자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Pfizer Inc.

- Johnson & Johnson

- GlaxoSmithKline plc

- Merck & Co., Inc.

- Sanofi SA

- Novartis AG

- F. Hoffmann-La Roche Ltd

- AstraZeneca plc

- Abbott Laboratories

- Medtronic plc

- Boston Children's Hospital

- Koninklijke Philips NV

- GE HealthCare Technologies Inc.

- Oracle Corporation

- Teladoc Health, Inc.

- Fresenius Medical Care AG & Co. KGaA

- Cardinal Health, Inc.

- Siemens Healthineers AG

- Takeda Pharmaceutical Company Ltd.

- Dr. Reddy's Laboratories Ltd.

제7장 시장 기회와 미래 전망

SHW 26.01.26The pediatric healthcare market size in 2026 is estimated at USD 16.56 billion, growing from 2025 value of USD 15.93 billion with 2031 projections showing USD 20.09 billion, growing at 3.95% CAGR over 2026-2031.

Strong demand for routine immunizations, rapid gene-therapy approvals, and the rising use of artificial intelligence in diagnostic imaging anchor the current growth trajectory of the pediatric healthcare market. Market participants add digital tools to their portfolios, pursue hospital consolidation, and partner with schools to expand telehealth, all of which shape competitive strategies. Newborn-critical-care equipment priced up to 70% below imported alternatives improves access in developing regions and drives localized manufacturing. At the same time, the resurgence of respiratory syncytial virus (RSV) outbreaks, a USD 25 billion annual burden across age groups, fuels demand for vaccines and antivirals.

Global Pediatric Healthcare Market Trends and Insights

Rapid Uptick in Routine Pediatric Immunization Funding

Expanded public-health budgets add new vaccine lines and strengthen supply chains, particularly in Asia-Pacific where child mortality remains high. National programs now integrate digital registries that track doses and flag missed schedules, improving coverage rates. Pharmaceutical firms benefit from larger procurement volumes that stabilize manufacturing forecasts and raise barriers to entry. Cold-chain specialists, data-analytics vendors, and logistics providers also capture value. Multiplier effects span training, storage, and mobile-clinic deployment, reinforcing the pediatric healthcare market as a resilient growth platform.

Expansion of Rare-Disease Gene-Therapy Approvals

U.S. and European regulators authorized curative treatments for metachromatic leukodystrophy, Duchenne muscular dystrophy, and aromatic L-amino acid decarboxylase deficiency, setting new clinical benchmarks. Casgevy and Lyfgenia became the first CRISPR-based therapies for sickle-cell disease, delivering crisis-free outcomes in most adolescents. Although price tags exceed USD 2 million, payers trial milestone-based contracts to offset budget impact. Patent-term extensions under the pediatric exclusivity program further attract biopharma investment. Over the forecast horizon, new submissions in Asia-Pacific will widen access and lift the pediatric healthcare market.

Rising Antimicrobial Resistance in Children

Multidrug-resistant sepsis adds USD 38 billion to U.S. costs each year and lengthens pediatric hospital stays. Children consume higher antibiotic volumes, accelerating resistance cycles. Stewardship programs improve prescribing in tertiary centers yet remain patchy in rural clinics. Pipeline scarcity for child-specific antibiotics heightens clinical risks. Without policy incentives or pooled procurement, resistance will temper revenue expansion across anti-infective portfolios within the pediatric healthcare market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Pediatric Radiology Adoption

- Re-Emergence of RSV & Other Respiratory Outbreaks

- Gap in Pediatric-Specific Device Reimbursement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The pharmaceuticals segment captured 46.21% of pediatric healthcare market share in 2025 on the back of essential vaccines and chronic-disease therapies. Branded formulations benefit from patent extensions, while generics sustain volume demand in public programs. Digital health solutions are forecast to outpace other categories at 4.17% CAGR. Remote-monitoring apps, symptom checkers, and medication-adherence bots cut emergency visits by 42% in pilot cohorts.

Growing venture funding supports pediatric-centric platforms that integrate behavioral-health modules, nutrition coaching, and immunization reminders, making them stickier for families. The pediatric healthcare market size for digital tools is projected to expand further as reimbursement codes widen. Medical devices follow pharmaceuticals in revenue but struggle with limited pediatric labeling, prompting clinicians to repurpose adult hardware, a practice that attracts regulatory scrutiny. Pediatric healthcare industry advocates push for harmonized standards to accelerate device approvals.

Infectious diseases remained the largest revenue pool at 27.94% of pediatric healthcare market size during 2025, underlining persistent RSV, influenza, and gastrointestinal burdens. Comprehensive vaccine schedules and antimicrobial combinations sustain baseline demand. Oncology exhibits the fastest CAGR at 4.45%, fueled by targeted therapies and gene-editing breakthroughs.

Precision-medicine trials match tumor genetics with small-molecule inhibitors, lifting survival rates and supporting premium pricing. Neurological disorders attract AI-driven imaging tools that refine lesion mapping, while cardiovascular applications test dissolvable stents calibrated for pediatric vasculature. The diversified pipeline strengthens the pediatric healthcare market and mitigates reliance on any single therapy class.

The Report Covers Global Pediatric Healthcare Market Share & Analysis. The Market is Segmented by Type (Chronic Illness and Acute Illness), Treatment (Vaccines, Drugs, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (in USD Million) for the Above Segments.

Geography Analysis

North America contributed 33.88% to global revenue in 2025 as advanced insurance coverage, specialist density, and early technology adoption underpin spending. Nevertheless, 2 million children reside more than 80 miles from vital subspecialists, prompting telehealth grants and mobile-clinic programs. Gene-therapy accelerations and hospital mergers drive strategic realignment, while AI adoption in radiology spreads from academic centers to community imaging sites. Public-private partnerships invest in rural broadband and diagnostic hubs, extending the pediatric healthcare market footprint.

Asia-Pacific is projected to log 6.05% CAGR through 2031. Rapid urbanization raises income and insurance penetration, while governments budget USD 138 billion for hospital construction and equipment upgrades by 2027. China leads clinical-trial volume for pediatric drugs, upscaling manufacturing to serve regional demand. Indian start-ups develop cost-effective neonatal equipment adopted by public hospitals. Regional harmonization of regulatory review times shortens launch cycles, accelerating revenue capture within the pediatric healthcare market.

Europe maintains steady mid-single-digit growth backed by universal coverage and coordinated rare-disease frameworks. Joint procurement lowers vaccine prices, yet declining birth rates moderate volume growth. Emerging ecosystems in South America and Middle East & Africa record double-digit growth off smaller bases. Governments there partner with NGOs to deploy mobile clinics and maternal-child health campaigns, enlarging access to the pediatric healthcare market.

- Pfizer

- Johnson & Johnson

- GlaxoSmithKline

- Merck

- Sanofi

- Novartis

- Roche

- AstraZeneca

- Abbott Laboratories

- Medtronic

- Boston Children's Hospital

- Koninklijke Philips

- GE HealthCare Technologies Inc.

- Oracle

- Teladoc Health

- Fresenius

- Cardinal Health

- Siemens Healthineers

- Takeda Pharmaceuticals

- Dr. Reddy's Laboratories Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid uptick in routine pediatric immunization funding

- 4.2.2 Expansion of rare-disease gene-therapy approvals

- 4.2.3 AI-assisted pediatric radiology adoption

- 4.2.4 Re-emergence of RSV & other respiratory outbreaks

- 4.2.5 School-based tele-health roll-outs (under-the-radar)

- 4.2.6 Micro-hospital formats targeting children (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Rising antimicrobial-resistance in children

- 4.3.2 Gap in pediatric-specific device reimbursement

- 4.3.3 Dearth of long-term safety data for mRNA vaccines (under-the-radar)

- 4.3.4 Shortage of pediatric subspecialists in low-income regions (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 Pharmaceuticals

- 5.1.2 Medical Devices

- 5.1.3 Digital Health Solutions

- 5.1.4 Pediatric Services

- 5.2 By Therapeutic Area

- 5.2.1 Infectious Diseases

- 5.2.2 Respiratory Disorders

- 5.2.3 Neurological Disorders

- 5.2.4 Cardiovascular Disorders

- 5.2.5 Oncology

- 5.2.6 Others

- 5.3 By Age Group

- 5.3.1 Neonates (0-28 days)

- 5.3.2 Infants (1-23 months)

- 5.3.3 Children (2-11 years)

- 5.3.4 Adolescents (12-18 years)

- 5.4 By Care Setting

- 5.4.1 Hospitals

- 5.4.2 Clinics

- 5.4.3 Homecare

- 5.4.4 Telehealth

- 5.5 By End User

- 5.5.1 Public Healthcare Providers

- 5.5.2 Private Healthcare Providers

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Pfizer Inc.

- 6.3.2 Johnson & Johnson

- 6.3.3 GlaxoSmithKline plc

- 6.3.4 Merck & Co., Inc.

- 6.3.5 Sanofi S.A.

- 6.3.6 Novartis AG

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 AstraZeneca plc

- 6.3.9 Abbott Laboratories

- 6.3.10 Medtronic plc

- 6.3.11 Boston Children's Hospital

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 GE HealthCare Technologies Inc.

- 6.3.14 Oracle Corporation

- 6.3.15 Teladoc Health, Inc.

- 6.3.16 Fresenius Medical Care AG & Co. KGaA

- 6.3.17 Cardinal Health, Inc.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Takeda Pharmaceutical Company Ltd.

- 6.3.20 Dr. Reddy's Laboratories Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment